BTU - Peabody Energy - An Assortment Of Good And Bad Sub-Plots

2023-10-09 15:28:05 ET

Summary

- Peabody, a mid-cap play on thermal and metallurgical coal, has underperformed other mining stocks this year.

- We touch upon a few key fundamental themes.

- We close with some thoughts on the valuations, technicals, and important stakeholder positioning.

Company Snapshot And Performance

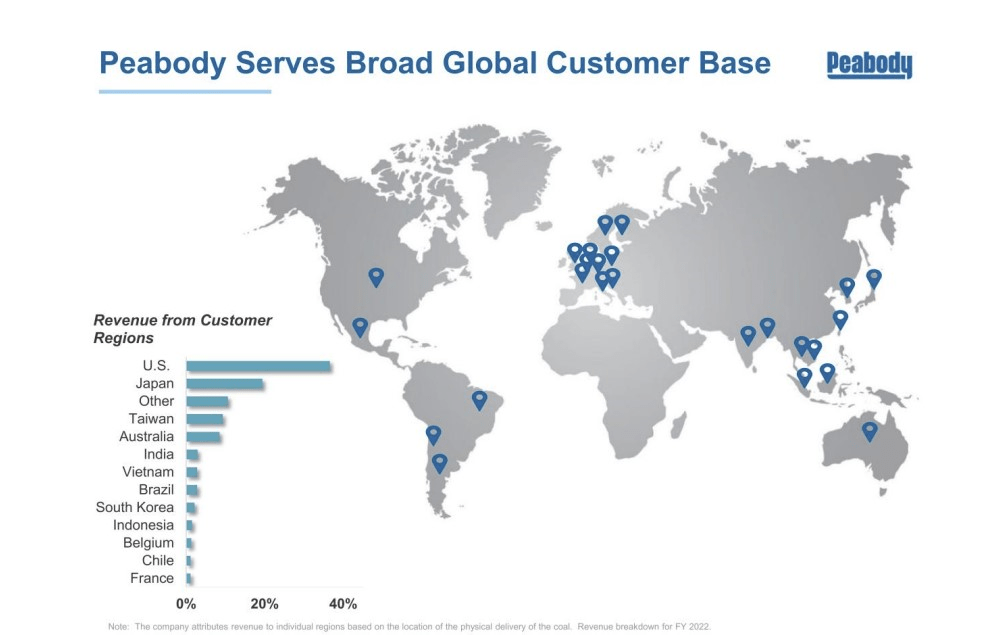

Peabody Energy Corporation (BTU) can be construed as a mid-cap play on both the metallurgical and thermal coal markets. This company owns, or manages 17 coal mining operations across the US and Australia, whilst it also serves as a broker or middleman for other coal producers. An overwhelming majority (~85%) of BTU's volumes come from long-term coal supply arrangements, with the likes of utilities, industrial units, and steel entities, with close to 40% of its client base based in the US alone.

{kind=link}

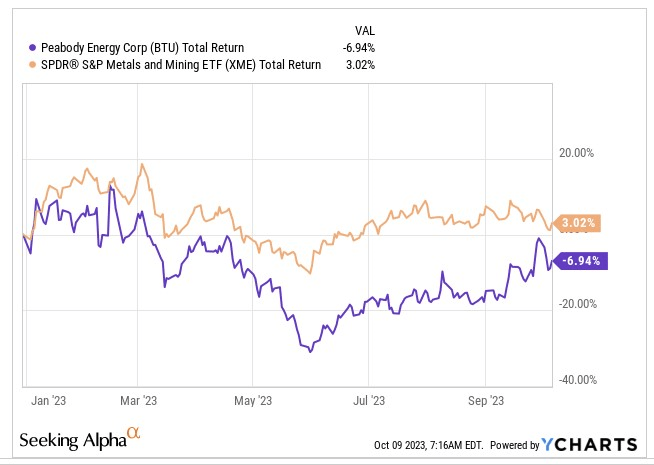

On a YTD basis, BTU's stock performance has been nothing to write home about, losing -7% of its value, even as its metal and mining peers have managed to eke out marginal gains.

{kind=link}

The Fundamentals

As far as the fundamentals are concerned, we would pay keen attention to dynamics impacting BTU's seaborne metallurgical mining division, which was the largest contributor of group EBITDA ( 42% share) and also has the most attractive EBITDA margin per ton profile (by far) amongst all the four divisions.

Annual Report 2022

The pricing picture in the seaborne met coal market has been abetted by subdued supplies particularly out of Queensland (unappealing residual wet weather impacts), and robust import momentum from India in particular (which will likely now be passed on by domestic mills there), whose domestic steel production credentials are proving to be an X factor of sorts, and will soon overtake China

So far so good, but investors may want to consider that the coking coal import momentum in India is now showing signs of slowing down there. Coking coal import traffic in India, which had been growing at 10% levels in the preceding two months, recently slowed down to 6% as of the October report. It's also worth noting that after a fairly resilient Q2, BTU management did suggest that BTU's seaborne metallurgical volumes would drop off sequentially by around 1.5m tonnes in Q3.

Conversely, BTU's seaborne thermal export volumes in Q3 will likely be a lot more resilient compared to Q2 (2.7m ton sequential progress in Q3 relative to Q2) and whilst there could be a seasonal pickup in restocking ahead of the winter months, do consider that the medium-term outlook for pricing isn't the most robust. Europe appears to have made significant inroads in boosting gas storage capacity levels, whilst India's domestic coal mining capabilities have been boosted this year, thus reducing the reliance on thermal coal imports, particularly from Australia where BTU is based. All in all, Newcastle thermal coal prices are expected to drop by 18% this year, and could fall by another 5-6% p.a. over the next two years, before hitting levels of $130/ton by 2027.

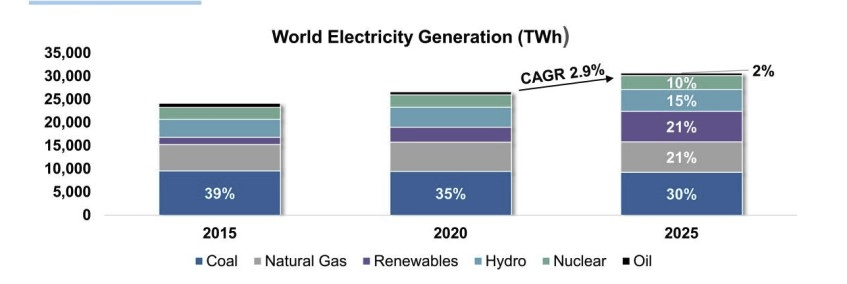

In fairness, despite the relatively sobering outlook on long-term prices, it's still worth highlighting that coal will still serve as the largest source of electricity generation (30%) for the foreseeable future.

{kind=link}

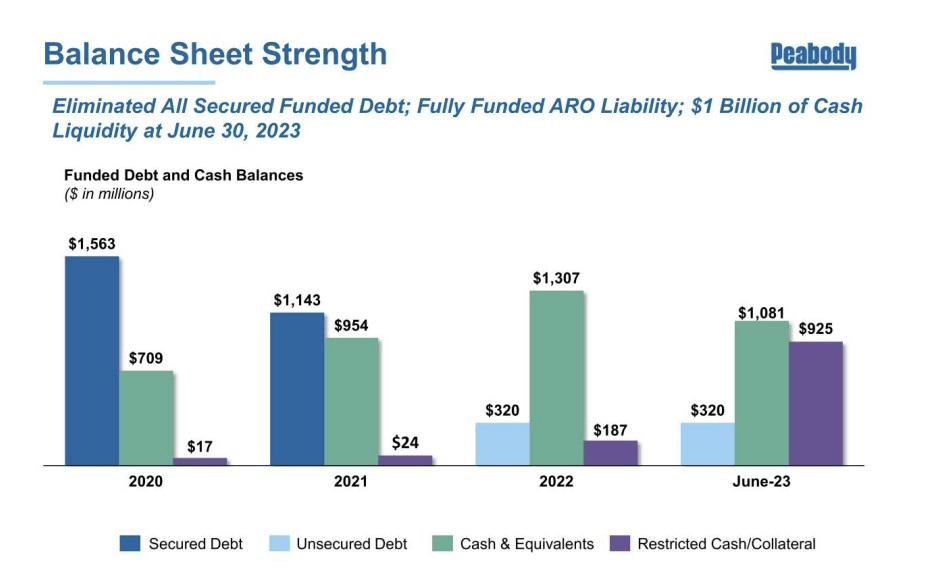

Whilst the outlook for coal looks rather ambiguous, we certainly feel a lot more confident about BTU's balance sheet and its ability to not just support the growth ambitions of this business but also shareholder distributions.

For the uninitiated, note that a few years back, this was a business that was carrying over $0.9bn of net debt (debt over cash) on its books, but these days that position has almost reversed with a net cash position (cash over debt) to the tune of $0.7bn. BTU has also garnered an added degree of flexibility in its funding profile, in that it no longer carries any senior secured debt like it did a few years back ($1.5bn as of FY20).

One can also always have a lot of time for companies that take the time out to craft explicit plans to share their largesse with the shareholder base, and BTU did something of that ilk at the start of Q2-23.

The company's goal now will be to return 65% of its Available Free Cash Flow (AFCF) which is essentially what's left of the operating cash flow every quarter, after accounting for investing cash flow, other anticipated expenses, distributions to noncontrolling interests, and adjustments to restricted cash and collateral agreements. In H1, the onus was down to just dividends ($0.075 per share) and buybacks, but looking ahead, you could also have an additional floating component to the dividend, that will be linked to FCF generation in any given quarter.

{kind=link}

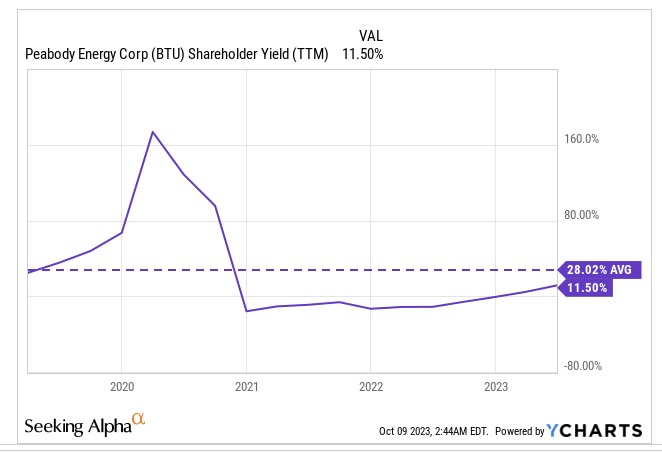

It's worth noting that despite a pickup in the distribution profile of BTU in recent months, the stock's shareholder yield (this is a function of dividends, buybacks, and debt paydowns) is still not even half as good as its 5-year average, so there's still ample scope for this to pickup.

{kind=link}

But then again, investors may not want to get too euphoric given the recent trend of coal prices. Crucially, BTU also generated around $353m of positive operating cash flow in Q2, buoyed in part by over $109m of working capital timing benefits, but this is expected to reverse in Q3, so that could eventually end up adversely impacting the variable dividend component or the level of buybacks (a pending buyback war chest of $816m as of H1-23).

Closing Thoughts - Valuation and Technical Commentary

Even from the valuation and technical angles, we don't see any overwhelming reasons to get behind Peabody Energy or short it.

As far as valuations go, currently, BTU is neither priced exorbitantly nor cheaply, but if one is prepared to stretch one's horizons and look at conditions a couple of years down the line, we're not convinced there's great value here unless one witnesses a drastic shift in the pricing regime (which of course is not beyond the realm of possibilities when you're dabbling with the mercurial commodity universe).

{kind=link}

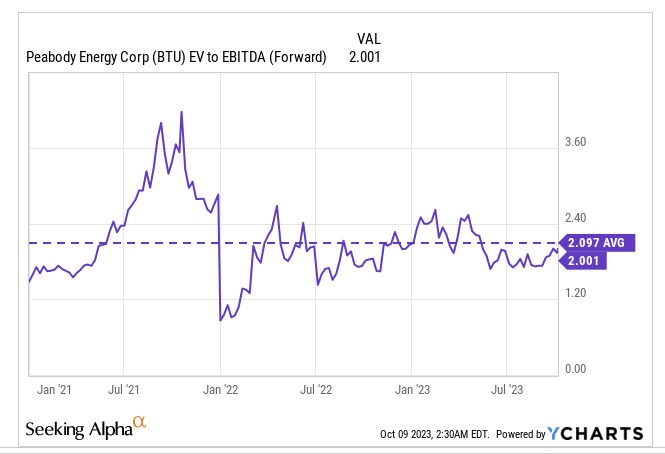

For context, based on the FY23 expected EBITDA, note that BTU is currently priced at roughly 2x EV/EBITDA, which would put it a tad lower than its long-term average of 2.1x.

{kind=link}

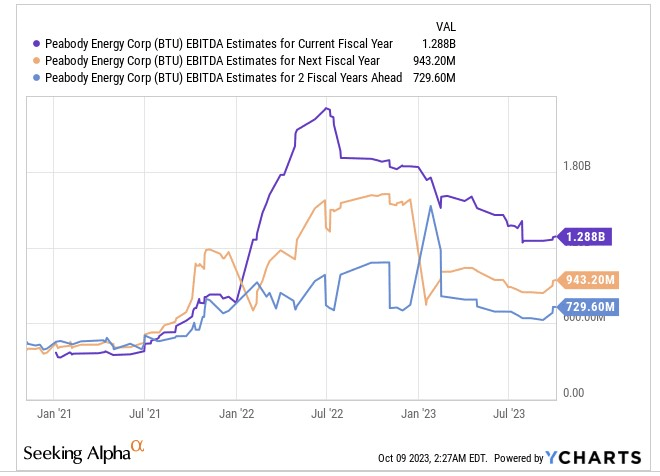

However, sell-side estimates for the following two years (as captured in the image below), look rather drab, implying that group EBITDA could witness a 2-year CAGR decline of over -25% from the FY23 year-end levels. Thus, under normal circumstances, while most companies would showcase cheaper forward valuation multiples for the years ahead, with BTU you're staring at a situation where the EV/EBITDA based on FY25 estimates could be a lot pricier at 3.5x.

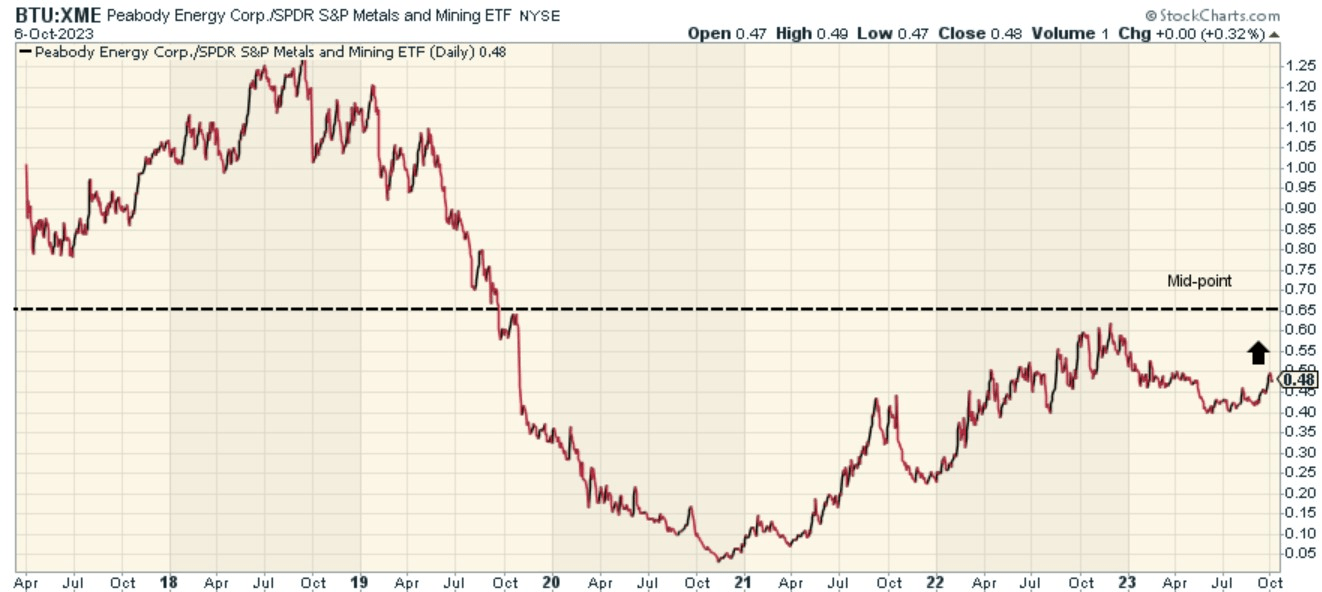

On the relative strength chart, there is still further scope for BTU's relative strength ratio (as a function of other metals and mining stocks) to mean-revert to the mid-point of its long-term range (-26% variance), but that trade is not as attractive as it was during the start of 2022.

{kind=link}

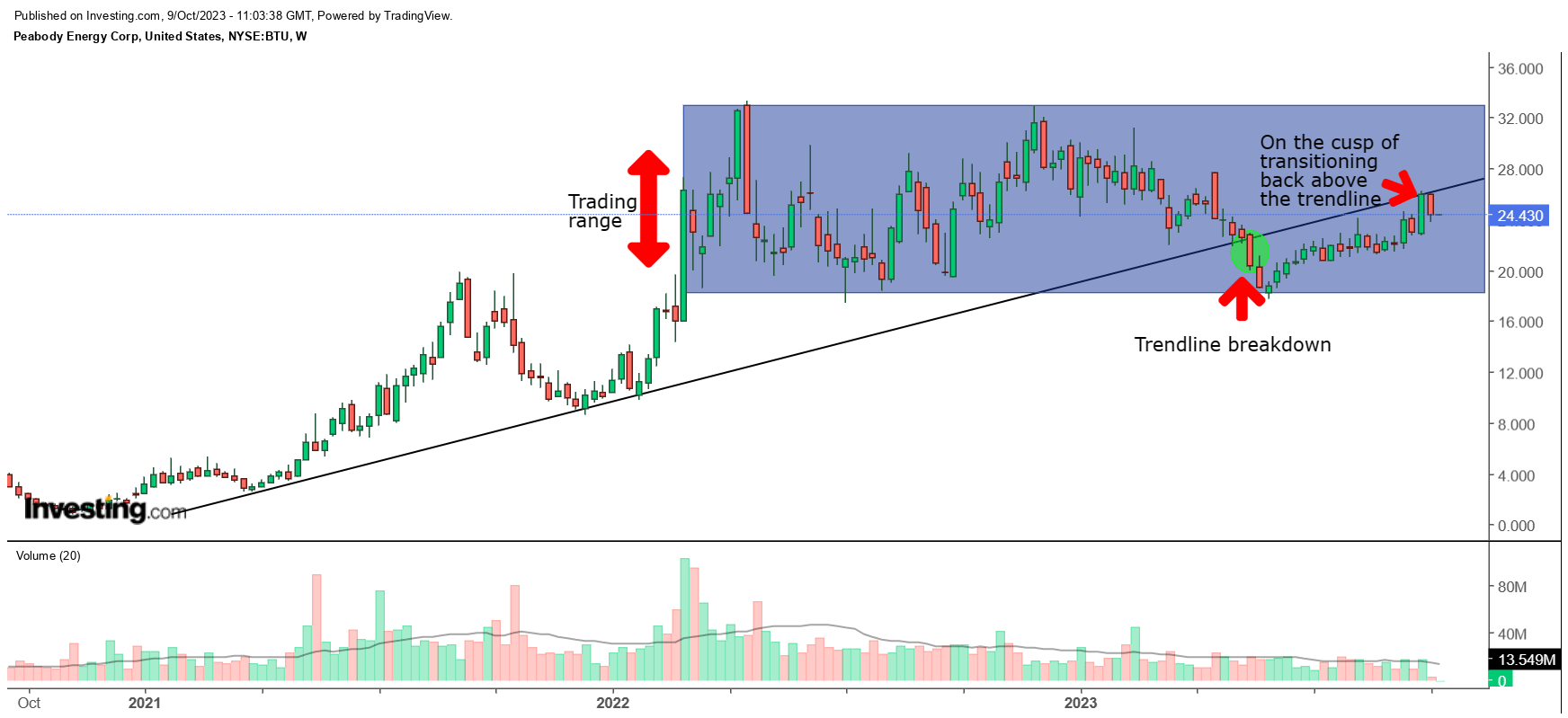

Switching over to Peabody Energy's own standalone price imprints, there are a few important points to note. Firstly, note that in the middle of May, we saw the stock breakdown from its upward-sloping trend line which had been in play since the turn of 2021. The stock then formed a bottom around the $17 level, and has since staged a decent comeback, with the intention of almost recouping the old trend line, which is quite encouraging on the face of it.

{kind=link}

The second thing to note is that the stock appears to have formed an intermediate trading range within the $17-$33 levels, and if one were to stage an entry at current levels, the risk-reward does not look too shabby, considering the respective distances between the resistance and support.

{kind=link}

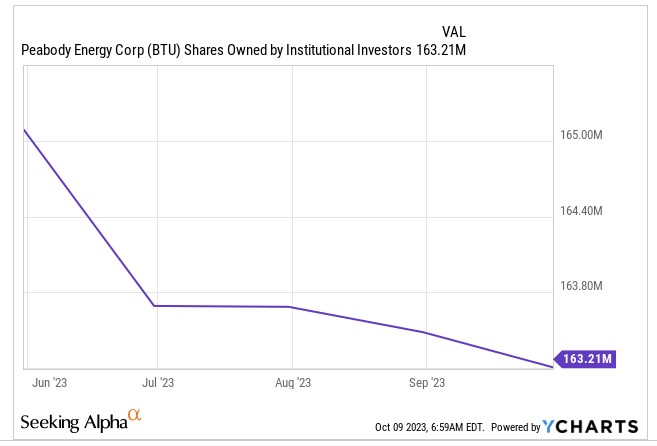

However, investors may also want to consider that the recent rally largely appears to be retail-driven, whereas the smart money continues to unload their stake in BTU even in recent months. Also consider that despite decent bullish momentum since June, there hasn't been any meaningful drop off in the short-interest in the stock, which stands at over 14%.

All things considered; we'd rate BTU as a HOLD.

For further details see:

Peabody Energy - An Assortment Of Good And Bad Sub-Plots