PDI - PDI Yields 13.76% And I Am Adding To My Position

Summary

- Since inception, PDI has never missed a monthly dividend and generated $36.18 per share in income.

- PDI has generated 145% of its initial share price in income since inception, and when the dividends are netted from share declines, there is a 10.89% annualized return.

- I believe shares have established a bottom, and 2023 could be a good year for the share price of PDI.

PIMCO is synonymous with fixed income and manages $1.69 trillion for central banks, sovereign wealth funds, pension funds, corporations, foundations, endowments, and individual investors globally. With helping clients meet their objectives for over 50 years, PIMCO has become a premier investment house, with 66% of its assets outperforming benchmarks over a 5-year period. With U.S. 2-year treasury notes yielding 4.26% and a 1-year CD rate producing a 4.3% yield, traditional equities such as Morgan Stanley ( MS ) offering a 3.54% yield aren't as enticing as they once were for income investors. From the standpoint of generating passive income, we're not living in a low-yield environment, and investors don't need to take on equity risk to generate respectable levels of yield. Even dividend ETFs constructed from world-class companies, such as the Schwab U.S. Dividend Equity ETF ( SCHD ), aren't as appealing as they once were from an income perspective as it produces a 3.30% yield. SCHD is a great fund which I am a shareholder of, and MS is a great company, but times have changed, and when income investors can generate over 4% with zero downside risk, the alternatives in 2023 for income are certainly appealing.

There is nothing wrong with investing in traditional equities when looking for yield, but I am incorporating more high-yielding investments into my portfolio. The PIMCO Dynamic Income Fund ( PDI ) has been stuck in a downtrend, but a bottom may be forming. PDI has been a high-yield investment I have been adding to as it is a combination of PIMCO's best income-generating ideas, with an established track record of generating income, and yields 13.76%. Nobody can predict the future, but PDI looks interesting as inflation continues to decline, and there are real-time indicators that the fed could make a pivot in the first half of 2023. PDI had a terrible 2022, which hasn't been the same since the pandemic's start, but the tide could change over the next several months. I am continuing to add to my position in PDI as I am looking for history to repeat itself over the next decade.

How PDI operates and builds a portfolio geared toward income-producing assets

PDI utilizes a dynamic asset allocation strategy among multiple fixed-income sectors in the global credit markets, including corporate debt, mortgage-related and other asset-backed securities, government and sovereign debt, taxable municipal bonds, and other fixed-, variable- and floating-rate income-producing securities of U.S. and foreign issuers to meet its investment objectives. PDI is a closed-end fund that focuses on current income as its primary objective while seeking capital appreciation as a secondary goal.

PDI invests in a global portfolio of debt obligations and other income-producing securities of any type and credit quality with varying maturities and related derivative instruments. PDI invests in investment-grade debt securities and below-investment-grade debt, including securities of defaulted and stressed issuers. PDI will not normally invest more than 20% of its total assets in debt instruments, other than mortgage-related or asset-backed securities, that are at the time of purchase rated CCC+ or lower by S&P and Fitch and Caa1 or lower by Moody's, or that are unrated but determined by PIMCO to be of comparable quality. PDI may normally invest up to 40% of its total assets in bank loans and will not normally invest more than 10% of its total assets in convertible debt securities.

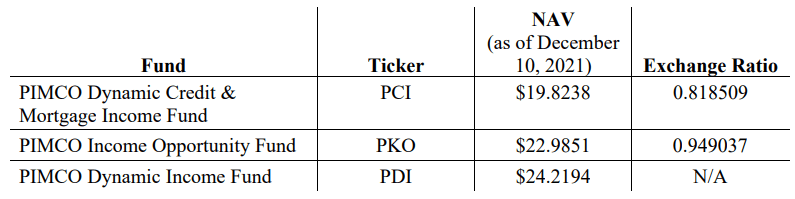

Two of PIMCO's other funds , the PIMCO Dynamic Credit & Mortgage Income Fund (PCI) and PIMCO Income Opportunity Fund (PKO) we reorganized into PDI on Friday 12/10/21. PDI acquired all of the assets and assumed all of the liabilities of each of PCI and PKO in exchange for newly-issued common shares of PDI. The exchange was based on the net asset value per common share of PCI and PKO.

{kind=link}

PDI's historical performance

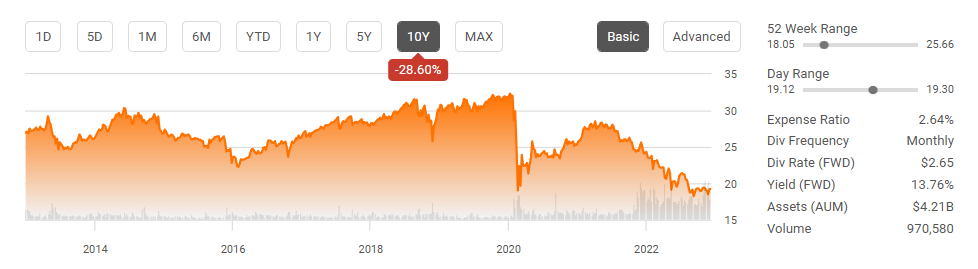

PDI debuted on 5/30/12 at $25 per share. Over the past decade, PDI has declined by -28.6%, and shares have recently formed a bottom. A level of resistance of around $18.20 has been established since 9/26/22. PDI declined to $18.25 on 9/26, then appreciated and receded to $18.21 on 10/14/22. PDI then hovered around the $19 level for around 2 months prior to dropping to $18.29 on 12/28. Looking at PDI over the last year, it was stuck in a channel of making lower lows until the end of September, and now it looks like a bottom has formed.

{kind=link}

{kind=link}

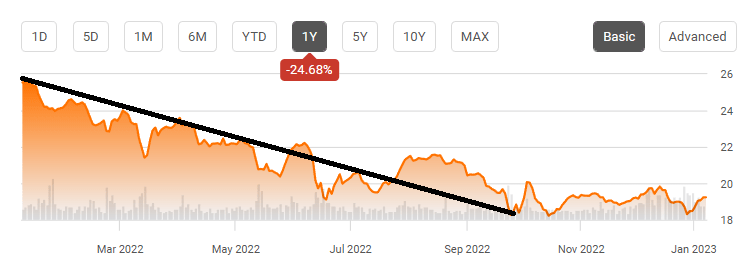

Since PDI was formed, it has traded at a premium to its NAV for the majority of its existence. The fact that PDI has declined by -24.68% over the past year, but the fund trades at a premium to its NAV isn't concerning to me. PDI experienced a period where it briefly exceeded a premium of 20% and, for a significant period of time, exceeded 10%. I don't believe paying a single-digit premium is unwarranted, as PDI hasn't traded at a discount for an extended period since the beginning of 2016. If the market turns in 2023, we could see PDI appreciate in value, which should increase the NAV, and even if the premium doesn't expand, the shares will appreciate in value.

{kind=link}

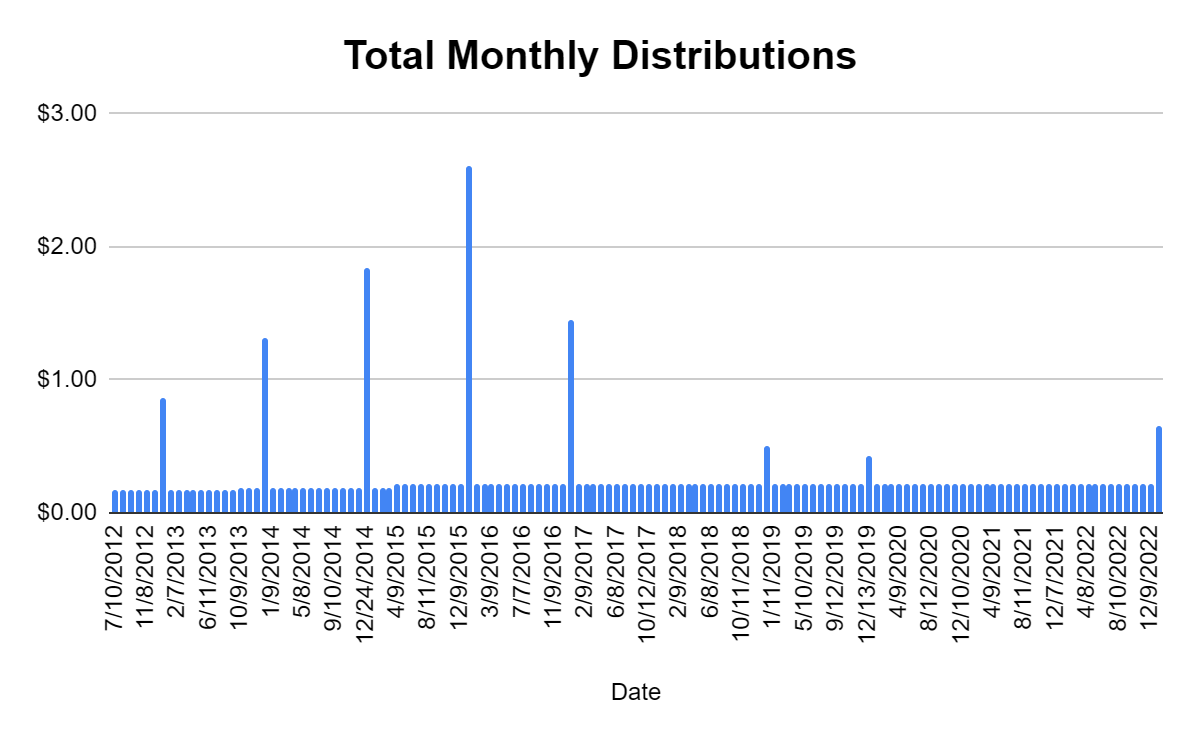

Investors aren't looking at PDI for a capital appreciation vehicle, their main focus is income. Since PDI's inception, each share has generated $26.55 in dividend distributions, $8.28 in special cash dividends, $0.90 in long-term capital gain distributions, and $0.46 in short-term capital gain distributions. Below I constructed a chart of PDI's total monthly distributed income.

PDI hasn't missed a month since inception of distributing cash to its investors. With over a decade of data, this is an exceptional accomplishment. The monthly distribution has also grown by 24.58% from $0.177 to $0.2205. Since 5/30/12, PDI has distributed 106.19% ($26.55) of its inception price in monthly distributions. When all the distributions are accounted for, PDI has distributed $36.18 in income to its investors, which is 145% of PDI's inception price.

Some investors may look at PDI declining by -23.08% since its inception and be turned off, but not me. As an income investor, I look at the entire picture. To date, PDI has declined by $5.77 or -23.08% as shares have fallen from $25 to $19.23 since inception. Without taking compounding into consideration, PDI has generated $36.18 in income since its inception. When you combine the share price of $19.23 and the income generated of $36.18, the total current investment is worth $55.41, which is a 121.64% ($30.41) ROI. This is an annualized return of 10.89% as PDI has been in existence for 11.17 years.

From an income perspective, I wouldn't be upset with these returns. After 11.17 years, an investor would still have their original shares, producing over 13% of annualized income, and would have collected $36.18 over the life of the investment. At this point, the actual share price of PDI is a moot point because it's already paid for the initial investment and is still generating monthly income. Going forward, there is no reason why history can't repeat itself, as PDI hasn't given anyone a reason to doubt its ability to generate income on a monthly basis.

{kind=link}

The next several months could be difficult, but a Fed pivot could be in the works for 2023 and this would be good for PDI.

The Feds goal has been to stop inflation and get back to a 2% level. The CPI reports are a backward-looking indicator, and the Minneapolis Fed President Neel Kashkari sees the fund's rate rising to 5.4% and possibly higher if inflation doesn't trend down. Many economists have also projected that the U.S. will enter a recession in the coming months due to the Fed's tightening and an economy dealing with inflation still running near 40-year highs.

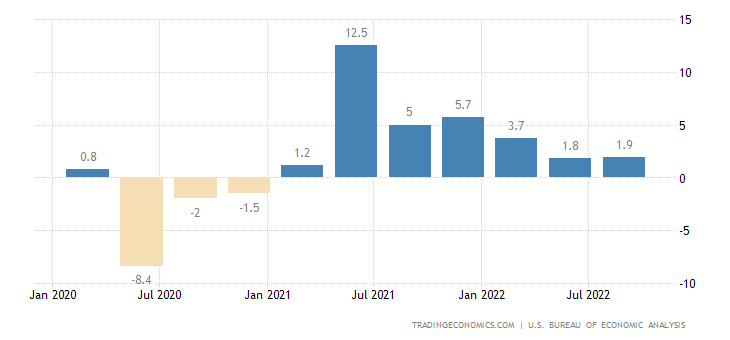

I have a news flash for everyone, you can't change the definition of recession to fit a specific narrative. The U.S already had a recession , as we saw 2 consecutive quarters of declining economic growth in the first half of 2022. Just because the bellwethers of the market, such as Apple ( AAPL ) and Microsoft ( MSFT ) have declined, and technology has been a lagging sector, that doesn't mean we're going into recession. In Q3, the U.S got back to economic growth, and if we see Q4 data that exceeds 1.9% growth, we would need a repeat of 2022, where Q1 and Q2 GDP declines QoQ to see a recession again.

{kind=link}

We already had a recession, and I don't believe another one is in the cards in 2023. Inflation from the CPI reports is a lagging indicator, and it's not telling the story about what is currently happening in the economy. Inflation looks to have topped out in June at 9.1% and is falling faster than it rose. Over the previous five months, inflation has declined by 2% from 9.1% to 7.1%, while it increased by 1.6% in the five months leading into the June peak.

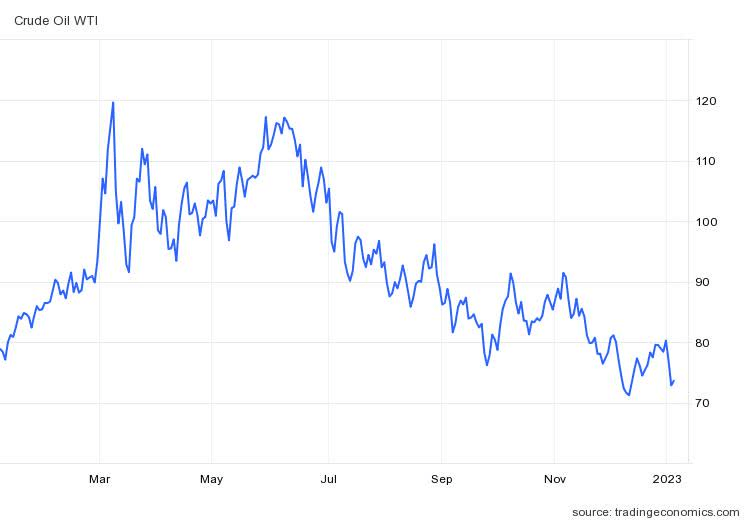

Trading Economics

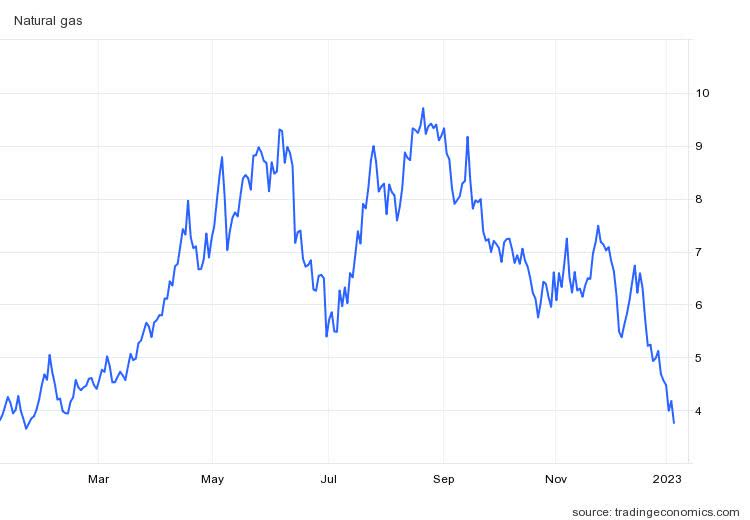

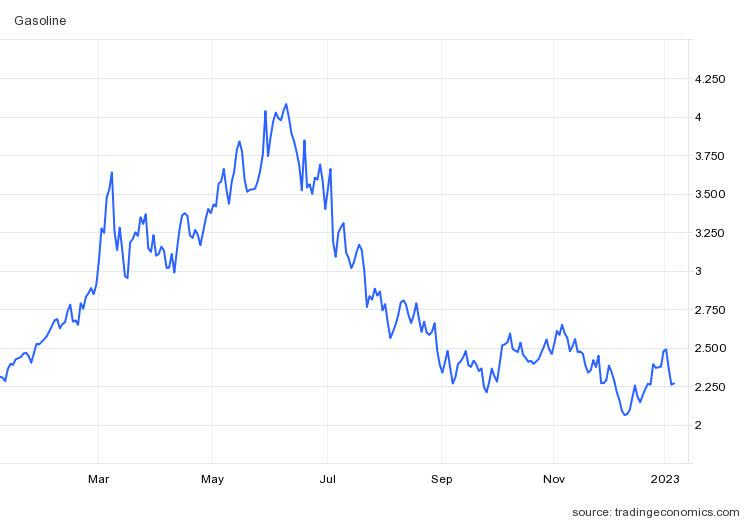

Since June, commodities have also been in a perpetual decline which hasn't been worked through the markets yet. On 6/6/22, gasoline reached $4.08 per gallon and declined from 44.36% to $2.27. Natural gas has declined -59.78% since 6/6/22, falling from $9.30 to $3.74. Crude has declined -37.16% since 6/8/22, falling from $117.15 to $73.62. As major inputs for manufacturing, transportation, and overall business operations decline and the effects work its way through the market, there is no reason why inflation will continue to decline based on CPI reports. Keep in mind, CPI is backward-looking, and commodities have continued to fall. There is a better chance of the next CPI report continuing to decline rather than a surprise increase as prices across the board continue to decline.

{kind=link}

{kind=link}

{kind=link}

If everything stays on the current trajectory, the Fed will have less of a reason to increase rates after the first several months in 2023 and could pivot if inflation declines enough. The key will be commodity markets as they peaked with inflation. I believe that a Fed pivot would be a strong catalyst for PDI as their investments would face less pressure. As many of PDI's investments are in fixed income, mortgages, and credit, a declining interest rate should provide relative strength across the board to its investments.

Conclusion

PIMCO is a world-class asset allocator, and in an environment where I can get over 4% risk-free by locking my capital up in a 1-year CD, sub 4% yielding equity investments are not enticing. From an income perspective, I am looking for solid high-yield investments that have an impeccable track record of returning capital to shareholders. PDI provides a level of diversification to my portfolio because it allocates capital to investment instruments I don't have access to as an individual investor. Since its inception, it hasn't missed a monthly dividend and has returned 145% of its initial share price from dividends. I believe PDI is a strong buy as its yield exceeds 13%, and there is a significant chance that a Fed pivot will occur in 2023, which would be a catalyst for PDI.

For further details see:

PDI Yields 13.76%, And I Am Adding To My Position