PDI - PDI: I Have Been Buying This 15% Yielding CEF Despite Its Decline

2023-10-03 08:45:00 ET

Summary

- PIMCO Dynamic Income Fund shares have declined by -9.43%, and the total return is -7.26%, compared to -6.47% from the S&P 500.

- Rising interest rates have negatively impacted PDI's underlying assets, including bonds and mortgage-backed securities.

- I believe that PDI is bottoming out, and I am dollar cost averaging into my position, expecting a rebound as interest rates decline.

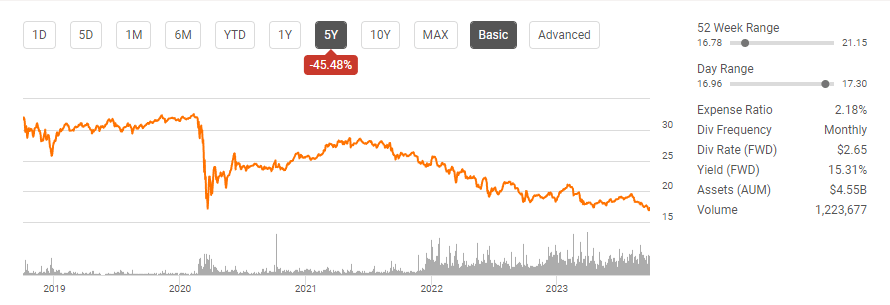

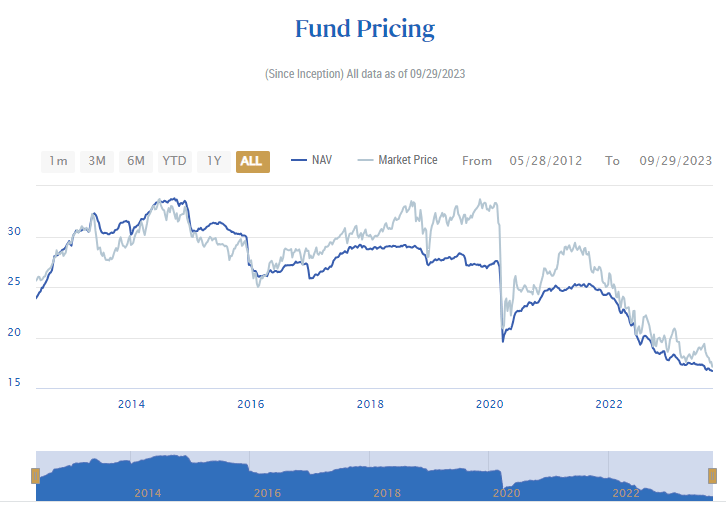

Since my last article on the PIMCO Dynamic Income Fund ( PDI ) ( can be read here ), shares have declined by -9.43%, and after its distributions have been accounted for, the total return is -7.26% compared to a decline of -6.47% from the S&P 500. During this period, I increased the number of shares purchased by 61.85% as I continued to dollar cost average into the position. Since starting the position, I have added to PDI 13 times in my main dividend account and have collected 5.03% of my total shares from reinvesting the distributions. Over the previous 5-years, excluding the distributions, the share value of PDI has declined by -45.48%, and while shares forged a path back to $30 after the pandemic crash, the rising rate environment has been a major deterrent to reclaiming its previous value. I am willing to increase my exposure to PDI as I believe we are coming to the end of the Fed's tightening cycle, and this should act as a catalyst for PDI's underlying assets. If the Fed hikes rates again and keeps them higher for longer, then shares of PDI could face additional pressure. This is a risk I am willing to absorb as I am now being paid 15.3% to endure the declining prices while reducing my cost basis. My current cost basis is $19.05 for the shares I have paid for out of pocket, and when the distributions are factored in, my cost basis declines to $18.07.

{kind=link}

What's been going wrong with PDI

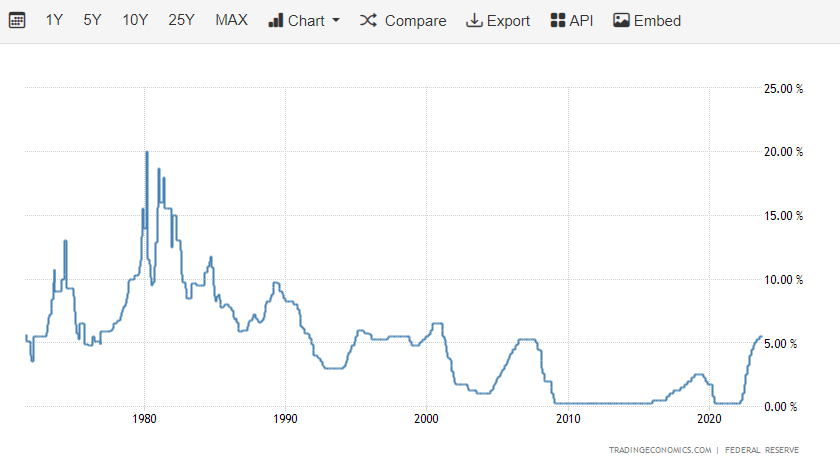

PDI's assets consist of debt obligations and other income-producing securities, including mortgage-backed securities, investment grade, and high-yield corporates, developed and emerging markets corporate and sovereign bonds, other income-producing securities, and related derivative instruments. PDI's net assets consist of $4.65 billion spread across 1,866 holdings. The current economic environment is problematic for PDI's underlying assets as we're living in a rising rate environment. Interest rates have exceeded 5% for the first time since 2008, and while pre-2010 5% interest rates were not uncommon, the rate at which the Fed has taken rates above 5% hasn't been seen since the early 1980s.

{kind=link}

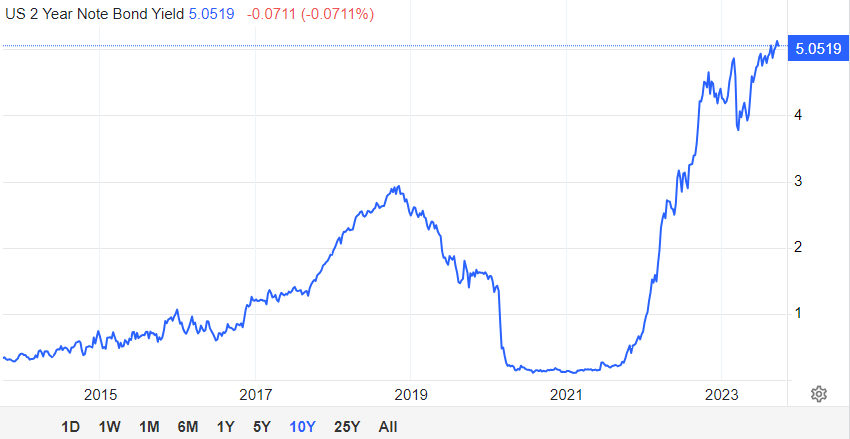

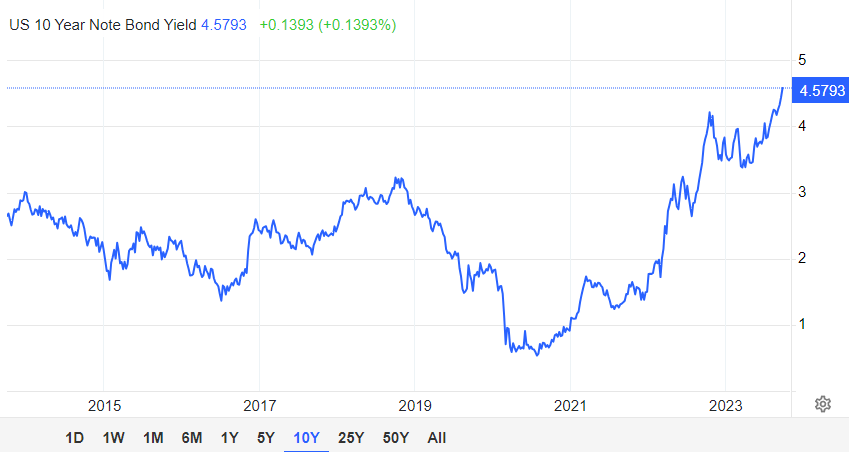

The rising rate environment has pushed the yield on risk-free assets such as the 2-year treasury note past 5%, and the 10-year treasury note has a yield of 4.58%. This has created a safe haven for capital to generate an attractive, risk-free rate of return. Investors looking for yield now have alternative options than capital markets, and in some cases, they would rather generate 4-5% risk-free than take on risk for a higher yield.

{kind=link}

{kind=link}

While rising rates provide an alternative option to generate yield, it's often destructive to funds such as PDI. Elevated interest rates can be problematic for bonds, mortgage-backed securities, and funds that hold these assets. If you were to purchase a bond with a 5-year maturity rate and a 5% coupon for a par value of $1,000, you would receive $50 in annualized interest and the principal upon maturity. When interest rates increase, the value of the 5% coupon bond will fluctuate to the downside. If rates went to 7% and new bonds generated a 7% coupon, the bonds with a 5% coupon would trade at a discount to their face value. The inverse would create a scenario where if rates decline instead of rise, bonds with higher coupons would trade at a premium because the amount of income being generated from the yield would be greater than newly issued bonds at a lower coupon. This methodology spills over to the mortgage-backed security sector. Rising rates can lead to a decline in the value of MBSs. An MBS is essentially a bundle of home loans and other real estate debt bought from banks. In a rising rate environment, newly issued home loans will be issued at higher interest rates and could cause existing MBSs to decline in value because they are not generating the same amount of yield.

In a rising rate environment, funds that hold an array of bonds and MBS products could face declines, as we're seeing in PDI. PDI has over 1,800 investments, and when rates rise, shareholders may liquidate their shares to avoid further losses. When this occurs, the fund managers could be in a position where they are forced to sell bonds prematurely to raise enough capital to offset their redemptions. This can cause the net asset value ((NAV)) of the fund to decline and put pressure on its shares. I believe this is part of the reason we are seeing PDI's NAV and share price decline to the lowest points since its inception.

{kind=link}

Why I think PDI is bottoming and I am dollar cost averaging into my position

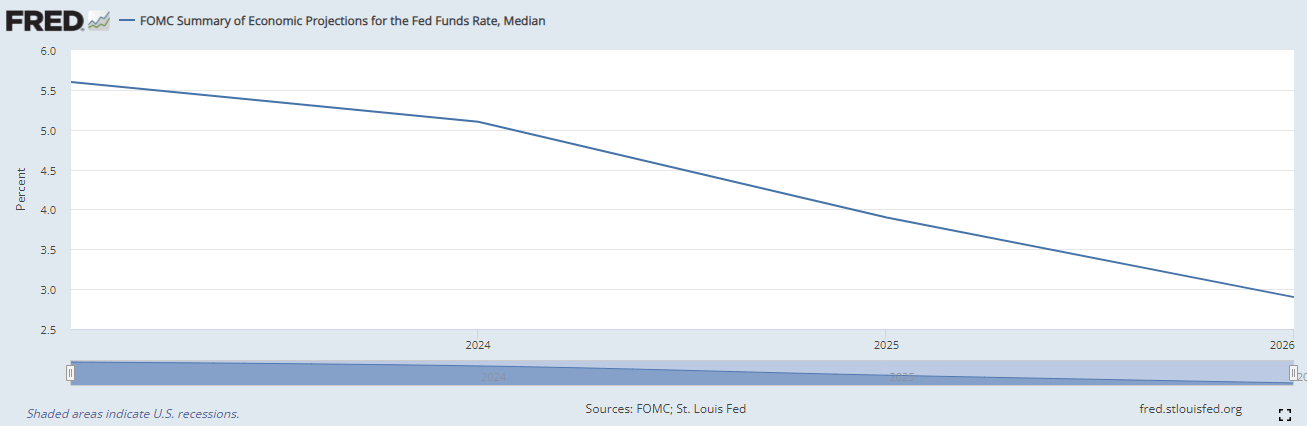

The latest FOMC meeting has come and gone. Jerome Powell left the door open for another raise and was overly hawkish, in my opinion. The CME group has projected that there is an 18.3% chance that the Fed will raise rates to 550-575 in November, and a 31.4% chance that rates will go to 550-575 in December. The St. Louis Fed has adjusted its economic projections on interest rates to reflect the latest sentiment coming from the Fed. The updated outlook consists of higher rates for longer but declining in 2024. The St. Louis Fed is pricing in one more rate hike, then declining from 5.6% to 5.1% in 2024, with rates falling to 3.9% in 2025 and 2.9% in 2026.

{kind=link}

While it's completely possible that we will endure an additional rate hike in 2023 or early 2024, I think there are several factors that will play into the Fed pivoting. First, it's an election year, and no party wants to go into an election cycle with an economy that is perceived to be weak or interest rates that are restrictive and cause economic hardship to the voting population. I think there will be political pressure to cut rates so the cost of capital decreases, and we see increased economic activity. Issuing debt at higher interest rates is a problem for the United States economy because it increases the amount of capital being spent on interest payments. The net interest on the nation's debt has exceeded $700 billion annually and is closely catching up to the defense budget. This is a problem as it requires a larger portion of the nation's outlays and causes additional strain on balancing the budget. The government needs to issue debt at lower rates to reduce the cost of the interest from the national debt. I also believe that the Fed is extremely close to breaking things, and while taking rates over 5% hasn't blown up the banking or credit markets, the cracks are starting to show. If the Fed keeps raising or keeps rates higher for too long, we could see an elevated rate of defaults and bankruptcies that could send a ripple effect through the economy. While the Fed's mandate is to have stable prices and achieve maximum sustainable employment, their actions have both a direct and indirect impact on the macro-environment, and I think they're at the end of their tightening cycle, and the pivot will occur in the spring.

PIMCO is one of the largest investment houses, managing over $1.79 trillion for central banks, sovereign wealth funds, pension funds, corporations, foundations, endowments, and individual investors globally. PDI utilizes a dynamic asset allocation strategy among multiple fixed-income sectors in the global credit markets, including corporate debt, mortgage-related and other asset-backed securities, government and sovereign debt, taxable municipal bonds, and other fixed-, variable- and floating-rate income-producing securities of U.S. and foreign issuers to meet its investment objectives. I believe PDI's holdings will be more valuable in the future as rates decline. While bonds and MBS products have seen value erode during the period of rising rates, these assets should reclaim value as rates are lowered because newly issued bonds and MBS products will have lower yields, making PDI's current holdings more valuable. PDI has also been active, and there is a chance that the fund will have assets issued at the top of the cycle embedded in its holdings, with rates becoming less restrictive, these assets could demand a higher elevation in price because their yields won't be able to be replicated.

{kind=link}

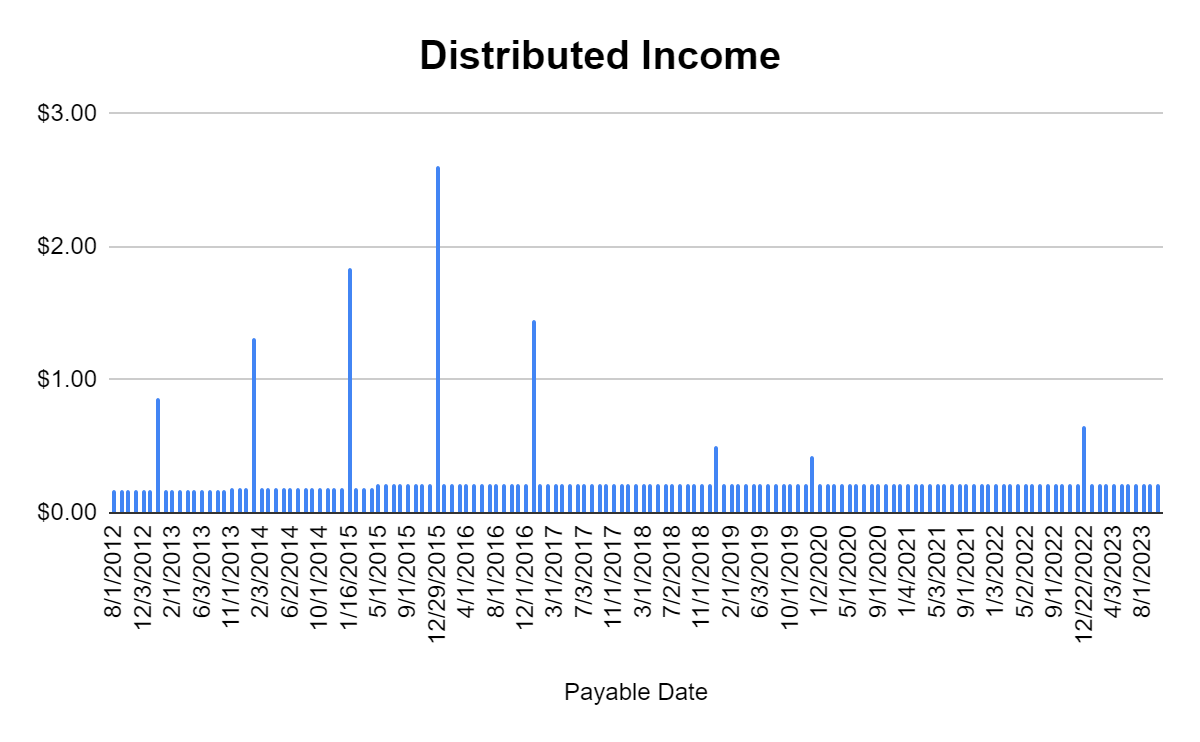

I am being paid to wait, and PDI currently yields 15.3%. Since its inception, PDI has generated $38.17 in income for its shareholders, consisting of $28.53 in normal distributions, $8.28 in special distributions, $0.90 in long-term capital gains, and $0.46 in short-term capital gains. Since going public on 5/30/12 at $25 per share, the share value has seen a decline of -30.88%, but the fund has distributed 152.68% of its initial value in income. Between the current value of its shares and the distributed income prior to the impact of reinvesting the distributions, PDI has generated a 121.8% return in less than 12 years. PDI has never reduced the distribution; no matter what has occurred, they have always distributed monthly income to their shareholders. While the value has declined on PDI's net assets, their ability to generate income hasn't been impacted, and I suspect that PDI will continue generating monthly income even if the fund slides a bit.

PDI is a risk, and don't invest in it because I am willing to take the risk

Every time you allocate capital toward an investment, your return is generated from putting your money at risk. The Fed could keep rising rates, and large global markets could see their rates continue to increase, and the projections about what will occur could be incorrect. If 5% becomes the new normal and we see rates go higher, then PDI could face additional headwinds, and my investment thesis could backfire. I am taking a risk with PDI that I feel is acceptable for me. I am comfortable with PDI trading sideways or even lower over the next year or so while collecting the distributions because I feel it will eventually rebound. This may not occur, and PDI could cut its distribution. Everyone needs to make their own choices, and while I think PDI will work out, there are factors outside of anyone's control that will impact PDI's future. Just because PDI falls within my level of acceptability doesn't mean it's a good investment idea for you, so please do additional research.

Conclusion

I am dollar cost averaging into my position to lower my cost basis and increase my yield on capital. I believe that an environment where rates are declining will be positive for PDI's underlying assets and will add value as the yields of newly issued bonds and MBS products decline. While the macro environment could work against PDI, I think it's setting up to be less restrictive, and PDI will be rewarded in 2024. On the surface, PDI hasn't done well, but the large yield provides a buffer, and I think that adding PDI at the top of the cycle will prove to be a strong income investment in the future.

For further details see:

PDI: I Have Been Buying This 15% Yielding CEF Despite Its Decline