PCQ - PCQ: One Year Later A Vastly Different Story Can Be Told

2023-12-28 11:16:19 ET

Summary

- PIMCO California Municipal Income Fund previously traded at a high premium but now has a double-digit discount to NAV, making it a more attractive investment option.

- The supply of new municipal bonds has decreased, creating a favorable market dynamic for funds like PCQ.

- California's improving revenue and the expectation of a steepening yield curve in 2024 are positive factors for PCQ's performance.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO California Municipal Income Fund ( PCQ ) as an investment option at the current market price. The fund invests primarily in California municipal bonds, and therefore seeks to provide current income which is exempt from federal and California income tax. The fund normally invests at least 90% of its net assets in municipal bonds that pay interest that is exempt from federal and California income tax. It also seeks to be “AMT-free” by investing only up to 20% in bonds generating interest that may subject individuals to the alternative minimum tax.

I have often covered PCQ, but generally with a grain of salt. Those who follow PIMCO CEFs closely know that this used to be a "darling" of the PIMCO family, in that it traded at consistently high premiums for years. While that generally dissuaded me from investing, it didn't stop others, who felt confident enough to bank on that premium continuing to exist. Well, back in December last year, I simply saw too many hurdles facing the fund that suggested the premium was going to get wiped out. And, I was spot-on correct with that assessment:

Fund Performance (Seeking Alpha)

This was undoubtedly a painful lesson for many investors in PCQ. Looking back, the warning signs were a bit obvious, but I was surprised by just how rapid and steep the drop ended up being. Live and learn.

But the more important discussion as we approach 2024 is where PCQ goes from here. Fortunately, the outlook is a bit brighter than it was twelve months ago. Some of the negative attributes have self-corrected, enough that I feel comfortable upgrading my rating. I will explain the reasons behind this decision in detail below.

From Outrageous Premium To Steep Discount

Perhaps the biggest change from December 2022 to December 2023 for PCQ is the fund's valuation. As my followers know, I generally avoid CEFs at premium prices (and for good reason). There are exceptions, but I would rarely (if ever) contemplate buying something above the 10% premium range. This has kept PCQ off my buying block for some time - including last year - when the fund sported a premium in excess of 48%!

That alone should have given investors pause. I honestly can't believe someone would pay that large a premium for any CEF, much less one in which there are many viable alternatives. But that is water under the bridge, and what matters today is PCQ's valuation has reversed sharply. Rather than sporting a premium, PCQ now has a discount to NAV in double-digits:

PCQ's Fast Facts (PIMCO)

It should be fairly clear why I light PCQ a lot more today than a year ago. Aside from the stunning reversal, a 12% discount is quite attractive in isolation. While I am not suggesting PCQ is going to climb back to its prior premium highs, I do see a 12% discount as a reasonable entry point. It compensates for some of the downside risk and gives investors a chance at "alpha" if the discount were too narrow somewhat. All things considered, I view this quite positively for the time being.

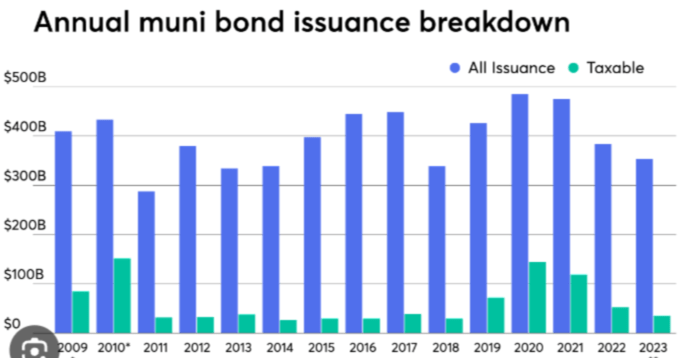

Muni Issuance Remained Tight In 2023

Another positive factor for PCQ has more of a macro-tilt. This is supply, which has come down for the sector as a whole for a few consecutive years. This trend accelerated a bit in 2023 as state and local governments found themselves with enough cash/savings to make ends meet, while simultaneously being reluctant to take on a lot of new debt with a higher interest rate backdrop. The net result is fewer new muni bonds hit the market:

{kind=link}

While this could change in 2024, for the time being it means the market is not over-saturated with new bonds. As investors rotate back in to fixed-income in order to lock-in yields before they drop, we should have more buyers chasing a smaller pool of securities. This is a favorable dynamic for the underlying bonds, and should help boost returns for the funds that hold them - such as PCQ.

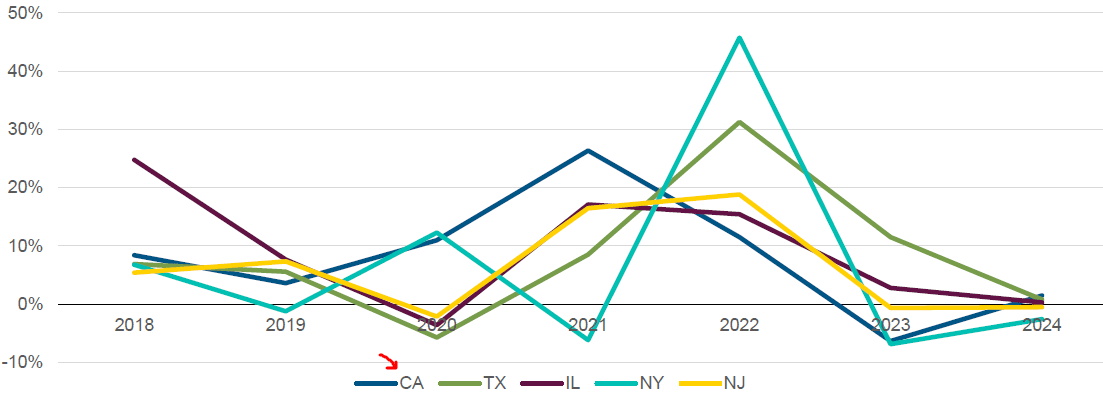

Revenue Growth To Rebound A Bit

Another point to consider is that California should enter the new fiscal year with more revenue than a year ago. While there have been plenty of negative headlines about California's budget deficit in recent months, the good news is the state had a large "rainy day" fund cushion to be utilized in just such a case. This should limit short-term defaults. And, fortunately, an improving stock market means that the state should see higher tax collections than it did this year (when 2022 stock returns were quite poor). This is a consistent trend amongst most of the "high tax "states, which make up a large chunk of the broader muni bond market:

{kind=link}

Given that PCQ holds a large portion of its debt in California-backed General Obligation ((GO)) bonds, this is an important development:

PCQ's Sector Breakdown (PIMCO)

While these revenue figures are not overwhelmingly positive, they do show YOY improvement. Further, PCQ has seen such a change in its valuation that I am willing to bet on the fund without seeing a "perfect" backdrop for California's finances. The same cannot be said last year, given PCQ's lofty valuation. But now, the fund is not priced for perfection, so seeing modest improvement within the underlying state is good enough for me.

Income Metrics Still Need To Be Watched Closely

Part of my "sell" argument last year rested on the fact that PCQ's income metrics were quite poor and would likely result in an income cut. This turned out to be a timely forecast, as the fund saw a cut in January this year. That was a clear culprit behind the terrible performance of this fund since that time, although there were other factors at play as well.

Fast-forward to today, and we aren't completely out of the woods in this respect. While PCQ's coverage ratios have improved, they aren't exactly stellar either:

{kind=link}

The takeaway for me is there needs to be a change for this fund to get back on track in terms of keeping its distribution consistent. While it has in the short-term (after the January cut), this headwind is still present. As a result, readers should monitor any developments closely for signs of deterioration.

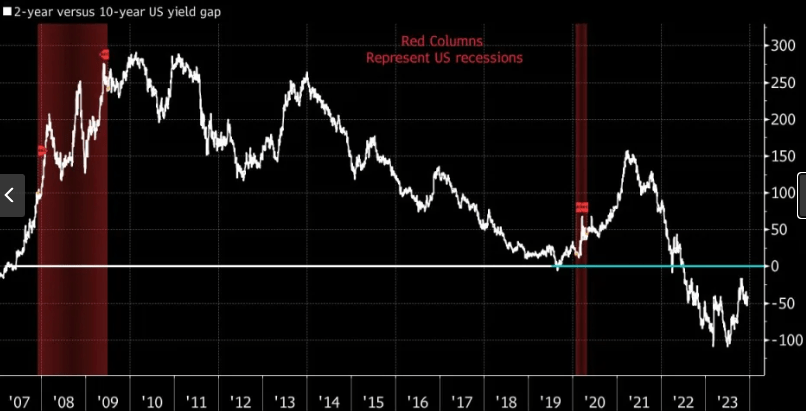

Fortunately, there is some hope on the horizon. As readers probably are aware, part of the problem facing leveraged CEFs (PCQ included) has been the inverted yield curve. This has made short-term borrowing more expensive, and limited longer-term opportunities at the other end of the curve. Since leverage works by borrowing cheaply and investing for a higher income stream with longer-dated securities, leveraged CEFs faced a world of hurt for most of the year. But the go-forward outlook has improved because the yield curve, while still inverted, has steepened considerably:

{kind=link}

What this shows is a major headwind has begun to trend in the right direction for investors in these types of funds. While the curve remains inverted and that will continue to pressure PCQ right now, I am optimistic this will normalize in 2024 and that will prove to be a tailwind for leveraged CEFs of most stripes. Similar to the state revenue attribute, I am okay with this balanced outlook supporting a buy for PCQ given the fund's discounted price. It reflects some of this risk, which wasn't the case a year ago.

A Reminder On Who This Product Caters To

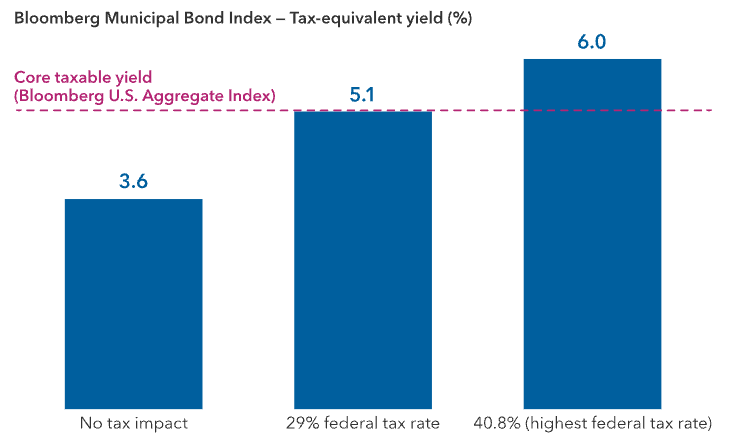

My final point touches on the broader fixed-income market, and who is best served by utilizing municipal bonds when allocating a portion of their assets to fixed-income. For residents of California, PCQ offers those residents a way to shield some of their income from local, state, and federal taxes. For those in the upper-income brackets, this can mean considerable savings!

But that is the precise point I want to harp on. Those in the upper-income brackets see this benefit. If you are not realizing a significant amount of tax savings from these vehicles, then traditional, taxable bonds may be more appropriate for you. This is because the aggregate bond market (made up of treasuries, corporates, and mortgages) can yield more than munis if maximizing tax savings is not considered:

{kind=link}

This is important since investors have many options to choose from. When considering PCQ, readers should contemplate what other California-focused muni funds are out there. But they should also evaluate whether non-muni funds may offer higher yields and returns. We don't invest in a vacuum, so the attractiveness of munis against other fixed-income sectors is something that should always be on the table for analysis.

With that said, I do see a good story ahead for bonds in 2024. At this moment, U.S. households are under-exposed to bonds. With lower interest rates on the way, I would expect this to even out towards historical averages. That could result in a nice bull-run for bonds overall:

Households Exposure To Fixed-Income (As a % of total assets) (Federal Reserve)

The conclusion I draw here is that bonds are set to rise in the new year. This will include munis (and PCQ) but other sectors as well. So place your bets where you like, but make sure it is in the area where you are getting the largest bang for your buck.

Bottom-line

PCQ was a darling that fell out of favor in a fast and furious action. With a high premium and a distribution cut, the fall from grace was painful to watch (and likely more painful to experience first-hand).

While those wounds are probably still sore from anyone holding PCQ over the years, the good news is that better days are probably ahead. The fund's premium to NAV has turned into an attractive discount. The income metrics, while not great, have improved. Further, bonds as a whole are positioned to see gains in the new year, including California's muni bonds. As a result, I feel comfortable upgrading this fund to "buy", and I would suggest readers give the idea some thought going forward.

For further details see:

PCQ: One Year Later, A Vastly Different Story Can Be Told