PCN - PCN: A Very Good CEF For Income But The Market Is Overvaluing It

2023-07-12 15:10:26 ET

Summary

- Investors today are desperate for any source of income in order to maintain their lifestyles in an inflationary environment.

- PIMCO Corporate & Income Strategy Fund invests in a portfolio of bonds to provide its investors with a very high level of income.

- The bond market appears to be pricing in near-term rate hikes that are unlikely to actually occur.

- The PDN closed-end fund pays a 9.90% yield, and this appears to be sustainable.

- The fund is incredibly expensive, and it may correct if the Federal Reserve stands firm with interest rates.

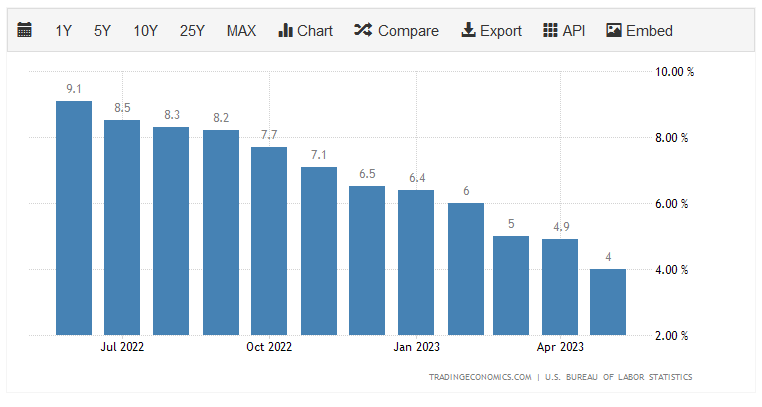

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high inflation that has been dominating the economy. This inflation has pushed up the cost of everything that we use in our daily lives, making it so the income that we earn and depend on does not go nearly as far. We can see how rapidly inflation is causing the cost of living to rise by looking at the consumer price index, which claims to measure the cost to purchase a basket of goods that is regularly used by the average consumer. As we can see here, the consumer price index has risen at a year-over-year rate that far exceeds the 2% that is considered healthy during each of the past twelve months:

{kind=link}

The official headline numbers seem to indicate that inflation is slowing down, but there are two things to consider here. The first is that inflation compounds, just like investments do. Thus, the 4% year-over-year increase that we saw in May was on top of the 8.6% increase that we experienced in May of 2022. This is what the actual person on the street experiences. The second thing to consider is that the improvements shown above are almost entirely caused by the fact that energy prices are lower than a year ago. If we look at the core consumer price index , which excludes volatile food and energy prices, inflation actually looks much worse than it did a year ago. I pointed this out in a previous article . This has caused real wage growth to be negative for 26 straight months and is the biggest cause of the financial and budgetary strain being experienced by the average person in the United States today.

As investors, we are certainly not immune to this. After all, we have bills to pay and require food for sustenance just like everyone else. The cost of performing these tasks has gone up over the past few years, so the money that we get from either our jobs or our assets does not go as far as it once did. This can make it feel as though we are growing progressively poorer with the passage of time.

Fortunately, there are some things that we can do about this problem that do not require us to take on a second job or something like that. For example, we can put our money to work for us earning an income. One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in the generation of income. These funds are unfortunately not very well followed in the financial media and many investment advisors are unfamiliar with them. This makes it difficult to obtain the information that we would like to have in order to make an informed investment decision. That is a shame because these funds offer some advantages over familiar open-ended and exchange-traded funds, such as the ability to employ certain strategies that boost their yields well beyond that of pretty much anything else in the market.

In this article, we will discuss the PIMCO Corporate & Income Strategy Fund ( PCN ), which is one fund that can be used by those investors that are seeking to earn a high level of income. This is evidenced by the fact that this fund sports a whopping 9.90% yield at the current price. I have discussed this fund before and was reasonably satisfied that it is a good fixed-income fund, but the price was incredibly high. This is a characteristic of PIMCO closed-end funds, as most of them trade well above their intrinsic value.

It is still the case that this fund is incredibly expensive, although some people might be willing to pay a high price for access to PIMCO's management team. Let us investigate and see if the PCN fund could be worth considering today, as naturally, a few things have changed since we last discussed it.

About The Fund

According to the fund's webpage , the PIMCO Corporate & Income Strategy Fund has the objective of providing its investors with a high level of current income. This is not particularly surprising considering that this is a PIMCO fund, and PIMCO is known for its fixed-income funds. This one is no exception as the fund is almost entirely invested in common stocks, although it does have a small allocation to common stock:

CEFConnect

The reason that this objective is not surprising given this asset allocation is that bonds are income investment vehicles. A bond is purchased at face value when it is issued, makes regular payments to the investor that owns it, and then pays back its face value at maturity. Thus, the only investment returns that a bond provides over its lifetime are the interest payments made to the investors. There are no net capital gains possible because the bond is both issued and redeemed at face value and it has no inherent link to the growth and prosperity of the issuing company.

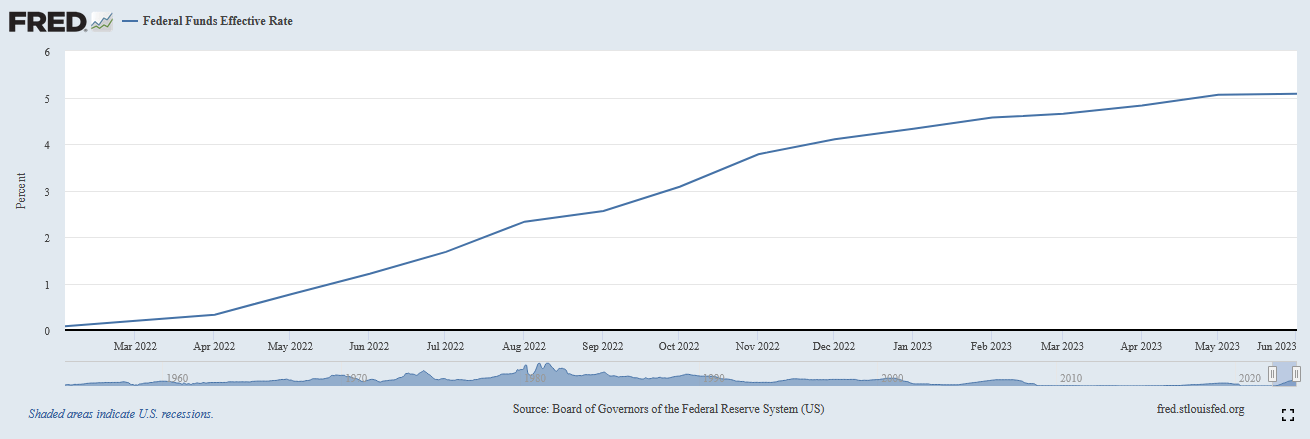

With that said, the price of a bond fluctuates over its lifetime alongside interest rates. Thus, it is possible to make some capital gains by trading the bond prior to maturity. It is an inverse relationship, so when interest rates go up, bond prices decline. The reverse is also true. As everyone reading this is no doubt well aware, the Federal Reserve has been very aggressively raising interest rates over the past fifteen months in an effort to combat the high inflation that has been dominating the economy. As we can see here, the federal funds rate has gone from 0.08% in February 2022 to 5.08% today:

{kind=link}

This has had a devastating impact on bond prices because of their inverse relationship with interest rates. After all, a bond that is issued today will have a much higher interest rate than a bond that was issued a year ago. In fact, today's interest rates are the highest that the United States has experienced since 2007, so any bond issued today will have a higher rate than just about all of the bonds currently in circulation! As a result, nobody would buy an existing bond at face value when they could get an otherwise identical brand-new bond paying a much higher interest rate. As such, the price of an existing bond has to decline so that it offers a similar yield to maturity as a brand-new bond with otherwise identical characteristics.

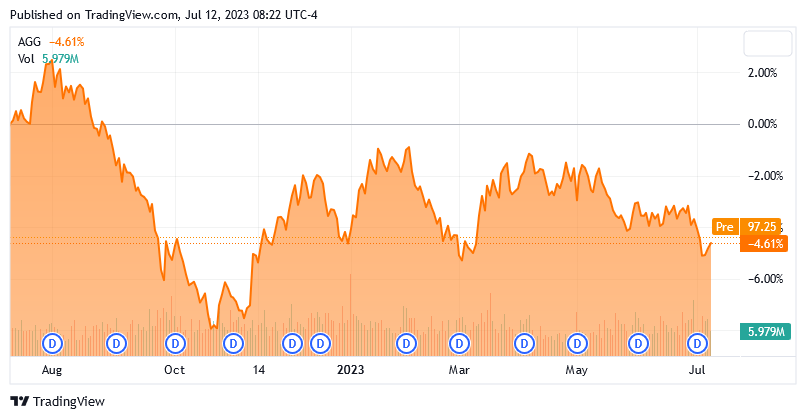

This is not really a problem for anyone that plans to hold the bond to maturity as it will be redeemed for face value regardless of the market price of the bond. However, it does pose a problem for anyone holding a bond fund because of the fact that these funds are priced based on the value of their assets. Over the past year, the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 4.61% for this reason:

{kind=link}

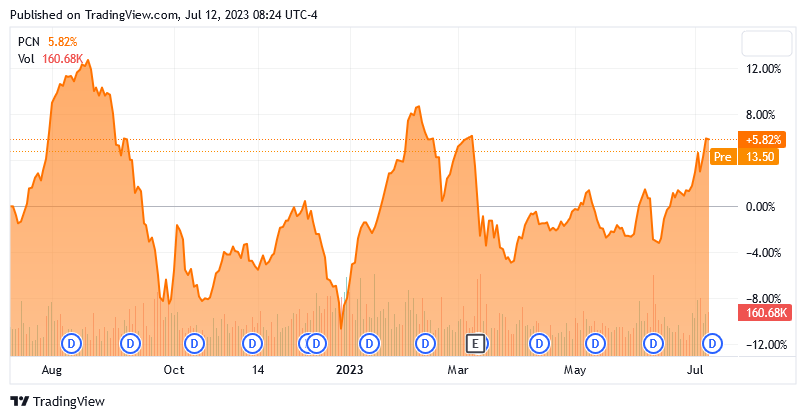

Curiously though, the PIMCO Corporate & Income Strategy Fund has done much better. This fund is actually up 5.82% over the past twelve months:

{kind=link}

The fund is also up 13.02% year-to-date. This is very surprising because it is the exact opposite of what we would expect from a bond fund. After all, the Federal Reserve has been hiking rates this year, albeit not as rapidly as the bank was raising them last year. As I have pointed out in a few previous articles though, the market appears to be overly optimistic about the trajectory of the federal funds rate. The Federal Reserve stated at its most recent meeting that there will almost certainly be two more rate hikes this year and no cuts. Yet, the action of the bond market is suggesting that interest rates will be lower by the end of 2023 than they are today. This belief is precipitated by the expectation that the central bank will cut rates as the economy heads into a recession.

We can see this belief reflected in the stock market, too, which lately has been going up anytime bad economic news comes out. If the Federal Reserve actually does cut rates when a recession hits, it will reignite inflation so doing so would be an incredibly foolish move. Then again, 2024 is an election year and the bank may be hesitant to do anything perceived as negative for the economy during that year. It will be interesting to see how this all plays out, but I do think that the fund's bull run over the past three weeks is likely to reverse if the central bank shows any sign of backbone. Thus, today might not be the best time to purchase shares.

PIMCO bond funds tend to be a bit more aggressive about their trading activity than fixed-income funds from other managers. This is one reason why people like them, as it can result in much higher realized profits for the shareholders when done successfully.

The PIMCO Corporate & Income Strategy Fund is certainly no exception to this as its 47.00% annual turnover is quite a bit higher than most fixed-income closed-end funds. This is important because it costs money to trade bonds or other assets, and these expenses are billed directly to the fund's shareholders. This creates a drag on the fund's performance and makes the job of the fund's managers more difficult. After all, management needs to earn sufficient returns to cover these additional expenses as well as deliver an acceptable return to the shareholders. This is a very difficult task that few management teams manage to accomplish on a consistent basis. This is one of the reasons why actively-managed funds tend to underperform their benchmark indices.

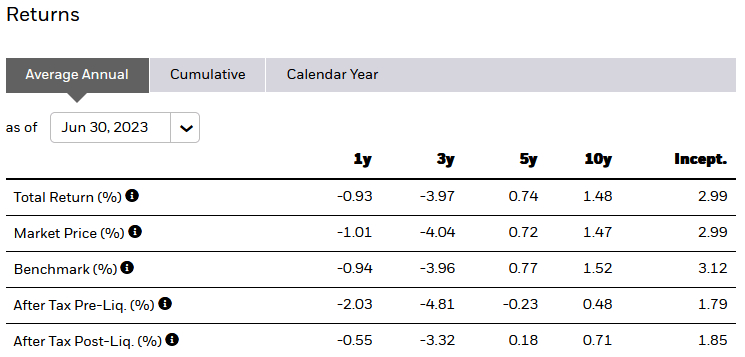

The PIMCO Corporate & Income Strategy Fund appears to be something of an exception here as it has performed very well relative to the indices. Here is the fund's historical performance over several periods of time that ended on June 30, 2023:

{kind=link}

Here is the performance data for the iShares Core U.S. Aggregate Bond ETF for the same period:

{kind=link}

As we can clearly see, the PIMCO closed-end fund completely dominated the index fund during any relevant period. While past performance is no guarantee of future results, this does speak very highly about the skill of the fund's management team. It also explains the fund's general popularity with investors.

One thing that we do notice though is that the fund's market share price performance over the past year has greatly exceeded the performance of the actual portfolio. The fund itself only managed to achieve a 9.77% total return over the trailing twelve-month period that ended on June 30, 2023. However, the fund's shares delivered a 17.14% total return in the market over the same period. This is a very clear sign that the shares have gotten ahead of themselves and could mean that today is a bad time to buy the fund. We will discuss this in more detail later in this article.

Leverage

As stated in the introduction to this article, closed-end funds such as the PIMCO Corporate & Income Strategy Fund have the ability to employ certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of the strategies that is used by this fund to accomplish that task is leverage. In short, the fund borrows money and uses that borrowed money to purchase bonds and similar securities. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is not nearly as effective today with rates at 5% to 6% as it was a year ago when rates were about 0%.

The use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. Thus, we want to ensure that the fund is not employing too much leverage as that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

Fortunately, the PIMCO Corporate & Income Strategy Fund meets this requirement, as its levered assets comprise 26.79% of the portfolio as of the time of writing. This is a reasonable level that represents a pretty good balance between risk and reward. We should not have to worry too much about the risk posed by the fund's leverage.

Distribution Analysis

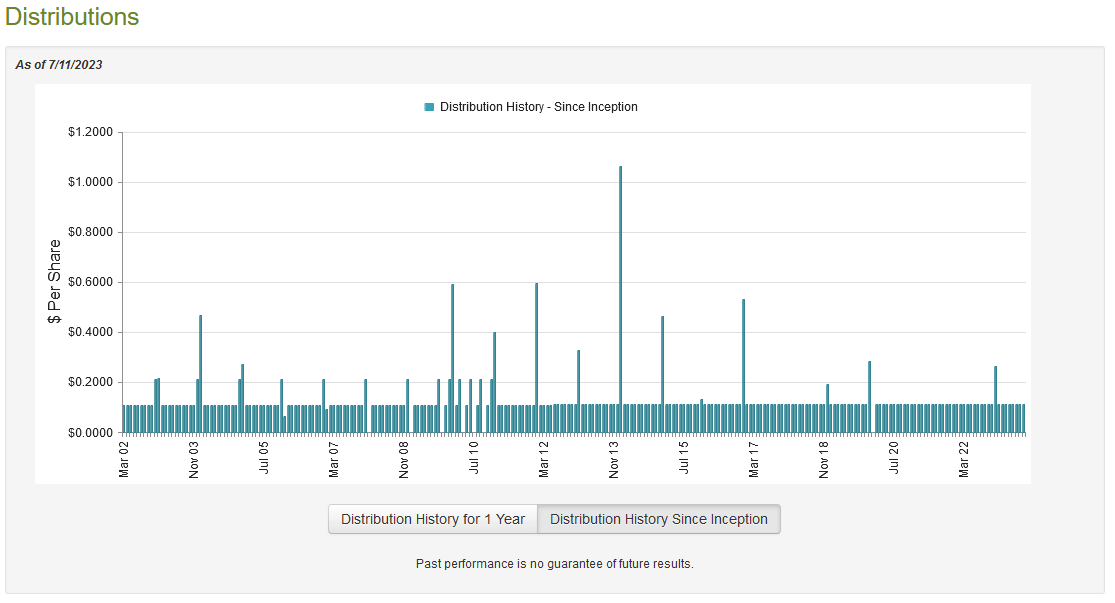

As mentioned in the introduction, the PIMCO Corporate & Income Strategy Fund has the stated objective of providing its investors with a high level of current income. In order to achieve this objective, it invests in a combination of government and corporate bonds in both the United States and abroad. Bonds tend to have respectable yields, especially in today's environment, and this fund employs leverage to artificially boost the yield that it gets from the bonds in its portfolio. As such, we can assume that it will have a relatively high yield itself. This is indeed the case as the fund pays a monthly distribution of $0.1125 per share ($1.35 per share annually), which gives it a 9.90% yield at the current price. The fund has been remarkably consistent in its distribution over its history as shown here:

{kind=link}

This is a much more consistent distribution history than that possessed by just about any other fixed-income closed-end fund. Nearly all of these funds vary their distribution with interest rates, but this one has been very stable. This could be either a blessing or a curse since it certainly increases the fund's appeal among those that are seeking a stable and secure source of income but it is also curious that this fund has been able to accomplish a feat that others have not. Naturally, we want to investigate to determine how well this fund can sustain its distribution as we do not want to be the victims of a distribution cut. This is because a distribution cut will reduce our incomes and almost certainly cause the stock price to decline.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on December 31, 2022. As such, it will not include any information about the fund's performance year-to-date. This is unfortunate because the bond market rally did provide some opportunities to make trading profits, even though I do think that the market is overly optimistic. The fund's report will give us a pretty good idea of how well the fund navigated the incredibly challenging market conditions of 2022 though, which was probably the worst market for bonds that most of us have ever seen.

During the six-month period, the PIMCO Corporate & Income Strategy Fund received $33.645 million in interest and $258,000 in dividends from the assets in its portfolio. This gave the fund a total investment income of $33.903 million during the period. It paid its expenses out of that amount, which left it with $27.668 million available for the shareholders.

Unfortunately, that was nowhere near enough to cover the $37.341 million that the fund actually paid out during the period. At first glance, this is certainly concerning because we like to see a fixed-income closed-end fund cover its distributions solely through net investment income.

With that said, the fund does have other methods through which it can obtain the money that it needs to pay its distributions. As already mentioned, this fund tends to engage in a great deal of trading in order to take advantage of bond price fluctuations. That can give it profits that could be distributed to the investors. The fund did have some success at that task as it achieved net realized gains of $38.767 million but these were offset by $46.885 million net unrealized losses. Overall, the fund's assets went up by $30.446 million during the period after accounting for all inflows and outflows. However, those inflows included a $26.348 million capital raise. It did actually manage to cover its distributions in the absence of the capital raise though as the net realized gains plus net investment income was more than enough to cover the distribution and give the fund some money left over to offset the net unrealized losses.

This is, admittedly, one of the best performances that I have seen for any fixed-income fund during 2022, and the fund's assets actually were higher on January 1, 2023, than they were on August 1, 2021, so the fund did do acceptably over the entire period. If it can achieve similar performance going forward, then this distribution should be sustainable. There is no real reason to assume that this will not be the case.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the PIMCO Corporate & Income Strategy Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of July 11, 2023 (the most recent date for which data is available as of the time of writing), the PIMCO Corporate & Income Strategy Fund had a net asset value of $11.09 per share but the shares currently trade for $13.49 each.

This gives the fund's shares a 21.64% premium to the net asset value. That is an incredibly high price to pay for any fund and it is well above the 17.37% premium that the fund's shares have had on average over the last month. Overall, it might make sense for a more value-oriented investor to wait until PIMCO Corporate & Income Strategy Fund shares are trading at a much lower valuation before buying in.

Conclusion

In conclusion, the PIMCO Corporate & Income Strategy Fund appears to be one of the best fixed-income closed-end funds available in the market. The fund delivered a very respectable performance last year despite the challenging conditions in the market and is one of the few that actually managed to cover its distributions last year.

In fact, my only complaint about PIMCO Corporate & Income Strategy Fund is that it looks ridiculously expensive today, and there is a very real chance that the price will fall if the Federal Reserve retains its integrity and does not cut rates in the face of a recession. Thus, it might be possible to get a better price by waiting. With that said, the fund's distribution is high enough that long-term investors will probably get a reasonable total return even if they do buy at today's price.

For further details see:

PCN: A Very Good CEF For Income, But The Market Is Overvaluing It