PDI - PDI: A Story About Good Leverage And Quality Holdings

2024-01-08 17:11:43 ET

Summary

- PIMCO Dynamic Income Trust offers a 15% current distribution rate and focuses on diversified exposure across asset classes, sectors, and geography.

- The fund takes advantage of older, cheaper, fixed rate leverage to overweight mortgages and high yield bonds.

- PDI does come with some risks discussed in this column, and its allocation should remain small.

- I am buying and adding this fund to my CEF portfolio.

Introduction

With the Effective Fed Funds Rate now sitting at its potential peak, something I recently wrote about here , investors are searching for opportunities to take advantage of the high yields before they go away. I believe this retreat back to lower rates will take time, likely through 2026.

This gives us the opportunity to hold onto good closed-end funds for a few years before traditional bonds start to look more attractive from a risk/reward perspective.

PIMCO Dynamic Income Fund ( PDI ) is positioned well to take advantage of this opportunity in the market. In this column, I am going to cover why I believe PDI is a buy in the current market and why it deserves a place in most income portfolios. My thesis on PDI is broken into three key points:

- PDI is positioned to take advantage of dislocations in multiple markets, spreading risk across sectors, regions, and asset classes.

- The fund's use of leverage, currently at 40%, looks to be profitable as their cost of carry is low compared to the high yields of emerging market and non-investment grade bonds.

- PIMCO screens the holdings thoroughly to ensure that credit risk remains low comparatively to the income the fund can produce.

This has resulted in a fund that can generate a 15% yield and has been able to provide absolute returns to investors in excess of 10% p.a. since inception. Included in the chart of its price, NAV, and return below is a comparison to the 10-year UST.

Brief Overview

At a glance:

-

Price: $18.47.

-

Distribution Rate:15.73%.

-

Premium/Discount: 7.95%.

-

Leverage-Adjusted Duration: 3.20yr.

- Effective Leverage: 40.44%.

-

Beta: 0.66.

-

Volatility (1Y): 15.18%.

-

Net Asset Value: $4,734,000,000.

-

Expense Ratio (less interest/carry): 1.92%.

Description as per PIMCO -

Offering access to PIMCO's best income-generating ideas across multiple global fixed income sectors, the multi-sector fund seeks current income as a primary objective and capital appreciation as a secondary objective.

The fund normally invests worldwide in a portfolio of debt obligations and other income-producing securities of any type and credit quality, with varying maturities and related derivative instruments. The fund's investment universe includes mortgage-backed securities, investment grade and high yield corporates, developed and emerging markets corporate and sovereign bonds, other income-producing securities and related derivative instruments.

{kind=link}

Portfolio

As mentioned above, PDI invests in debt and credit across several sectors, geographies, and asset classes. This offers investors a layer of diversification to reduce some risk.

Figure 4 (PIMCO)

Note the very heavy exposure to mortgages, specifically non-ABS. A large source of yield for the fund is generated from this leveraged position in these mortgages, so it is important for investors to note here that PDI has a very large exposure to real estate via these mortgages.

With mortgage rates currently near decade highs, it seems like a good idea to load up on these bonds now, but it does add a good chunk of concentration risk to the fund.

These mortgages also add a layer of risk via their callable nature. They are not "callable" in the traditional sense, but mortgages are eligible for early pay-off or refinancing on a whim.

In the chart below, you can see how the leverage magnifies the volatility of PDI compared to a fund of funds.

The essential part to get right for a CEF of this nature is selecting the right holdings in the right ratios. PDI accomplishes this via diversifying across sectors in their high yield and corporate bond holdings.

Figure 7 (PIMCO)

The fund typically invests across the lower end of the credit spectrum, often taking on unrated credit, which currently comprises almost 40% of assets.

Figure 8 (CEF Connect)

Leverage

You can't discuss CEFs without talking about leverage. It's one of the things that sets CEFs apart and one of the things that can make them very risky vehicles.

PDI has a maximum allowable leverage of 40%, which it currently is at. I believe this is prudent as we are now around lows for many of the instruments PDI is holding. This tactical use of leverage has allowed the previously discussed outsized position in mortgages and an increased position in high yield bonds.

The reference I made to "good leverage" in the title is an allusion to PDI's use of reverse repurchase agreements, or "repos," to secure their leverage.

These are set transactions akin to collateralized loans that come with specific set rates. Many of these agreements were made when rates were lower than today, meaning that the carry PDI pays for its leverage is less than the current risk-free rate.

Figure 10 (CEF Connect)

Note: the 12/05/23 repo shown above has passed and was replaced with a similar agreement expiring in June '24 with a 5.5% rate, above the risk-free rate.

This gives PDI the advantage of being able to buy basically any instrument and get a higher yield than they have to pay to borrow money. Even as they have to turn over these repos in March and acquire new ones at significantly higher rates, likely 6-7% as some of their holdings already suggest, the assets they hold are still able to pay for the carry and more.

Management has proven this with their dividend consistency.

Note: On December 14th, 2022, PDI issued a "special cash distribution" of $0.65/share as well as their typical $0.22/share distribution that occurred on 12/09/22.

Figure 12 (PIMCO)

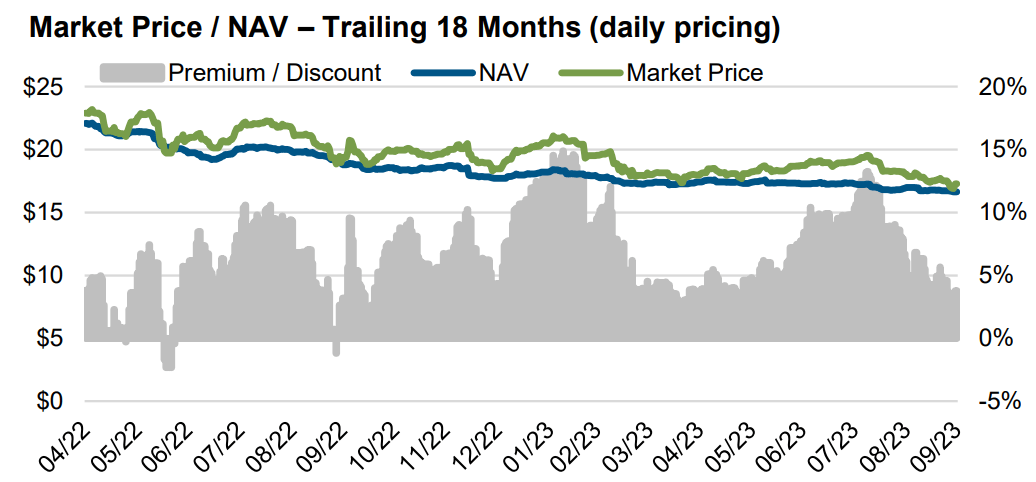

Premiums & Discounts

As with other CEFs, PDI tends to trade at a premium to its NAV. This premium is slight compared to some others I've covered, but still presents a risk to investors as they have to pay more than the fund is worth to buy shares.

While it used to trade at a discount, PDI merged with several other PIMCO CEFs in 2021. Since then, it has traded at a premium to NAV, and that trend shows no signs of going away. I am not covering the merger here, since it is "old news," but you can read great coverage from a fellow analyst here .

There is not much to discuss with the premium, since it has been fairly consistent since the merger, so just note that it may change or could come back to NAV, widen, or turn to a discount.

The chart below starts at the date of the merger of PKO and PCI into PDI, December 10, 2021.

Allocation

PDI earns a buy rating from me. For aggressive investors who are looking for CEFs to help increase portfolio yield via leverage. I recommend against holding more than 5% of an income portfolio in a single CEF.

For the moderately risk-averse who want to diversify their traditional bond holdings with CEFs, PDI is a great choice, but should occupy no more than 2% of an income portfolio.

With funds that offer incredibly high yields like PDI's 15% distribution rate, a little can go a long way.

Counterpoints

It is important to highlight the downsides to any fund that I do positive analysis for. Here are several of the potential issues investors may have with PDI.

- First, there is a premium to the fund of about 8%. This means that investors are overpaying for the NAV. There is no guarantee that the fund's price will return to NAV, or if the premium may widen or turn into a discount. This unknown is one of the most significant risks to consider with CEFs.

- This fund carries significant volatility when compared to traditional bond indices like MBB or CMBS. This could be above the risk tolerance of many income investors who are used to holding bond indices over-leveraged CEFs.

- Lastly, the thesis hinges on the current Fed Funds Rate being at a peak. If economic data changes its current trends and worsens, the Fed may raise rates. This would result in losses for PDI investors, as the fund has a positive duration of about 3yr.

Conclusion

The PIMCO Dynamic Income Fund offers investors an opportunity to leverage currently high mortgage rates and quality corporate and high yield bonds. In our current rate projection, we are likely at peak rates, which means now is the perfect time to buy into leveraged bonds.

PDI does have some risks that investors need to be aware of, such as its large exposure to mortgages, its premium over NAV, and macroeconomic concerns like a change in the Fed's course.

I give PDI a buy and will be adding it to my small CEF income portfolio.

Thanks for reading.

For further details see:

PDI: A Story About Good Leverage And Quality Holdings