PCN - PCN: Still Not A Buy As We Look To 2024

2023-12-17 00:48:29 ET

Summary

- The article evaluates the PIMCO Corporate & Income Strategy Fund as an investment option.

- The fund's premium to NAV, poor income metrics, and the market's narrowing of high-yield corporate spreads all suggest caution is warranted going forward.

- There is some good news, such as modest growth in corporate bond issuance globally and the potential for yield "pick up" in non-US holdings.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Corporate & Income Strategy Fund (NYSE: PCN ) as an investment option. This is a closed-end fund with a primary objective "to seek high current income, with a secondary objective of capital preservation and appreciation."

I cover PCN a few times a year because it has been a fund I have traded in and out of since I began my investment career. When 2023 got underway, I saw limited value in it and felt the market had plenty of other opportunities to pursue. Looking back, I was correct to avoid this fund this calendar year as the return since my February article has been negative:

Fund Performance (Seeking Alpha)

As usual, with a fresh year, I bring a fresh set of eyes to each fund I cover. This has led me back to PCN given that eleven months have passed since I've written about it and I wanted to see if a change in rating was warranted. After review, I still believe this fund remains overpriced and that better values exist elsewhere. As such, my "hold" outlook will remain in place, and I will explain why in more detail below.

The Premium Persists

The first and most obvious point to make is that PCN's market price remains a bit too rich for my blood. My followers know I shy away from funds trading at excessive premiums and that includes PCN. While the premium has narrowed since my February article - when it sat around 15% - the current level near double-digits is just not reflective of the value I look for:

PCN's Quick Stats (PIMCO)

The long and short of it from me is that PCN's price, despite being cheaper than back in February, is too expensive for me to consider a "buy" recommendation in isolation. There would have to be multiple other compelling attributes that can overcome this premium in my view. This alone has me leaning towards "hold" at a minimum, which is in line with my general outlook on CEFs and valuations that I have had over the years.

Opportunity In High Yield Is Limited

My next topic shifts to a discussion on PCN's underlying holdings. Consistent with the fund's strategy over the years, this is a big play on the high-yield credit sector. While PCN holds a lot of different types of securities, below IG-rated debt makes up over 38% of total fund assets:

PCN's Sector Breakdown (PIMCO)

This means that one would definitely want to be a "bull" on high-yield securities if they are going to buy or hold this fund. If you aren't optimistic about the outlook for this sector, buying into this fund wouldn't make a whole lot of sense.

Based on the title of this article, readers have probably surmised I am not a bull on the high-yield credit sector for the time being. And that is correct. While it has rallied recently (and performed generally well in 2023), I have concerns about the go-forward potential. This stems from the fact that spreads are very narrow compared to where they have sat for the last year and a half:

High Yield Spreads (Yahoo Finance)

{kind=link}

What this tells me is that the opportunity was much clearer in the past. While spreads could narrow further - helping to fuel more positive returns - history shows us in the short term that we are nearing a key resistance level. Buyers are going to have to keep coming in and being willing to accept a lower and lower level of income on an adjusted basis.

This doesn't present a favorable risk-reward backdrop. Add in the fact that PCN charges a premium to own it, I don't see the value. Why overpay for a sector that is looking like it may be near a peak? Hard for me to make that case and certainly helps explain why a neutral rating makes sense to me for now.

The Market Is Too Passive For Me

My second concern is a macro-one. This is related to the general calm that has presided over the markets for the past few months. We have seen both stocks and bonds rally - without any meaningful pullback since October. While "good" for investors (myself included!) it ties back to my broader worry that things may have gotten a bit carried away. When gains come in too far, too fast, I get cautious as a rule.

To amplify this, take a look at the VIX index. This measure of volatility shows that the wider market is extremely passive and hardly pricing in any level of go-forward risk or shock to the market:

{kind=link}

So - why does this matter to a fund like PCN? Because PCN is a leveraged, risk-on play that will almost certainly see a spike in volatility if the "market" shows volatility as well. We know this because, as just mentioned, PCN has a lot of below-IG quality debt. This high-yield corner of the market tends to be very correlated with equities. While there is still some key diversification between the two asset classes, over time the strength of the correlation is clear and well above what other fixed-income sectors offer:

Correlations To Stocks (S&P 500) (FactSet)

My takeaway here is that the VIX can't stand at rock bottom levels forever. There is bound to be an uptick in market volatility and probably sooner than later. If that happens stocks will see some swings, and the high-yield credit sector is not likely to avoid that. That means PCN will see some swings by extension. This suggests to me that waiting for a better entry point in the fund is completely justifiable.

Income Story Remains A Concern

Another critical element of PCN is the fund's income stream. Much of the high-yield market offers a double-digit yield and that is reflected in PCN's current payout. At just under 11%, this is sure to attract plenty of interest from retail investors:

Current Distribution (PCN) (Seeking Alpha)

The problem I have is not in the level of income - this registers as quite high to me, of course. The challenge is with sustainability. PCN's income metrics haven't been very strong this calendar year and the December report shows that there hasn't been a lot of progress in the short term:

{kind=link}

As you can see, PCN is deep in the red in terms of its UNII balance and the coverage ratios indicate this isn't going to change any time soon. While I am not one to over-exaggerate the risk of a distribution cut, the fact is these numbers do not inspire much confidence.

Ultimately, it comes down to the value proposition for me. Reverting to the premium price, the income metrics certainly don't indicate the premium is warranted. An 11% yield sounds great, but only if the fund can maintain it will a reasonable amount of certainty. I don't see that being the case here, so this is another attribute that keeps me away from being a buyer.

There Has To Be Some Good News, Right?

Through this review, I have touched on a number of elements that I believe support my decision not to buy into PCN. But I always feel the need to balance any article I write with pros and cons. I believe that sets me apart from many of the bloggers out there and I will maintain the consistency in my approach in the new year as well.

With respect to PCN, where is the good news? Well, for one the fund is very diversified beyond the high-yield credit sector. While domestic, below IG-rated debt is a heavy allocation in the portfolio, that still leaves two-thirds of the securities finding a home elsewhere. About 20% of the holdings are in non-US debt, both developed and emerging markets and another 15% is in mortgage-backed securities.

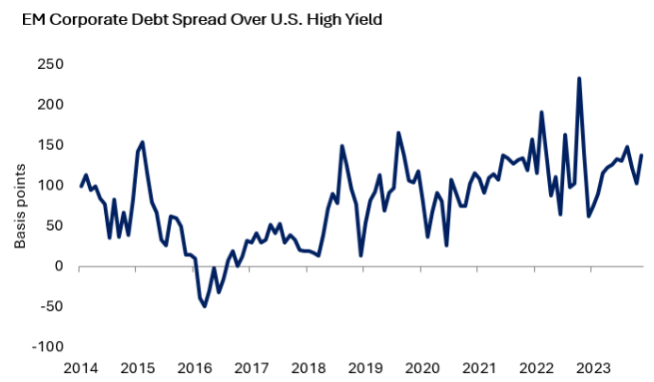

Of particular interest to me is the EM-backed allocation. The benefit here is that while US-backed high-yield credit spreads are narrow, EM-backed high-yield spreads have a clear spread advantage that has been growing in the short term:

Additional Spread (EM Credit over US high yield) (World Bank)

{kind=link}

Of course, EM credit has unique risks. There are generally more geo-political concerns, credit risk can be elevated, and currency fluctuations add an extra layer of complexity. So I would personally need more compensation for diving into this sector over high-yield credit inherently. But the fact that spreads look historically wide and have widened recently suggests to me there is value here. This makes their inclusion in PCN's portfolio a benefit in my view.

Corporate Issuance Subdued

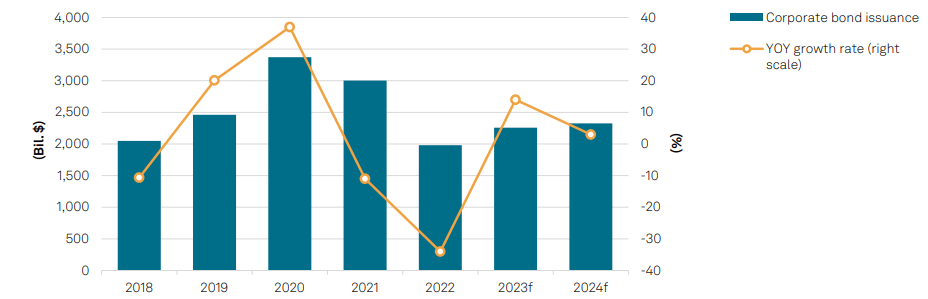

Another positive for PCN relates to a macro-development we are witnessing in the corporate credit market. Specifically, as rates have risen, corporations have been reluctant to take on a lot of new debt. This has been aided by more fiscal prudence and - perhaps most importantly - the reality that companies binged on cheap debt while it was available for years. The net result was that as interest rates have risen, net bond issuance has not seen a lot of growth:

Corporate Bond Issuance (By Year) (Global) (S&P Global)

{kind=link}

This helps to support the underlying values of existing corporate bonds because supply has been relatively tight compared to prior years. While there is no guarantee as to what 2024 will bring, the macro-environment for the time being is supportive of valuations for many of the securities in PCN's portfolio. Given that global issuance has been steady, this impacts both the US and non-US assets within this CEF. This trend could certainly adjust next year, but for now, I view this backdrop positively.

Bottom-line

PCN hasn't offered much to investors this year and that is a story I don't see changing in the next few months. The fund's premium to NAV is much too high, especially when I consider that the income metrics are weak and high-yield corporate spreads are narrow (which is the fund's largest sector by weighting).

There is good news to balance this out - such as modest growth in new bond issuance globally and high-yield opportunities outside the US, which PCN has taken advantage of. Still, I think that the next quarter is likely to see an uptick in volatility that will challenge PCN's total return. As a result, I see no reason to upgrade my outlook now and will keep the "hold" rating in place as we look to begin 2024. This means readers should approach any new positions very selectively at this time.

For further details see:

PCN: Still Not A Buy As We Look To 2024