PDI - PDI: How Good Is This Juicy 14% Yield?

2023-06-28 08:46:36 ET

Summary

- The PIMCO Dynamic Income Fund offers a high dividend yield of 14% but has underperformed in 2023, remaining flat for the year and trading down by double-digits compared to its February high.

- The fund's underperformance cannot be fully explained by the rise in interest rates, as long-term rates have not risen across the board. One possible reason is that PDI was overvalued in the past and this overvaluation has now been corrected.

- PDI's net asset value per share has mostly been moving sideways since April, indicating that the fund has managed to stabilize its portfolio. However, future NAV movements will likely be influenced by interest rate changes, with potential pressure if longer-term interest rates move higher.

Article Thesis

PIMCO Dynamic Income Fund ( PDI ) offers a very high dividend yield of 14% at current prices. But investors should not rush into the CEF solely due to it trading with a high yield -- that seldomly is a good idea. While the price has become more attractive so far this year, there are still some other factors that should be considered and that could mean that other investments are more attractive.

PDI Has Underperformed

2023 has been a strong year for the market so far. On the back of hopes about a Fed pivot and increased artificial intelligence enthusiasm, markets have soared over the first six months of the current year:

While the Dow Jones ( DIA ) is up by a comparatively meager 2%, the S&P 500 index has risen by a compelling 14% year to date. That is, for reference, comparable to what the index has historically delivered in around one and a half years, on average. The Nasdaq ( QQQ ) index has exploded upwards, soaring by 37%, driven by hefty gains in companies such as Nvidia ( NVDA ) and Microsoft ( MSFT ).

But not all investments have performed well so far this year, which includes the PIMCO Dynamic Income Fund:

PDI is flat so far this year, and currently trades down by double-digits compared to the 2023 high that was hit in February. Of course, PDI is not an equity fund, thus it is not too surprising that it did not partake in the compelling performance seen in the broad equity markets so far this year. Nevertheless, PDI's rather weak return is noteworthy.

PIMCO Dynamic Income Fund invests in assets such as non-agency mortgage backed securities, corporate bonds (both investment grade and high-yielding), sovereign bonds, and so on. These assets generally decline in value during times when interest rates rise, while they rise in value during times when interest rates decline, all else equal.

The Fed has continued to increase interest rates so far this year, but long-term rates do not always move in line with short-term rates (which are set by the Fed). We see this in the following chart:

The Federal Funds rate has increased meaningfully this year, but long-term rates did not move in line with that. The market seems to believe that the Fed will have to lower rates in the not-too-distant future, otherwise the yield curve wouldn't be this inverted. In fact, 10-year rates have moved down marginally so far this year, which indicates that the move in interest rates does not fully explain why PDI's shares have underperformed so much. If long-term rates had risen meaningfully this year, then the value of the bonds, MBS, and so on that PDI holds would have declined, which would explain the weak price performance PDI has experienced in recent months. But since long-term rates have not risen across the board, it is not true that the value of all fixed-income investments has declined -- the downward move that PDI has experienced in recent months thus has other reasons.

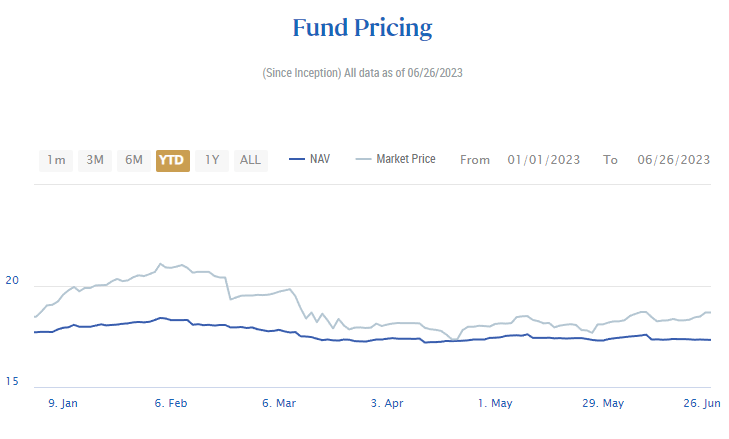

One explanation is that PDI was overvalued in the past and that this overvaluation has now been corrected. In the following chart, we see how PDI's net asset value has performed so far this year, and we also see the CEF's price performance:

{kind=link}

We see that the gap between PDI's net asset value (on a per-share basis) and PDI's price has been particularly wide in February. Back then, investors seemingly were willing to pay a sizeable premium to NAV. Since then, this gap has declined, although PDI still trades at a small premium to its net asset value even today. But with that gap being lower now, compared to a couple of months ago, multiple normalization, or a declining premium compared to the market value of PDI's assets, explains why the CEF has not been a great performer in the recent past.

In the above chart, we also see that PDI's net asset value per share has mostly been moving sideways, starting in April. Prior to that, there was a bit of a downward move in PDI's net asset value. The fact that the fund and its management team have found a way to stop the NAV decline and to stabilize the portfolio is good news, of course. That being said, investors ideally want to see NAV increases . It is not possible to know where NAV will move in the coming months and years, but it is pretty reasonable to assume that interest rate movements will play a major role. When longer-term rates head lower, that should be positive for PDI's NAV, while NAV could come under pressure in case longer-term interest rates move higher. That could happen if inflation does not fall fast enough and if the Fed is forced to hike rates further -- eventually, that should flow through to long-term rates.

PDI Offers A Hefty Dividend Yield

PIMCO Dynamics Income Fund is, as the name suggests, an income investment. This CEF has always been offering a lot of income, and the income yield has risen to a very hefty level following the share price slump we have seen in recent months.

At today's price of $18.70, PDI offers a dividend yield of 14.2%, relative to its market price. When we look at its net asset value, the yield is even higher, at 15.3%. Of course, with a yield this high, investors should ask themselves how likely it is that payments will be maintained at the current level. While it is possible for investments to offer high and also sustainable yields at times, investors should oftentimes be suspicious when it comes to the dividend safety of investments with 10%+ yields.

PIMCO Dynamics Income Fund has not lowered its dividend in the past, and the monthly payout has remained stable since late 2015. That's pretty good, I believe. However, it is also worth noting how the CEF's net asset value has performed over that time frame. In September of 2015, when the dividend was set to the current level, PDI had a net asset value (per share) of a little more than $30. A little less than eight years later, PDI's net asset value per share has almost been cut in half, as NAV per share stands at just $17.30 today. Clearly, PDI has not made dividend payments purely from the profit it generates, but dividend payments have, at least partially, been made out of the CEF's "substance". Maintaining the dividend at the current high level was possible since PDI paid out more to its owners than it generated in profit. It seems questionable, to me, whether this strategy will work forever. If PDI continues to experience NAV declines comparable to what we have seen over the last seven to eight years, the funds' entire net asset value would be gone in around ten years. Management will hardly want to risk that, so there are several possibilities.

First, the fund might be able to improve its returns going forward. If PDI is able to deploy its capital more profitably, the fund could theoretically generate a higher return on its net asset value, and a higher distribution would be sustainable, relative to what would be sustainable today. Higher interest rates could be positive in that regard, as they could allow for higher returns on PDI's NAV.

Second, PDI could lower its payout at some point, to bring it more in line with the returns it generates on its NAV. If PDI generates a return on NAV of 10%, for example, a dividend yield of around 10% (relative to NAV) would be sustainable.

The first option would be preferable, of course, and if management can pull this off, future returns could be very appealing. But it is, I believe, a somewhat risky bet -- if past returns have been meaningfully below what would have been needed to keep NAV stable while making dividend payments as large as PDI did, then I don't see why this will change drastically going forward. I thus believe that a dividend cut is not unlikely, although it will not necessarily happen in the near term.

Final Thoughts

The premium to net asset value has declined, but PDI continues to trade at a premium nevertheless. The dividend yield is very high, but that alone is not a reason to buy. In the past, total shareholder returns have been meaningfully lower than PDI's dividend yield, as NAV and price have headed lower for years.

I believe that the same could hold true in the future, too -- while PDI offers a high yield for now, NAV could erode further. I thus don't want to buy at current prices, despite the very high yield.

For further details see:

PDI: How Good Is This Juicy 14% Yield?