BTU - Peabody: Defying Doubts On The Future Of Thermal Coal

2023-06-27 17:14:53 ET

Summary

- I discuss embracing the potential of thermal coal in shaping Future Energy.

- This involves thinking about digitalization and decarbonization when it comes to thermal coal.

- Challenging the skeptics: Peabody demonstrates the enduring value of thermal coal, defying expectations with resilience and innovation.

Investment Thesis

Peabody Energy Corporation's ( BTU ) business is roughly 50% thermal coal and 50% met coal.

Peabody is very cheaply valued, with strong prospects over the next twelve months.

In this analysis, I put all my focus on thermal coal. The reason for this is that I believe that the bulk of the bear case points to thermal coal as a sunsetting industry.

Indeed, I don't believe reasonable investors are calling for the demise of met coal, which is used to make steel.

With that in mind, let's get to discuss how to think about thermal coal's uses and why consider Peabody? Here's why I'm very bullish on Peabody.

Why Peabody? Why Now?

Peabody's business is 50% tied to thermal coal. That means coal that is used in electricity generation. Now, I want to spend a few moments explaining how I see Future Energy as part of my portfolio.

Future Energy is the confluence of 3 different trends, Digitalization, Decarbonization, and Deglobalization. Within my portfolio of Future Energy, I aspire to participate in two or more of these secular trends in each stock.

In the case of Peabody, it's decarbonization and digitalization. Allow me to elaborate. When everyone is gushing over artificial intelligence, or AI, some understanding of what AI does is necessary.

The best way to describe AI is in this manner. The same leap in computing power to go from a calculator to a PC is the same as going from a PC to cloud computing. And it's about the same leap in computation to go from cloud computing to AI computing.

AI requires tremendous horsepower. Modern deep learning models involve even billions of parameters, and training them can be computationally intensive and require substantial computational resources. OK, that's great, what has that got to do with decarbonization?

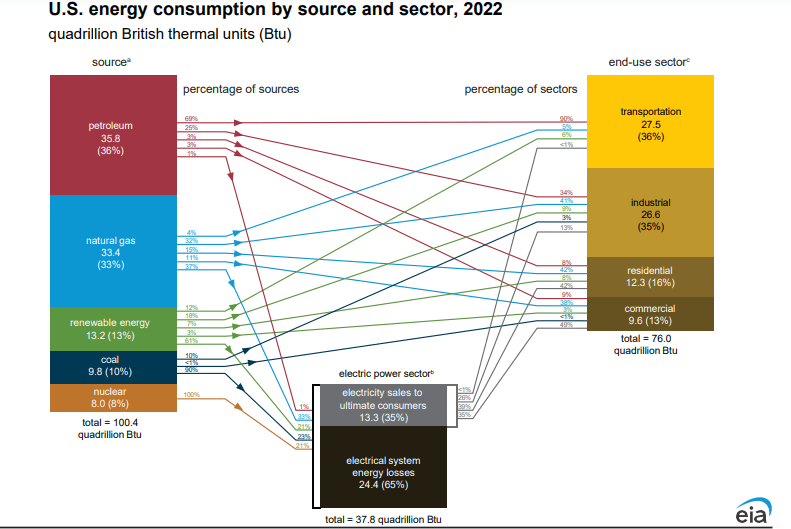

Allow me to highlight the following chart.

{kind=link}

You'll have to click above for the detail. What you'll see is that about a quarter of U.S. electricity comes from burning coal. And about a third comes from natural gas.

What this means, is that even if there's an ambition towards decarbonization, the reality is that nearly a quarter of U.S. electricity sources come from coal. This is an unavoidable fact.

And my question is this, how many more years until this significantly stops being the case?

Having already alluded to the digitalization trends, allow me to provide further context. In your home in the next few years, you'll have significantly more electricity demand. This will be the source of charging your electric vehicles, or EVs, as well as cooling your home (with air cons) and heating your home (with heat pumps).

The aspiration is that, in the future, EVs will be ''cleaner.'' But they are only cleaner depending on where the input to charge the EV comes from. And this goes back to decarbonization goals.

To decarbonize our energy sources, we must bring some other replacement energy sources. The obvious replacement is wind and solar energy. However, I honestly don't believe that in the next 6 or 7 years, before 2030, we'll massively succeed in replacing our coal consumption all the way to zero. So, keep this figure in mind, of 6 years, because I'll come back to it soon.

Why Context Matters?

I recognize that in 2023, demand for thermal coal was nowhere near as strong as many had hoped it would be. The warm winter last year didn't help matters.

Also, the fact that natural gas was so cheap throughout 2023, nearly all power plants adopted natural gas for running their power plants, rather than coal.

As a consequence, this led to an overabundance of thermal coal. But is this where this story ends?

I truly don't believe it is. And I'll explain why.

In the first instance, I passionately declare that we are going to need a lot more electricity to digitalize our economy. I've already talked about EVs and AI, but also, note that all our appliances in our home will be smart.

Think about your fridge telling you that you haven't consumed enough leafy green vegetables or your coffee machine telling you that your pulse is high and since you didn't sleep well last night, you should probably have a nap rather than a power-up a double-expresso.

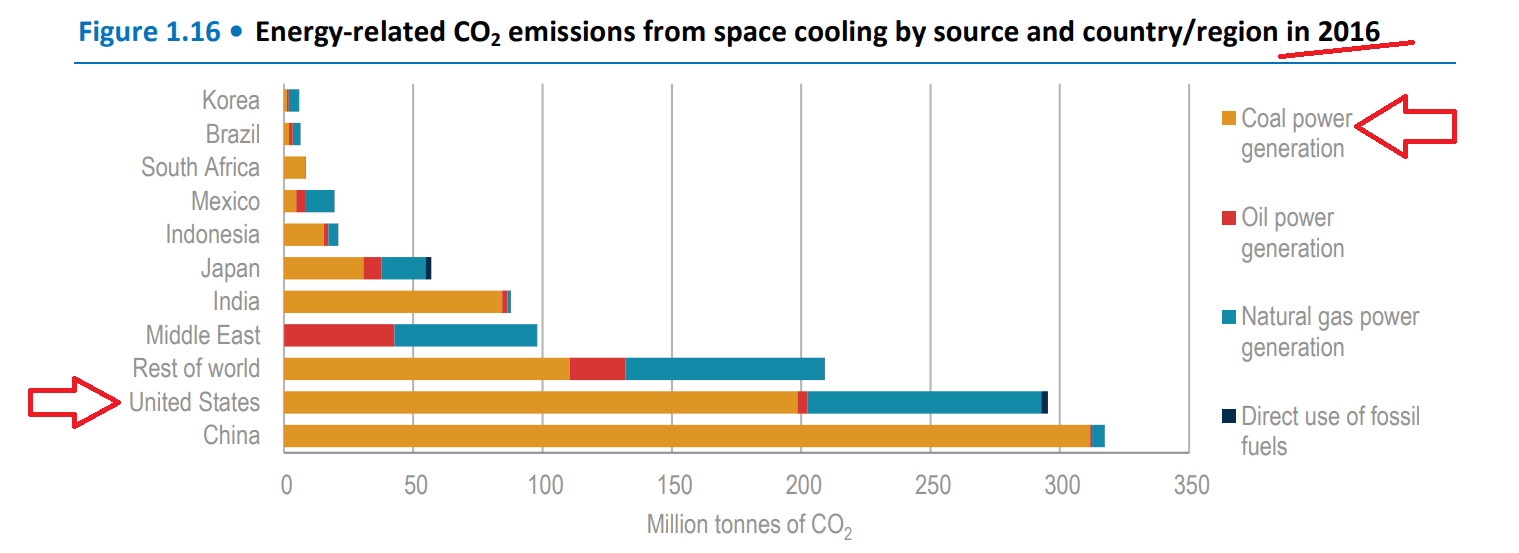

Secondly, consider the chart below:

{kind=link}

The chart is a few years out, but it works for our purposes. It shows that 54% of global CO2 emissions caused by cooling come from power stations in the United States and China, which rely heavily on coal.

Of the 2.8 billion people living in the hottest parts of the world, only 8% currently possess ACs, compared to 90% ownership in the United States and Japan (EIA data ).

The implications are obvious: as countries become wealthier, more households will look to air conditioners to keep cool.

The Bull Case Focuses on This

I believe that Peabody will make approximately $1 billion of free cash flows this year, and probably a similar figure next year.

Given that the stock is priced at 3x free cash flow, what this means is that investors believe that Peabody's prospects will be finished in 3 years.

Even putting aside Peabody's massive capital returns program where Peabody is determined to return at least 65% of its free cash flows, even more simply than this, the argument the market is making is that within 3 years we'll no longer need thermal coal.

Meaning that the market is pricing in approximately half the lifetime value of this company, which is even more aggressive than political aspirations to bring coal use down by 2030.

This is an argument that I simply don't see as holding much water, once we look into the real fundamentals of the thermal coal industry.

The Bottom Line

In my analysis, I examine Peabody Energy Corporation, a company with a 50% stake in both thermal coal and met coal businesses.

While many see thermal coal as a declining industry, I believe met coal, which is used in steel production, has a more promising future.

Furthermore, understanding the significance of thermal coal's applications and considering Peabody's position, I have a bullish outlook on the company.

Peabody's ties to decarbonization and digitalization align with the Future Energy trends that I aim to incorporate into my investment portfolio.

With the increasing demand for electricity due to factors like electric vehicles and smart appliances, the need for coal-generated power persists, even amid decarbonization goals.

Additionally, the growing adoption of air conditioners in countries like the United States and China heavily reliant on coal-based power stations presents opportunities for Peabody Energy Corporation. The market's belief that thermal coal will become obsolete within three years, reflected in the stock's valuation, seems overly aggressive when examining the true fundamentals of the thermal coal industry.

For further details see:

Peabody: Defying Doubts On The Future Of Thermal Coal