PCQ - PCQ: The Time To Sell Has Passed

Summary

- As 2022 was coming to a close, PCQ was one of the few tickers I cover that I placed an outright "sell" on. Since then, it has dropped near 30%.

- This has come at a time when munis have generally recovered after a difficult year. Looking ahead, I still see bright spots for the sector as a whole.

- With a large drop, this fund sits with a valuation right at par. This is favorable and in stark contrast to the double-digit premium the fund traded at for years.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO California Municipal Income Fund ( PCQ ) as an investment option at the current market price. The fund invests primarily in California municipal bonds, and therefore seeks to provide current income which is exempt from federal and California income tax. The fund normally invests at least 90% of its net assets in municipal bonds that pay interest that is exempt from federal and California income tax.

This is a fund I was quite bearish on when 2022 was wrapping up. I saw a distribution cut in January as a likely scenario, and expected heavy losses post-cut. In hindsight, this outlook was spot on. PIMCO did announce an income cut for PCQ when January got underway and the fund has lost almost 30% as a result:

Fund Performance (Seeking Alpha)

This is certainly a scary return and does not inspire confidence. But for this review I will consider what the future holds, not dwell on the past.

In this vein I see merit to upgrading my rating. I was torn between a "buy" and a "hold" and reluctantly said "hold" because the recent volatility could spur continued volatility. This means that for those who do buy now it will not likely be a straight shot higher. But I also believe the worst is behind us and there are some positive attributes that warrant buying California's muni bonds as a whole. This review will discuss the reasons behind this rating upgrade.

The Selling Has Wiped Away The Excessive Premium

I will start with a look at valuation. This was central to my "sell" opinion back in December. It is important because I generally viewed municipal bonds favorably as we entered 2023, but I saw the hefty premium coupled with the potential for a distribution cut as too ominous for buying PCQ. While there is not a lot of "good" news when it comes to seeing a fund fall 30%, the one thing that does stand up is this fall from grace has resulted in PCQ now offering investors relative value. What I mean is - the fund had a whopping 48% premium when I wrote about it in December. Now, with the drop in price and subsequent strength in the underlying bonds, this premium has been wiped clean away:

PCQ's Valuation (PIMCO)

The obvious takeaway here is that PCQ is no longer at risk of such a massive drop going forward due to an untenable premium. That premium was persistent for a long time, causing some investors to ignore it (the same can be said for other PIMCO CEFs at this very moment!). But as those who have followed these leveraged products for years, as I have, they know that the premium eventually catches up to them. PCQ has dealt a harsh blow to its holders by reversing years of precedent, and the result has not been pretty.

Fortunately, this gives new positions some merit. While I would have a hard time coming up with an argument to buy a fund with a 40% premium (regardless of other merits), this headwind is no longer present. We can now evaluate PCQ with an overweight emphasis on its current income, holdings, and prospects for the broader muni sector without the glaring valuation issue overriding all those attributes. This is key to supporting why I see a reason for upgrading my outlook at the moment.

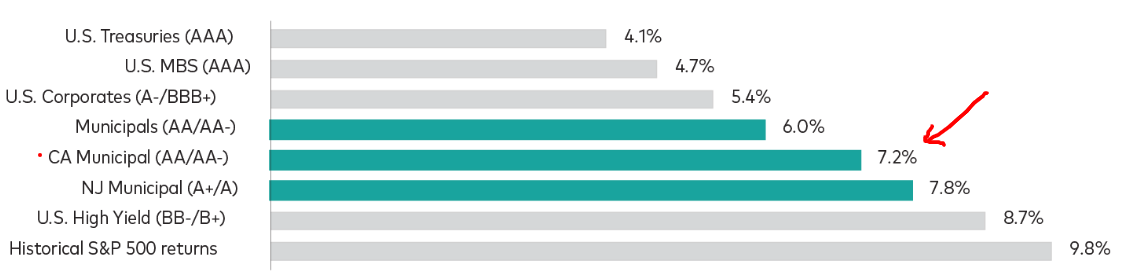

High-Tax Cali Drives Muni Interest

I will now shift to why I keep Cali munis on my radar. This is true in all economic cycles for a couple of reasons. One, California is one of the biggest issuers of muni debt - so a follower of this space should keep a keen eye on this state to understand how the sector is operating. Two, because of California's high tax structure, these bonds are extremely desirable for in-state residents that earn a lot of income. After the drop in bond prices last year, there is quite a bit of inherent value at current levels for those needing to save on taxes. For example, if we assume the highest tax bracket for an in-state (California) resident, the sector is yielding over 7% on a tax-adjusted basis:

Tax-Equivalent Yields (Bloomberg)

{kind=link}

This is relevant to PCQ because even with the hefty income cut last month, the current yield sits at around 4%. With tax savings factored in, that yield does get near the 6% range. Hard to argue against that high of a yield, especially with the Fed slowing down on rate hikes and inflation easing.

The conclusion I draw here is that California's muni debt is attractive on a relative basis. With yields in the 5-7% range - depending on the fund and an investor's tax bracket - this compares very well to other fixed-income products. To me, this suggests that buying in to this sector theme will serve investors well in 2023.

California's State Reserves Bring Comfort

Another reason for finding value in the Sunshine State is the "rainy day" balance in the state's coffers. This is an item that is going to come in useful in 2023 if we do enter a recession and state revenues come under pressure. Since this is the scenario I would personally predict, I view Cali's reserves as an extremely important consideration right now.

The good news is this is an aspect where the state is better than average. While the median among all 50 states is to have a rainy day fund that covers almost a month and a half of spending, California has almost double that median, as shown below:

Rainy Day Funds (The Pew Charitable Trusts)

This doesn't put California at the top of the list by any means, but it is certainly near the top. This is critical to understanding the longer term health of California's finances and should provide some level of comfort for positions for the time being.

The relevance here extends to PCQ because California's GO bonds (both state and local) dominate the fund. So it is extremely dependent on performance by those bonds backed by the credit standing of Cali's municipalities:

PCQ's Sector Allocations (PIMCO)

One key point to keep in mind here is that California has a more volatile tax base than the average state. It has very high taxes on upper-income residents, which is partly the reason for the excess rainy day fund going in to 2023. With last year being an exception, stock markets had generally been performing well over the past decade. This means those at the top were likely enjoying strong returns and, as a follow through, were paying a fairly high chunk of taxes to their state and local governments.

The challenge here is whether that will continue going forward. Last year was difficult, and this year could be as well if we do hit a recession. This means the spike in personal income tax collections within the state may not remain at such a high level. While California has the current reserves to manage this risk, it is still something that California's muni investors should take seriously.

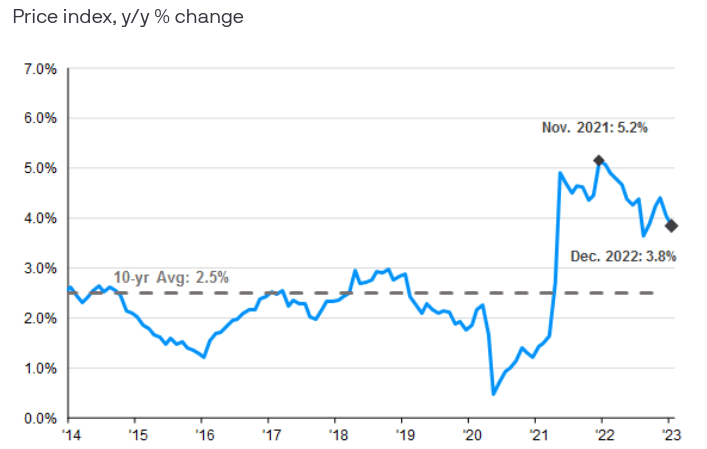

Fixed-Income Gets Boost From Lower Inflation

I will now shift to a more macro-view for fixed-income. This is relevant for munis (and PCQ), but also for any bond asset class - most of which were hammered last year in sync!

Again, we entered 2023 after a very difficult year for bonds. Things were abnormally bad and that has set us up for a nice rebound in January. Personally, I see gains continuing for IG debt of all stripes primarily because yields are attractive and inflation is easing. With this backdrop it is easy to see why investors would begin to gravitate towards income-oriented options:

PCE Core Services (ex-Housing) (Federal Reserve)

{kind=link}

I bring this up because I want to illustrate why I am generally bullish on high-grade credit going forward. With inflation pressures easing, there is an argument for buying fixed-income that really was not present last year. We don't see sell-offs like the one in 2022 occur very often. Rather than use it as reason to avoid this asset class I see it as a rationale for buying in. This extends to munis/PCQ but also corporate debt and treasuries as well.

Muni Supply Remains Tight, Supporting Prices

My last point regards munis has to do with supply and demand. This is another factor that makes me cautiously bullish on the sector going forward. While we have only wrapped up one month so far in the new year, the net result was a decline in issuance year-over-year. While monthly figures can change (and often do) vastly from month to month, it does support current prices for the time being:

Muni Supply (By Year) (Goldman Sachs)

The backdrop this provides is that there continues to be a balanced muni market out there. This means that underlying prices are not at risk of devaluing due to a sharp increase in supply (higher supply can mean lower prices if demand does not increase by a similar amount).

With supply tight and prices lower than they were a year ago, it is hard not to like the sector here. PCQ is a perfect example of this with a valuation that is dramatically lower than where it used to trade at. This supports my belief that moving PCQ to at least a "hold" is the right move.

Bottom-line

PCQ was ripe for a fall and fall it did. Sitting with a ridiculous premium and facing a steep income cut, the writing was on the wall. That writing turned out to be painful for holders of this CEF - but it offers opportunity for those either waiting on the sidelines or looking to add to their positions. The fund now sits right near par value, the yield remains attractive for California residents, and supply in the muni space is tight. All of these factors suggest PCQ's worst days are behind it. Therefore, I believe a "sell" rating on this fund is no longer warranted and readers who are interested in this space have merit to giving long positions some consideration at this time.

For further details see:

PCQ: The Time To Sell Has Passed