AGG - PCN: A Very Good Bond Fund With A Sustainable Yield But Price Is Way Too High

2023-04-19 16:51:37 ET

Summary

- Investors today are desperately in need of additional sources of income due to the rapidly rising cost of living.

- PIMCO Corporate & Income Strategy Fund invests primarily in a bond portfolio that seeks to provide investors with a high level of current income.

- The PCN closed-end fund has a long history of beating the broad bond market indices, which likely explains some of its popularity.

- The fund's distribution has been remarkably consistent over the years, and PCN appears that it can maintain its current 10.71% yield.

- The PCN CEF is trading at a substantial premium to the net asset value, so it may be a good idea to wait and see if the price improves.

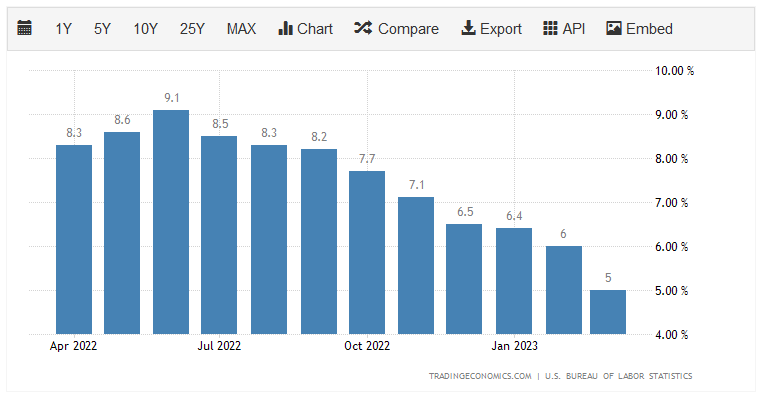

It is unlikely to be a surprise to anyone that one of the biggest problems facing the average American today is the incredibly high inflation rate that has dominated the economy. This is evident by looking at the consumer price index, which has increased by at least 6% in eleven of the past twelve months:

{kind=link}

Although we have seen a bit of a decline in recent weeks, as I pointed out in a blog post earlier today, this trend could reverse in the near future due to rising energy prices. Regardless, this high level of inflation has had a devastating effect on the finances of many American families, particularly those of lesser means. This has caused people to take on second jobs or enter the gig economy just to keep themselves fed and their homes heated. In short, people are desperate for any source of income that they can find just to get by in the current environment.

As investors, we are definitely not immune to this problem, but we do have other options available to us beyond working more hours or coming out of retirement. After all, we can put our money to work for us in order to earn an income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well followed in the investment media, and most financial advisors are not familiar with them, so it can be difficult to learn about them. That is unfortunate, as these funds provide easy access to a diversified, professionally-managed portfolio that can usually provide a higher yield than any of the underlying assets actually possess.

In this article, we will discuss the PIMCO Corporate & Income Strategy Fund ( PCN ), which is a CEF that can be used to put your money to work. This fund boasts a very impressive 10.71% yield as of the time of writing, so it is certainly no slouch when it comes to delivering on this promise. I have discussed this fund before, but a few months have passed since that time so naturally some things have changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund's finances. Let us investigate and see if this PIMCO closed-end fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the PIMCO Corporate & Income Strategy Fund has the stated objective of providing its investors with a high level of current income while preserving the value of its principal. This is hardly surprising considering that this is a PIMCO fund and PIMCO is widely renowned as a fixed-income fund house. As might be expected, the fund is a bond fund, although it does have a small amount of common and preferred stock included in the portfolio:

CEF Connect

As a general rule, bond funds focus on current income because this is how bonds deliver the majority of their returns. After all, a bond is just a certificate of indebtedness that states that a company owes an investor a certain amount of money. The company makes regular payments to the bondholder and then pays off the loan on a specific date. The security has no inherent link to the growth and prosperity of the issuing company as a borrower will not increase the increase rate that it pays to its creditors just because its income increases. Can you imagine what it would be like if your mortgage payment worked that way? As such, a bond's potential to deliver capital gains to its investors is limited.

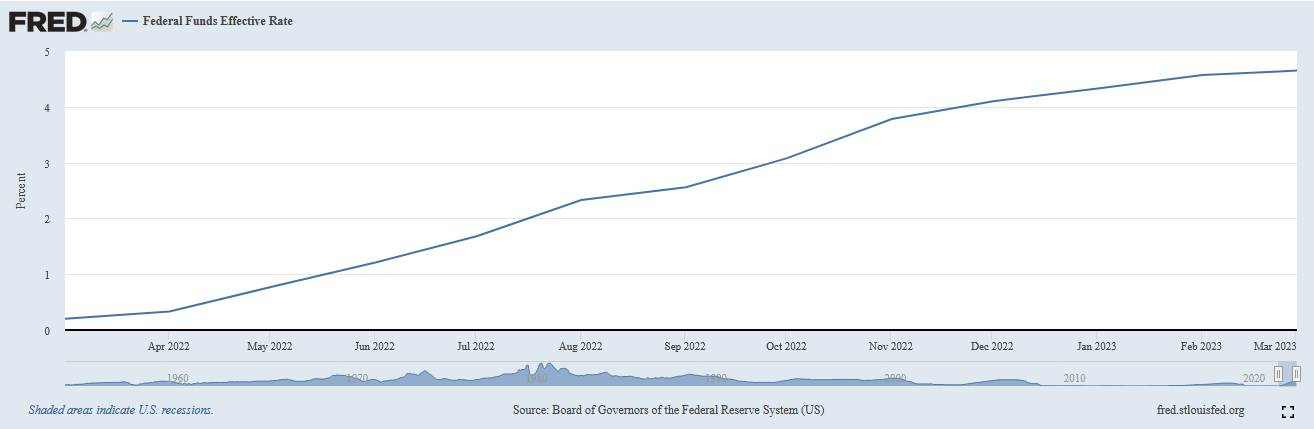

With that said, a bond's price does vary with interest rates, and this offers it the potential to deliver capital gains to an investor. It is an inverse correlation, so when the market interest rate goes up, bond prices go down. The reverse is also true. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates over the past year. We can see this quite clearly by looking at the federal funds rate, which is the rate at which the nation's commercial banks lend money to each other in the overnight market. In March 2020, the effective federal funds rate was 0.20% but today it is 4.65%:

{kind=link}

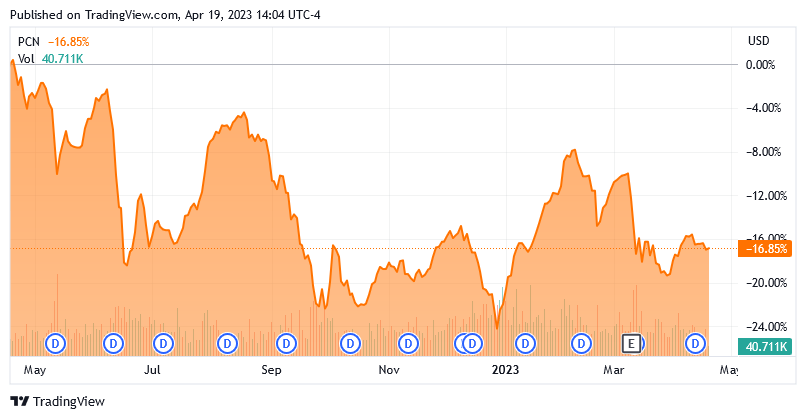

Given the relationship that we just discussed between interest rates and bond prices, we can logically assume that this event would cause bond prices to decline. That should reflect itself in the price of this fund since its shares should decline in price when the value of its assets declines. That has certainly been the case. Over the past twelve months, the PIMCO Corporate & Income Strategy Fund has declined by 16.85%:

{kind=link}

The reason for this is that newly issued bonds will have a yield that corresponds to the market interest rate at the time of issuance. Thus, a $1,000 bond that is issued today has a higher interest rate than a $1,000 bond that was issued a year ago. Therefore, there is no reason for anyone to purchase the older bond when they could buy the brand-new one and make more money. In order to compensate for this, the old bond must decline in price in order to deliver a competitive yield to a buyer.

This would not be a problem if the fund simply bought bonds and then held them to maturity. After all, bonds always pay out their face value when they mature so an investor is guaranteed not to lose money over the life of the bond unless the issuing entity goes bankrupt. However, PIMCO funds have a tendency to trade bonds in an attempt to obtain capital gains and in the process generate higher returns. This one is no exception to that, as its 47.00% annual turnover rate is higher than many other fixed-income funds. The reason that this is important is that it costs money to trade bonds or other assets. These expenses are billed directly to the shareholders and thus create a drag on the fund's performance. After all, the fund's management needs to generate returns that are sufficient to cover these added expenses and still give the shareholders an acceptable return.

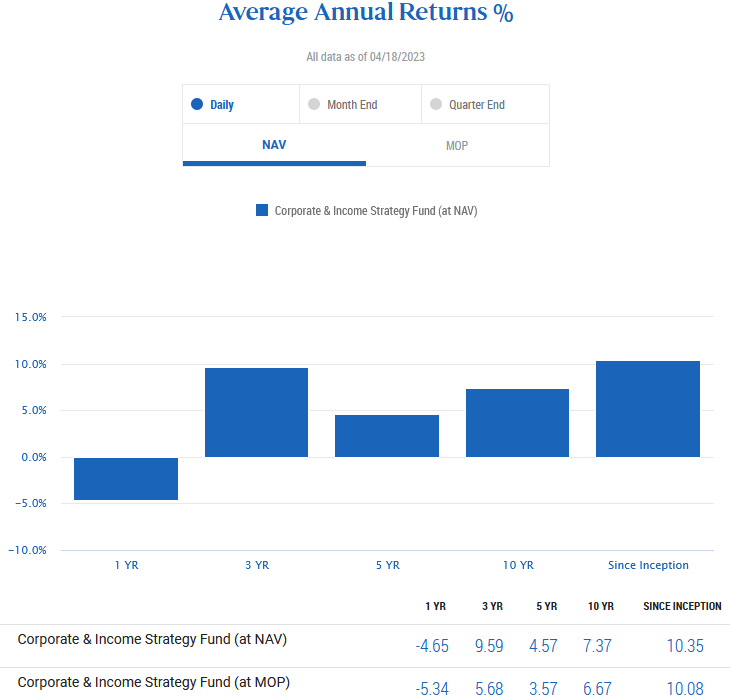

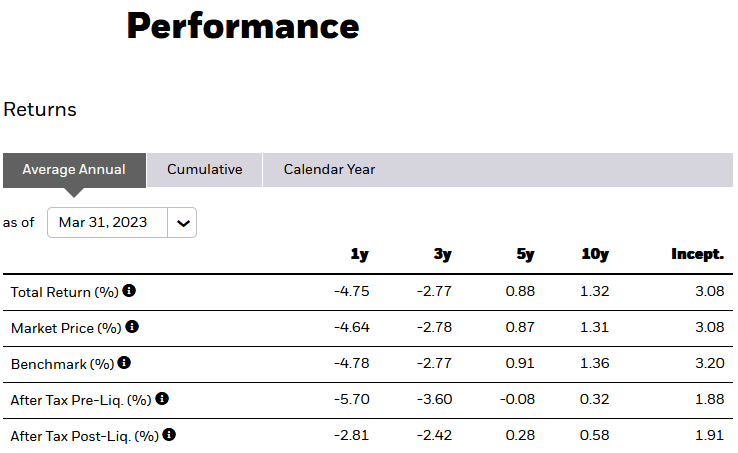

There are very few fund managers that can manage to accomplish this feat on a consistent basis, which is one of the biggest reasons why most actively managed funds fail to beat their benchmark indices. This one, though, is an exception, as it has fairly consistently beaten the Bloomberg US Aggregate Bond Index ( AGG ) over an extended period. Here are the fund's total returns over a variety of trailing periods:

{kind=link}

It is important to note that these are the fund's total returns, so these returns assume that an investor is reinvesting the distributions into shares of the fund. An investor that is not doing that will obviously have a different performance. Here are the same figures for the Bloomberg US Aggregate Bond Index:

{kind=link}

As we can see, the PIMCO fund generally beat the bond index by quite a lot over the trailing ten-year period. That certainly speaks well for the quality of this fund's management team.

We do see that the PIMCO Corporate & Income Strategy Fund has somewhat different total returns for its net asset value and market price. This is something that sets closed-end funds apart from open-end funds and exchange-traded funds. In short, a closed-end fund's price performance will not always be the same as the performance of the underlying portfolio. We can easily see this in the fact that the fund's shares delivered a -5.34% total return in 2022 but its portfolio only delivered a -4.65% total return. The fund's portfolio performed much better over the 2020 to 2022 period than its shares did in the market. That can sometimes create an opportunity for investors to acquire shares of the fund for less than the value of the assets that they represent. We will discuss this in just a bit.

Naturally, as investors we are well aware that past performance is no guarantee of future results. We are also aware that anyone purchasing the fund today will not benefit from its performance in the past. The fund's future performance is the most important thing. That is, unfortunately, difficult to predict because it is very dependent on the policies of the Federal Reserve. Earlier this week, it appeared likely that the Federal Reserve would hike rates one more time in May and then pause while it evaluated the conditions in the economy. Indeed, just a few weeks ago, there were signs that the Federal Reserve could cut rates as early as June. However, energy prices just might challenge this narrative.

Earlier today, I discussed how we could see gasoline prices rise this summer due to supplies being much tighter than last year. That would have the effect of reversing much of the progress that has been made on inflation so far and force the Federal Reserve to hike rates even as the economy continues to weaken. Thus, it is uncertain what will happen in the near term. For that reason, it might be a good idea to dollar-cost average into the fund to help reduce the negative impacts that changing rates could have on the fund's value.

Leverage

Earlier in this article, I stated that closed-end funds such as the PIMCO Corporate & Income Strategy Fund have the ability to employ certain strategies to boost the effective yield of the portfolio. One of these strategies is the use of leverage. Basically, the fund borrows money and then uses that borrowed money to purchase bonds and other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage increases both gains and losses. As such, we want to ensure that the fund is not employing too much leverage, as that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for that reason. Fortunately, this fund fulfills that requirement. As of the time of writing, the PIMCO Corporate & Income Strategy Fund has levered assets comprising 27.17% of its portfolio. This is an acceptable level that represents a reasonable balance between risk and reward.

Distribution Analysis

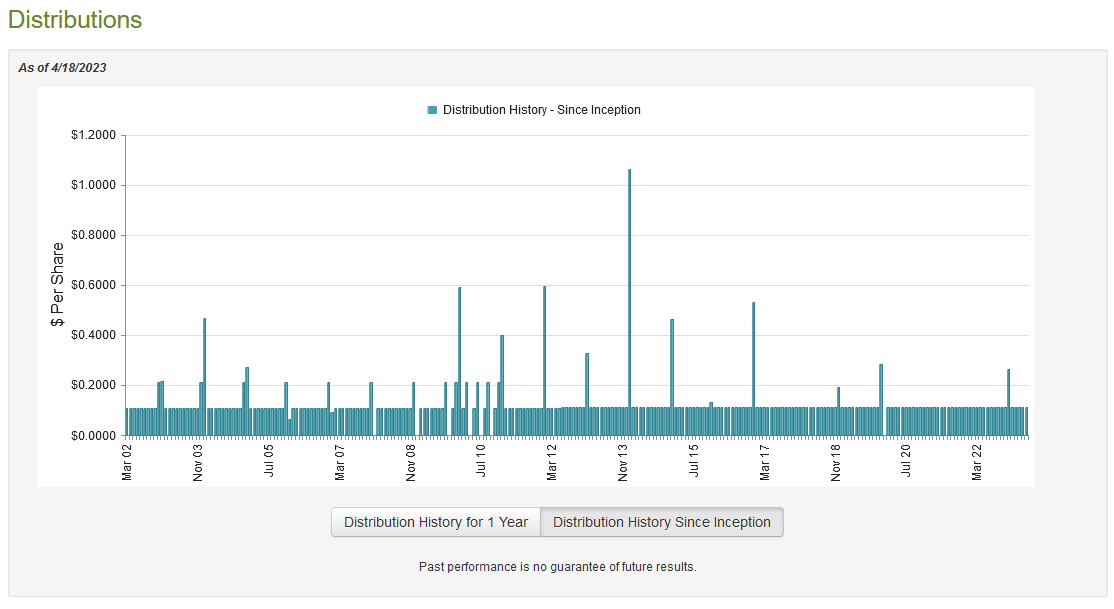

As mentioned earlier in this article, the primary objective of the PIMCO Corporate & Income Strategy Fund is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in a portfolio of bonds that primarily deliver their returns through direct payments made to the investors. The fund then leverages up the portfolio in order to increase the effective portfolio yield. As such, we might assume that the fund has a very high yield itself. This is certainly the case as the fund pays a monthly distribution of $0.1125 per share ($1.35 per share annually), which gives it a 10.71% yield at the current price. Unlike most fixed-income funds, this one has been remarkably consistent in its distribution over its history:

{kind=link}

This sort of stability is highly unusual for a fixed-income fund considering how affected most of these funds are by interest rates. The fact that this one is so stable over time is certain to be appealing to those investors that are seeking a stable and secure source of income with which to pay their bills or finance their lifestyles, however. As this history is so different from similar funds, we naturally want to investigate and see how well the fund is doing at financing it. After all, we do not want to find ourselves the victims of a distribution cut, since such an event would reduce our incomes and almost certainly cause the fund's share price to decline.

Fortunately, we do have a very recent document that we can consult for this purpose. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on December 31, 2022. This is a much more recent document than we had available the last time that we discussed this fund and, as such, it should give us a pretty good idea of how well the fund handled the turbulent market conditions that dominated 2022. During the six-month period, the PIMCO Corporate & Income Strategy Fund received $258,000 in dividends along with $33.645 million in interest from the investments in its portfolio. This gives the fund a total income of $33.903 million during the six-month period. That was unfortunately not enough to cover the $37.341 million that the fund paid out in distributions during the period, although it did get pretty close. However, the fact that the fund's net investment income was not sufficient to cover the distribution might still be concerning.

Naturally, the fund does have other methods that it can employ to obtain the money that it requires to cover the distribution. For example, it might have been able to generate capital gains from the bond trading that it engaged in during the period. In fact, it was more successful at this than might be expected. During the six-month period, the fund had net realized gains of $38.767 million, although this was offset by $46.885 million in net unrealized losses.

Overall, the fund was able to cover its distributions just using the net realized gains and net investment income, which is rather nice to see. It also issued new shares during the period, and because of this, the fund's assets actually increased by $12.108 million after accounting for all inflows and outflows. Admittedly, this distribution is probably sustainable for the time being, especially considering that the fund's assets are almost flat from the level that they were at on August 1, 2021. We should not worry too much unless something goes very wrong here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the PIMCO Corporate & Income Strategy Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all of the fund's assets minus any outstanding debt. This is therefore the money that the investors would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is certainly not the case with this fund today. As of April 18, 2023 (the most recent date for which data is currently available as of the time of writing), the PIMCO Corporate & Income Strategy Fund had a net asset value of $11.08 per share but the shares currently trade for $12.61 each. That gives the shares a 14.12% premium to net asset value at the current price, which is an incredibly large premium to pay for any fund. It is also well above the 12.57% premium that the shares have traded at on average over the past month. PIMCO funds almost always trade for a premium so it is unlikely that this one will ever be available at a reasonable price, but it may be possible to at least get it for a smaller premium by waiting and watching the fund.

Conclusion

In conclusion, the PIMCO Corporate & Income Strategy Fund appears to be a very good bond fund as it consistently outperforms the corresponding indices and has been able to maintain a very stable distribution over the years. The fact that the distribution appears to be sustainable at its current level is even more impressive considering that many of its peers have been forced to reduce their payouts in recent months. The only real problem here is that PIMCO Corporate & Income Strategy Fund is incredibly expensive, even for a PIMCO fund. It may be best to wait and see if a better price presents itself at some point.

For further details see:

PCN: A Very Good Bond Fund With A Sustainable Yield, But Price Is Way Too High