PDT - PDT: Income And Gains Potential Means A Lot To Like

2023-07-10 16:56:59 ET

Summary

- Investors today are desperate for any source of income to help them maintain their lifestyles in the face of surging inflation.

- John Hancock Premium Dividend Fund invests in a portfolio of dividend-paying stocks and fixed-income securities to earn a high level of income.

- The common stocks in this closed-end fund are mostly utilities, which provide a degree of protection against inflation along with some resistance to recessions and economic problems.

- The PDT fund recently had to cut its distribution due to a steep decline in the value of its assets over the past eighteen months.

- The fund is trading at a reasonably attractive price and could be good for new money.

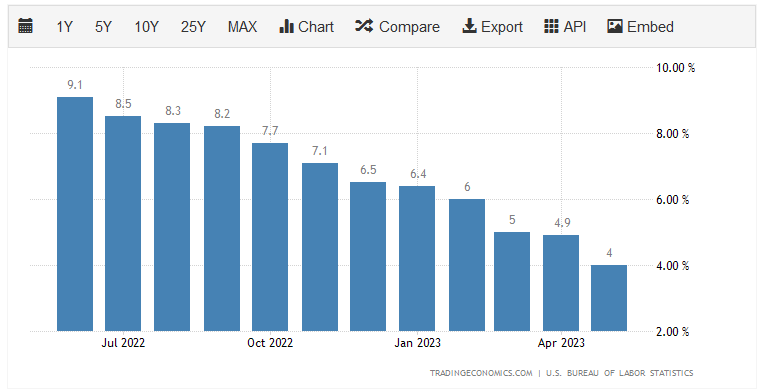

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high inflation rate that has been dominating the economy. For most of the past two years, prices have risen at the highest rate that the nation has seen in more than forty years, making it ever more expensive to provide for our basic needs. This is evidenced by the consumer price index, which claims to measure the cost of a basket of goods that is regularly purchased by the average American household. As we can see here, the consumer price increase has gone up by more than the 2% year-over-year rate that is considered healthy during every month of the past year:

{kind=link}

This has actually caused real wage growth to be down for 26 straight months, which clearly illustrates the budget strain faced by the average person. This is almost certainly the reason why a significant proportion of the population is seeking out second jobs or entering the gig economy simply to make ends meet. That is almost certainly a major reason for the strong job numbers despite every other major indicator of economic performance pointing towards a recession. The above chart does seem to indicate that this problem is getting better, but most of the improvements are driven by the simple fact that energy prices are generally lower than they were in the comparable month of last year.

As I pointed out in a recent article , the core consumer price index, which excludes food and energy, paints a much worse picture of the attempts by the Federal Reserve to get the inflation rate down. The takeaway from all of this is that most people in the United States today are desperately in need of additional sources of income.

As investors, we are certainly not immune to this. After all, we need to eat and heat our homes just like anyone else. However, we do have methods that we can employ to accomplish this goal besides working extra hours. For example, we can put our money to work for us earning an income. One of the best ways to accomplish this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well-followed by the financial media and most investment advisors are unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have to make an informed decision. That is a shame, because these funds offer a number of advantages over more familiar open-ended and exchange-traded funds. In particular, a closed-end fund is capable of using certain strategies that have the effect of boosting its yield and total return well beyond that of pretty much anything else in the market.

In this article, we will discuss the John Hancock Premium Dividend Fund ( PDT ), which is one fund that can be employed by investors that are looking to earn an income. Unlike most income-focused funds, though, it has some potential for capital gains and some inbuilt protection against the ravages of inflation. These are very appealing things when we consider that the fund has an 8.68% yield at the current price. I have discussed this fund before, but a few months have passed since that time, so naturally several things have changed. This article will, therefore, focus specifically on these changes and provide an updated analysis of the fund's finances.

About The Fund

According to the fund's webpage , the John Hancock Premium Dividend Fund has the stated objective of providing its investors with a high level of current income along with modest capital appreciation. This is not surprising considering that this fund is invested in a mix of common equity and fixed-income securities:

CEF Connect

As I have pointed out in numerous previous articles, preferred stocks and bonds deliver all of their lifetime investment returns in the form of direct payments to the shareholders. An investor will purchase a bond at its par value when it is issued, receive a regular interest payment from the issuer of that bond, and then receive the par value back from the issuer on the maturity date. Thus, there are no inherent capital gains for an investor that holds the bond for its entire lifetime. This is because there is no inherent link to the growth and prosperity of the issuing company. The same thing is true for preferred stock, except that preferred stock does not have a maturity date. However, in many cases, the company does have the ability to repurchase the preferred stock at its par value, which is the same price that investors paid to purchase the securities when they were issued. While both of these securities do have the ability to deliver capital gains to traders that are trying to capitalize on price fluctuations prior to the maturity date, the securities themselves deliver no net capital gains over their lifetimes.

It is a different story from common stocks. These securities do deliver capital gains since they increase in value as the issuing company grows and prospers. Thus, this fund will be able to benefit from that as more than half of the portfolio consists of common stocks. As the name of the fund implies, this one focuses specifically on dividend-paying common stocks, primarily in the utility sector. It states this on its webpage:

{kind=link}

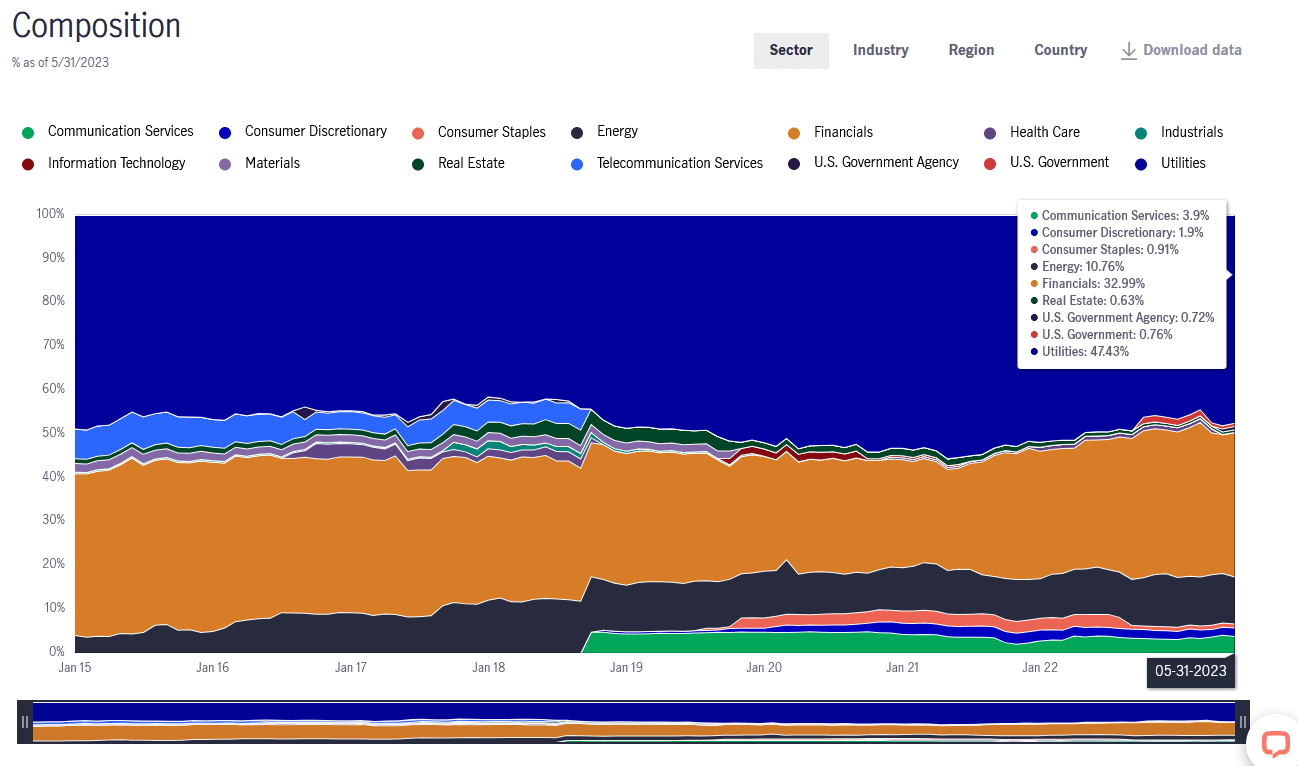

Companies in the utility sector are common investments for retirees and other conservative investors for a variety of reasons. These include the fact that these companies tend to enjoy very stable cash flows through any economic environment and pay out a significant proportion of their cash flows to the investors as dividends. Currently, 47.43% of the portfolio's assets are invested in utility stocks:

{kind=link}

This is something that is fairly nice to see today, considering that there are numerous signs that the economy may soon enter into a recession. In fact, the Federal Reserve has been attempting to push the economy into a mild recession to try and get the inflation rate down. The utility sector in general is much more resistant to recessions than companies in other industries due to the fact that the products provided by these companies are considered necessities for daily life. After all, nobody is going to go out to eat in a restaurant when the electric service to their home is about to be shut off. As such, many of the companies that the fund is invested in should be able to weather any near-term economic problems better than companies in many other sectors of the economy.

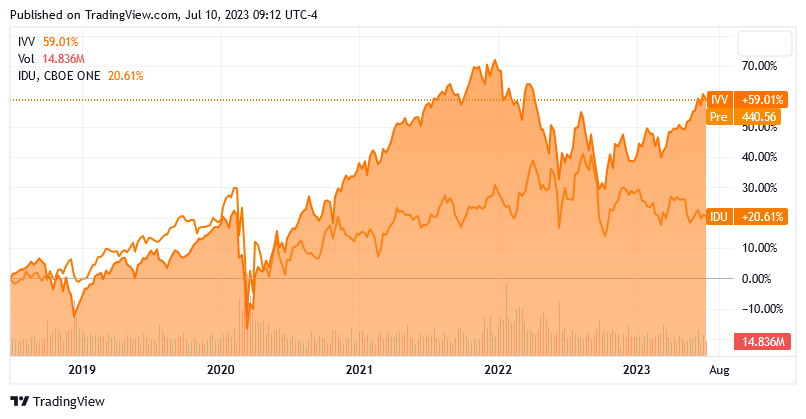

Unfortunately, the utility sector has generally underperformed the broader stock market for quite some time. This chart shows the S&P 500 Index ( IVV ) against the U.S. Utilities Index ( IDU ) over the past five years:

{kind=link}

As we can see, the utilities sector has generally underperformed the broader market over the past five years. This is particularly noticeable during the 2021 and 2023 bull markets which were both driven by strong performance in the technology sector. As a result of this, investors in the John Hancock Premium Dividend Fund would not have received the same capital gains that they would have received by investing in other things. However, the utility sector typically boasts higher yields than technology and most utility companies grow their dividends over time. Thus, this fund's portfolio provides it with a relatively high level of income that should grow over time. That is the sort of thing that appeals to any investor that is seeking income. It should also work pretty well with our thesis of using this fund as a way to generate extra income in the face of today's high inflation rate. The fact that many utilities grow their dividends over time also helps to offset the fact that electric and heating bills have gone up over the past few years.

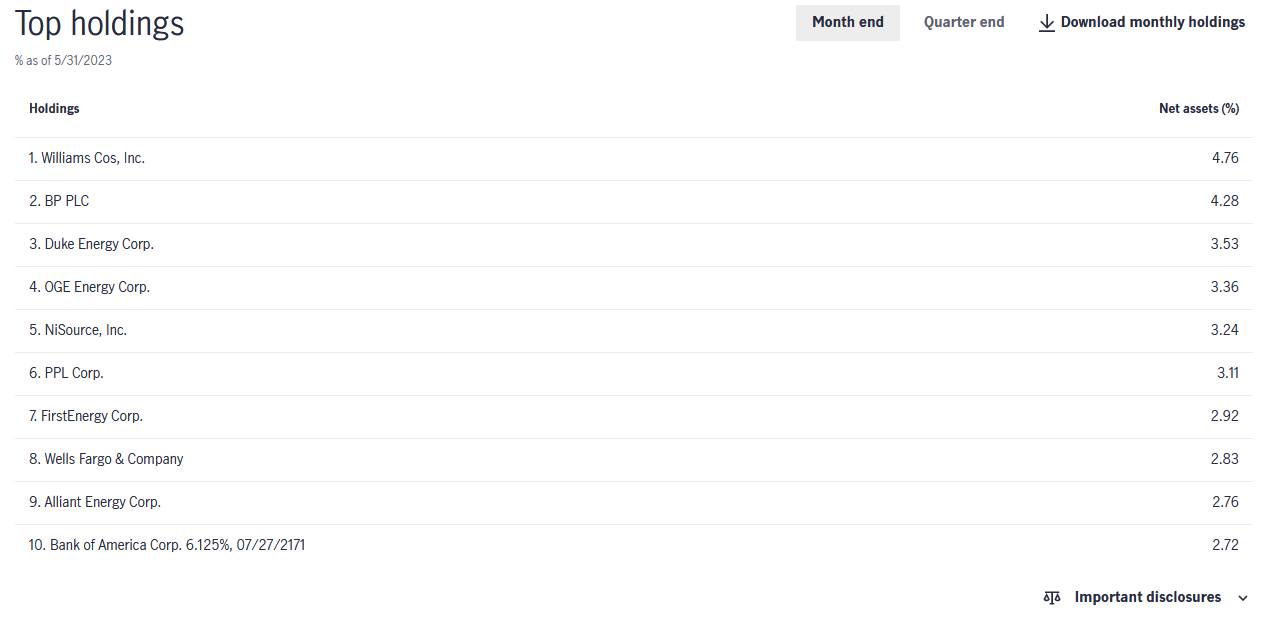

As regular readers are no doubt well aware, I have devoted a considerable amount and time and effort to discussing various utility companies here at Seeking Alpha over the past few years. As such, the largest positions in the fund will probably be familiar to most of you. Here they are:

{kind=link}

We do see that there are a few companies on this list that are not utilities, which reinforces the fact that the fund does have reasonably large allocations to both financials and energy in addition to utilities. In particular, we see BP ( BP ) and Wells Fargo ( WFC ) here, which are obviously not utilities. We also see The Williams Companies ( WMB ), which is generally considered to be a midstream company but shares enough characteristics with traditional utilities that it can arguably be lumped in with them. We also see Bank of America ( BAC ), but that is a preferred stock issue and not a common stock position. The remainder of the companies on the list are traditional electric or natural gas utilities and I have published articles on all of them except for PPL Corp. ( PPL ) at various times in the past. Thus, most of these companies should be familiar to most readers.

For the most part, the top ten holdings list is the same as the last time that we looked at the fund. Indeed, the only change of note is that the NiSource ( NI ) preferreds were removed and replaced with Bank of America ones. This is actually a bit nice to see because it improves the diversity of the fund somewhat. The fact that so few positions have changed could lead someone to assume that this fund has a very low turnover. This is in fact the case as the John Hancock Premium Dividend Fund had an annual turnover of 16.00% last year, which is one of the lowest levels around for an equity closed-end fund. This is nice because it costs money to trade stocks or other assets and these expenses are billed directly to the shareholders of the fund. That creates a drag on the fund's performance and makes management's job more difficult. After all, the fund's management needs to earn a sufficiently high return to cover these additional expenses as well as still satisfy the shareholders. That is a very difficult task to achieve on a consistent basis, and it normally results in actively managed funds underperforming comparable index funds.

In this case, though, we can see that the John Hancock Premium Dividend Fund has generally underperformed its benchmark blended indices during bear markets but has outperformed during bull markets:

{kind=link}

Overall, this is a reasonable track record and shows that the fund's management appears to be doing a reasonably good job of achieving a high level of performance. However, this fund does underperform the S&P 500 Index, but it is using an entirely different investment strategy so that is to be expected. An investor looking for income will generally not invest in the S&P 500 Index because the market has an incredibly low yield that is incapable of providing a reasonable level of income. As of the time of writing, the iShares Core S&P 500 ETF yields 1.50%, which means that a $1 million portfolio will produce $15,000 in annual income. That is nowhere close to enough income to support the lifestyle of someone that has managed to save up $1 million over their lifetime. This fund uses an entirely different strategy to achieve a much higher yield, but it, unfortunately, has to sacrifice some capital gains potential to achieve it.

Interest Rate Risk

As stated numerous times throughout this article, the John Hancock Premium Dividend Fund is a blended fund that keeps a bit less than half of its assets in fixed-income investments such as preferred stock and bonds. This is nice for income because fixed-income securities usually have higher yields than common equities, but it also exposes the fund to interest rate risk. This is due to the fact that the market price of preferred stocks and bonds varies with interest rates. It is an inverse relationship, so when interest rates go up, bond prices go down and vice versa. This is because newly-issued securities will have a yield that corresponds to the market interest rate at the time of issuance. Thus, a security that is issued when interest rates are low will have a lower yield than a security issued when rates are high. The price of each of these securities will fluctuate so that they deliver a yield competitive to a brand-new security with identical characteristics on a given date.

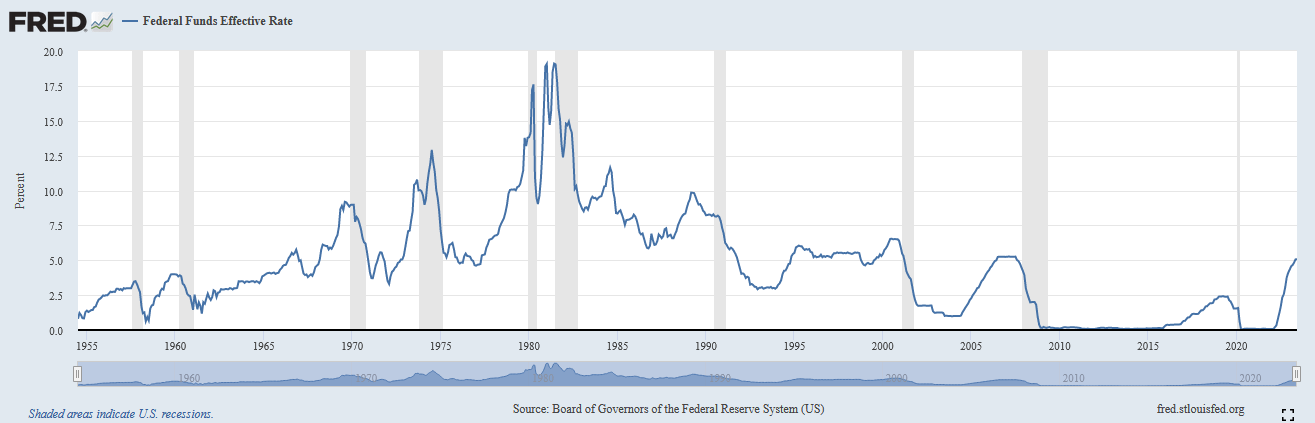

As everyone reading this is no doubt well aware, the Federal Reserve has been very aggressively raising interest rates over the past fifteen months in an effort to combat the high inflation that has been dominating the economy. As of the time of writing, the federal funds rate is at the highest level that it has been since 2007:

{kind=link}

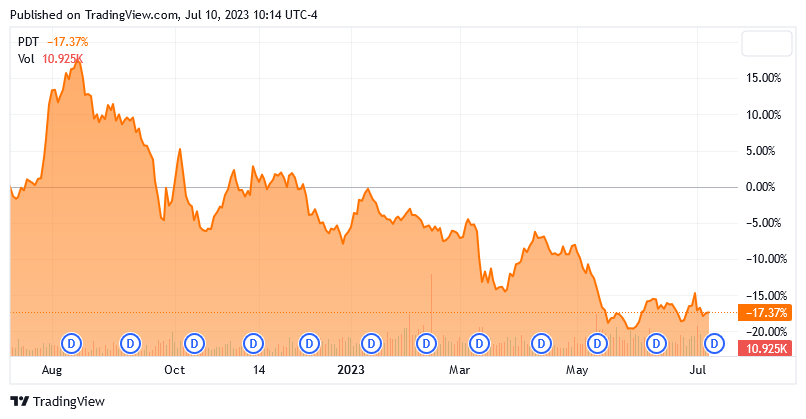

As such, pretty much any fixed-income security issued today will have a higher yield than anything that has been issued in the past fifteen years. While this is good for income investors, it also has the effect of driving down the price of the existing securities contained in the fund. As a result, every bond fund suffered losses over the last year. While the John Hancock Premium Dividend Fund is not a pure fixed-income fund, it does have substantial exposure to bonds. As we can see here, the fund's share price is down 17.37% over the past twelve months:

{kind=link}

That is certainly an annoyance for people that have held this fund for any length of time. However, anyone considering purchasing the fund today will not be affected by the fund's history. The question that they will undoubtedly have is what will happen in the future.

The market is currently projecting that the Federal Reserve will hike rates one more time (in July) and then begin cutting them in the second half of the year. The expectation is that rates will be lower by December than they are right now. However, the Federal Reserve itself has said the exact opposite. The central bank has stated that it will hike rates two more times and will not cut at all, even if the economy descends into a recession. The question is now whether or not the central bank will actually have the political will to allow the economy to be weak during the 2024 presidential cycle. It will undoubtedly be under considerable pressure from politicians to cut rates, which will naturally cause inflation to take off again. It is difficult to predict how the Federal Reserve will react in this situation, but I think that the market is overly optimistic about the near-term trajectory of interest rates and expect that we will continue to see the fund suffer a bit during the second half of this year and potentially in 2024. However, the worst is probably behind us as it is unlikely that any future rate hikes will be nearly as aggressive as what we saw last year. Thus, investors in the fund will likely see some downward pressure from the continuing monetary tightening cycle, but nothing like what the fund experienced over the past twelve months.

Leverage

As mentioned in the introduction to this article, closed-end funds such as the John Hancock Premium Dividend Fund have the ability to employ certain strategies that have the effect of boosting the fund's returns and yield beyond that of any of the underlying assets in the fund. One strategy that is used to accomplish this is leverage. Basically, the fund borrows money and then uses that borrowed money to purchase common stock and fixed-income securities. As long as the purchased securities deliver higher total returns than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective returns of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that leverage is not nearly as effective at boosting returns with interest rates at 5% as it was at 0%, so the benefit that the fund receives from this strategy is going to be much less than it was a year ago.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This is undoubtedly the reason why this fund outperforms its benchmarks during bull markets but underperforms during bear markets. Due to this, it is important that we ensure that the fund is not using too much leverage because that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for that reason. Sadly, this fund greatly exceeds this level as its levered assets currently comprise 39.40% of the portfolio. Thus, it may be exposing its investors to too much risk. While the fund is invested in reasonably safe assets and can probably carry much more leverage than a more volatile growth fund, it is still a near-term concern since the downside risks appear greater than the upside potential right now. Thus, it may be wise not to weight this fund too heavily in your portfolios.

Distribution Analysis

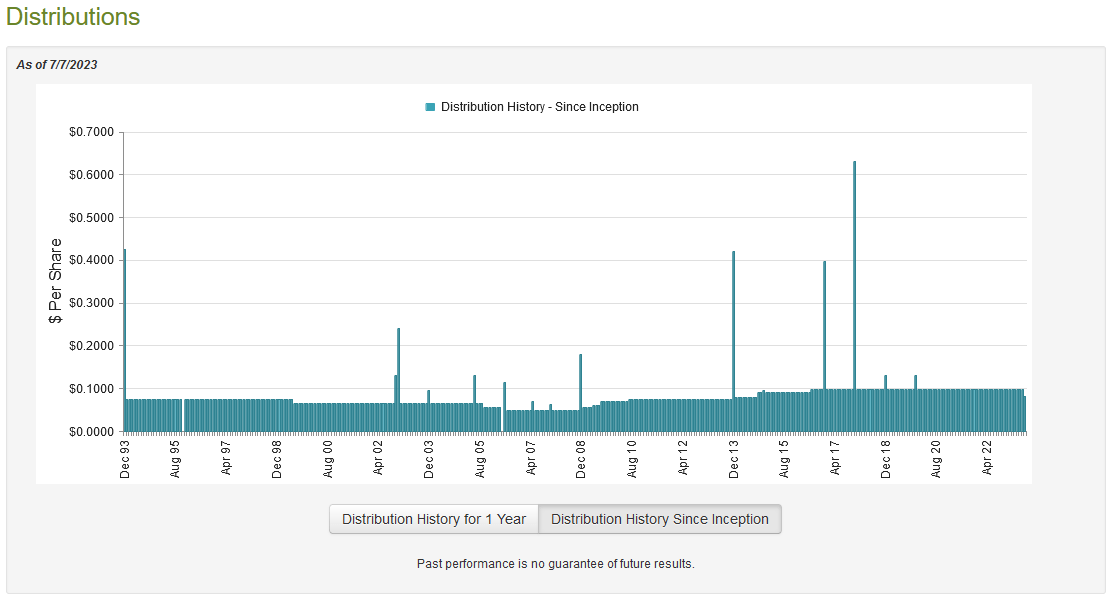

As mentioned earlier in this article, the primary objective of the John Hancock Premium Dividend Fund is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in a combination of dividend-paying common equities and fixed-income securities, many of which have respectable yields in the current market. The fund then applies a layer of leverage to artificially boost the effective yield and total return of the portfolio. It then aims to distribute all of its capital gains and income to the shareholders after covering its own expenses. As such, we can assume that this fund will have a very high yield itself. That is certainly the case as the fund currently pays a monthly distribution of $0.0825 per share ($0.99 per share annually), which gives it an 8.68% yield at the current price. The fund has historically been quite consistent with its distribution, as it has grown it since 2006. Unfortunately, it recently broke its track record and cut the distribution last month:

{kind=link}

The fact that the fund recently cut its distribution is very disappointing considering its historic track record. Prior to this cut, the fund was very appealing to anyone looking for a safe and secure source of income to use to obtain the income that they need to cover their bills and finance their lifestyles. The cut is not surprising though, as the interest hike hikes have had a devastating effect on the asset values of most fixed-income funds. Indeed, with the exception of those funds that are investing in floating-rate securities, just about all of them have had to cut. The same is true of most common stock funds, as 2022 was a rather challenging year for the stock market.

However, anyone purchasing today does not have to worry about the recent distribution cut as it does not hurt them. This is because anyone buying the fund today will receive the current distribution at the current yield and will not be negatively impacted by the distribution cut. The most important thing for these people is how well the fund can sustain the current distribution.

Fortunately, we have a very recent report that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, it will give us a pretty good idea of how the fund performed during the market rally that characterized the first half of this year. It will also provide us with some insight into the events that resulted in the fund being forced to cut its distribution. This is also a newer report than we had available the last time that we discussed this fund, so it will prove quite useful just as an update. During the six-month period, the John Hancock Premium Dividend Fund received $18,285,073 in dividends along with $9,121,798 in interest from the assets in its portfolio. After we subtract the amounts that the fund had to pay in foreign withholding taxes, we get a total investment income of $27,292,647 from the assets in its portfolio. The fund paid its expenses out of this amount, which left it with $13,068,346 available for shareholders. That is, unsurprisingly, nowhere close to enough to cover the $28,745,081 that the fund paid out in distributions during the period. At first glance, this is likely to be concerning as the fund's net investment income was not enough to cover its distributions.

However, the fund has other methods that can be employed to earn the money that it needs to pay out to its shareholders. For example, it might have capital gains that can be distributed. The fund generally failed at this as it reported net realized losses of $26,542,219 that were partially offset by $20,387,138 in net unrealized gains. However, the fund's assets still declined by $20,769,074 after accounting for all inflows and outflows during the period. This certainly explains the distribution cut as most John Hancock funds are fairly conservative and like to keep their asset levels relatively stable. This one saw its assets decline from $725,942,696 on November 1, 2021, to $597,874,907 on May 1, 2023. The fund is thus obviously trying to conserve its assets by reducing the payout. That is admirable, if disappointing to some investors.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the John Hancock Premium Dividend Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of the fund's assets minus any outstanding debt. This is the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of July 7, 2023 (the most recent date for which data is available as of the time of writing), the John Hancock Premium Dividend Fund has a net asset value of $11.69 per share but the shares currently trade for $11.36 each. This gives the fund's shares a 2.82% discount to net asset value at the current price. That is much better than the 0.60% premium that the shares have had on average over the past month. Thus, the current price looks like a very reasonable entry point for this fund.

Conclusion

In conclusion, the John Hancock Premium Dividend Fund is a very good way for an investor today to get a nice income boost to help them maintain their lifestyles in the face of today's very high rate of inflation. The fund also has some built-in protection against inflation due to its high exposure to utilities and energy companies. Unfortunately, the fund does have a fairly high level of leverage and had to cut its distribution recently. With that said though, it still looks like a decent choice for a new investor given its current discount valuation.

For further details see:

PDT: Income And Gains Potential Means A Lot To Like