BTU - Peabody: Potential For A 2023 Special Dividend Or Massive Buyback

2023-03-17 16:47:10 ET

Summary

- Peabody Energy Corporation is one of the cheapest coal producers out there.

- One of the reasons for its low valuation is restrictions to buybacks and dividends.

- There is only one restriction left before buybacks and dividends are likely to be resumed.

- When investors can count on a return of capital it de-risks the investment and makes it far more attractive.

Peabody Energy Corporation (BTU) produces metallurgical and thermal coal in the U.S. and Australia. The company has a market cap of $3.37 billion. It sits on a mountain of cash of $1.3 billion (which is exceptional vs its peer group). Its total debt is around $361 million according to Seeking Alpha data. Net income last quarter was $ $632 million or $3.92 per diluted share (the current share price is $22.83). The quarterly cash flow was around $580 million. Cyclicals always look amazing when they're reporting record quarters, but this is next-level in my opinion. Coal prices have been falling lately:

{kind=link}

But they were coming from record highs. At current prices, the company should still be doing quite well. Analyst estimates point to EPS of $6.65 for the full year and $2.58 in the year after that before falling off to $1.09 for 2025.

{kind=link}

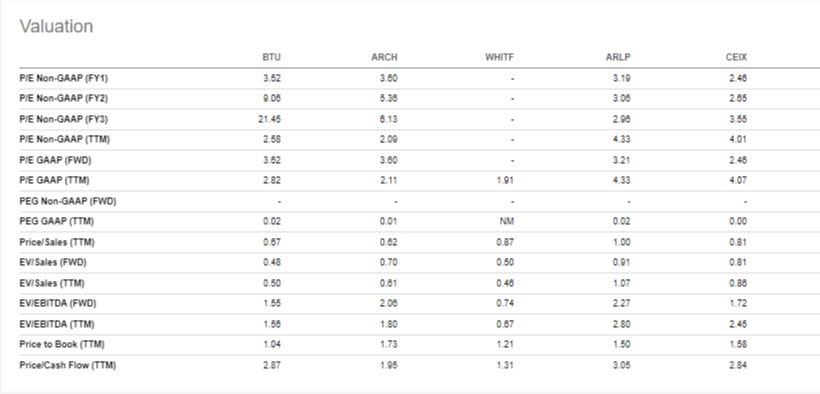

In terms of its valuation, Peabody looks quite attractive vs peers. Its P/E or forward P/E doesn't really stand out. However, it is relatively attractive on the EV/EBITDA metrics, the EV/Sales metrics, the price to book, and price to cash flow valuations.

{kind=link}

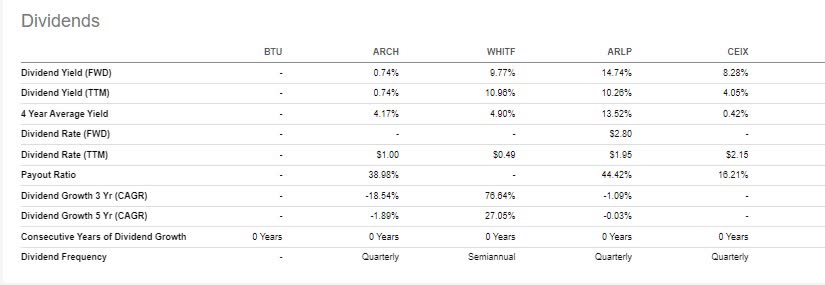

One reason Peabody is likely trading at the lower end of the range vs. its peers is that it is capital-inefficient. The company sits on a hoard of cash because it has some restrictions that prevent it from paying a dividend or buying back shares. The table below shows peers are paying substantial dividends and often combined with massive buyback programs ( like Arch resources ).

{kind=link}

The final thing that's keeping the company from returning capital is finalizing a reclamation surety agreement. In the last call , management said:

Further, we are actively addressing the reclamation surety agreement to arrive at a sensible straightforward path to prefund all final reclamation costs and eliminate the remaining restriction on shareholder returns. We are optimistic this will be completed in the near future.

They gave a little bit of additional color on the call:

Yes. Sure. Lucas, good to be with you this morning. As we mentioned at Investor Day, any shareholder return program that we're looking at is certainly going to be proportional to free cash flow and it's going to be flexible to return cash to shareholders through both buybacks and dividends.

When we look at a broad spectrum of companies with shareholder returns programs, those companies that return the most and utilize both dividends and buybacks have performed best over time. So that's not lost on us.

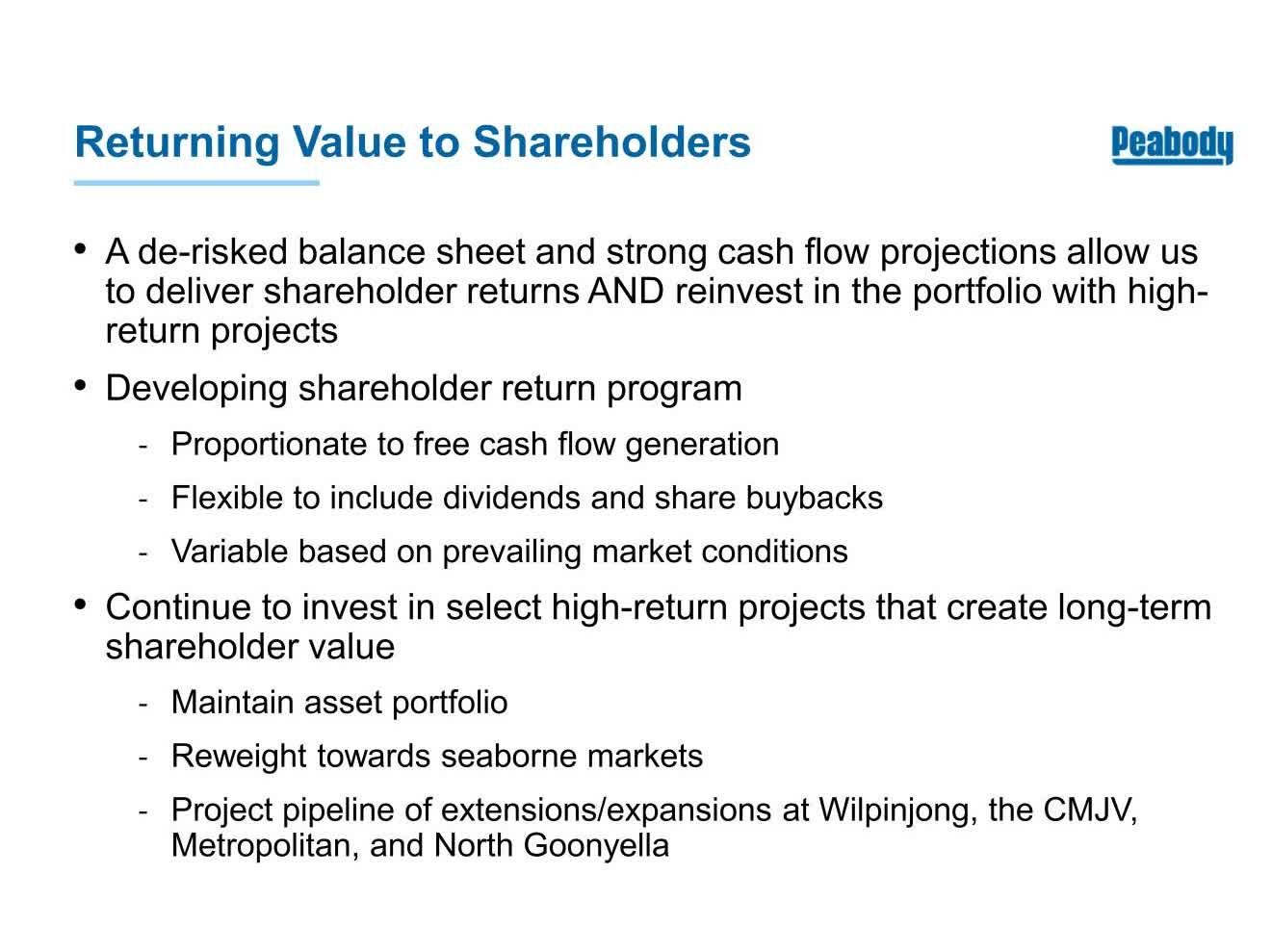

There were also two relevant slides in the latest presentation:

{kind=link}

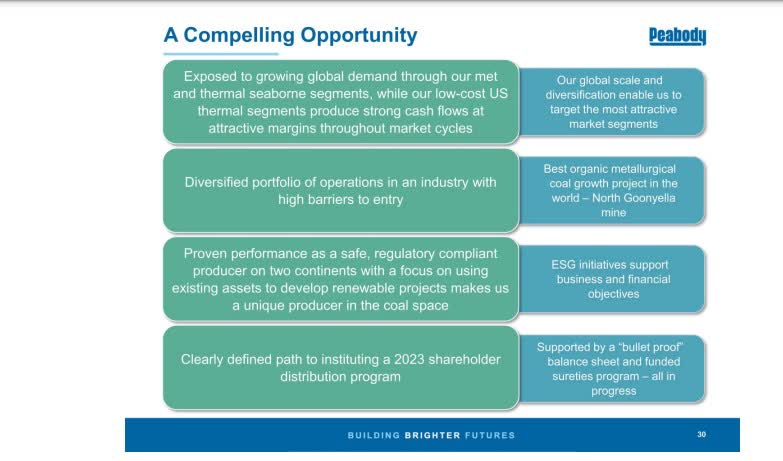

and this one showing the program is supposed to be instituted in 2023:

{kind=link}

I think the company could easily do a $6 per share special dividend or a $1 billion buyback program. It will likely institute a sustainable, dynamic dividend (percentage of free cash flow) and do a $300 million buyback program. Whether it will also do a special dividend is speculative, but it will have the capacity to do so in my opinion. Because coal prices are falling and headlines are suddenly dominated by bank failures (indirectly supposedly bringing on a recession through credit contraction).

I'll assign Peabody a buy, with the caveat it might be better to wait a week or two because of the uncertainty introduced by the bank problems. Coal prices are falling, but only last week Freeport received permission to restart train 1 at its LNG export terminal. This increases gas export which tends to help coal prices. In addition, we're moving into a seasonally more favorable period for gas prices in general.

If we're going straight into a recession, none of the above will likely save this investment. If coal prices continue to go down the investment likely doesn't work in the short term. In the medium to long term, Peabody Energy Corporation should achieve decent prices and produce attractive amounts of free cash flow. Meanwhile, it has a rock-solid balance sheet and isn't bothered by the interest rates being hiked. Perhaps it could deposit $1.3 billion at suddenly attractive rates at a community bank.

For further details see:

Peabody: Potential For A 2023 Special Dividend Or Massive Buyback