ONL - Peakstone Realty: Steer Clear Of This Single-Tenant Net Lease Office REIT

2023-06-27 08:35:33 ET

Summary

- Peakstone Realty Trust's heavy exposure to single-tenant office properties makes it a risky investment due to the potential costs of converting these spaces for multi-tenant use.

- PKST stock appears overvalued, with potential downside ranging from 27% to 67% depending on the assumed net asset value.

- The uncertain future demand for office space in a hybrid work environment and lack of positive catalysts for PKST make it an unattractive investment option.

Peakstone Realty Trust ( PKST ) is a net lease real estate investment trust ("REIT") that owns single-tenant industrial and office properties across the United States. Its 18.7 million square foot portfolio is 96% leased and made up of relatively new buildings with an average age of 13 years.

Right off the bat, learning that PKST's largest property type is office repels me from the stock. As Aaron Halfacre, CEO of fellow net lease REIT newcomer Modiv Inc. ( MDV ), put it to me recently while explaining why he does not like single-tenant office properties, "Single-tenant office eventually becomes multi-tenant office."

In other words, if and when the tenant of a single-tenant office building decides not to renew their lease and moves out, the landlord typically has to perform expensive modifications to the building to turn a space designed for a single users into a segmented space for multiple users. And in the process, the property ceases to be a net lease asset, in which the tenant is obligated to pay for building maintenance, taxes, and insurance. In multi-tenant office buildings, the landlord is typically responsible for those items as well as common area maintenance, exposing them to inflationary operating cost increases.

It's a very different kind of investment than a simple, single-tenant net lease in which the landlord basically just collects a monthly check with little to no property-level obligations.

That said, at a 3.0% dividend yield and very low payout ratio of around 37%, PKST is retaining a lot of cash, which should help the REIT deleverage and protect it from potential downsides from office tenant turnover.

All in all, for REIT investors, PKST is an unappealing investment option in almost every way and likely has significant downside to fair value. Let's explore why.

Peakstone's Primary Shareholder Base

Let's back up a minute and address how PKST came into being. The company that became the current PKST formed from the merger of several private, non-traded REITs and real estate funds.

Rather than DIY retail investors, these sorts of private real estate funds are often trafficked by third party investment brokers who put their (typically high net worth or ultra-high net worth) clients into a number of funds and investment products. Many of these clients don't delve deeply into the monthly or quarterly statements, instead just checking to make sure the balance isn't going down and that the regular checks they expect to receive are still coming in.

Often, a HNW client will tell their broker that they want income, so the broker will find high-yielding funds (that also usually feature high commissions) to put them in. (Of course, RIAs who face penalties for failure to act in their clients' best interest would probably have gone for the no-load, no-commission share classes. In case there are any of those folks reading this, I'm not maligning you.)

I suspect that for many investors in the original Griffin Realty Trust, Griffin Capital Essential Asset REIT, and Cole Capital funds, being in a private fund was something of a comfort because it hid the market value losses of these office portfolios over the last few years. And then there was a 1-for-9 reverse stock split prior to the public listing, so some shareholders may be confused about exactly how much value has been lost in their investments.

I believe this explains why PKST's stock price has done relatively well since its April 2023 IPO.

Much of its legacy shareholder base (which makes up the vast majority of shareholders) may not have noticed, at least initially, that they are now in PKST instead of the private funds that preceded PKST.

Others may be well aware of the situation but unable to sell because of technical difficulties and the need to transfer their shares into a form or account where it is possible to sell.

Interestingly, the first two spikes in volume since the initial public listing were both from surges in buy orders, which I wouldn't have assumed given PKST's primarily office portfolio.

But the most recent spike in volume has been on a wave of selling, which I think could signal the beginning of a longer selloff. After all, some of those HNW shareholders may have perused their Q1 2023 statements to find themselves now in the low-yielding PKST instead of the former high-yielding private funds and instructed their broker to sell.

Or perhaps the brokers themselves may now be selling on behalf of their clients in order to redirect the funds somewhere more lucrative (both for their clients and themselves).

Or perhaps the private fund shareholders have just recently figured out how to actually sell their shares.

In any case, as it becomes clear that the market value of PKST's portfolio is nowhere near its original cost basis and legacy shareholders attain the ability to sell, I would expect PKST's stock price to continue its downward trajectory.

Peakstone's Portfolio

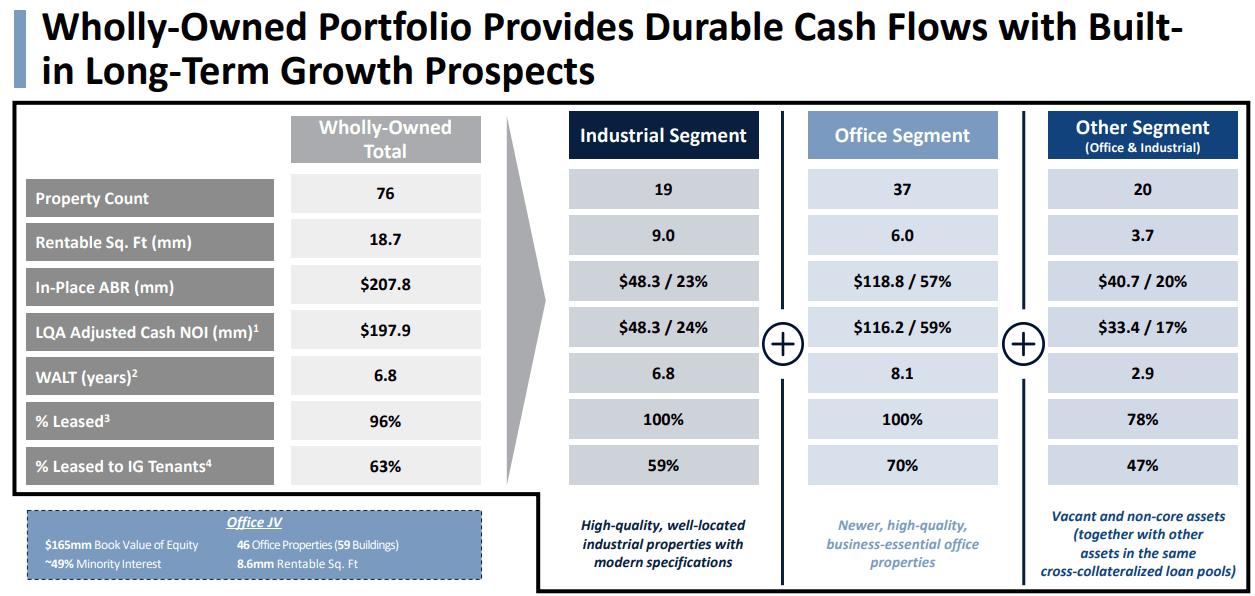

PKST owns 37 office properties accounting for 57% of rent, 19 industrial properties accounting for 23% of rent, and 20 non-core office and industrial properties that make up the remaining 20% of rent. This "other" segment is split 83%/17% office and industrial, respectively.

{kind=link}

PKST June Presentation

Thus, about 75% of PKST's rent derives from office properties.

Additionally, as you can see in small letters in the bottom left hand box in the image above, PKST owns a 49% interest in a joint venture that owns office properties. The REIT recently sold that slight majority interest in these office properties in order to reduce its total office exposure, pay down debt, and reduce future capex requirements.

Notice a few points about the office segment.

First, 100% of PKST's offices are leased, and 70% of them are leased to investment grade-rated tenants.

Second, the office segment has a relatively long weighted average remaining lease term of about 8 years. Although it could be the case that management has separated out most of the office properties with shorter remaining lease terms or non-IG tenants into the "other" segment in order to make the "office" segment look stronger.

Third, not shown above is the point that 40% of office rent is from corporate headquarters, and 35% is generated from properties with a research, laboratory, or data center function.

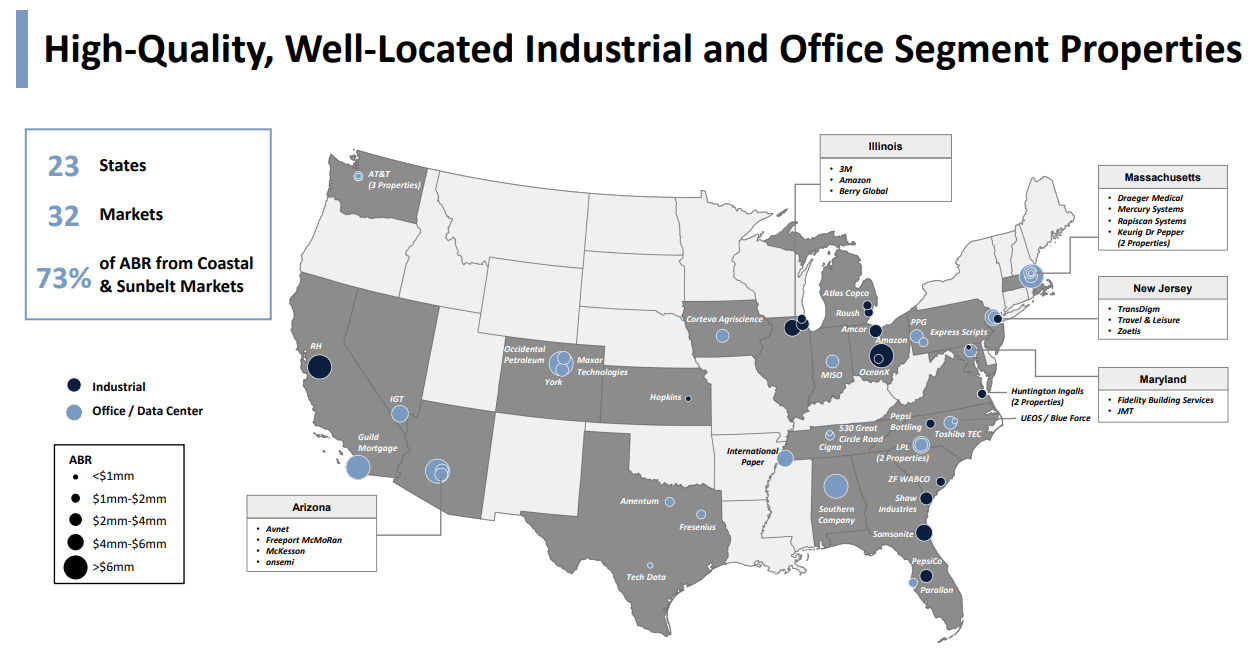

Geographically, there is no particular focus for PKST's portfolio, but seeing the particular tenants at PKST's properties does give a sense of their credit quality. There are lots of recognizable names across the board, including Keurig Dr. Pepper, PepsiCo, Southern Company, McKesson, and International Paper.

{kind=link}

PKST June Presentation

Going forward, PKST says that its future focus will be on acquiring warehouse/distribution properties while continuing to own many of its single-tenant office properties.

In addition, PKST aims to achieve an investment grade credit rating of its own.

But to my mind, neither of these two goals seem likely to be achieved any time soon. The heavy office exposure is likely to weigh down the stock price, which in a high interest rate environment will make all forms of capital expensive.

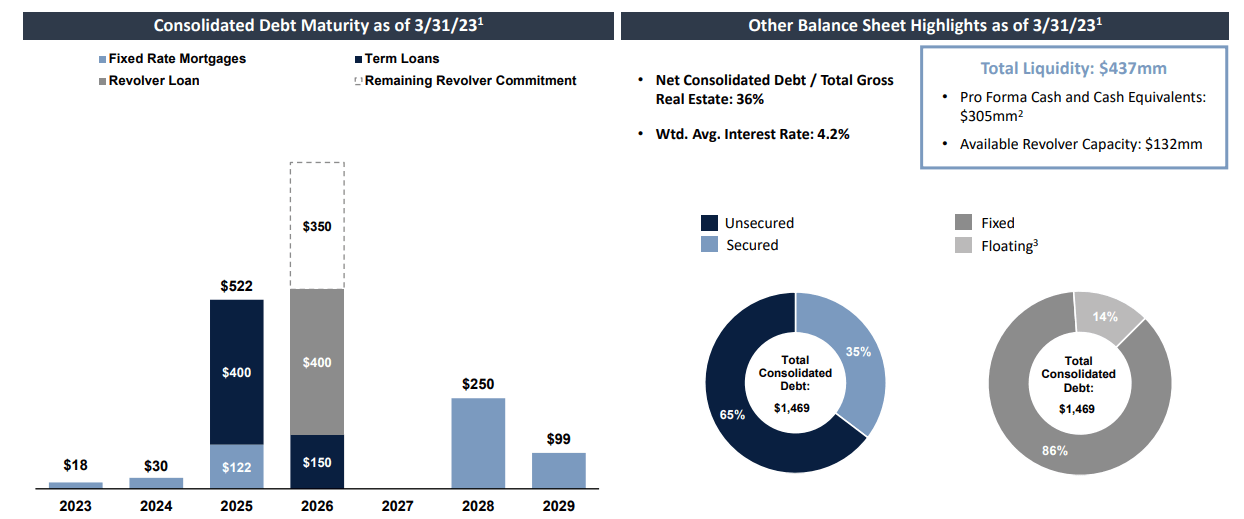

Moreover, even after some property sales and the 51% JV sale of the 46-property office portfolio, PKST still ended Q1 2023 with relatively high leverage at a net debt + preferred to EBITDA ratio of 7.5x (or 7.4x adjusting for a recent asset sale).

Fortunately for PKST, very little debt comes due (without optional extensions) until 2025.

{kind=link}

PKST June Presentation

But unfortunately, 14% of total consolidated debt is floating rate, which has been a headwind as the Fed has raised rates this year.

It appears that capital recycling will be PKST's primary source of funds for acquisitions, but that means that the REIT will be selling relatively high cap rate office properties and exchanging them for lower cap rate industrial ones, which will make accretive, per-share FFO growth very difficult.

Dilutive capital recycling + lingering high leverage + heavy office exposure will likely result in stagnant or declining FFO per share going forward. That setup does not strike me as the kind of balance sheet or portfolio that will likely earn an investment grade credit rating anytime soon.

Valuation: Watch Out Below

In his April article on PKST, Dane Bowler gave a quick and dirty estimate of PKST's net asset value per share of around $11.11. But he acknowledges this is just a back-of-the-envelope estimate, so it might be fair to say Bowler's view of NAV per share is somewhere in the neighborhood of $10-12.

That would give PKST's current ~$30 stock price about 60-67% downside to true NAV.

I assume those figures are too pessimistic, especially the 11% cap rate valuation for the office segment.

If NAV is $15, then PKST still has 50% downside.

If NAV is more like $20, then PKST has about 33% downside.

Then again, when I do the same calculation as Bowler (with slightly adjusted cap rate assumptions), I end up with a very different NAV per share that makes me question my math.

| Q1 Annualized NOI |

| Assumed Cap Rate |

| Valuation |

| Office |

| $116m |

| 9% |

| $1.29B |

| Industrial |

| $48m |

| 6% |

| $800m |

| Other |

| $33m |

| 12% |

| $275m |

| Total Asset Value |

| $2.364B |

| Cash |

| $307m |

| Office JV Book Value + Other Assets |

| $244m |

| Consolidated Debt + Other Liabilities |

| $1.551B |

| Net Asset Value |

| $1.364B |

| Shares Outstanding + Unvested Restricted Shares |

| 36.199m |

| NAV Per Share |

| $37.68 |

I am dubious of my own math here. Where I'm most uncertain is the weighted average share count, which the 10-Q lists as ~36 million. I included ~199,000 unvested restricted shares, but I believe there is another share class that I may not be considering in this calculation of shares outstanding.

So let's view it from a different angle. PKST is currently valued at about a 12.5x FFO multiple based on the analyst consensus estimate of 2023 FFO.

Compare that to pure-play single-tenant net lease office REIT Orion Office REIT ( ONL ), which currently sports a 4.1x FFO multiple.

There's also Office Properties Income Trust ( OPI ), which is another single-tenant net lease office REIT, which is valued even lower at a 1.9x FFO multiple. But OPI is externally managed by The RMR Group ( RMR ), which has a very poor track record of shareholder returns for their managed REITs, so it is not as good a comparison as ONL, which is internally managed.

Finally, remember that about 25% of PKST's rent comes from industrial properties, so let's look at a pure-play single-tenant net lease industrial REIT for comparison's sake. STAG Industrial ( STAG ), for example, sports a 15.5x FFO multiple.

If we assume STAG's FFO multiple is a good estimate for PKST's industrial assets and ONL's FFO multiple is a good estimate for its office assets, then we end up with a weighted average fair value FFO multiple of right around 7x.

That fair value estimate would give PKST downside of about 45% to a FV share price of $16.50.

Or, if we assume ONL is oversold and that its long-term fair value is closer to 7x, then PKST's fair value FFO multiple would rise to 9.1x, implying only 27% downside to a FV share price of around $22.

The bottom line here is that, however I look at it, PKST looks overvalued, and not by a small amount.

Bottom Line

I don't really want to own office real estate at all right now, even if it is deeply discounted. That is because the new hybrid work environment is making it extremely difficult to predict future demand for office space.

Single-tenant offices are especially risky, because the risk is more binary than for buildings that are already set up to accommodate multiple tenants. If and when the tenant vacates the building, the landlord either has to pay enormously high tenant improvement and leasing commission costs to get another tenant into the building, probably also taking a haircut on the rent (and waiting however long it takes to find a replacement tenant), or invest a large sum of money to reposition the building into a multi-tenant property so that there can be at least some revenue flowing in while the rest of available space is being marketed for lease.

In any case, I see no positive catalysts for PKST and plenty of downside risks. I am steering clear of this REIT and would sell my shares if I owned any.

For further details see:

Peakstone Realty: Steer Clear Of This Single-Tenant Net Lease Office REIT