PDI - PDI: Dividend Underwater A Bet On Interest Rates

2023-11-28 04:02:07 ET

Summary

- PIMCO Dynamic Income Fund has significant exposure to non-agency MBS and high yield credit, posing risks to its cash flow streams.

- PDI has delivered lower returns compared to the S&P 500, but still offers a high dividend yield of 15%.

- PDI's ability to sustain its high dividend yield is uncertain, and it may need to attract additional leverage or divest positions to maintain it.

- Currently, it is a pure play bet on the medium-term trajectory of Fed Funds rate. If the interest rates do not go down, PDI would be in a serious position to cut its dividend.

About a half year ago I wrote an article on PIMCO Dynamic Income Fund ( PDI ) warning investors about three potential risks, which could impose notable headwinds for PDI investors.

The key areas of concern were the following:

- Massive exposure towards non-agency MBS . Approximately 40% of PDI's portfolio is exposed to non-agency MBS, which against the backdrop of looming recessionary risks and the overall pressure on household income could at some point impair PDI's underlying cash flow streams. Plus, if these securities were forced to experience a mark-to-market activity, PDI would suffer serious depreciation of its capital (due to a combination of higher interest rates and increased credit risk premiums for non-investment grade securities).

- High yield in struggling sectors. About 20% of PDI's portfolio is placed against high yield credit. The lion's share of this exposure is explained by junk utility companies and financial institutions, which, in my view, elevates the risk even further considering the sensitivity of these segments to higher interest rates.

- Significant leverage on leverage. To make things more interesting (i.e., going up the risk curve beyond the aforementioned positions, which already embody high risk) PDI employs additional leverage to magnify the potential returns. When I published the article back in May this year, PDI had ~41% of the total AuM backed by external leverage. The combination of rather speculative investments and additional leverage to enhance the exposure does not seem prudent, when the macroeconomic outlook (and especially the interest rate environment) is so unclear.

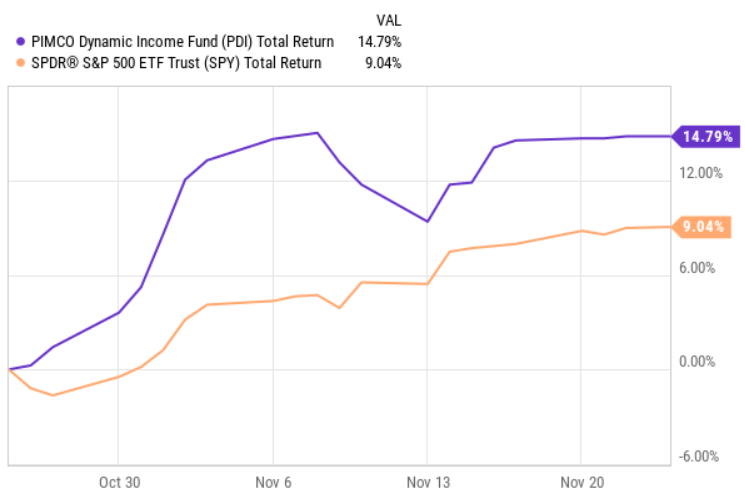

Since the publication of the article, PDI has delivered ~3% returns (on a total return basis), which is ~7% below the S&P 500.

{kind=link}

Most of the returns have come in the past month, where PDI responded very well to a more positive market's sentiment on the future path of Fed Funds rate.

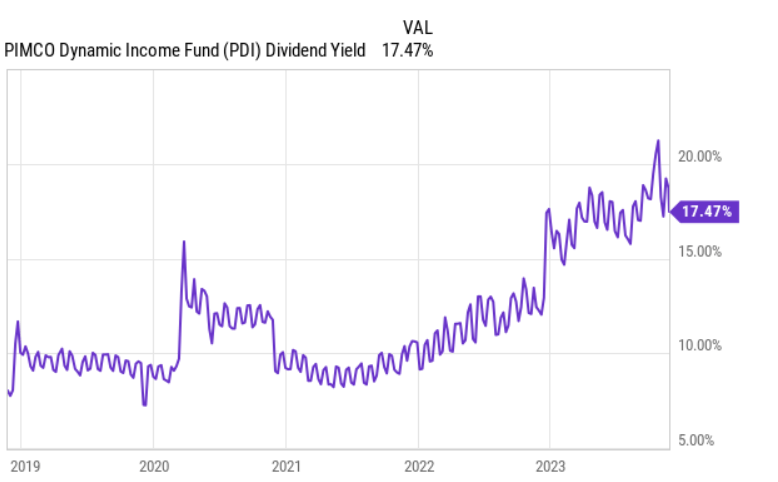

Despite the recent run-up in PDI's share price, the Fund still offers a juicy yield of 15%.

Now, the question is whether PDI will be able to accommodate this high dividend yield on a go forward basis (and not break its remarkable track record).

{kind=link}

Thesis update

In my opinion, whenever a security offers a yield that is in double digits investors have to be extra cautious to not enter into a value trap.

{kind=link}

Even looking at PDI's historical dividend yield, the level we are seeing now could be easily considered abnormal.

Let's first take a look at PDI's portfolio and check the prevailing structure of the underlying exposures.

All in all, the allocation setting has not changed in a notable fashion. We still see that PDI holds 20% in high yield credit and the exposure towards mortgage securities accounts for a bit less than 40%. Yet, now the investment amount in non-agency MBS has decreased to 25% with the remaining 15% allocated into CMBS.

There are two credit exposures, which could be deemed safe, but the invested percentage in these securities amounts to less than 3% (roughly an even split between IG credit and government bonds).

{kind=link}

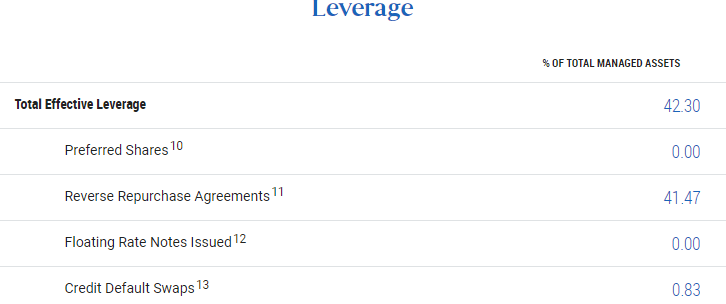

Importantly, there have not been any changes made in the external leverage segment. Currently, about 42% of the portfolio is supported by additional leverage stemming from repo agreements.

So, now when we have established that PDI has not made any material adjustments to its asset allocation strategy (which is somewhat obvious given what is stipulated in the prospectus), let's peel back the onion a bit and check whether the underlying cash flows have been sufficient to cover the expenses related to external debt service as well as the juicy dividend.

{kind=link}

What we can notice in the above reflected table is that on a YTD basis PDI is underwater when it comes to the coverage of distribution levels. Ratio below 100% means that the distributions have exceeded the net investment income generated by PDI.

This is clearly not a positive sign for PDI investors, who, in my opinion, have invested with an aim to capture reliable and juicy streams of income.

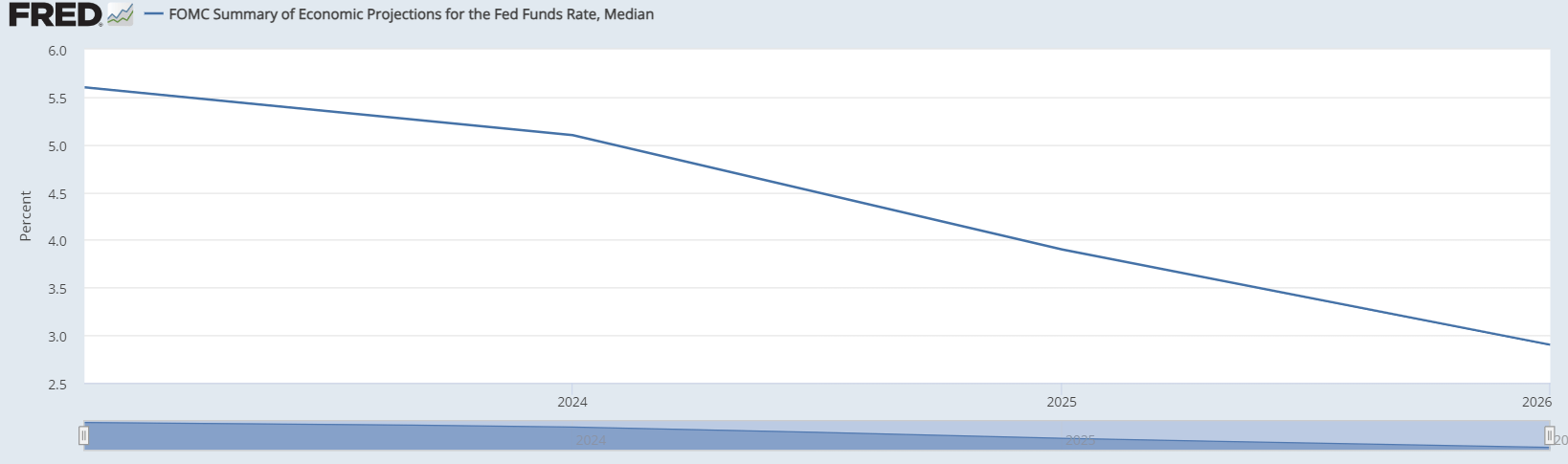

My assumption here is that PDI will try to stick to the current dividend level by either attracting additional leverage (the Fund has a bit of a room left to reach the ceiling level that is stipulated in the prospectus) or divesting some of its positions. These efforts would make sense considering the overall expectations on the normalization of SOFR already in 2024.

{kind=link}

In case the interest rates go down next years, PDI would benefit from a positive repricing of external credit that should, in turn, put off the pressure on the net investment income component thus bringing the coverage ratio above 100% again. This way, PDI would also avoid damaging its remarkable track record of distributing attractive dividends.

However, the risk with the aforementioned approach is that the interest rates turn out to be sticky and do not adjust so fast. For example, let's imagine that the SOFR stays at the current levels over the 2024. In such a case if PDI wants to stick to its dividend policy, the Fund would have to sell some of its existing positions to close the cash flow gap, thereby recognizing further losses due to mark-to-market activity of credit, which has for sure lost some chunks of value due to higher interest rates. Alternatively, there would have to be an assumption of additional leverage to avoid negative mark-to-market, which could imply even higher losses (and potentially even deeper cut to its dividend) provided that interest rates do not decrease.

The bottom line

In my humble opinion, PDI is a pure play bet on the medium-term trajectory of Fed Funds rate. For PDI investors to remain in comfort with the existing dividends, there have to be some notable interest rate cuts made by the Fed (i.e., 25 or 50 bps would not move the needle). Otherwise, the Fund will sooner or later embark on a dividend cut to protect its holdings.

If the interest rates really normalize in 2024 and do so in a meaningful fashion, investors would likely be rewarded heavily on a total return basis, effectively locking in ~15% dividend yield and experiencing notable price gains as in the past month.

It is neither long nor short for me. The recommendation remains as hold.

For further details see:

PDI: Dividend Underwater, A Bet On Interest Rates