PDI - PDI: How To Profit From A Coming Recession

2023-04-17 06:26:25 ET

Summary

- The PDI fund holds a portfolio of junk bonds and levered credit investments that are susceptible to a deteriorating economy.

- Although its ~15% distribution yield is attractive, I fear the distribution may be at risk in a recession.

- The best way to profit from a recession is to sit on our hands until high-yield credit spreads reach 8-10%.

- Since credit is mean reverting, a well-diversified portfolio of credit investments made in recessionary environments may lead to above-average forward returns.

A few months ago, I warned that a recession was imminent for the U.S. economy, and holding a levered credit fund like the PIMCO Dynamic Income Fund ( PDI ) was not the ideal investment strategy.

While we patiently wait for the inevitable, the PDI fund has continued to struggle with a 12% drop in price and delivering total returns of -4.0% (Figure 1).

Figure 1 - PDI performance since last article (Seeking Alpha)

With the first quarter of 2023 in the history books, has my views on an impending recession changed? Should investors go and buy the PDI fund now, with it yielding almost 15%?

PDI Muddled Through Q1

In my prior article, I laid out two possible scenarios for the PDI fund. First, in a 'muddle-through' scenario, I expected the PDI's portfolio to earn income, while suffering from duration induced MTM losses.

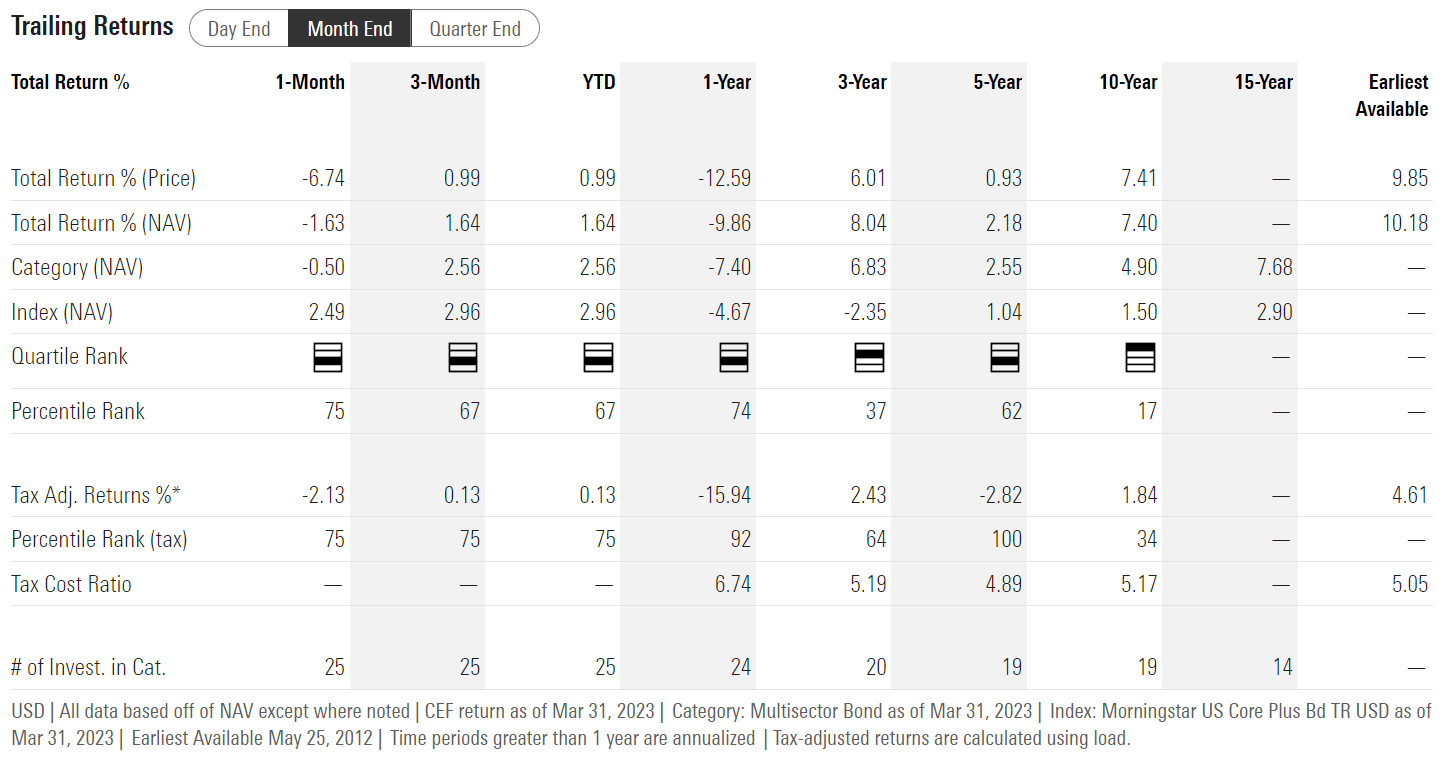

This is basically what happened to the PDI fund in the first quarter, as the Federal Reserve continued to raise interest rates to fight inflation. Although the PDI fund paid unitholders $0.6615 in distributions to March 31st (3.6% yield on 2022 year-end price of $18.48), actual total returns in Q1 were only 1.6% (Figure 2).

Figure 2 - PDI historical performance (morningstar.com)

{kind=link}

Economic Clouds Darkening

However, as we transition into Q2, economic clouds are darkening and I fear my second scenario, a 'hard-landing' recession, will play out in the coming quarters. In recent months, we have seen continued deterioration in many economic indicators.

Declines In Retail Sales Point To Struggling Consumer

For example, U.S. retail sales that were released on April 14th showed retail sales fell 1.0% in March, following a 0.2% decline in February (Figure 3).

Figure 3 - Decline in March retail sales (Census.gov)

Historically, for a consumer nation like the U.S., back-to-back declines in retail sales are rare and typically associated recessions (2000/2001,2008/2009, 2020). Therefore, March's back-to-back decline is concerning. In fact, the U.S. economy has seen a monthly decline in retail sales in 4 of the past 5 months and 6 of the past 9 (Figure 4).

Figure 4 - Back-to-back decline in retail sales are rare (Census.gov)

{kind=link}

Declining retail sales are especially concerning given the fact that retail sales are measured in nominal dollars that are not adjusted for inflation. With inflation running hot, retail sales should not be declining MoM if volume of goods sold were stable (Figure 5).

Figure 5 - CPI inflation has been running hot (BLS)

{kind=link}

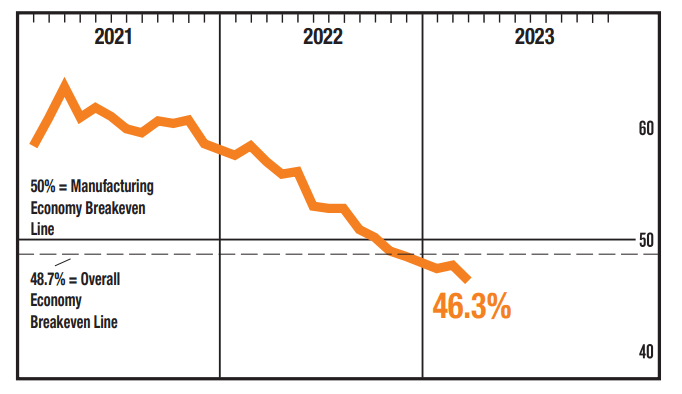

Manufacturing In Contraction Since Late 2022

Economic activity in manufacturing has not fared much better, with the latest ISM Manufacturing PMI survey coming in at 46.3, having been in contraction territory since late 2022 (Figure 6).

Figure 6 - ISM Manufacturing PMI has been contracting since late 2022 (ismworld.org)

{kind=link}

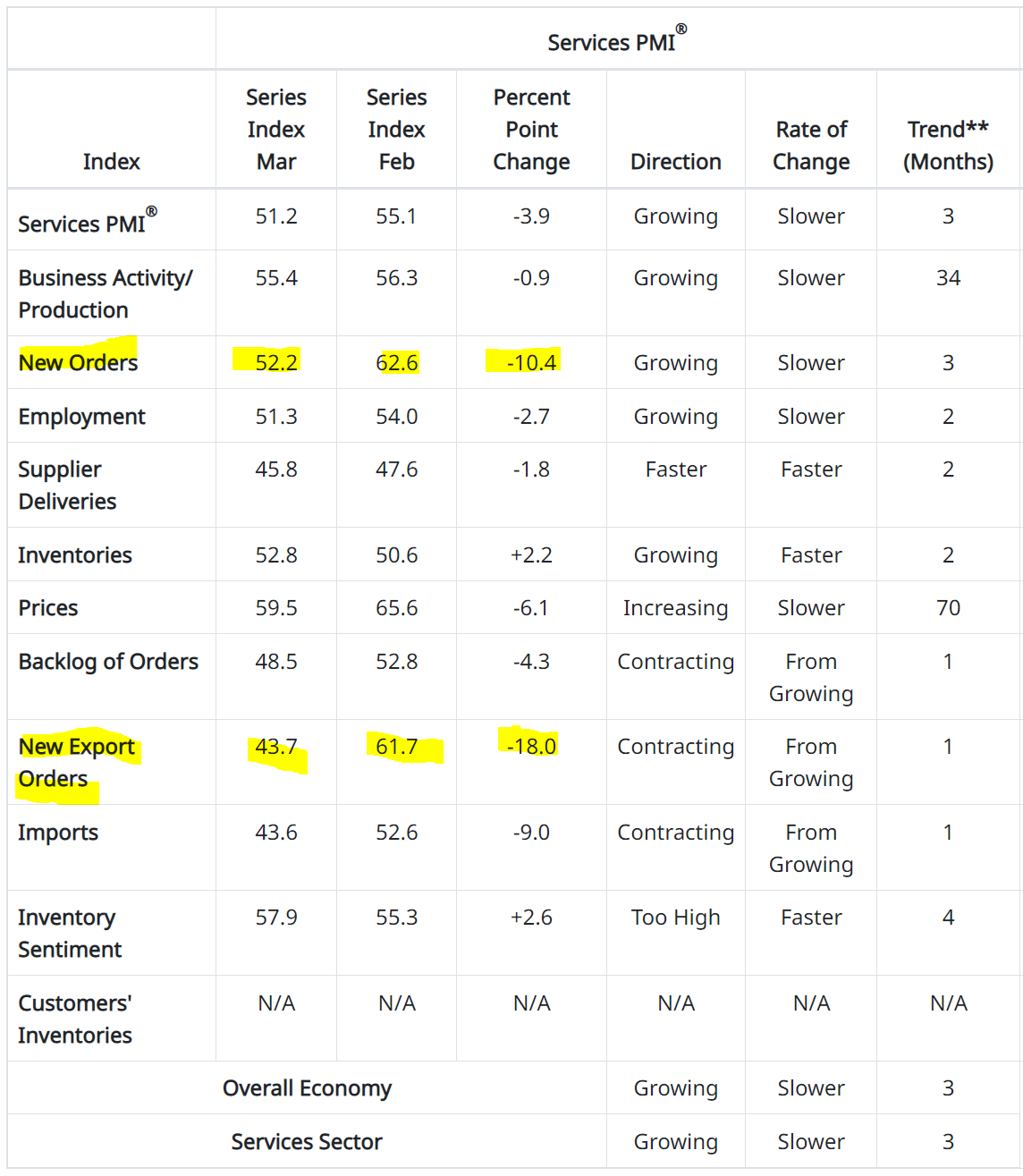

Services See Orders Plunge

Although the ISM Services PMI continued to see expansion in March, registering 51.2, the survey declined markedly from 55.1 in February. Importantly, the New Orders sub-component plunged in March, suggesting a sharp slowdown in future services activity (Figure 7).

Figure 7 - ISM Services PMI New Orders plunged (ismworld.org)

{kind=link}

Regional Banking Crisis Tightens Credit Conditions

Finally, in recent weeks, the impact of the Fed's rapid interest rate increases is finally flowing through to the real economy, as several regional banks failed in spectacular fashion from a combination of deposit flight (bank deposits paying 0.37% are unattractive compared to money market funds paying over 4%) and investment securities losses (many regional banks held portfolios of bonds that lost value due to higher interest rates).

As regional banks fight to retain deposits, their funding costs are expected to rise which will further tighten lending standards for consumers and businesses. According to the Fed, this could be equivalent to one or more interest rate hikes. Commercial real estate is a sector that's particularly hard hit, as regional banks were large lenders in the space.

Recession Seems All But Certain

Putting it all together, it is no wonder that a many economists believe a U.S. recession is all but certain in the coming quarters (Figure 8).

Figure 8 - U.S. recession probability at 99% (Conference Board)

In fact, even the Fed's own staff economists are projecting "a mild recession starting later this year, with a recovery over the subsequent two years," as we recently learned from the Fed's FOMC Minutes.

Levered Credit Funds Suffer During Recessions

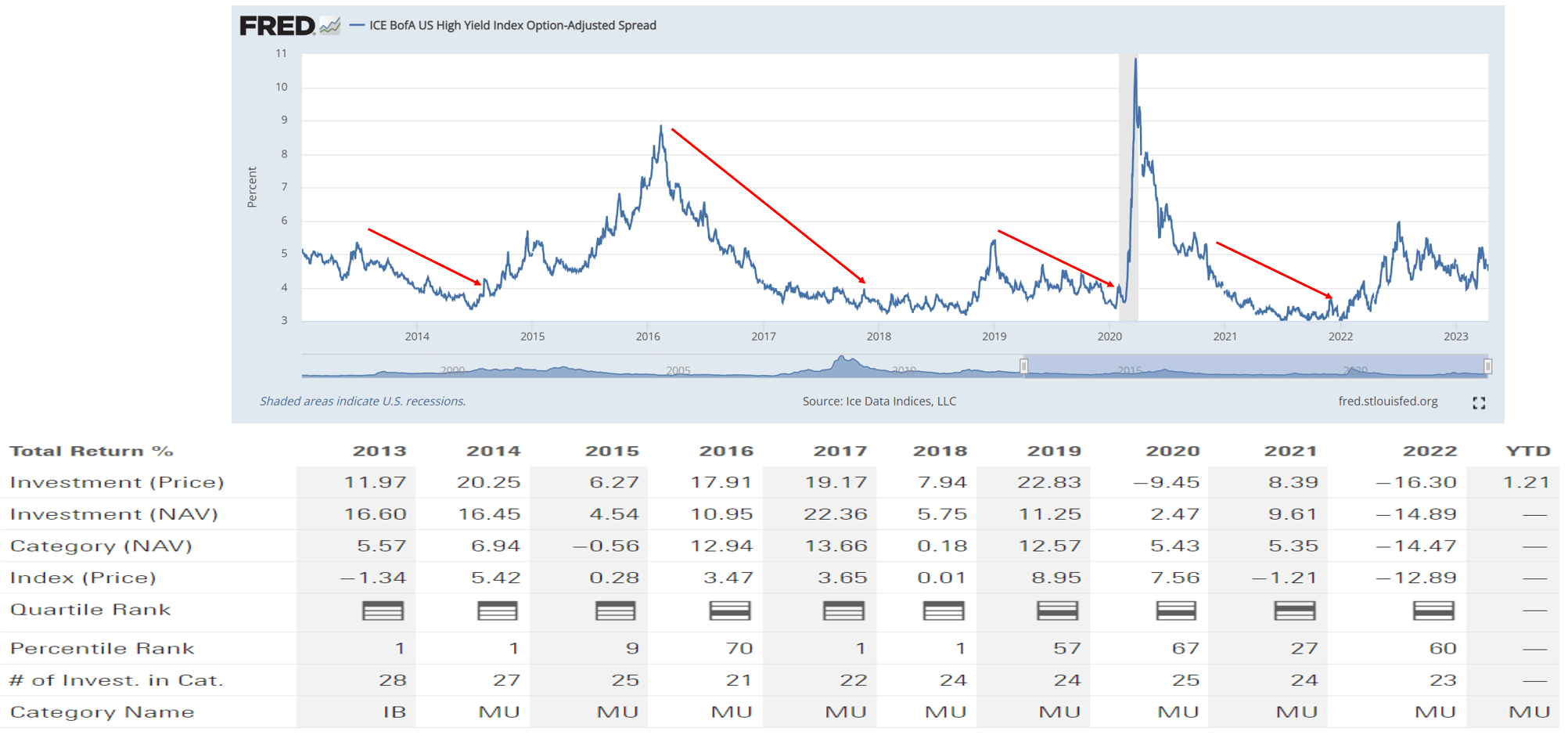

As I wrote in my prior article, "if the economy does enter a recession, then I expect credit spreads and bond defaults to spike, as companies will struggle to service their debts. A recession has never occurred without a rise in high yield credit spreads (as measured by the ICE BofA High Yield OAS) to 8-10%" (Figure 9).

Figure 9 - Recessions are accompanied by spikes in high yield credit spreads (St. Louis Fed)

Given high yield credit spreads are currently trading at only ~4.50%, there is a lot of price downside to the credit investments held within PDI's portfolio.

A 1% increase in credit spreads has as much impact to a bond as a 1% increase in interest rates. Given the PDI fund's 3.9 Yr duration, a first order approximation is that a 1% widening in credit spreads will cause ~4% decline in prices. Therefore, if high yield credit spreads do widen to 8-10% in a recession scenario, PDI's 2023 returns could be as bad as 2022's, when the fund lost 14.9% overall.

Will PDI's Distribution Be At Risk?

Many investors depend on high yielding closed-end funds like the PDI to fund their retirements or supplement their income. A key question for these investors is whether a recession will have any impact to PDI's distribution?

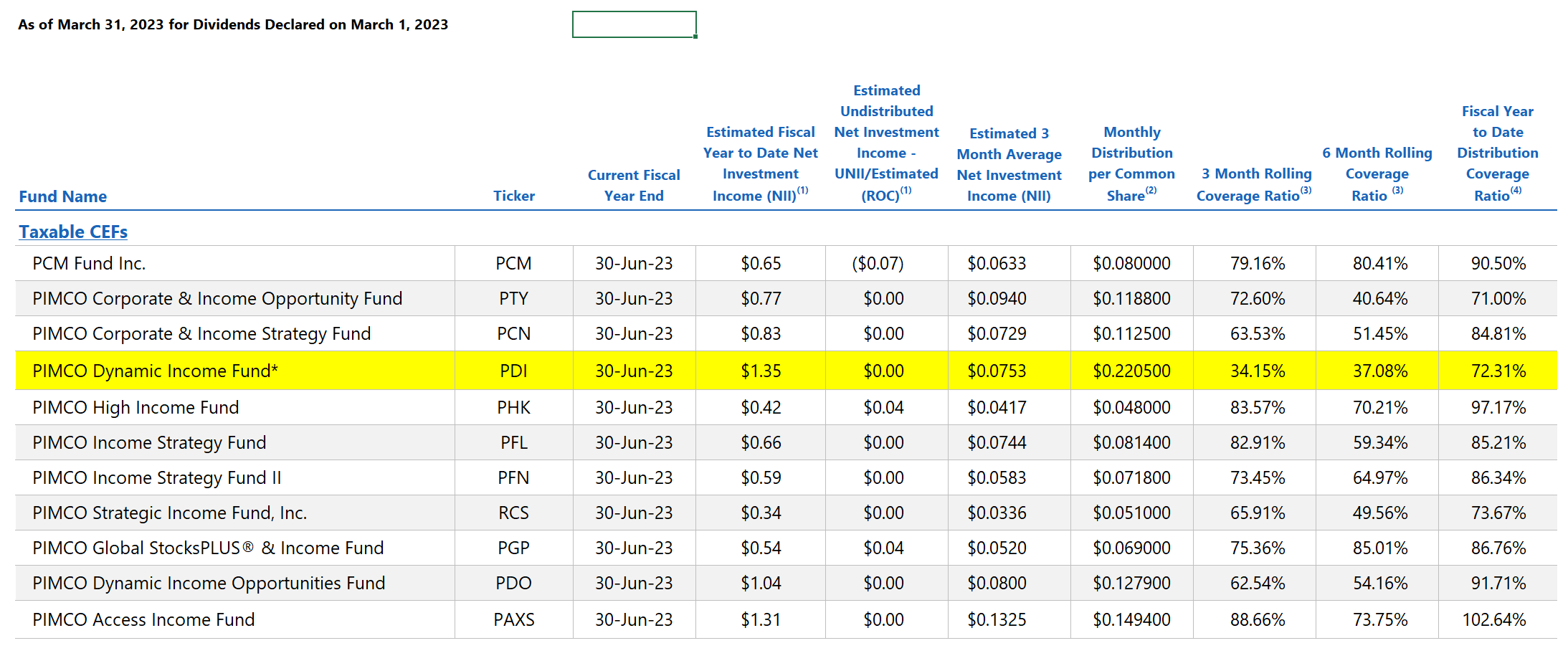

First, based on the fund's latest UNII report , the PDI fund is not currently earning its distribution with 3 month distribution coverage ratio of only 34% (Figure 10).

Figure 10 - PDI UNII report (PIMCO)

{kind=link}

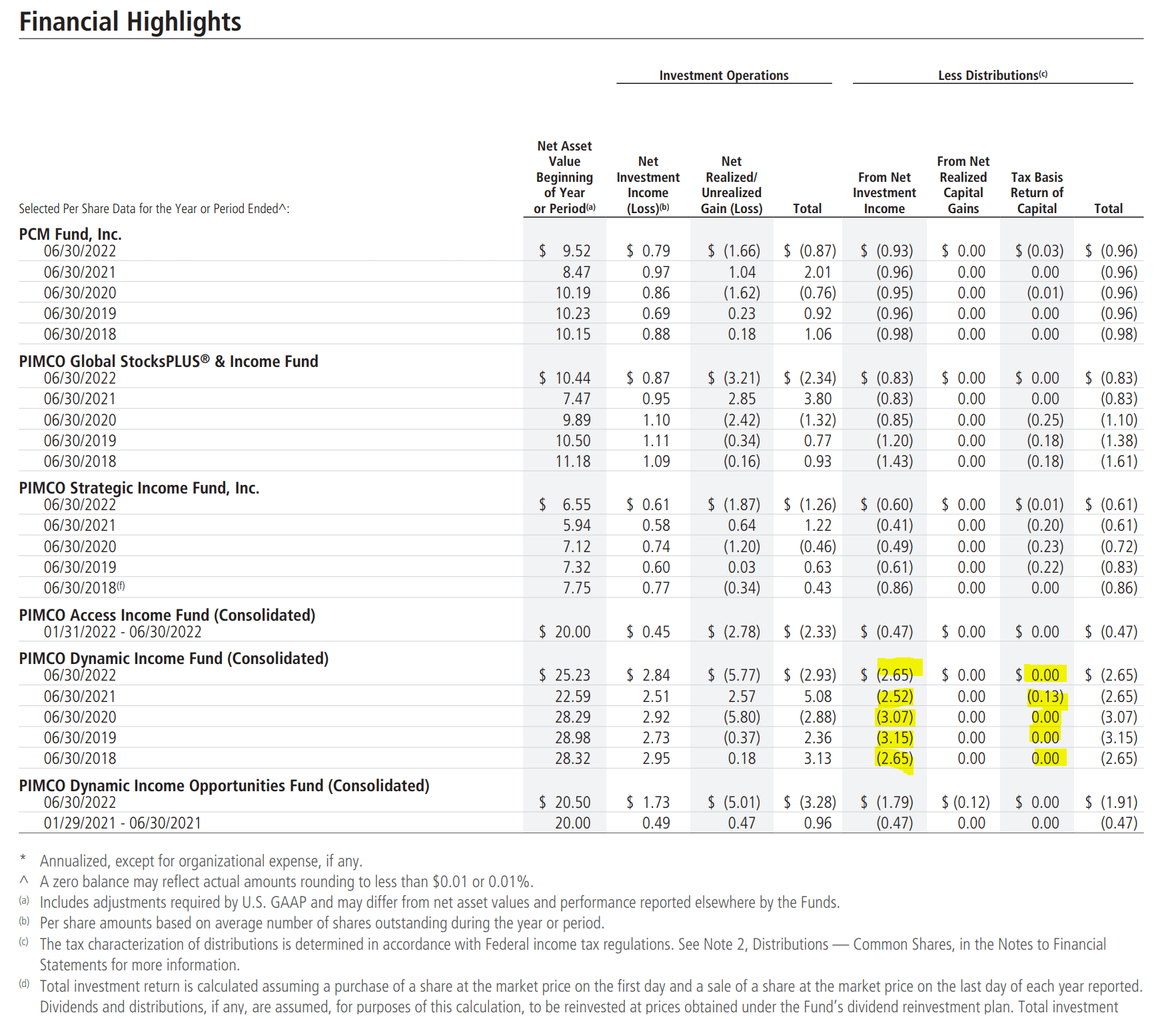

However, this coverage figure can fluctuate and as many commentators like to argue that historically, the PDI fund has been able to fund its distributions mostly out of net investment income ("NII") (Figure 11).

Figure 11 - Historically, PDI has funded distribution out of NII (PDI 2022 annual report)

{kind=link}

However, another way to think about the sustainability of a fund's distribution is to compare the distribution rate to the fund's long-term average annual returns. In PDI's case, the PDI fund has only earned 3/5/10Yr average annual returns of 8.0%/2.2%/7.4% respectively to March 31, 2023, compared to the fund's 15.3% of NAV distribution rate (see figure 2 above).

Even if we compare PDI's distribution rate to the generous 3Yr average annual return of 8.0% (which is flattered by the starting period of March 2020, the depths of the COVID lows), the PDI fund is paying far more than it earns.

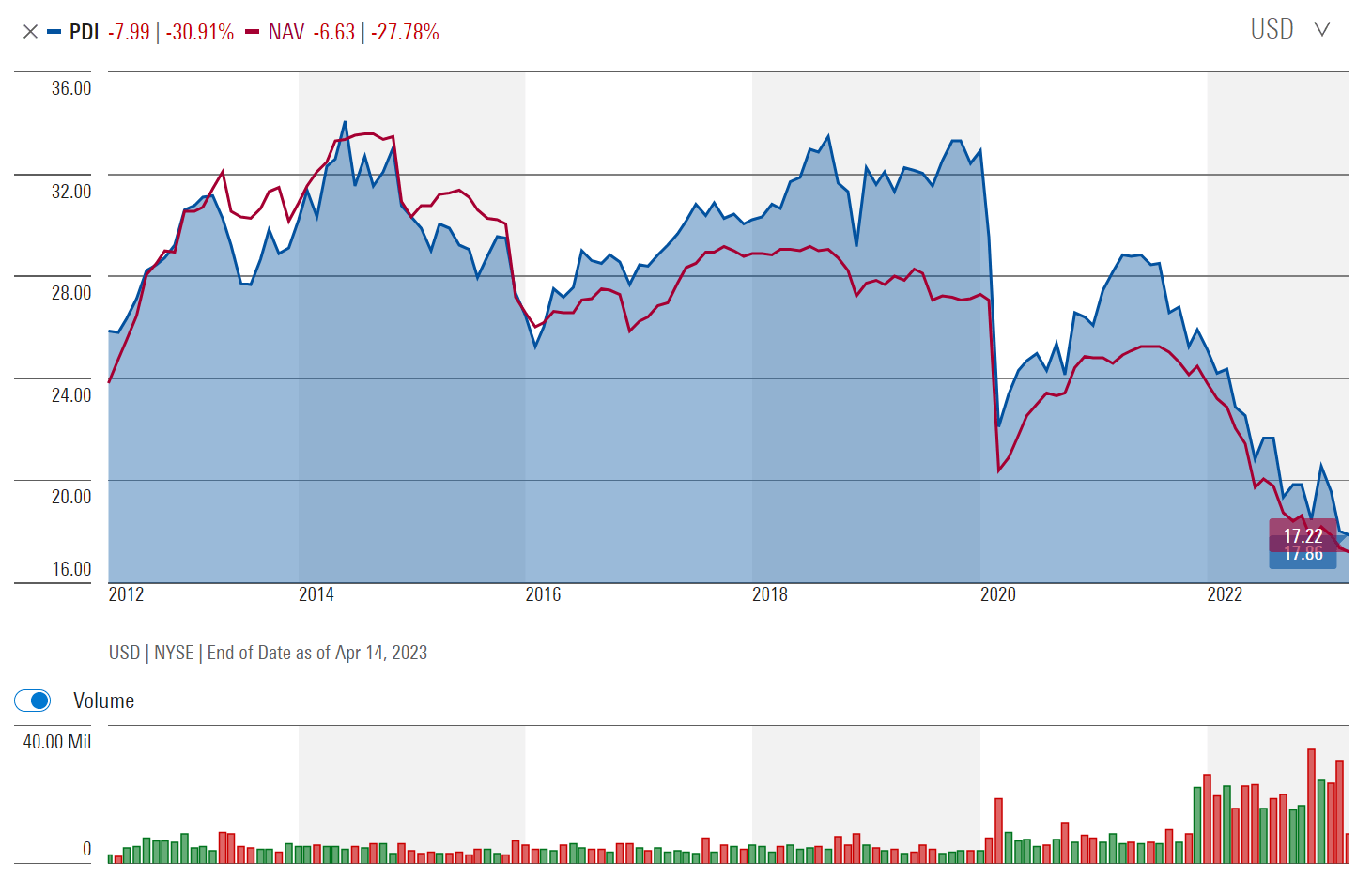

Funds that do not earn their distributions are called 'return of principal' funds by Eaton Vance and are characterized by an amortizing NAV. Looking at PDI, we can see the that the fund's NAV has indeed shrunk, from over $32 in 2014 to $17 recently (Figure 12).

Figure 12 - PDI's NAV has shrunk over time (morningstar.com)

{kind=link}

While PDI's distributions may indeed be 'fully funded', investors could be losing through 'realized and unrealized investment losses'. For example, from figure 11 above, we can see that the fund accumulated $9.19 / share in realized and unrealized losses in the past 5 fiscal years.

Some readers may argue, aren't these just unrealized losses that will normalize once interest rates decline? Unfortunately, I don't believe that will be the case.

Similar to my argument against the Blackstone Strategic Credit Fund ( BGB ), I believe the reason PDI suffers from investment losses is because the fund may have been 'reaching for yield' and invested in risky loans and bonds that have led to permanent losses of principal. So although the fund generates sufficient NII to fund its distribution, it also suffers from principal losses from heightened credit events throughout its portfolio.

Credit events do not have to be full on bankruptcies. They could be as simple as credit downgrades that cause credit spreads to widen and prices to decline. Through portfolio turnover, the PDI fund would turn these unrealized MTM losses into permanent losses of principal.

For example, during the COVID pandemic, PDI's NAV plunged from over $27 / share to $22 / share. Since credit is a mean reverting asset class, if the PDI fund had held onto its investments, the subsequent recovery in 2020 and 2021 should have recovered most of the NAV declines as the Fed lowered interest rates to zero and backstopped all credit markets. However, we can see that PDI's NAV only recovered to $25, which suggest permanent losses were taken.

PIMCO Precedents For Distribution Cuts

My biggest worry is that distribution cuts usually happen at the worst possible time for investors. For example, during the 2008/2009 Great Financial Crisis, many closed-end funds had to cut their distributions just as the recession took their portfolio values to the woodshed. Countless unitholders were left literally holding the bag, never to recover their losses in principal and income.

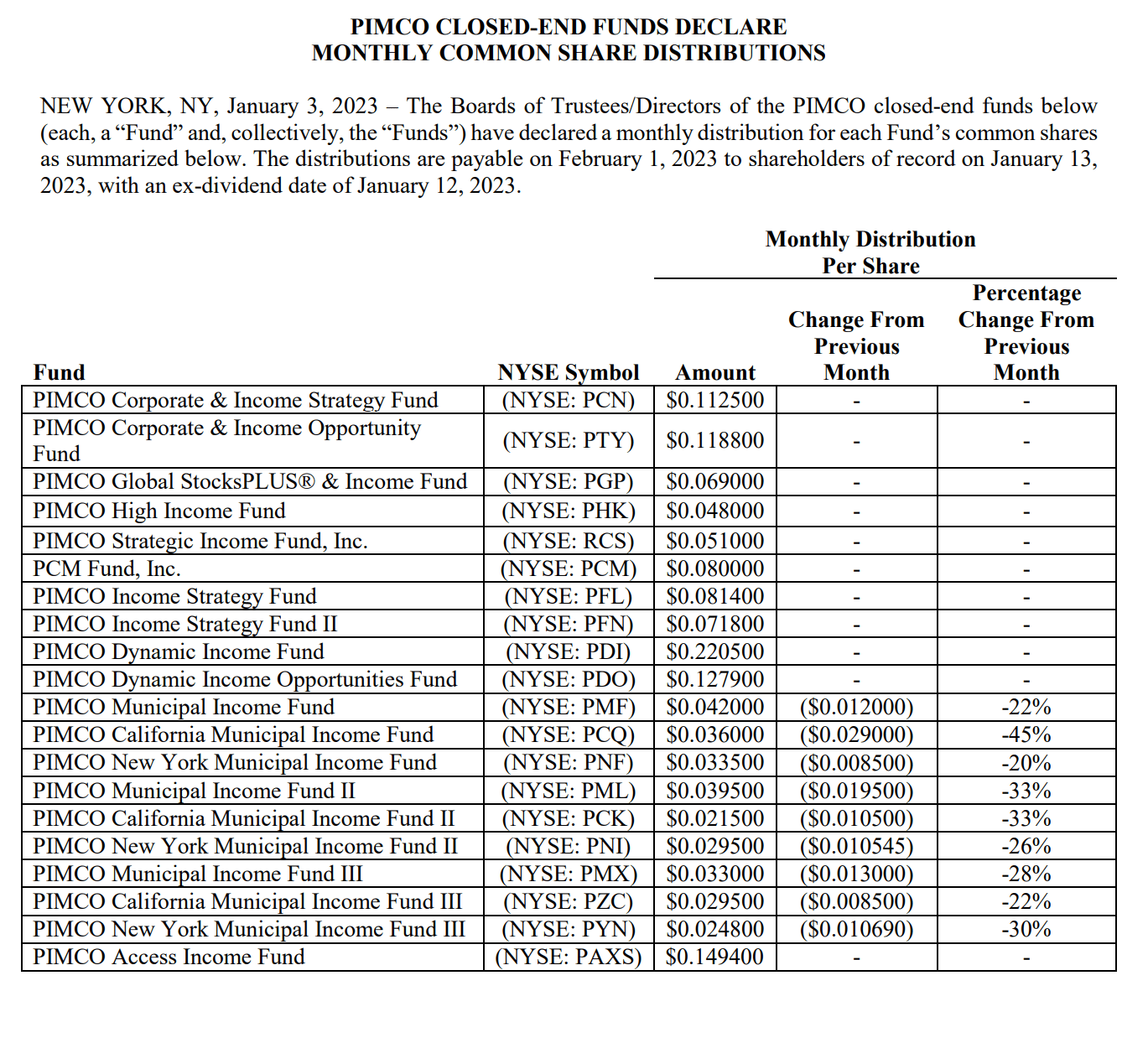

Recently in January, PIMCO chopped the distributions on many of its municipal CEFs (Figure 13). Fortunately, the broad income funds like PDI were spared, but for how long?

Figure 13 - PIMCO cut its municipal CEF distributions (PIMCO)

{kind=link}

A Recession Could Be An Opportunity

On the bright side, a U.S. recession could be a blessing in disguise for investors looking to buy bargains.

As we mentioned above in figure 9, recessions tend to be accompanied by spikes in credit spreads. For credit funds like PDI, this will lead to massive declines in the MTM values of its portfolio.

The mean reverting nature of credit spreads mean that eventually, credit spreads will normalize and investors who have the courage to buy when markets look bleak will earn above average forward returns. Empirically, the PDI fund and other similar credit funds typically earn strong forward returns after credit spreads spike. The challenge for investors is to have the patience to wait for such an event to occur (Figure 14).

Figure 14 - Credit spikes lead to strong forward returns (Author created with data from Morningstar and St. Louis Fed)

{kind=link}

Conclusion

In summary, since my last article, the U.S. economic fundamentals have deteriorated further, with even Fed officials now projecting a recession to begin shortly. My main worry is that heading into a recession, credit spreads will spike, which will turn into MTM losses for credit funds like the PDI. Furthermore, with a ~15% distribution yield, I fear PIMCO may have to cut its distribution if asset values were to fall significantly during the coming recession.

However, not all is gloom and doom. Recessions are also terrific opportunities for patient investors to snap up bargain credit funds like the PDI. This is because credit is a mean-reverting asset class, and eventually, credit spreads will normalize. Investors who can sit on their hands in the meantime may be able to enjoy above average forward returns when buying from panicked sellers.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

PDI: How To Profit From A Coming Recession