PDI - PDI Looks Like It Bottomed And Is Still Yielding Over 14%

2024-01-09 09:00:00 ET

Summary

- I have been consistently adding to my position in the PIMCO Dynamic Income Fund and plan to continue doing so in 2024.

- PDI has maintained its distribution rate and has continued to generate income, despite macroeconomic headwinds.

- I believe that PDI shares will appreciate in 2024 as the Fed cuts rates, creating a larger market for higher-yielding assets.

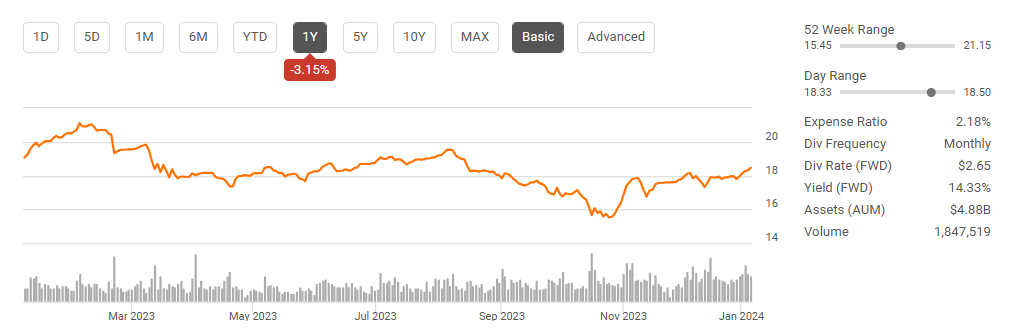

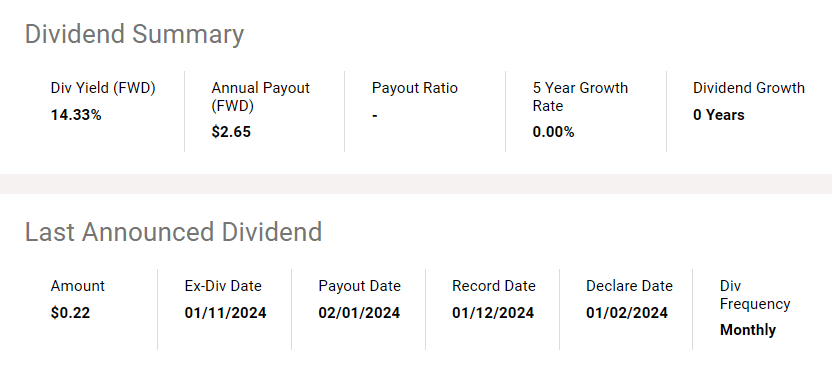

I have been adding to my position in the PIMCO Dynamic Income Fund ( PDI ) throughout 2023, and I have no intention of stopping in 2024. PDI continues to be an income-producing machine in my dividend portfolio, as they just announced a continuation of their distributions at the same monthly rate of $0.2205. PDI ended 2022 at a share price of $18.48. Investors who added PDI at the beginning of 2023 for around $18.50 generated between a 14-15% distribution yield on capital, while shares ended up in basically the same position they started when 2023 closed. As of now, it looks like PDI will maintain its current level of distributions, and investors can look forward to $2.65 of distributed income per share in 2024. I think that shares of PDI will continue to rebound as their underlying assets should appreciate in value when the Fed pivots. If this occurs, investors could see further capital appreciation as the share value should increase as PDI's net asset value ((NAV)) grows. PDI can still be a large income generator with a side of capital appreciation in 2024.

{kind=link}

Following up from my previous article on PDI

On October 3 rd, I wrote an article on PDI ( can be read here ), and since then, shares have increased 9.29% compared to the S&P 500, which has appreciated by 10.01%. When PDI's distributions are factored in, the total return since October 3 rd has been 13.51%. I continue to be bullish on PDI as I feel it can generate both capital appreciation and a strong distribution of income going forward. Now that we have more clarity on the Fed's trajectory, I wanted to follow up with an update to my previous article. I am upgrading my view from bullish to very bullish as I believe the future environment will create a much larger demand for PDI's underlying assets.

{kind=link}

There are risks to investing in PDI so I would like to address those first

I can't predict the future, and my investment case is based on what will occur in the macroeconomic environment. If the Fed decides to deviate from what was presented at the most recent Fed meeting or if a credit crunch occurs, shares of PDI could be negatively impacted. For my investment thesis to play out how I envision it, the rate environment needs to decline. If the Fed changes course and stays higher for longer, then the risk-free rate of return will remain intact, and we would probably see bond rates increase again. This would negatively impact the underlying assets in PDI's portfolio and put fears of debt defaults back on the table for many companies, especially in the real estate sector. PDI also utilizes leverage in its investment methodology, and while the fund managers have been able to mitigate risk to some extent, if a higher for longer rate environment creates a credit crunch, then the losses PDI sustains could be elevated. There is also opportunity cost risk as I am not expecting PDI to outperform the Nasdaq or the S&P 500 over an extended period of 5-10 years. From a capital appreciation standpoint, there is probably a larger return from a capital appreciation aspect in other investments.

PDI has continued to generate large amounts of income despite macroeconomic headwinds or unpredictable market cycles

I am looking at PDI as an income-producing asset where I can reinvest the monthly distributions to increase the amount of future income that is generated. PDI just announced its first distribution in 2024, which is the same monthly rate as 2023. No matter what article I read about PDI, there is always a concern about PDI reducing their distribution rate. PDI has paid a monthly distribution of $0.2205 since the September 2015 distribution, and the monthly rate hasn't changed. When individuals ask me how I can be comfortable with a CEF that has such a large yield, my answer is always the same. Until PIMCO gives me a reason to doubt them, I have no reason to do so. In just over 8 years, we have endured the Pandemic, the Fed taking rates to the highest levels in 4 decades, geopolitical tensions being elevated, new and ongoing conflicts overseas, inflation, and a regional banking crisis. Throughout these macroeconomic and geopolitical events, PDI has maintained its distribution rate, so when I look toward a future setup that is favorable to PDI's underlying assets, I am very bullish on its ability to continue generating ongoing income at these levels.

{kind=link}

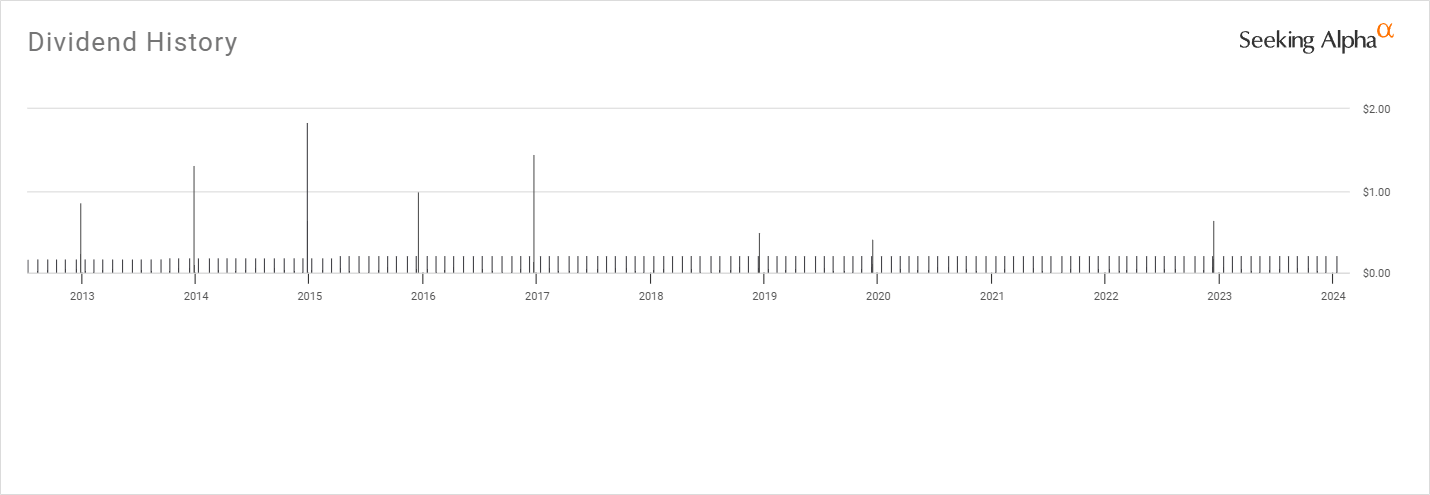

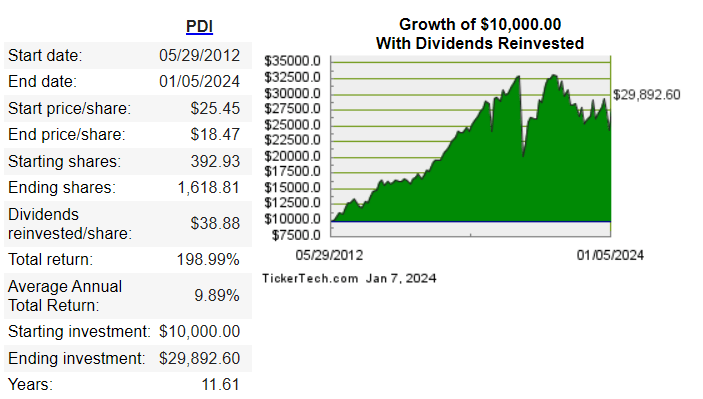

Since going public on 5/30/12 at $25 per share, the share value has seen a decline of -26.12%, but PDI has distributed $38.83 in distributed income without including the declared distribution for January 2024. PDI has distributed $29.19 in the normal monthly distributions, $8.28 in special cash distributions, $0.90 in long-term capital gains, and $0.46 in short-term capital gains. While long-term shareholders are down -26.12% on their original investment, PDI has distributed 155.31% of its original share price in distributed income since going public. This is a yield of roughly 13% on an annualized basis, and that's before considering if some reinvested the distributions.

{kind=link}

I am not looking to take any income from my investments in the near future; rather, I am looking to add to them with new capital while reinvesting the income they generate. My goal is to build out a portfolio of income-producing assets that I can live off of during retirement. Utilizing a DRIP calculator , if you had allocated $10,000 toward PDI when it went public, you could have purchased 392.93 shares. PDI was paying a monthly distribution of $0.177. This would have been a distribution of $2.12 per share, and the lot of 392.93 shares would have produced $834.58 in annualized income. By reinvesting all the distributed income since inception, the share count would have increased to 1,618.81. Based on the increased distribution of $2.65 and the new share count, the new forward-distributed income that the investment would generate is $4,283.37. This is an increase of $3,448.79 or 413.23% in distributed income just by doing nothing. At this point, the original investment would be produced in 2.33 years and gradually decrease every time a distribution is reinvested. From an income perspective, this is very enticing for me, and I am excited to not just hold but add to my PDI position for decades to come unless my investment thesis on the position changes.

{kind=link}

Why I think shares of PDI will appreciate in 2024 leaving investors with positive capital appreciation

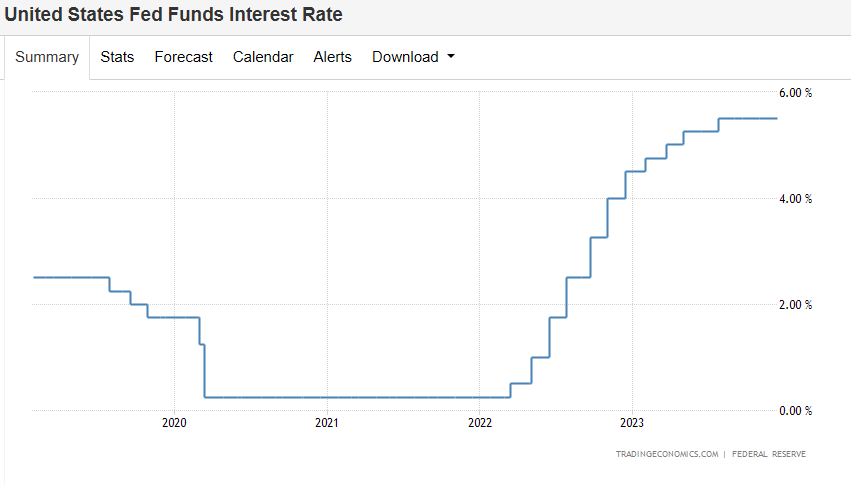

PDI is more or less a yield play, and when the risk-free rate of return exceeds 5%, there is much less of a reason to take on risk to generate yield. The fact that people created and regurgitated the phrase T-bill and chill is an indication of how enticing rates were to a segment of the investment community. PDI's assets consist of debt obligations and other income-producing securities, including mortgage-backed securities, investment grade, and high-yield corporates, developed and emerging markets corporate and sovereign bonds, other income-producing securities, and related derivative instruments. The higher rate environment is not favorable to PDI's underlying assets, and during the rising rate environment, shares of PDI declined from the mid $20s to the upper to mid-teens.

In a rising rate environment where the risk-free rates on money markets were gradually increasing or, long-term rates could be locked in, or ladder could be built with multiple maturity dates through CDs and treasuries, there was less of a reason to invest in corporatized debt instruments. If you were to purchase a bond with a 5-year maturity rate and a 5% coupon for a par value of $1,000, you would receive $50 in annualized interest and the principal upon maturity. When interest rates increase, the value of the 5% coupon bond will fluctuate to the downside. If rates went to 7% and new bonds generated a 7% coupon, the bonds with a 5% coupon would trade at a discount to their face value. PDI's yield looks so high because its underlying assets have declined in value, which has pushed the share price lower and the yield higher.

{kind=link}

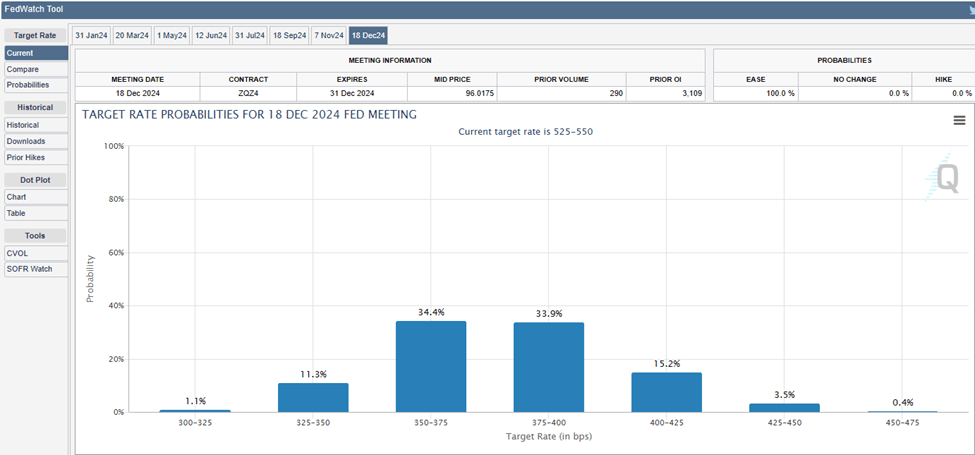

At the last FOMC meeting , Jerome Powell specifically stated that the Fed believes they are likely to be near or at the peak of its tightening cycle. He also disclosed that Fed members took an individual assessment as to what they felt would be the appropriate path going forward. The results indicated that the Fed Funds Rate was at 4.6 percent at the end of 2024, 3.6 percent at the end of 2025, and 2.9 percent at the end of 2026. The CME Group FedWatch Tool indicates that there is a 68.3% chance that rates will close out in 2024 somewhere between 350 bps and 400 bps. The market is pricing in more cuts than what the Fed is saying, but regardless of whether the Fed sticks to its plan or provides additional cuts, the fact is that the Fed is at the end of its tightening cycle. Regardless of whether rate cuts start in March or June, the probability is on the side of multiple cuts during the 2024 calendar year.

As rate cuts start to occur, the risk-free rate of return will continue to decline. We have already seen the yields from the 2-year and 10-year significantly decline. I believe that once the rate cut cycle officially starts, investors looking for yield will start to exit risk-free options and venture back into corporatized debt instruments. We may even see some investors try to front-run a shift from the Fed. As the yield on risk-free rates declines, we should see debt instruments trading at a discount start to appreciate as there will be a larger market for higher-yielding assets. This should push PDI's NAV and shares higher, and I feel that 2024 could be a positive year for shares of PDI.

{kind=link}

Conclusion

I am long PDI and plan to add to my position throughout 2024. Once the Fed starts to cut rates, I think we will see a race to buy discounted yield instruments as new debt will be issued with lower coupons. While investing in PDI comes with multiple risks, I think it's in a position to have a multi-year tailwind from a cutting cycle, and I want to grab more PDI at discounted prices. I am reinvesting every distribution to let the powers of compounding work their magic. Ultimately, I think PDI can generate capital appreciation with a yield on cost that exceeds 14%, depending on when shares are purchased. This could be one of the income investments that provides large amounts of income with a side of modest capital appreciation to investors in 2024.

For further details see:

PDI Looks Like It Bottomed And Is Still Yielding Over 14%