PDT - PDT: More Tempting After Discount Opens Up

2023-08-20 11:28:58 ET

Summary

- John Hancock Premium Dividend Fund is currently looking like an attractive fund to consider due to its valuation.

- PDT recently underwent a distribution cut, which was the catalyst to open up the latest discount for the fund.

- No one likes distribution cuts, but it can often create some of the best times to get a great deal for a closed-end fund.

Written by Nick Ackerman, co-produced by Stanford Chemist.

I regularly cover John Hancock Tax-Advantaged Dividend Income Fund ( HTD ) as a solid fund for long-term investors. However, when discussing HTD, getting questions on John Hancock Premium Dividend Fund ( PDT ) is inevitable. These funds are fairly similar as they both take an approach of investing primarily in equity utility positions as well as allocating to preferred and fixed-income sleeves.

Today, PDT looks like the better buy to put capital to work if I was choosing between the two. However, the difference in valuation isn't so dramatic that we need to stampede into this swap.

The Basics

- 1-Year Z-score: -2.69

- Discount: -11.06%

- Distribution Yield: 9.77%

- Expense Ratio: 1.48%

- Leverage: 39.35%

- Managed Assets: $950 million

- Structure: Perpetual

PDT's investment objective is "high current income, consistent with modest growth of capital." To achieve this, the fund will "typically invest at least 80% of net assets in dividend-paying securities." Additionally, they are "seeking income from both dividend-paying preferred stocks and common equity securities" and "emphasizing securities in the high-dividend-paying utilities sector."

The fund's total expense ratio, when including leverage, has been significantly impacted by higher interest rates increasing their borrowings. That pushed the total expense ratio to 4.59% in the last semi-annual report from the 2.42% it was at fiscal year-end 2022. That period in itself was a rise from the 1.82% expense ratio that was shown at fiscal year-end 2021.

The fund also has a high amount of leverage, which should be considered. Should a black swan event come along, that could cause the fund to have to deleverage, and that could cause permanent damage. They deleveraged a touch during Covid, but that was a quick bear market with a swift recovery nearly as fast as the crash.

Opportunity Opening Up For PDT

HTD and PDT aren't exactly the same, as they take slightly different weights for each slice, but they are close enough. Even over the longer term of the last decade, the total NAV return was quite similar.

Ycharts

Until recently, the clear choice in the last several years has been HTD over PDT due to valuation. This has now flipped, and PDT is looking like the better value today.

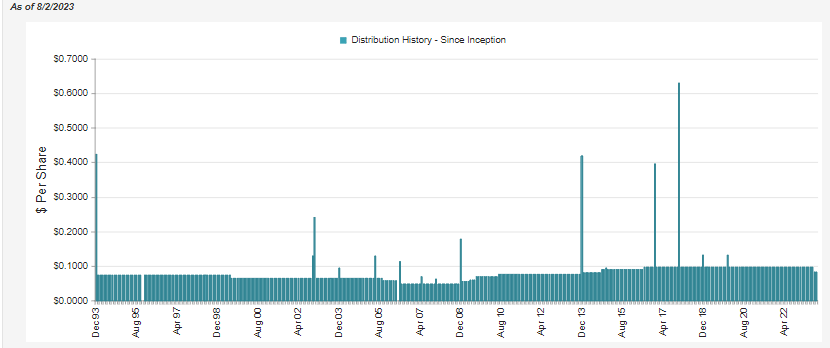

The event to cause this to play out is thanks to a distribution cut from PDT a couple of months ago, while HTD had held steady. The distribution rate for PDT was just out of line and needed to be adjusted back to a more sustainable level. Some fund sponsors allow rates to drift higher than others.

Even after this cut, PDT's distribution rate on a NAV basis is higher relative to HTD, as it comes in at 8.34% compared to HTD's 7.70%. The NAV rate is the more important piece of the puzzle because that's the amount the portfolio has to earn. Prior to the cut, the NAV rate for PDT had started to push into 10%+ levels.

This cut happened after years of PDT maintaining the same distribution payout month after month.

{kind=link}

Investors love a steady distribution, but sometimes it can be relied upon too highly, despite becoming elevated or there being clear risks that should be realized.

Gabelli Utility Trust ( GUT ) is a clear example of this. Investors have bid up that fund to a ~112% premium to its NAV. The distribution rate investors are collecting for that is 8.71%, while the fund's NAV distribution rate comes to 18.5%. If there ever is a cut, investors could look at a massive collapse. Investors aren't even collecting a necessarily attractive distribution rate based on the risks. In fact, investors could do themselves a favor and swap from GUT today and into PDT. They'd instantly reduce the risk of a GUT implosion in their portfolio and receive a higher distribution rate of 8.98%.

Distribution Coverage

Besides the yield itself getting higher for PDT to cause concern and management needing to take action, the pressure from higher interest rates shouldn't be ignored. The rising costs have been putting pressure on net investment income.

Since PDT was trading at a premium previously, they were able to issue shares through an at-the-market offering and through their dividend reinvestment plan. Since it was at a premium, these would have been accretive moves. Going forward, if it continues to trade at a discount, the outstanding share count should remain flat.

{kind=link}

On a per-share basis, the fund had NII of $0.72 last year, and in the last report, it came to $0.27, or what would annualize out to $0.54. As we can see, even after the distribution adjustment, the fund will still require a sizeable amount of capital gains to pay its distribution. This isn't all that unusual for a fund that has a material allocation to equity securities.

It should be noted that the fund utilized futures contracts in what would have thwarted some of the downside moves due to higher yields. This was done by going short 10-Year U.S. Treasury Note futures. Unfortunately, it was a fairly limited amount in terms of gains and didn't have a material impact on the outcome of the fund. At the end of April 30th, 2023, they had no futures contracts listed in their report.

PDT Realized/Unrealized Gains/Losses (John Hancock (highlights from author))

{kind=link}

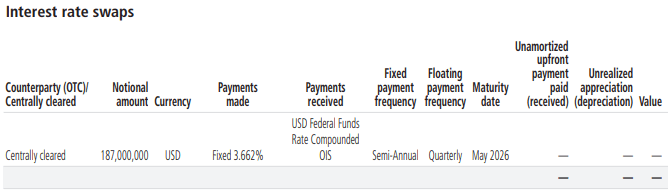

Additionally, last year, the fund utilized interest rate swaps as well to hedge against rising rates. They had no outstanding interest rate swaps at the end of their fiscal 2022 . However, they once again initiated interest rate swaps in their last semi-annual report. This could provide some gains going forward, as we know the Fed has raised rates since this was reported.

{kind=link}

With a notional amount of $187 million and borrowings outstanding of $374 million, that means it's not completely protected, and exposure to higher rates is still there. Their borrowings are based on LIBOR plus 0.625%. At the end of April 30th, 2023, they listed that the borrowings had an interest rate of 5.51%. This would have since increased.

For tax purposes, 2022's total distributions were $1.17. $0.89901 as "ordinary dividends," of which $0.554774 were considered qualified (leaving $0.344236 as ordinary.) There was another $0.27099 listed as long-term capital gains. With this breakdown, PDT could be appropriate for a taxable account, though there is some ordinary seemingly due to some bond weighting in their portfolio.

PDT's Portfolio

The portfolio turnover here is quite low, listed at just 16% in the last fiscal year and only 6% in the last six-month report. It will be interesting to see how the portfolio may change going forward. They have a slate of new managers on this fund with the average manager tenure of just two years - and that's only because one of the gentlemen has been with the fund for eight years. The other three managers - while having experience in the financial industry - are new to this fund, with only 1 year in.

{kind=link}

Overall, portfolio investment policy, I believe, bares the largest impact on the fund and is less often about the management. However, in this case, it felt appropriate to at least acknowledge the new blood for the fund. PDT wasn't the only one to see this change, as this impacted several of John Hancock's funds. That includes these same managers being added to HTD.

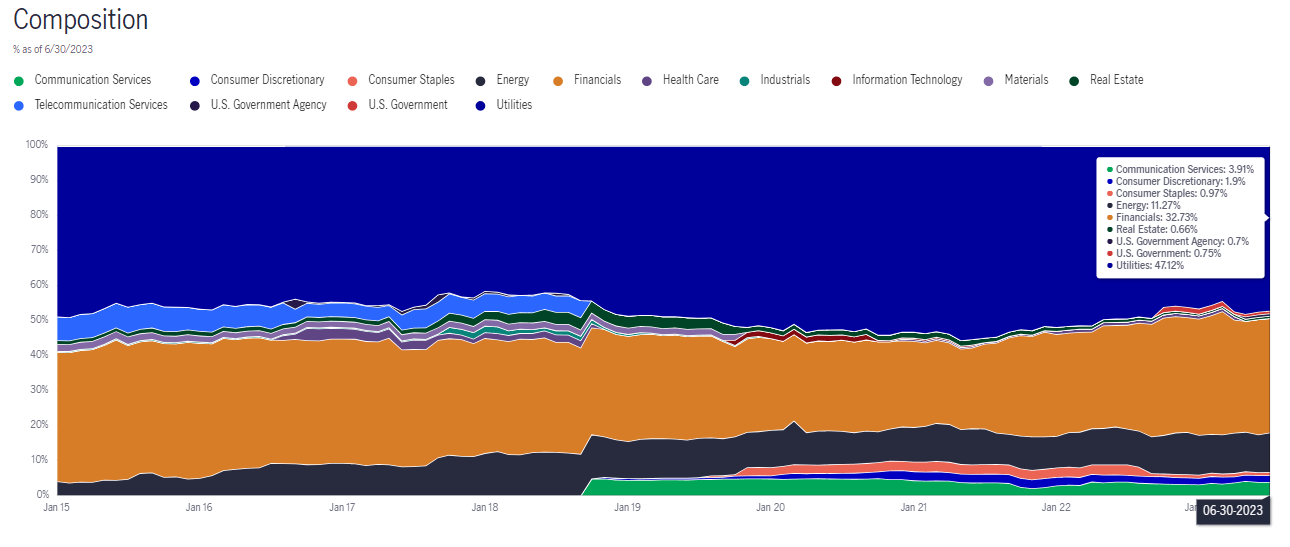

Taking a look at the fund's overall asset breakdown shows us that common equities are the largest weighting in the fund. However, preferred and bond exposure combined represents the majority of the portfolio.

PDT Portfolio Composition (John Hancock)

For comparison purposes, HTD's portfolio ending the same period was 60.8% equity, 19.3% bond and 17.7% preferred.

For sector exposure, the fund has a large weighting to utilities. Financials are the second-largest weighting, but that's going to be mostly comprised of the preferred or bond sleeve of the portfolio. Though not entirely, as there is some bank equity exposure.

{kind=link}

Energy also represents a fairly meaningful allocation to this fund. The positions here are mostly equity positions, and the utility exposure is overwhelmingly allocated through equity positions. Again, similar to the financial sector exposure, it's not exclusive as they also carry some utility bonds.

Given the fund is allocated primarily to utility equity exposure, with preferred and fixed income sleeves, that should make PDT relatively less volatile due to this positioning. That's probably why they feel comfortable ramping up the leverage to such high levels. However, that takes away from the relative safety of the underlying portfolio and creates higher volatility.

It isn't too shocking, but some of the largest positions for PDT are also the same positions we see in the top ten of HTD. Maybe even more interesting is that some of the top positions here were top positions when I last covered this fund in 2020 . That includes Williams Companies ( WMB ) and Duke Energy ( DUK ).

PDT Top Ten Holdings (John Hancock)

Conclusion

PDT generally gets brought up when discussing HTD, for a good reason, as they are similarly positioned. Through most of the last several years, HTD was always the clear choice when putting capital to work. However, after a distribution cut, the opportunity has now swung to favor PDT being the ideal fund to consider based on valuation. The difference isn't so material that I believe a swap between HTD to PDT is so obvious that it should be done today, but something to consider if putting new capital to work and to watch going forward. No investor enjoys distribution cuts, but it's often where the best opportunities can be found in closed-end funds.

For further details see:

PDT: More Tempting After Discount Opens Up