PTON - Peloton Remains A Very Risky Stock

Summary

- Peloton expects flat revenues for FY23 and break-even cash flow. The path to long-term profitability is not very clear at the moment and Peloton's balance sheet doesn't give much leeway.

- If the sale of its manufacturing facilities materializes in the next four months, Peloton will receive a much-needed cash injection.

- Our updated DCF model includes a 30% chance of Peloton not surviving and estimates a fair value at $9 per share, suggesting 30% downside to the current share price.

Since our previous article on Peloton (PTON) the shares have lost over 73% of their value, compared to almost 12% lost by S&P 500 in the same time frame.

John Foley, the company's founder and long-time CEO, was replaced by Barry McCarthy in February 2022, who came out of retirement after a career at Netflix (NFLX) and Spotify (SPOT) and whose job was to turn Peloton around.

During McCarthy's time in the office Peloton has reversed many its initiatives from prior years. During the COVID-19 pandemic the company experienced a huge surge in demand for its products, however, it suffered higher costs from supply chain issues. To mitigate that, Peloton's management (still Foley at that time) decided to invest in its own manufacturing facilities by buying gym equipment manufacturer Precor and building its own factories in Taiwan and Ohio. Fast forward one year later and Peloton's management made a decision to outsource its equipment production. Now Peloton is on the market trying to sell their manufacturing facilities at the right price.

The new CEO also initiated several rounds of layoffs in an effort to cut costs, with the last being announced in October 2022. Peloton's workforce was reduced from 6,700 in June 2021 to around 3,800 after the cuts. During its latest earnings call McCarthy promised that the October round was the last and there won't be more coming.

During McCarthy's tenure Peloton has opened new avenues for customers to acquire its products including through Amazon, Dick's or renting the equipment. The latter is part of the strategy "Fitness as a Service" - FaaS. During its latest earnings call the company disclosed that there were about 28,000 FaaS customers. While it's not even 1% of Peloton's customer base, company's management is quite optimistic about the new customer segment, as it allows the company to expand its TAM. This segment is also less profitable, as the customers are not paying for the equipment upfront and produce higher churn rates of about 4%. However, Peloton's management is confident that the company still generates 1.4x in LTV compared to CAC.

Peloton's Financial Performance

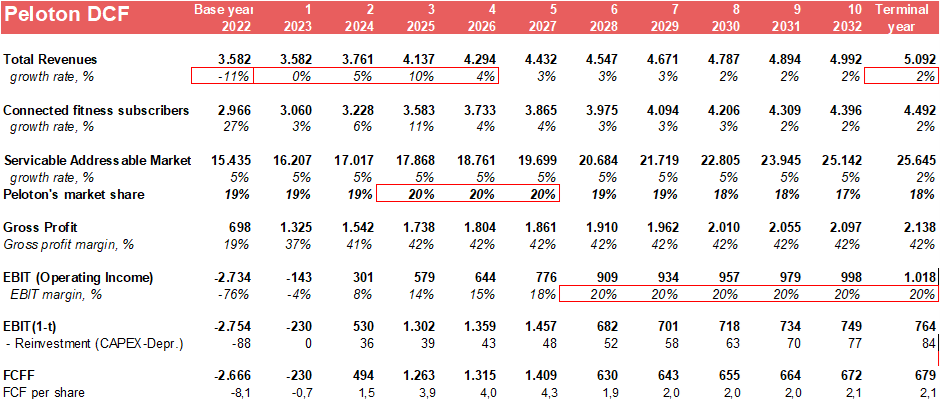

Peloton stopped publishing growth charts in its quarterly earnings, as there's no growth to show. The company's revenues have declined 11% to $3.6bn in FY22 and are expected to remain flat in FY23 ending at the end of June. Analysts' expectations are even lower at $2.75bn in revenues in FY23.

Peloton's new CEO used 2022 as a blood bath and the company filed $2.8bn in net loss in FY22 ($8.15 loss per share), out of which over a billion were restructuring, impairment and settlement charges, which are not expected to repeat in FY23. However, even excluding those, Peloton has spent $2bn on SG&A and marketing expenses in FY22, while earning only $700m in gross profit. Therefore, the company urgently needs to achieve cost savings in its operating expenses and in the best case to cut them by half to $1bn per year. McCarthy is aware of that and plans to address these issues next. However, the company has not published any guidance on the target cost savings rate.

Seeking Alpha

In January 2023 Peloton hired Leslie Berland, former Twitter executive, as Chief Marketing Officer (CMO). Berland will oversee over $1bn in annual marketing budget and will hopefully use marketing dollars sparingly.

Peloton is currently not expected to deliver positive earnings per share for the years to come, which is a critical issue if you look at Peloton's balance sheet.

Peloton's Balance Sheet Looks Terrible

Since the beginning of 2022 Peloton has written off about $500m in intangible assets, PP&A and goodwill. Another $300m were written off in inventories. These impairments, coupled with operating losses, virtually wiped out Peloton's equity, which in Dec 2022 stood at meagre $30.5m . As the company is burning through about $300m in cash per quarter, Peloton urgently needs to either raise additional equity or sell their assets at a premium to its book value thus realising a book gain. During its latest conference call, Peloton's management confirmed its plans to sell their Ohio factory by the end of June. However, in our opinion, Peloton needs equity right now.

Peloton already had to go to the market to raise equity under less than ideal circumstances in November 2021. At that time the company had to sell equity at $46, a discount to the market price at that time. At the current market price level, Peloton would have to seriously dilute its existing shareholders to raise any meaningful amount in equity.

In terms of cash, the company still had $871m at the end of Dec 2022, which could suffice for a couple of quarters at the current burn rate. Again, the sale of manufacturing facilities could provide the necessary injection, however, Peloton should find a way to mitigate its cash burn. Otherwise the company will run out of tricks to keep itself afloat.

Peloton's DCF Valuation Update

Revenues: We expect Peloton to deliver single-digit growth going forward as the company needs to perform a balancing act between its marketing spend and growth. We kept the terminal growth rate at 2% and expect the company to reach $5bn in sales in ten years' time.

Gross Profit margin: As the company increases the number of its subscribers, we expect Peloton to be able to achieve 42% gross profit margin.

EBIT margin: Our basic assumption is that the company manages to cut its operating expenses and limit them to $1bn p.a. going forward. In this case 20% EBIT margin should be attainable. In comparison, Planet Fitness ( PLNT ) consistently delivers 27% operating margin. This assumption is also not too ambitious compared to the industry averages. However, Peloton still has to prove that it's able to achieve profitability.

{kind=link}

WACC: We increase our WACC to 9.4% in line with increased risk-free rate of 3.77% , equity-risk premium of 4.89% and PTON's beta of 1.96x.

Probability of Failure: We have added a 30% probability of failure to Peloton's valuation. In this case the proceeds would amount only to 50% of company's book value of equity and debt or $1.2bn.

Author

Target Price: As a result, our DCF suggests a target fair value of PTON shares at $9, or 30% downside to the current share price. Without the discount for the insolvency risk, PTON's estimated fair share value would be around $16/share.

Relative Valuation: PTON is still trading at $5bn market cap or 1.4x P/Sales. If you take analysts' estimates for FY23, then the company is trading even at 1.8x P/Sales. This by no means is cheap for a company with a massive quarterly cash burn, which is on the brink of insolvency.

Conclusion

As Peloton is struggling for its existence, PTON remains a very risky stock for investors. The next couple of quarters will prove to be critical for the company. Peloton will either find a way for a break-even growth or will run out of cash and equity and will essentially be up for sale. As the estimated fair value oscillates between $9 and $16/share, a risky investor might attempt at taking a stance.

For further details see:

Peloton Remains A Very Risky Stock