BTU - Peabody's Shareholder Return Program Could Boost It Another 10%-30% In Coming Months

2023-04-17 11:28:43 ET

Summary

- Peabody Energy Corporation has announced a massive shareholder return program that includes returning 65% of operating free cash flow to shareholders.

- The company's board has authorized a buyback of up to $1 billion worth of stock.

- Peabody plans to transition to a more balanced shareholder return program of fixed quarterly cash dividends, variable dividends, and share repurchases in the second half of 2023.

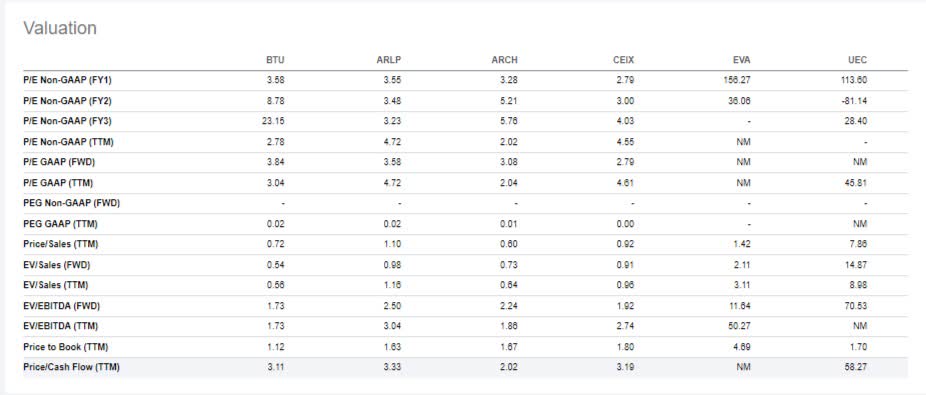

- The company continues to trade at the lower end of the valuation ranges compared to peers, even though it has one of the best balance sheets with a significant amount of cash.

- I expect Peabody Energy Corporation stock to rise by another 10% to 30% over the next few months.

Peabody Energy Corporation ( BTU ) just announced a massive shareholder return program, and it is up only 9% in the pre-market. I think it should go up more in a relatively short time frame. The main reason why is that the shareholder return program is massive. They're about to return 65% of operating free cash flow to shareholders and apply it retroactively to the start of 2023. This company has a market cap of under $4 billion, with the shares trading at $27.57. Its board authorized a buyback of up to $1 billion worth of stock, and cash from operations is about $7.5 per share. In a very rough way, we could see 1/4 of the shares getting taken out.

Here's what I wrote in my last article on Peabody:

I think the company could easily do a $6 per share special dividend or a $1 billion buyback program. It will likely institute a sustainable, dynamic dividend (percentage of free cash flow) and do a $300 million buyback program. Whether it will also do a special dividend is speculative, but it will have the capacity to do so in my opinion. Because coal prices are falling and headlines are suddenly dominated by bank failures (indirectly supposedly bringing on a recession through credit contraction).

Here's what the announcement says:

Peabody anticipates the shareholder return program will include a regular quarterly cash dividend of $0.075 per share. First half 2023 returns are expected to include the regular quarterly cash dividend with the remaining 65 percent of AFCF to be returned to shareholders exclusively through share repurchases. Peabody plans to transition to a more balanced shareholder return program of fixed quarterly cash dividends, variable dividends and share repurchases in the second half of 2023. All shareholder returns remain at the Board's discretion.

The regular cash dividend is tiny, and at first, Peabody is mainly hitting the buyback hard. After that (likely when it believes the shares are less undervalued) it is going to weigh more towards a balanced capital return program with higher but variable dividends.

It is implementing this plan after the next earnings. That's likely in early May. To top it all off, it isn't wasting the other 35%:

The balance of AFCF is expected to be allocated to value enhancing growth projects, repurchase of potentially dilutive securities, additional shareholder returns and capital preservation.

Coal producers are currently rightfully very selective about growth projects. As long as the company spends small amounts on selective, highly accretive projects (even at lower prices), I think this may not be so terrible. But under destinations to allocate the balance, the company again mentions shareholder returns and the repurchase of potentially dilutive securities.

The company continues to trade at the lower end of the valuation ranges compared to peers:

{kind=link}

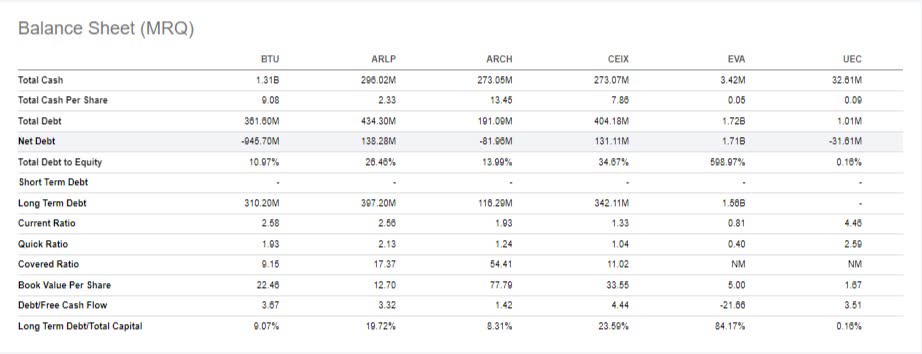

This is especially noteworthy given it has one of the best balance sheets with a humungous amount of cash ($1.3 billion). It could theoretically go to work in early May and be finished up with buybacks by mid-May.

{kind=link}

Peabody Energy Corporation stock is up around 9% in the pre-market, but I think it will quickly add another 10%-30% over the next few months given it is now returning capital as aggressively as some of the other coal stocks. I'm obviously not the only one who expected Peabody to take this route. They signaled their intent clearly. However, the sector is so out of favor that I believe a real structural bidder (i.e., Peabody itself) is likely to have quite an impact on the share price.

For further details see:

Peabody's Shareholder Return Program Could Boost It Another 10%-30% In Coming Months