PCN - PCN: Great Bond Fund But Enormous Premium Presents Risks

2023-09-18 17:39:12 ET

Summary

- The PIMCO Corporate & Income Strategy Fund offers a high level of income with a 9.83% yield.

- The fund has performed well in the market, but there are concerns about the market's optimism on bonds and interest rates.

- The fund's shares appear to be overvalued, which presents risks in the event of the bond market realizing that interest rates will not come down.

- This is one of the only bond funds that has managed to cover its distributions over the past year.

- The fund itself looks pretty solid, the major concern here is the substantial overvaluation.

The PIMCO Corporate & Income Strategy Fund ( PCN ) is a closed-end fund, or CEF, that investors can use to earn a very high level of income. The fund’s 9.83% yield indicates that it should do a reasonable job at this, although the yield is quite a bit lower than many other PIMCO closed-end funds. This may not be a bad thing though, since any time a fund’s distribution gets above 10% or so, it is a sign that the market expects that it may have to cut its distribution in the near future. The PIMCO Corporate & Income Strategy Fund has not hit this level yet, so that could be a very good sign.

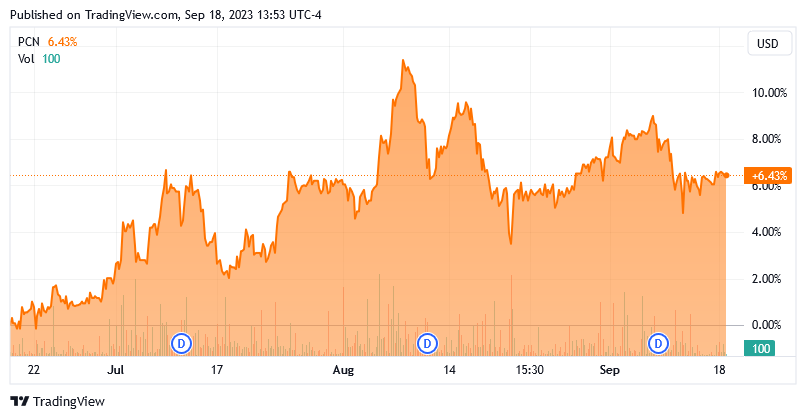

The fund has been performing very well in the market lately, as it is up 6.43% in the past three months:

{kind=link}

These recent gains may or may not be sustainable though, as there are currently numerous reasons to believe that the market is being far too optimistic on bonds and interest rates. After all, inflation has started to tick up as oil prices recently passed $90 per barrel, which is the highest level that they have had since November 2022. In addition, the core consumer price index remains at close to double the Federal Reserve’s target level. These things could cause the Federal Reserve to raise interest rates, rather than cut them as the market expects. This could very quickly cause this fund to erase all of the gains that it has enjoyed over the past few months. When we combine this with the fact that the fund’s shares appear to be substantially overvalued relative to their intrinsic value, it may be best to sit on the sidelines for the time being.

As regular readers may recall, we last discussed this fund back in July. While many of the comments that I made in that article about this fund are still valid, there have been some events since that time that have made the bond market riskier than it was previously. This extends to this fund, so it is worth revisiting this fund to determine if it really is worth the potential risks.

About The Fund

According to the fund’s webpage , the PIMCO Corporate & Income Strategy Fund has the objective of providing its investors with a high level of current income. This is a very common and understandable objective for a bond fund. This one includes much more than this in its description of its strategy and objectives, however. From the webpage:

Using a dynamic asset allocation strategy that focuses on duration management, credit quality analysis, risk management techniques, and broad diversification among issuers, industries, and sectors, the multi-sector fund seeks high current income, with a secondary objective of capital preservation and appreciation.

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets plus borrowings for investment purposes in a combination of corporate debt obligations of varying maturities, other corporate income-producing securities, and income-producing securities of non-corporate issuers, such as U.S. Government securities, municipal securities and mortgage-backed and other asset-backed securities on a public or private basis.

This description strongly suggests that the PIMCO Corporate & Income Strategy Fund is a fixed-income fund, which is exactly what we would expect from PIMCO. After all, PIMCO is quite well known as being a bond house. The fund’s asset allocation supports this conclusion. As of the time of writing, the fund has 189.17% of its assets invested in bonds, alongside comparatively small allocations to both common and preferred stocks:

CEF Connect

One immediate question that someone looking at the above table might ask is how the fund can have a negative allocation to cash. This comes from the fact that this fund employs leverage as a way to improve its returns. We will discuss this later in this article, but for now, it is important to keep in mind that this boosts both the fund’s total returns and potential losses relative to a fund that is not employing leverage.

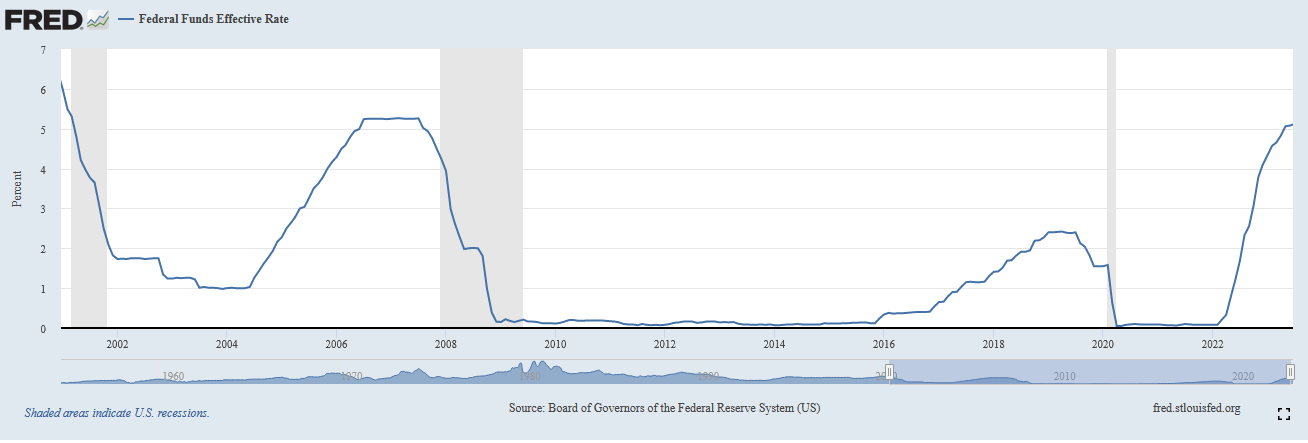

One of the defining characteristics of bonds is that their price declines when interest rates rise. This is one reason why the fund’s recent performance makes no sense. After all, the Federal Reserve has been very aggressively raising interest rates since the early months of 2022 in an attempt to combat the incredibly high rate of inflation that is pervasive in the economy. As of the time of writing, the effective federal funds rate is at 5.33%, which is the highest level that has been seen since early 2001:

{kind=link}

For those that can remember it, the early months of 2001 were around the time that the Internet bubble burst, and it goes without saying that this was a much stronger economy than we have today. Indeed, that was arguably the strongest economy that most people reading this can probably remember. The fact that rates are so high now is a sign that the Federal Reserve is strongly committed to getting inflation down to its target level. Chairman Powell has made comments that have suggested as much.

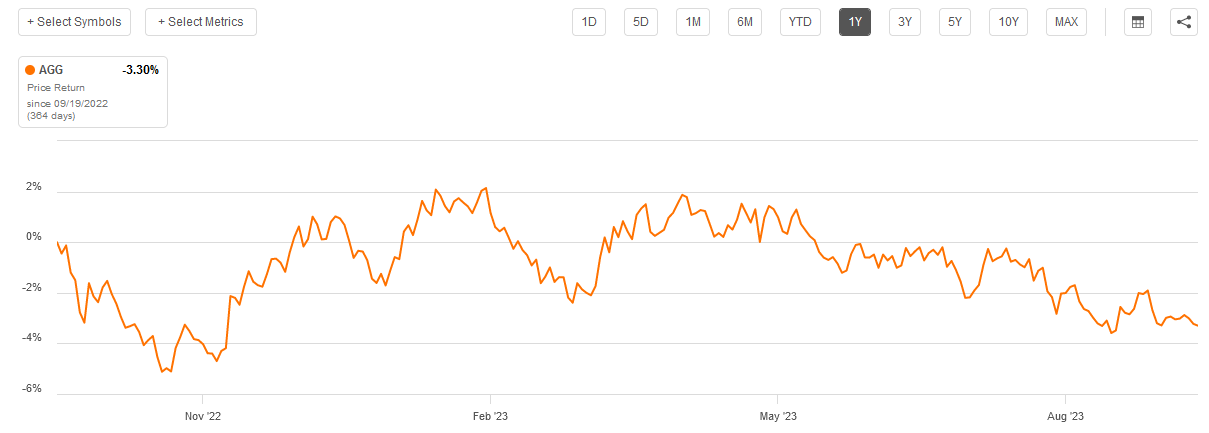

Over the past year, the effective federal funds rate has gone from 2.33% to 5.33%, which is a 300-basis point increase. Due to the inverse correlation between bond prices and interest rates, this would be expected to cause bond prices to decline fairly significantly. This has indeed happened, as the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 3.30% over the period:

{kind=link}

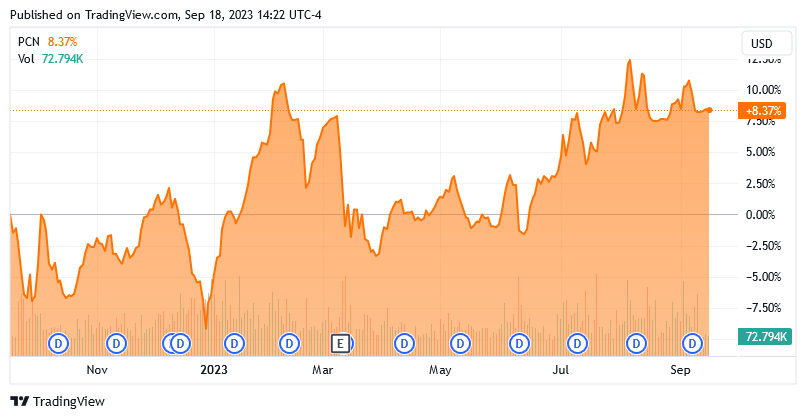

However, the PIMCO Corporate & Income Strategy Fund is up 8.37% over the exact same period:

{kind=link}

This makes no sense at all if this fund is buying traditional fixed-rate bonds. This kind of performance might make sense if the fund were holding floating-rate securities, however. As I pointed out in a previous article , floating rate securities tend to hold their value reasonably well regardless of interest rate movements. The fund’s strategy description that was quoted above makes no mention of holding floating-rate securities, but it does not specifically exclude them either. Likewise, the fund’s webpage does not say anything regarding the extent to which the fund is investing in floating-rate securities versus traditional fixed-rate bonds. The fund’s annual report , which is dated June 30, 2023, states that 37.4% of the fund’s assets are invested in “Loan Participations and Assignments.” Some of these are floating-rate securities, so the fund definitely includes them. However, the annual report points to the overwhelming majority of the fund’s assets being fixed-rate assets. As such, they should be losing value as interest rates increase, but for some reason, the market is driving up the fund’s share price.

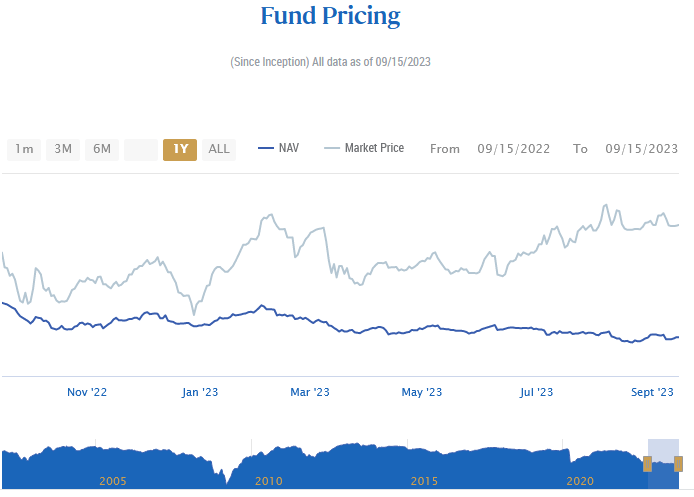

In other words, the fund’s shares do not reflect the performance of its actual portfolio. PIMCO itself verifies that this is the case. On its webpage, the fund sponsor helpfully provides a chart that compares the fund’s share price performance to that of the actual portfolio. Here it is, with the range limited to the past year:

{kind=link}

The dark blue line is the portfolio’s performance, while the lighter line is the fund’s performance in the market. As we can see here, the portfolio itself has actually delivered a negative return over the period, which is exactly what we would expect from a bond fund that is investing in fixed-rate bonds. Thus, the market performance does not reflect the actual performance of the portfolio at all. It stands to reason that at some point things will reverse and the fund’s shares will come crashing back to something reflecting the actual performance of the fund’s portfolio. When this happens, anyone holding the fund’s shares will suffer significant capital losses. Anyone considering purchasing this fund today should be very cautious.

In a few recent articles (see here and here ), I discussed that the market is far too optimistic about the potential for further interest rate hikes. The market appears to be suggesting that the Federal Reserve will either hold rates flat or cut them over the next six months or so. When we consider that the headline inflation rate has gone up for the past two months and the core consumer price index ex-Shelter, which is one of the Federal Reserve’s most watched indicators, ticked up last month, it seems highly unlikely that rates will be cut within the next few months. After all, Chairman Powell continues to state that the Federal Reserve will not stop its monetary tightening until inflation reaches its 2% target. PIMCO’s own Bill Gross seems to agree with the assessment that the market is too optimistic. As I pointed out last month, Mr. Gross believes that the ten-year Treasury should be at 4.500%, which would mean that the price has to come down from today’s 4.319%. Thus, he also believes that fixed-rate bonds, such as the ones held by this fund, are overpriced. When we combine this with PIMCO’s own statements that the fund’s performance does not justify its price action, we can see the very high risk.

The best way for the fund to protect itself against this risk is to hold floating-rate securities. After all, the price of floating-rate bonds tends to be almost perfectly flat over time. The second-best way is to hold very short-term securities. This is because the less time that the bond has until it matures, the less interest rates affect its price. The fund is doing this, fortunately. As we can see here, the fund’s portfolio is currently weighted towards short-term securities, with more than half of the fund’s assets maturing in five years or less:

PIMCO

As we can see, 60.85% of the fund’s assets mature in less than five years. As just stated, this should provide some protection against an interest rate increase (or anything else that makes the market suspect that the Federal Reserve is serious with its “higher for longer” mantra). The fund will still take some losses in such an event though, but they will not be as severe as if the fund were invested in long-term securities.

Another interesting benefit of short-term securities right now is that they have higher yields than longer-term securities. This is because the market expects fairly significant interest rate cuts going forward. The higher yields mean that the fund should be able to earn more income and reduce its risks compared to holding long-dated bonds. That is certainly a win for the fund’s shareholders, who are primarily seeking income.

Leverage

As mentioned earlier in this article, the PIMCO Corporate & Income Strategy Fund employs leverage as a method of boosting its effective portfolio yields and total returns. I explained how this works in my previous article on this fund:

In short, the fund borrows money and uses that borrowed money to purchase bonds and similar securities. As long as the purchased assets have a higher yield than the fund has to pay on the borrowed assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is not nearly as effective today with rates at 6% as it was eighteen months ago when rates were at 0%.

The use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. Thus, we want to ensure that the fund is not employing too much leverage as that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

The PIMCO Corporate & Income Strategy Fund has substantially decreased its leverage since the last time that we discussed it. As of the time of writing, the fund’s levered assets comprise 18.79% of the portfolio, compared to 29.79% of the portfolio a few months ago. This could actually be a sign that PIMCO’s management agrees with the thesis above that the current environment for bonds is getting riskier. For our purposes, we should not have to worry about this fund’s leverage too much since it is currently striking a reasonable balance between risk and reward.

Distribution Analysis

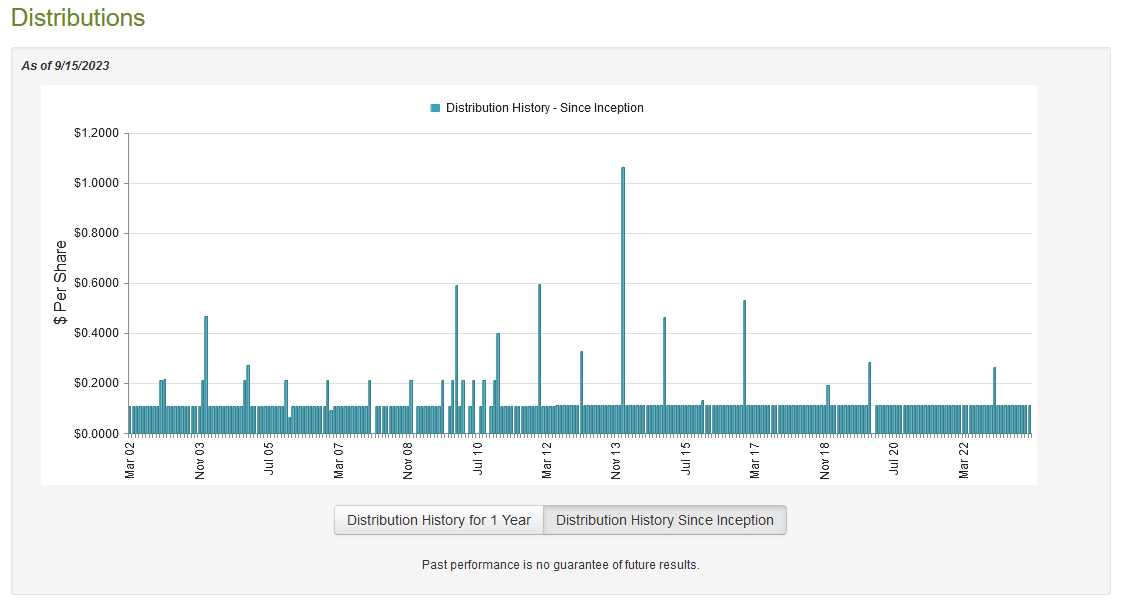

As mentioned earlier in this article, the primary objective of the PIMCO Corporate & Income Strategy Fund is to provide its investors with a high level of current income. In order to accomplish this objective, the fund purchases a variety of bonds that deliver a significant portion of their total return in the form of direct payments to their investors. The fund then applies a layer of leverage to boost the effective yield of the bonds in the portfolio. It then collects all of the money that it receives as coupon payments from these bonds, any capital gains that it manages to generate through trading bonds and exploiting bond price changes, and pays it out to the investors net of any expenses. As bonds frequently have respectable yields and this fund is boosting that with leverage, we can expect that the fund itself will have a very high current yield. This is indeed the case, as the PIMCO Corporate & Income Fund pays a monthly distribution of $0.1125 per share ($1.35 per share annually), which gives it a 9.83% yield at the current price. This fund has been remarkably consistent with its distribution over the years:

{kind=link}

Without a doubt, this is one of the best track records of any bond fund. We can see that the fund raised its distribution once over the past twenty years but has otherwise kept it quite steady. The majority of closed-end funds that invest in fixed-rate bonds have had to cut their distributions over the past year, so this fund is definitely an outlier. While that is nice to see, it is also a point of concern. After all, it makes little sense that this fund could accomplish such a task when very few of its peers can. As such, we want to pay special attention to the fund’s finances to determine exactly how sustainable its distribution is likely to be.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report (linked earlier) corresponds to the full-year period that ended on June 30, 2023. This is a much newer document than we had available the last time that we discussed this fund, which is nice as it should provide us with more insight into exactly how sustainable the distribution is likely to be. After all, the bond market bounced back quite a bit from its December 2022 levels during the first half of this year and that could have provided this fund with the opportunity to earn some trading profits.

During the full-year period, the PIMCO Corporate & Income Strategy Fund received $67.782 million in interest and $654,000 in dividends from the assets in its portfolio. When combined with a small amount of income from other sources, the fund reported a total investment income of $68.458 million during the period. It paid its expenses out of this amount, which left it with $55.626 million available to shareholders. This was, unfortunately, not nearly enough to cover the $69.905 million that the fund actually paid out to its investors. At first glance, this is certainly going to be concerning since we usually like a fixed-income fund to be able to completely cover its distribution out of net investment income. This one clearly failed in that task.

With that said, there are other methods through which a fund can obtain the money that it needs to cover its distributions. For example, it might be able to exploit fluctuations in bond prices to generate some capital gains. The fund had mixed success at this during the full-year period. It did manage to achieve net realized gains of $17.516 million but these were more than offset by $31.090 in net unrealized losses. While the fund’s assets did increase by $41.899 million during the period, this was only because the fund conducted a $63.275 million capital raise. In short, the fund brought in new money to cover its losses, and its net assets would have declined were it not for this new money. With that said, the fund did manage to cover its distributions during the period as net investment income plus net realized gains totaled $73.142 million, which was sufficient to cover the distributions made to the shareholders. The problem here was the net unrealized losses. These may or may not be a big deal as unrealized losses can be erased when the market shifts. This is one of the few bond funds on the market that appears to be capable of sustaining its distribution.

Valuation

As of September 15, 2023 (the most recent date for which data is currently available), the PIMCO Corporate & Income Strategy Fund has a net asset value of $10.96 per share but the shares currently trade for $13.74 each. That represents a 25.36% premium on net asset value. While this is better than the 26.28% premium that the shares have averaged over the past month, that is still an incredibly high price to pay for any closed-end fund.

Conclusion

In conclusion, there is a lot to like about the PIMCO Corporate & Income Strategy Fund. The fund’s management seems competent, and this is one of the few bond funds that has actually managed to cover its distribution over the past year or so. The bond market itself appears to be overly optimistic about the near-term outlook for interest rates and this could result in significant losses if the Federal Reserve does indeed raise interest rates further. That is hardly a problem that is unique to this fund, however. The only real problem here is that the fund’s share performance is greatly disconnected from the performance of the portfolio. PIMCO itself points this out, and this could represent a very real risk to investors.

For further details see:

PCN: Great Bond Fund, But Enormous Premium Presents Risks