NLS - Peloton: The Problem Is The Product

Summary

- Peloton is a company that has been criticized heavily for its solvency issues.

- With a debt/equity ratio of 9.3, those criticisms have certainly been merited.

- However, its real problem is that it launched a product that only made sense in the context of COVID-19 lockdowns.

- The pandemic resulted in gyms shutting down, leading many people to buy home gym equipment.

- Today that catalyst is no longer there and Peloton is having to cut prices in order to move its goods.

Peloton (PTON) was among the worst performing tech stocks of 2022. Down 95% year-to-date, it has taken a severe beating. The main issue with the stock is that it over-earned during the early months of the COVID-19 pandemic. When COVID-19 came to North America, many businesses were forced to shut down. Gyms were among the businesses hardest hit, with one in five closing permanently by the end of the year.

The closure of gyms was a big catalyst for gym equipment manufacturers like Peloton. Just like the closure of retail stores led to a surge in e-commerce sales, the closure of gyms led to a surge in home gym equipment ownership. At the height of the pandemic, Peloton saw its sales surge 172% .

That was then, this is now. In 2021, U.S. states started rolling back COVID-19 restrictions. By 2022, people reported that their lives had returned to normal . Naturally, gyms started operating at usual capacity, and demand for home gym equipment diminished. As a result, Peloton's sales declined: in the most recent quarter, revenue was down 23%.

Peloton earnings (Peloton)

For many people, the fact that Peloton's revenue is declining is enough to write the stock off. Nobody wants to invest in a shrinking enterprise. However, it's possible that the revenue decline is already priced in. Certainly, the negative free cash flow shown in the table above gives pause, but in itself does not make a company worthless. The loss got smaller compared to fiscal Q4, perhaps if the trend continues on this path, the company will be able to execute on its turnaround.

Unfortunately, such a turnaround looks unlikely when we examine the balance sheet.

As the table below shows, PTON has $984 million in notes and $690 million in bank loans, for $1.67 billion in debt. That produces a debt/equity ratio of 6.44x, which is absurdly high. If we use Seeking Alpha Quant's debt count ( $2.4 billion ), which appears to include finance leases as part of debt, we get a "mind meltingly" high debt/equity ratio of 9.3x.

Peloton liabilities and equity (Peloton)

Peloton's cash flow based coverage ratios are pretty poor too. Free cash flow and operating cash flow were both negative last quarter, so it goes without saying that interest is not being covered by cash flows. What's more interesting is the comparative growth in interest and revenue. Last quarter, revenue declined 23%, while interest grew 143%.

Hypothetically, if those rates of change continued, with revenue declining at -23% and interest expense growing at 143%, interest costs were surpass revenues in just three years! I don't mean to say that interest will grow at 143% for several more years, as that would be extreme; rather as mentioned this is just a hypothetical exercise to show what it would look like.

With Peloton's negative cash flows, the possibility of increased debt is very real, and with the Fed continuing to hike interest rates, the interest on the debt could be quite high.

Peloton interest expense (Peloton)

When you look at Peloton's balance sheet, you can see that the company has some solvency issues. That, in my opinion, is a bigger problem than the company's declining revenue. When you have a massive amount of debt AND declining revenue, the possibility of bankruptcy becomes very real.

Yet there's a still-bigger problem for Peloton, one that calls into question whether it will ever pull off the " turnaround " it's attempting:

The products.

Home exercise equipment just isn't the life necessity today that it was in March 2020. Therefore, people are likely to be more price sensitive when shopping for gym equipment today, compared to two and a half years ago.

This is a bad omen for a company like Peloton that sells gym equipment at high price points. Taken in combination with the balance sheet issues, it speaks to a company that is likely to fare poorly in the months and years ahead. For this reason, I consider the stock a 'sell,' although only in the sense that I'd avoid exposure to it; I would not actively suggest shorting a beaten down stock like Peloton. The issue here is risk: continued declines are far from certain (a risk to shorts) but bankruptcy is very much possible (a risk to longs). With a stock like this, simply avoiding the asset entirely is better than any position, short or long.

Peloton's Competitive Landscape

Peloton is a gym equipment manufacturer operating in an industry with robust competition. Some competitors include:

-

NordicTrack, a manufacturer of treadmills, exercise bikes, and ellipticals.

-

Nautilus Inc ( NLS ), the maker of Schwinn exercise bikes and Bowflex gym equipment.

-

Echelon Fitness, a subscription-based exercise bike service that competes directly with Peloton.

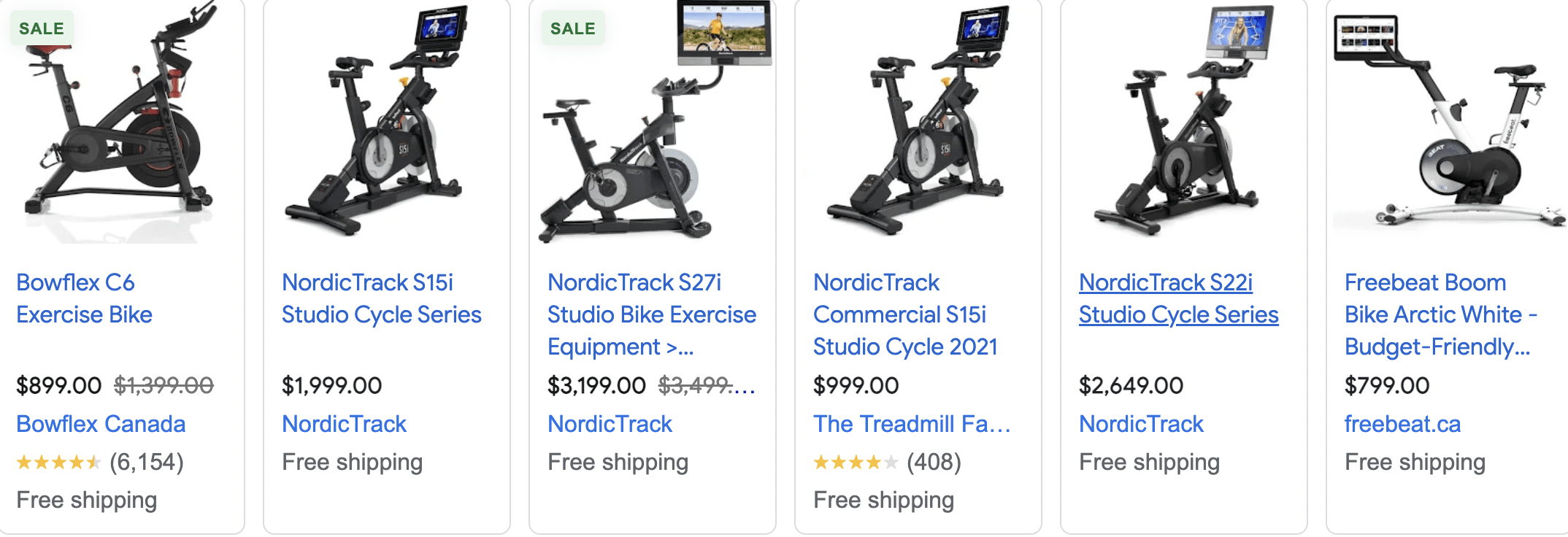

One advantage that Peloton has over these competitors is market share. It did $3.3 billion in revenue in the last 12 months, the #2 player Nautilus did just $387 million. So, Peloton is way ahead of its largest competitor. The data analytics firm M Science estimated Peloton's market share at 65% of the market for products priced over $1,400 (the percentage for the total market is lower than that). As for the negative part of the competitive dynamics, consider the images below:

Peloton Bike (Google Shopping) Competitor Bikes (Google shopping)

{kind=link}

These are the listings I was shown when I did a Google shopping search for peloton bikes. As you can see, the Peloton offering was by far the most expensive of the bunch, coming in at more than twice the price of several competitors' offerings, and $100 ahead of the least expensive competitor's offering.

Sometimes high prices can be a sign of high pricing power, but that doesn't seem to be the case with Peloton. PTON slashed the price of its original bike by $400 this year, for a 21% price decline. It really looks like the high prices that Peloton was able to charge in 2020 were a product of the pandemic-era surge in demand for such products. Unless lockdowns begin again, we wouldn't expect that demand to come back. So, Peloton's revenue will probably continue declining.

The problem here is that Peloton's product is not differentiated enough from those of its competitors to justify the high price point. The treadmills and bikes are structurally similar to those that NordicTrac and others offer. The only point of differentiation is the subscription, which gives you access to spin classes via the machine's built-in tablet. Many customers do claim to love this feature, but the problem is that it can easily be had more cheaply via options like:

-

Setting up a tablet on your exercise bike and watching YouTube.

-

Attending spin classes in person.

-

Using handheld gaming consoles like the Nintendo Switch, which let you do spin classes and other such things on any exercise bike.

Using simple options like the ones above, you can turn even the cheapest exercise bike into a viable Peloton substitute. Given that these options exist, why fork out extra money for a Peloton, whose sole differentiator is the subscription?

Peloton Valuation

Having looked at various issues with Peloton's business model and products, we can now turn to its valuation. Going by the multiples that are applicable, Peloton doesn't look particularly expensive, as it trades at :

-

0.80 times sales.

-

10.7 times book value.

-

A 1.27 EV/sales multiple.

The only multiple here that is high is the book value multiple: the other two are quite low. You're not even paying for a single year's worth of revenue when you buy Peloton stock--though of course, if sales keep declining, then you may be paying for more than next year's revenue.

Regardless of where sales go in the future, PTON's "low multiples" are mainly due to earnings and cash flows being negative and therefore non-meaningful. If Peloton managed to eke out a $0.01 profit per share in 2023, its earnings multiple (using today's stock price) would be 788, which is extremely high. The current negative earnings and free cash flow are even worse than such a high multiple would be. Peloton would either have to cut a lot of costs or somehow get revenue going up again to achieve $0.01 in earnings per share. So, the optical cheapness of PTON stock going by the sales and EV/sales multiples is misleading. Its earnings and free cash flow multiples would likely be high if the company managed to cut enough costs to produce positive profits, and that's assuming that the company's cost structure makes positive earnings possible at all. It could be that all of the company's current expenses are needed in order to sell the product, and that profits are basically impossible. Last quarter's 35% gross margin suggests that that's not the case, but the second-most recent quarter's -4.4% gross margin suggests that it was back then. At any rate, Peloton will need to cut out a lot of operating expenses if it's to have a shot at becoming profitable.

The Bottom Line

The bottom line on Peloton is that its core product isn't interesting enough to justify taking your chances on all these balance sheet issues. Peloton had negative gross profit as recently as two quarters ago, it's still EBIT-unprofitable today. In the meantime, it has a large debt load, a sky-high price/book ratio, and rising interest expenses. If Peloton were a differentiated product then maybe there'd be some outside chance of an early-2000s Apple ( AAPL ) style turnaround, but the product isn't that differentiated. Apart from the subscription, it's much the same as any other bike or treadmill. Therefore, the stock is not a good bet.

For further details see:

Peloton: The Problem Is The Product