SRVR - Peak Bear Has Arrived In Real Estate

2023-06-29 06:04:48 ET

Summary

- Allow me to utilize 2 overused quotes:

- Buy when there is blood in the streets.

- Be greedy when others are fearful.

REIT bearishness has spread maximally and has resulted in a tremendous discount in REITs vs. the S&P. REITs are now trading at anywhere from 50% to 65% of the 2023 earnings multiple of the S&P. Historically, REITs have traded at a slight premium FFO multiple to the S&P earnings multiple. The magnitude of bearishness priced into REITs has reached an extreme level and I believe it has peaked. From the peak bear state, there is significant upside ahead.

Forward fundamental performance for REITs appears to be about the same as that for the S&P, but the extreme discount at which REITs trade sets them up for outperformance. This thesis contains 5 parts

- The spread of bear sentiment

- Fundamental data contrasting bear sentiment

- The mechanism by which sentiment impacts market prices

- Attenuation of bear sentiment

- Relative Value

The spread of bear sentiment

Most sentiment is based on some sort of real data. I like to think of sentiment as the product of fundamental impact of data and the dissemination of that data.

Consider a piece of hypothetical data that hurts REITs. The actual amount of damage is X, but the amount of impact on market prices is amplified by how broadly spread that information becomes.

If the information is known by relatively few market participants, market prices will likely drop by less than X, whereas if the negative data is broadly disseminated, the impact on market prices will be amplified.

The same goes for positive data. The positive data will impact market prices by the product of X and Y where X is the fundamental impact and Y is some measure of how well disseminated the data becomes.

I posit that right now the “Y” for negative REIT data is huge and the “Y” for positive REIT data is small. Essentially, negative REIT data has taken off like wildfire in financial media, whereas the equally significant positive data is never mentioned outside of dedicated REIT analysts.

So what is the negative data that we are referencing?

- Rising interest rates (interest expense cost)

- Increased office vacancy

This information is ubiquitous, almost to a fallacious extent. It feels like a game of telephone where the further out you get from the original source of information the wilder the claims become. It starts with something factual like:

“higher interest rates are increasing interest expense for REITs”

Then as the information gets passed around it becomes:

“REITs are struggling to pay interest on their massive debt”

It has become a topic that gets a lot of attention and because it gets attention the news outlets want to cover it. Afterall, they get paid by number of viewers so the news starts to match public sentiment rather than the other way around. This is the June 26 th cover of Bloomberg’s Business Week:

Bloomberg

Beyond the not-so-subtle parody of a famous scene from horror movie “The Shining”, the magazine featured headlines like this.

{kind=link}

I think it is fair to say that information about office vacancy and interest rates is about as disseminated as information can possibly get.

As saddened as I am to see an otherwise reputable publication like Bloomberg go the sensationalism route, I think it is a huge bullish indicator for REITs. Bear sentiment has jumped the shark and we have reached peak bear.

In mathematical terms, bear sentiment has a maximal amplification factor presently.

There is an equal or greater amount of positive REIT data, it just doesn’t get the coverage.

- Rental rates are up

- Same store NOI is up

- FFO/share is up

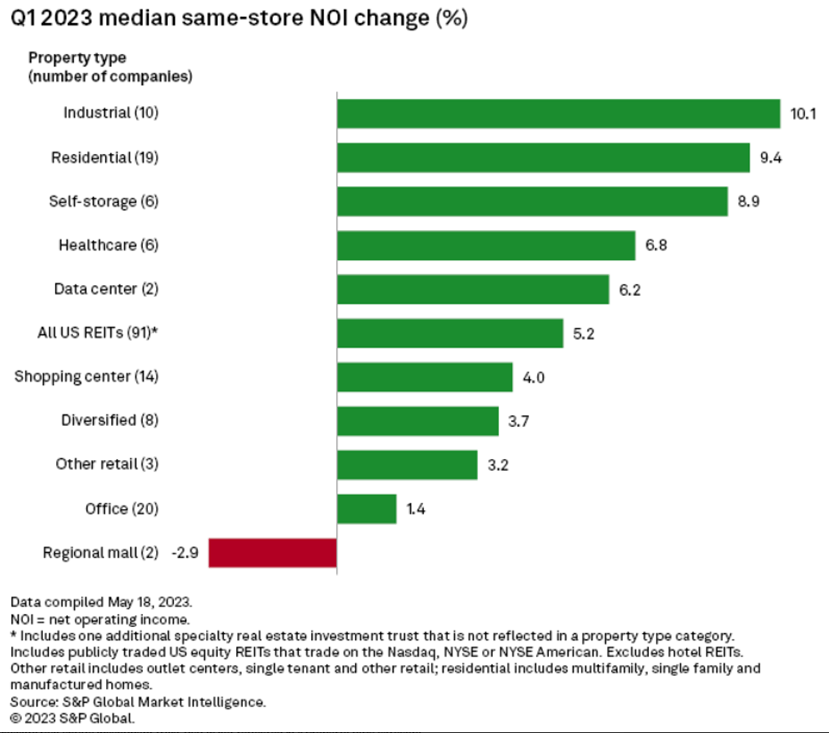

Lost in all the fear about interest rates is that the Fed’s action is driven by high inflation. Well, real estate is an inflation hedge because rents go up in inflationary environments. In fact, rents have risen significantly more than costs such that same store NOI for REITs as a whole was up 5.2% in the most recent quarter.

{kind=link}

This gain in net operating income is greater in magnitude than the increased interest expense such that the FFO/share of REITs has gone up. REIT cash flows are expected to continue to rise in 2024 based on analyst consensus.

This positive information is not blind to the bad news. It includes the bad news and it is just that the positive fundamental changes are of slightly greater magnitude such that the net is positive.

It just so happens that the good news gets no coverage in most financial media so sentiment is dominated by the negative.

How negative sentiment hurts prices

Generally, the more informed one is with regard to a subject, the less they will be influenced by the media prevalence of data.

A REIT expert is going to be aware of both the positive and negative data regardless of how widely publicized. For the most part, those who invest in REITs are among the more informed about REITs so how does the disinformation actually affect market prices?

In brief, through fund flows.

With a generally bearish public, professional asset managers have trouble raising capital for REIT investment vehicles.

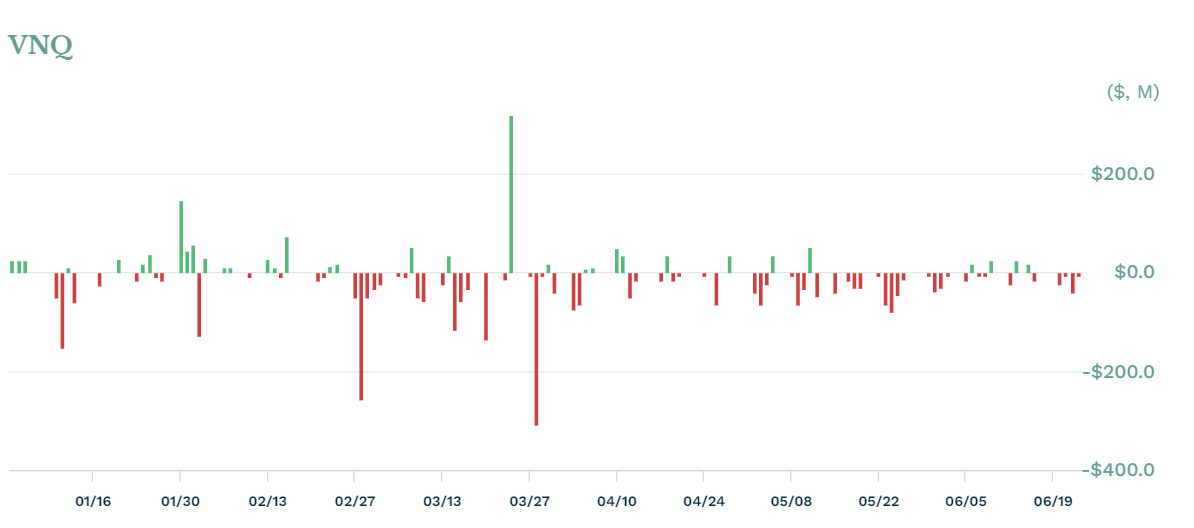

With a generally bearish public, REIT ETFs experience outflows. The Vanguard Real Estate ETF ( VNQ ) has had net outflows of $1.6B in 2023 as of 6/26/23.

{kind=link}

As money flows out of REITs, the market prices drop. I think these fund flows are about to reverse.

Attenuation of bear sentiment

Once information reaches a point of ubiquity it loses incremental impact. Anyone who would be scared off by headlines about office vacancy has already been scared off. The low conviction REIT owners are already out of the market. Those who remain are already aware of the negatives.

It is a strong base from which to build.

More importantly, it is a base that is backed up by fundamentals. Office is only 7% of REITs with the majority of the other sectors being in great shape. REITs are overwhelmingly raising their dividends. The yield disparity between REITs and the S&P has increased with REITs now yielding 4.22% compared to 1.57% for the S&P.

At some point fundamental analysts are going to notice the extreme valuation gap and get interested. Both REITs and the S&P are expected to grow earnings (FFO for REITs) in the mid single digits. That estimate could change if there is a significant recession, but it would change in about the same magnitude for each. The valuation gap has gotten too extreme to ignore.

Most attractive relative value for REITs in decades

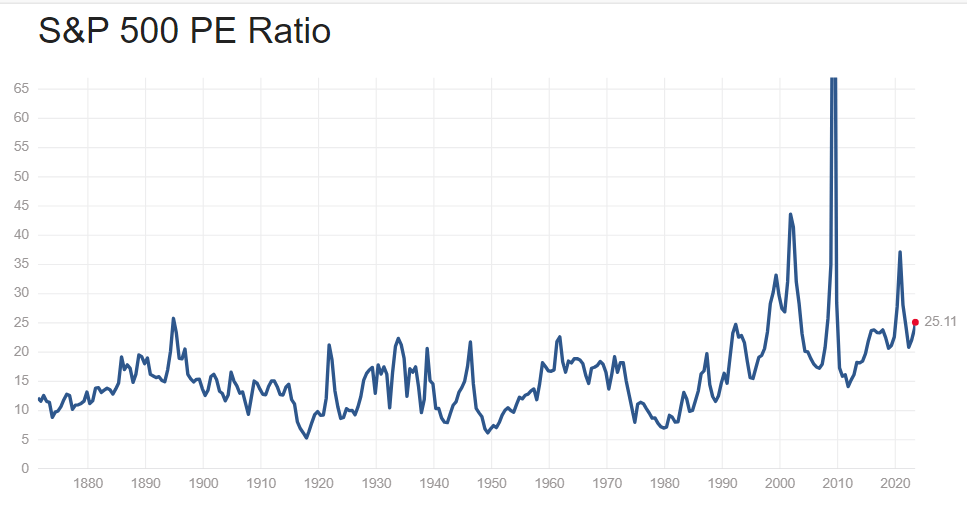

On a trailing basis, the S&P has hit 25X which is rarely seen outside of times when earnings collapse (2000, 2008, and 2020) which causes the multiple to shoot up.

{kind=link}

If one prefers to look at forward earnings, Morgan Stanley just came out with its 2023 S&P earnings forecast of $185. They are on the more bearish side at the moment with the other street estimates coming in a bit higher. With the S&P at 4338, its forward multiples are as follows depending on one’s earnings forecast.

| Forward earnings |

| Multiple |

| $230 |

| 18.9X |

| $220 |

| 19.7X |

| $210 |

| 20.7X |

| $200 |

| 21.7X |

| $190 |

| 22.8X |

| $180 |

| 24.1X |

In contrast, the REIT median multiple on 2023 FFO is 12.2X.

FFO and EPS are not the same metric but they are comparable and historically REITs have traded at a slightly higher FFO multiple than the S&P has on earnings. This sort of discounting is a recent thing related to the extreme bearish sentiment.

REITs can now be bought at multiples about 50%-65% the multiples of the S&P depending on which S&P estimate one looks at.

That is very attractive relative value given the similar growth rates.

Putting it together

There are legitimate risks in REITs as there are with any other sector, but the risks have been over generalized (7% office exposure treated as major component) and exaggerated (treating individual property givebacks to banks as the equivalent of bankruptcy).

Overall, REIT fundamentals look healthy and the peak bear market has provided an excellent opportunity to get in at a great valuation.

For further details see:

Peak Bear Has Arrived In Real Estate