PDI - PDI: High Risk High Yield

- PDI has a 13% distribution yield based on NAV.

- It is an unrestricted fund, meaning the manager can invest in almost any sector and geography, as well as throughout the capital structure.

- PDI's volatile performance makes me hesitant to recommend it.

I am constantly on the lookout for high-yielding funds and investments for my own portfolio. I recently wrote an article on the Simplify Volatility Premium ETF ( SVOL ) which generates income by short-selling VIX futures. In this article, I will take a look at the PIMCO Dynamic Income Fund ( PDI ), a closed-end fund ("CEF") that is more traditional in its approach to generating income.

While I find PDI's 13% NAV-based distribution yield attractive, I have reservations regarding the fund's volatile historical performance. My fear is that PDI is really just a high-return/high-risk fund that pays a high distribution yield to attract investors.

Fund Overview

The PIMCO Dynamic Income Fund is a $4.5 billion closed-end fund that seeks to generate current income by investing in debt and other income-producing securities across different geographies and credit quality. PDI offers access to PIMCO's best income investment ideas across an investment universe spanning mortgage-backed securities ("MBS"), investment grade ("IG") and high-yield ("HY") corporates in developed and emerging markets ("EM"), sovereign bonds, and other income-producing securities like preferred equities and derivatives.

Closed-end Funds, for those not aware, are a mix between the traditional open-ended Mutual Funds ("MF") and Exchange Traded Funds ("ETF"). Like ETFs, CEFs are traded on stock exchanges and the market price of CEFs fluctuate like that of other publicly traded securities. Unlike ETFs that typically track an index, CEFs tend to be actively managed.

ETFs and MFs can issue or redeem new units depending on supply and demand, thus their market price tends to track their Net Asset Value ("NAV") per share. Unlike ETFs and MFs, CEFs have a fixed number of units that don't change unless the CEF does a secondary offering, hence CEFs can trade at significant premium or discount to their NAV.

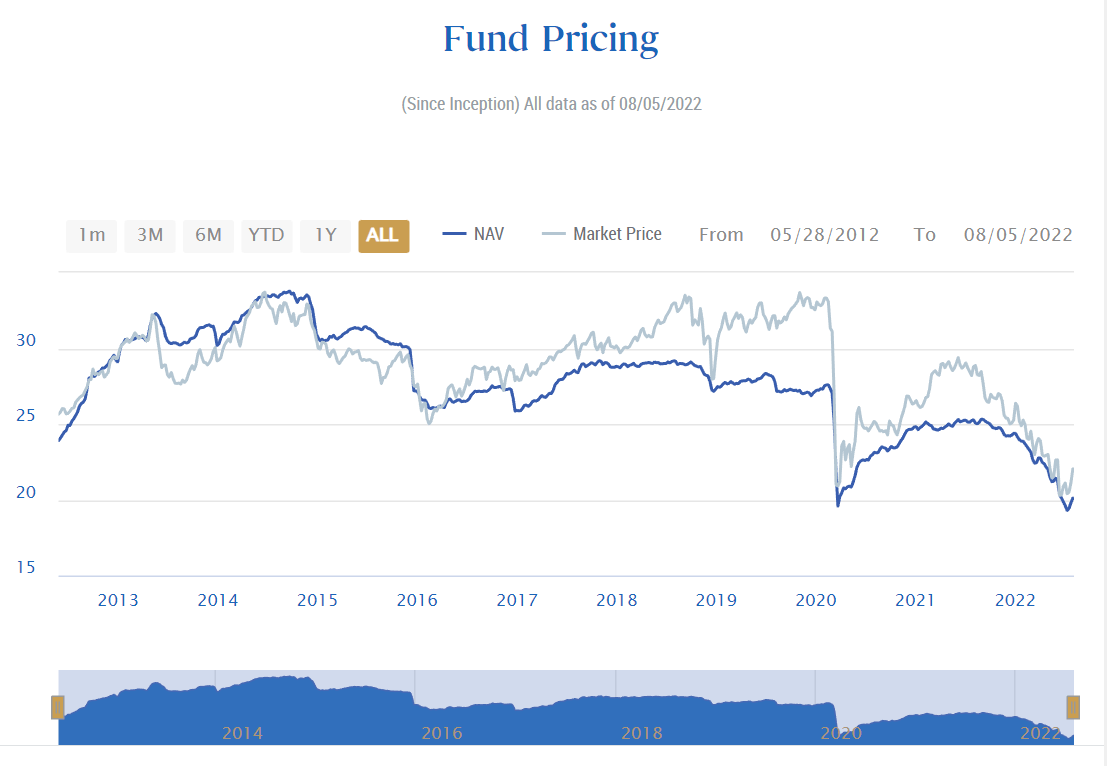

For PDI, it has historically traded at a premium to NAV, as shown in Figure 1, due to the attractive nature of its distribution yield. However, there are certain periods when the fund trades at a discount to NAV, such as in the early years of the fund's operations, between 2013 to 2016.

{kind=link}

Strategy

From PDI's prospectus, the fund's stated investment strategy is:

The Fund seeks to achieve its investment objectives by utilizing a dynamic asset allocation strategy among multiple fixed income sectors in the global credit markets, including corporate debt (including, among other things, fixed-, variable- and floating-rate bonds, bank loans, convertible securities and stressed debt securities issued by U.S. or foreign (non-U.S. and emerging market) corporations or other business entities), mortgage-related and other asset-backed securities, government and sovereign debt, taxable municipal bonds and other fixed-, variable- and floating-rate income-producing securities of U.S. and foreign (including emerging markets) issuers. The Fund may invest in investment grade debt securities and below investment grade debt securities (commonly referred to as "high yield" securities or "junk bonds"), including securities of defaulted and stressed issuers. The types of securities and instruments in which the Fund may invest are summarized under "Portfolio Contents" in the accompanying Prospectus. The Fund cannot assure you that it will achieve its investment objectives, and you could lose all of your investment in the Fund.

Having been a hedge fund CIO and written my fair share of fund prospectuses, this has to be as vague as one can get with respect to a stated investment strategy. Essentially, the fund has 'carte-blanche' to invest in any sector, up and down the capital structure (from bank loans to convertible bonds and distressed debt), including common stocks due to a corporate actions (restructurings and convertible bond conversions). PDI's ability to invest in anything/anywhere resembles that of hedge funds.

Dividend & Yield

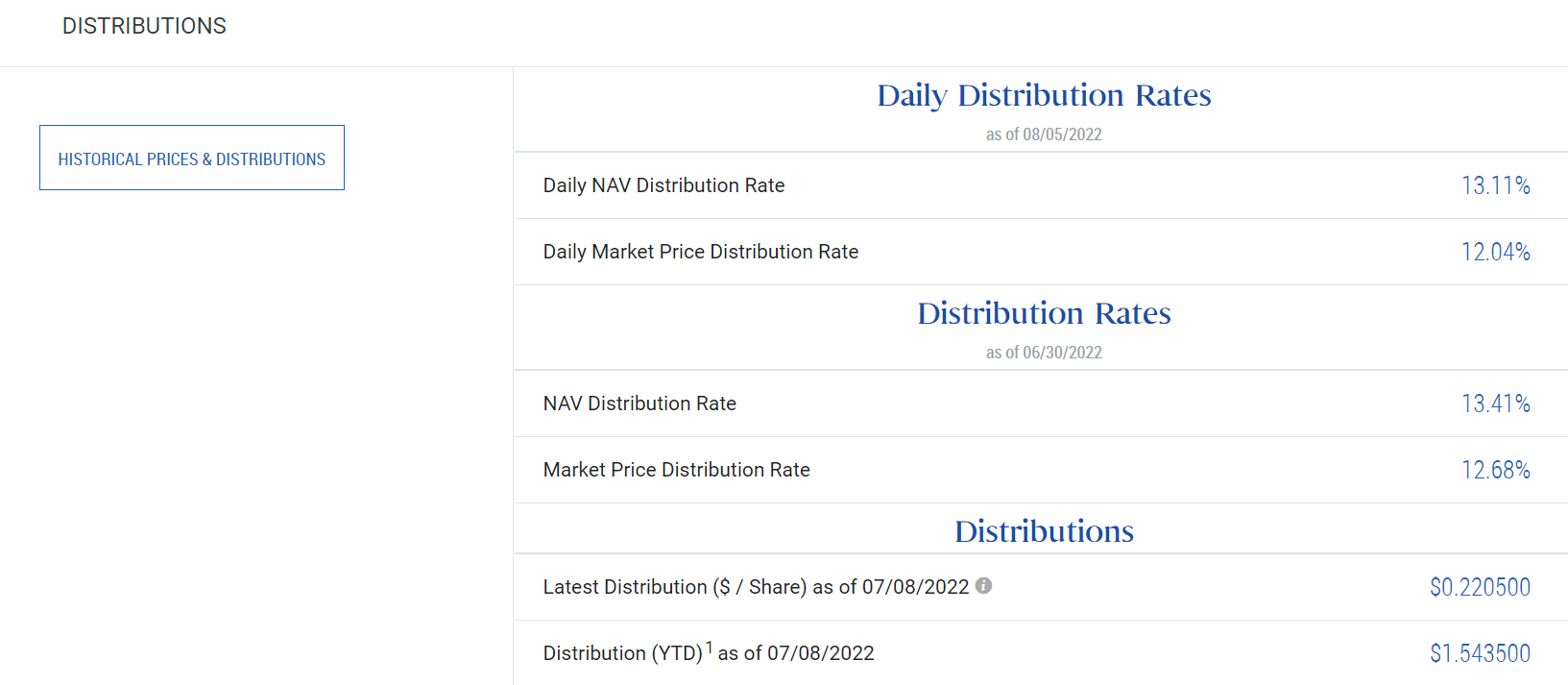

According to PIMCO's website, PDI currently has a 13% distribution yield, based on NAV (Figure 2). It's latest distribution was $0.2205 per share, for a 10% annualized yield on market price of $22 per share. YTD, it has paid $1.5435 per share in distribution.

{kind=link}

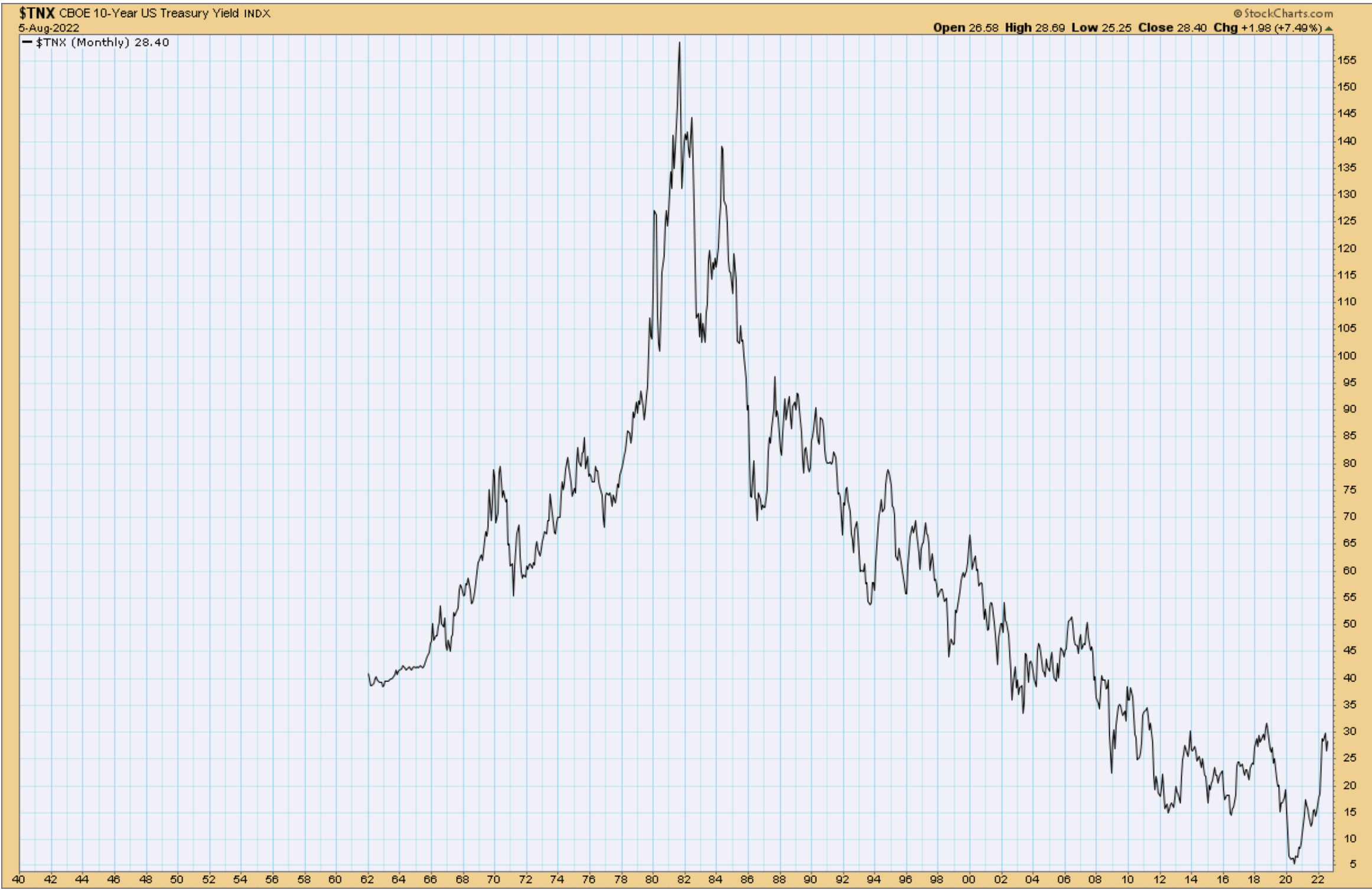

Although yields have increased in the past few months with the US 10-year treasury yield now at 2.75%, they are still low by historical standards (Figure 3). In a low-yielding world, how is PDI able to achieve double-digit distribution yield?

Figure 3 - Long term 10 year treasury yield (stockcharts.com)

{kind=link}

PDI achieves double-digit returns primarily through securities selection and leverage . With $4.5 billion in equity, the fund manages a $8.7 billion portfolio, giving effective leverage of 49% (Figure 4). This means that for over $1 of equity, the fund effectively buys $2 of assets. For example, if PDI can buy $2 of a 6% corporate bond while borrowing $1 at 3% themselves, then PDI can earn 9% yield on its $1 in equity.

{kind=link}

Portfolio Composition

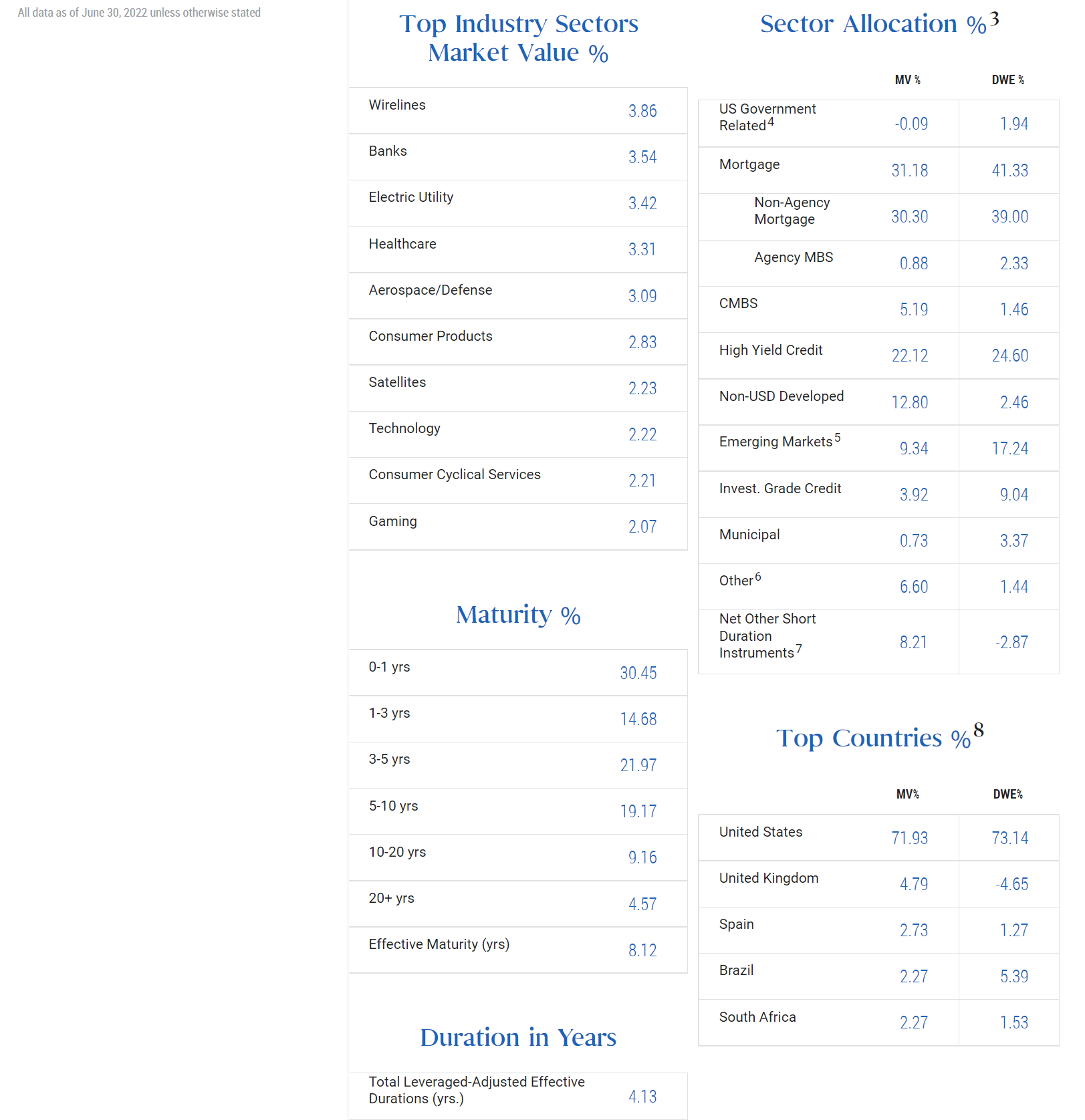

PDI's website gives a pretty good overview of the fund's holdings in terms of sector allocation and geographical allocation. As we can see from Figure 5 below, the fund is highly non-traditional, with large allocations to MBS, high-yield credit, non-USD developed countries, and emerging markets.

{kind=link}

Fund Returns

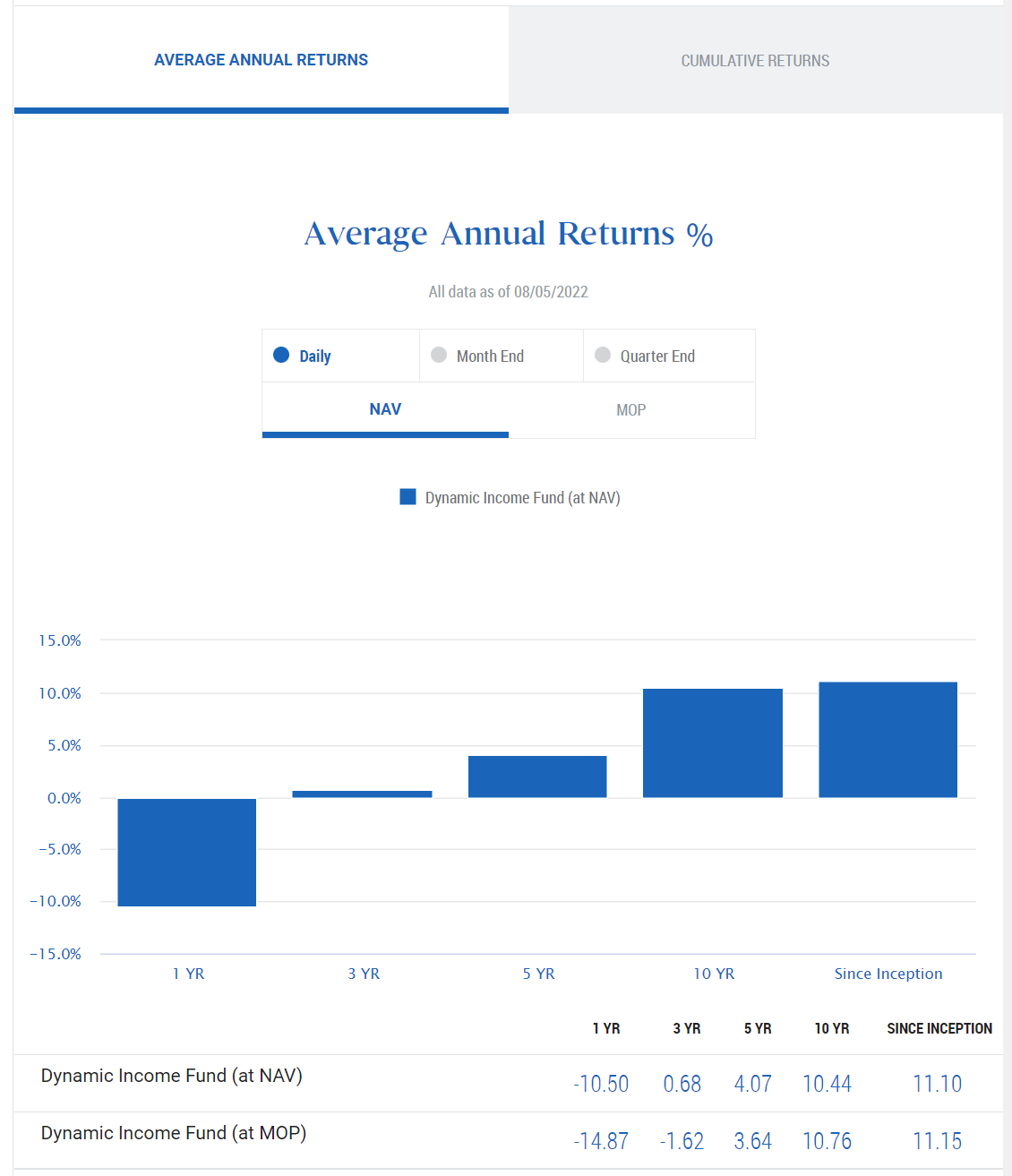

This non-traditional, hedge fund-like allocation has allowed PDI to deliver historically strong absolute returns (Figure 6). Since its inception in 2012, PDI has delivered average annual returns of 11.1%. However, performance has been weaker on a 3-year basis, with average annual returns of only 0.68%.

{kind=link}

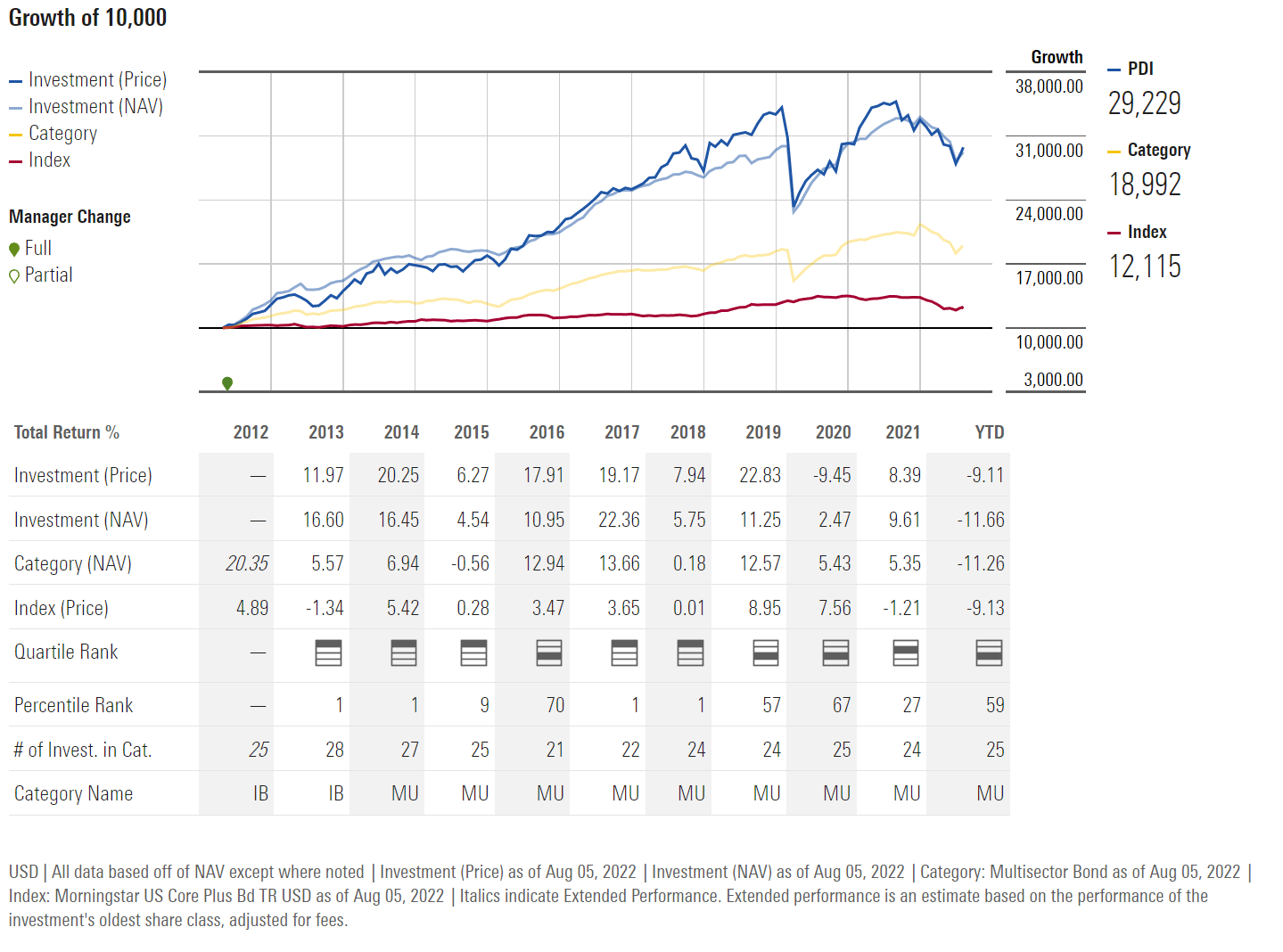

In fact, if we analyze PDI's returns on an annual basis, we can see that absolute returns were strong from 2013 to 2019, however, the past 3 years have not been as good. Morningstar ranked PDI's returns as first quartile in years 2013 to 2015, 2017, and 2018, but second or third quartile in other years (Figure 7).

Figure 7 - Morningstar ranking of PDI returns (morningstar.com)

{kind=link}

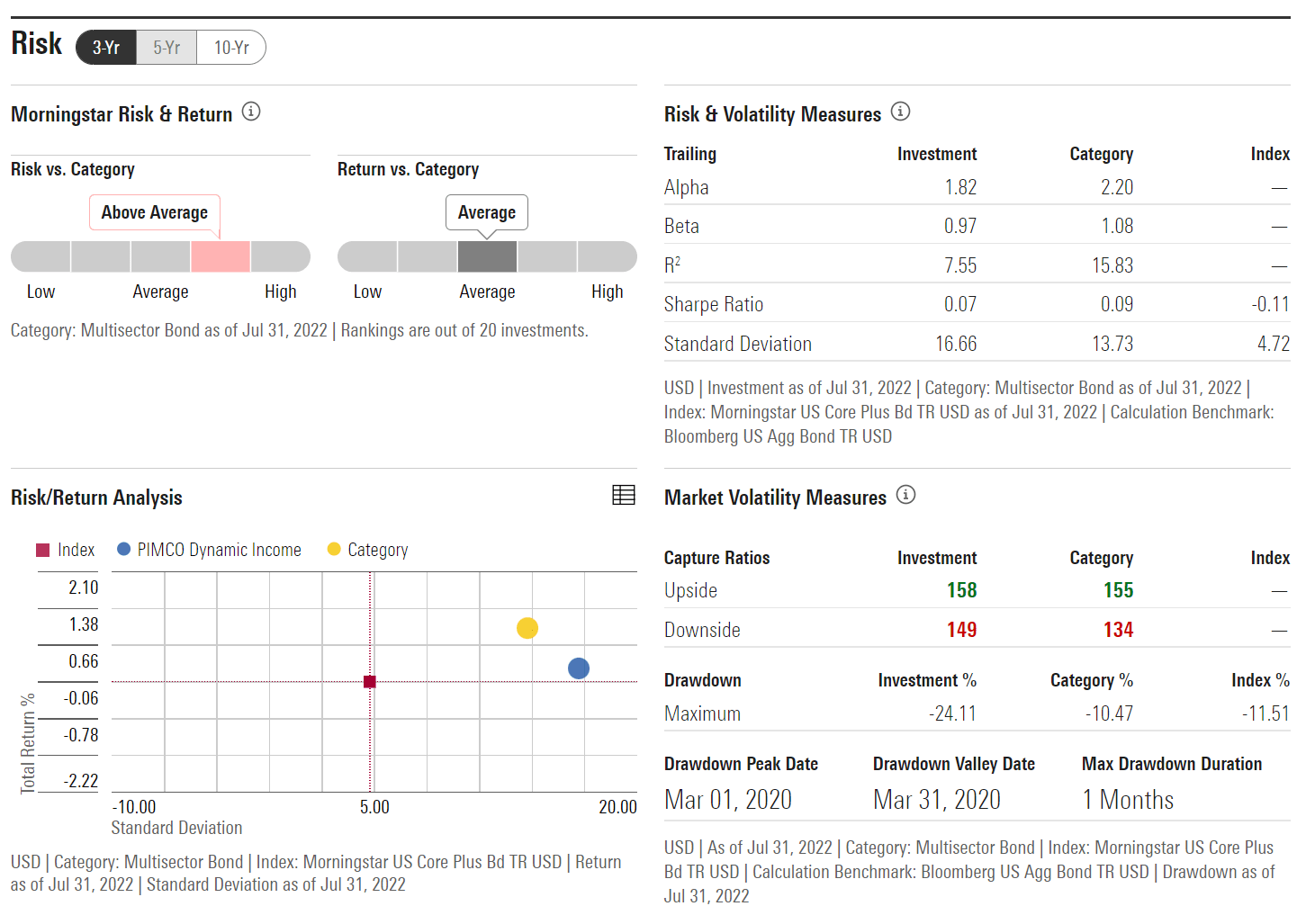

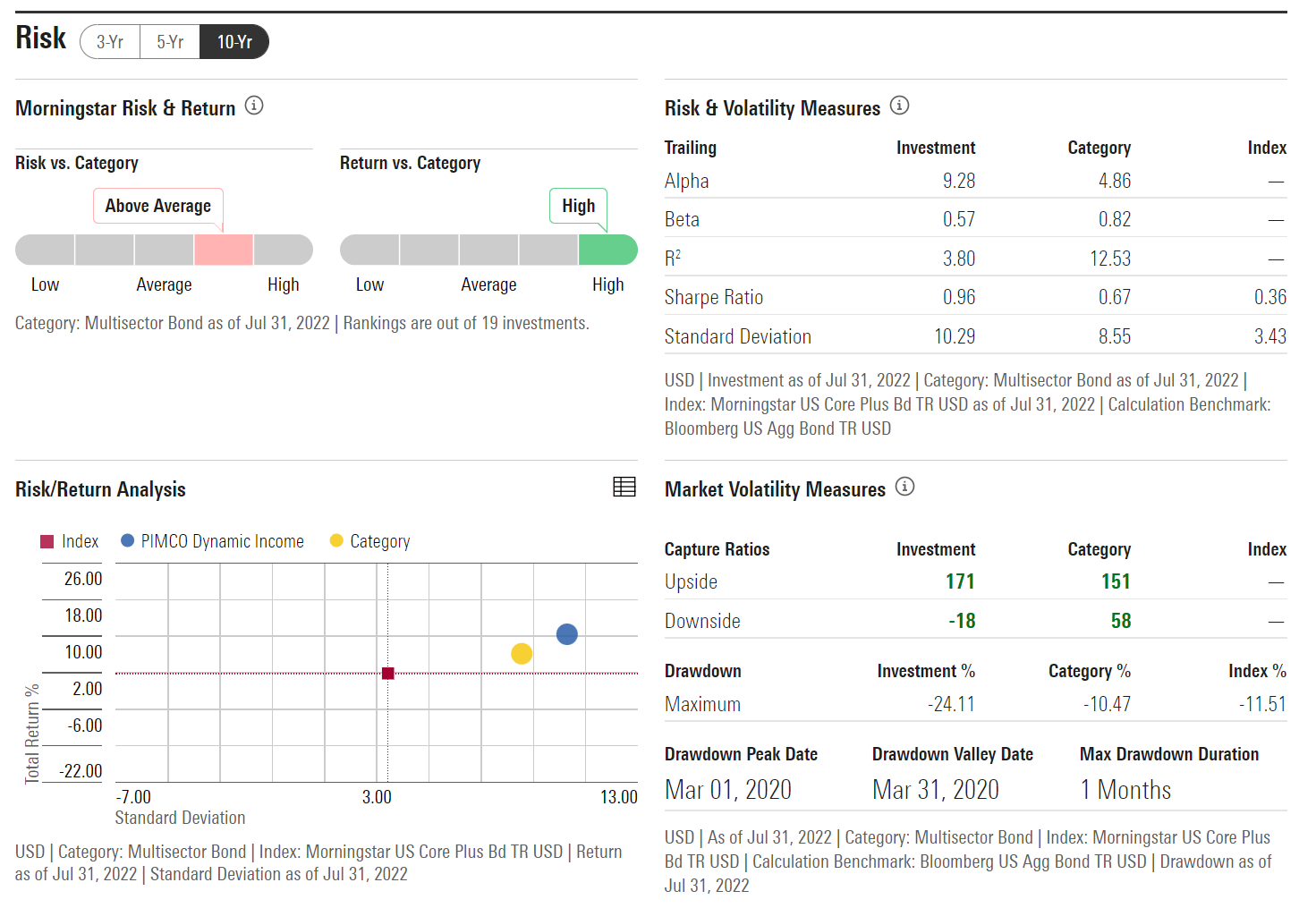

Unfortunately, this is the drawback of investing in an unrestricted strategy; the portfolio managers are only human and can go through hot and cold streaks. On a 3-year basis, PDI has lower returns and higher risk (volatility) than the Morningstar Category of "Multisector Bond Funds" (Figure 8). On a 5 and 10-year basis, PDI has higher returns, but also higher risk (Figure 9).

{kind=link}

{kind=link}

With this kind of return/risk profile (consistently higher volatility with inconsistent returns), investors must ask themselves whether the manager truly generates 'alpha', or is it just a high return/high risk 'beta' strategy.

In fact, PDI's 10-yr Return/Risk ratio of 10.42/10.29 is more like the SPDR S&P 500 ETF Trust's ( SPY ) 13.69/13.90 than the bond index's 1.84/3.43.

Fees

PDI certainly charges fees like a quasi-hedge fund, with a management fee rate of 1.1% and total expense ratio including interest, of 2.78%. For context, large, passive bond funds such as the Vanguard Total Bond Market ETF ( BND ) and the iShares Core U.S. Aggregate Bond ETF ( AGG ) charges 0.03% in management fees.

Figure 10 - PDI charges high management fees (PIMCO website)

{kind=link}

Key Risks

Leverage & Interest Rates

As we mentioned above, PDI uses leverage to enhance its distribution yield. Leverage is not necessarily a bad thing, as long as it is managed correctly and is not used excessively. However, it does introduce some additional risk to the portfolio.

In general, fixed income securities fall in value as interest rates increase. This is because future cash flows are discounted at higher interest rates. For a leveraged fund like PDI, this can become a double headwind, as its assets fall in value while the interest rate it pays on its loans increase.

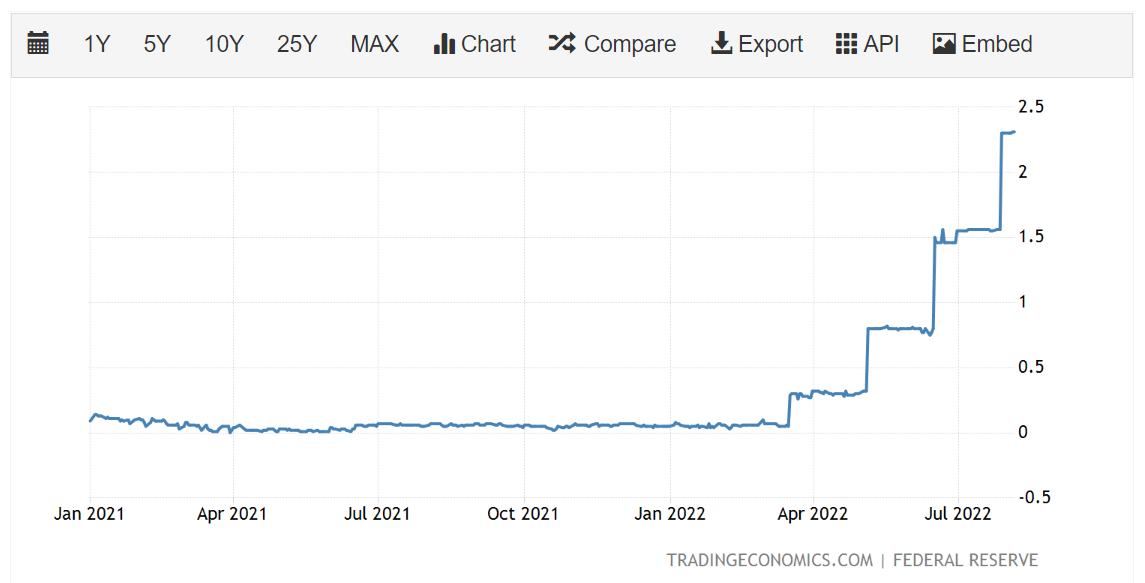

From Figure 4 above, we can see that PDI achieves its leverage primarily through reverse repurchase agreements ("Repo"). Figure 11 below shows the overnight reverse repo rate, which has been increasing rapidly, as the Federal Reserve raises interest rates. While PDI no doubt uses different tenors of repos and manages its borrowing rate closely, this figure does show the general trend that PDI's funding costs are rising rapidly.

{kind=link}

Manager's Security Selection

We touched on this topic briefly, but it's important to emphasize that PDI has an unrestricted strategy, giving the manager carte-blanche to invest in anything and anywhere. There is a significant risk that returns could deviate significantly from expectations. For example, 2020 was generally a good year for bonds, with the AGG ETF returning 7.4% as the Federal Reserve kept interest rates low and implemented quantitative easing to keep credit spreads in check. Yet PDI only returned 2.4%, significantly underperforming bonds.

The problem isn't necessarily the absolute return, but the deviation from the asset class return. For example, most investors hold bonds or fixed income in their portfolio as a hedge or a ballast. However, for PDI to underperform so significantly in a volatile year like 2020 when fixed income was expected to outperform, could be quite an issue from a portfolio diversification perspective.

Conclusion

In conclusion, while PDI's 13% NAV-based distribution yield is attractive, I have reservations regarding the fund's volatile historical performance (swinging from 1st quartile to 3rd quartile on a year-to-year basis). My fear is that PDI is really just a high-return/high-risk fund, as shown by its significantly higher volatility on a 3/5/10-year basis versus the category and bond index. In fact, it's return/risk performance resembles that of an equity ETF like SPY. Investors seeking high current yield may consider investing in PDI, but for me personally, I am staying away.

For further details see:

PDI: High Risk, High Yield