CANO - PennantPark: 3 Distribution Hikes Push Yield To 16%

2023-05-11 12:47:06 ET

Summary

- On our last review of PennantPark, we pointed out what we liked and what we did not like about this BDC.

- We review the performance of this company relative to what we forecasted.

- We look at the three recent distribution hikes and tell you whether the high yield should be bought.

It has been some time since we covered PennantPark Investment Corporation ( PNNT ). The business development corporation has been a yield favorite thanks to having one of the highest yields in the BDC universe. The company also has made its investors happier by raising the distribution for three consecutive quarters. We review what we had said on our last coverage and tell you how we see things playing out from here.

Our assessment almost two years back was that PNNT was doing OK, but it was not a slam dunk case. We liked it on a relative basis to the broader small cap index which was filled with bubbles, but less so relative to quality plays.

Relative to other BDCs though, PNNT is a mixed bag. There are other BDCs that are far more conservative than PNNT in terms of type of investments. Oaktree Specialty Lending Corporation ( OCSL ) is one that comes to mind with its far larger first and second lien exposure. But PNNT is certainly more attractive compared to BDCs like Newtek Business Services Corporation ( NEWT ) that are facing peak revenues this year and trade at a high multiple. We would rate PNNT shares as neutral at this time and note that they deserve consideration as an alternative to investing in the Russell 2000 ( IWM ).

Source: Looking At Risk Levels Today

How did that turn out? Actually that prediction was close to perfect.

PNNT did better IWM and worse than OCSL. It took NEWT to the cleaners with a 43% beat. Some of NEWT's problems stem from its conversion to a bank holding company , but the primary reason it did so horribly was the abnormal valuation that income chasers had pushed it to back then.

The key lesson there is that you "make" a lot more money by avoiding losers like NEWT than you make by picking winners like OCSL.

Q2-2023

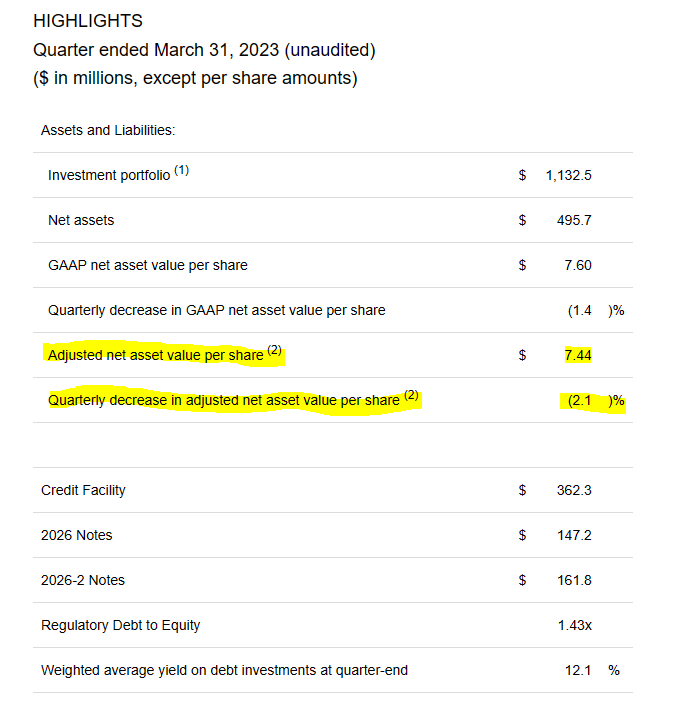

PNNT has its fiscal year end in September 2023. The just released quarterly results is hence for Q2-2023. PNNT reported a small decrease in NAV and adjusted NAV per share.

{kind=link}

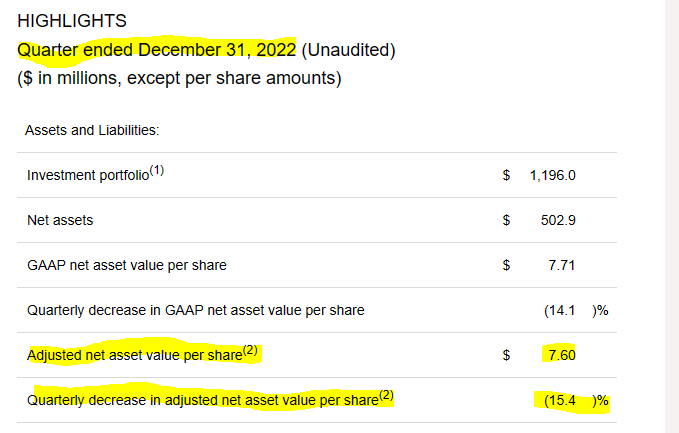

While most BDC NAVs have held up relatively well over the last three months, we would keep in mind that these valuations are highly subjective. A 2% NAV drop is a rounding error on Level 3 spreadsheets. While this quarter's drop was small, it came on the back of a rather humongous fall last quarter.

{kind=link}

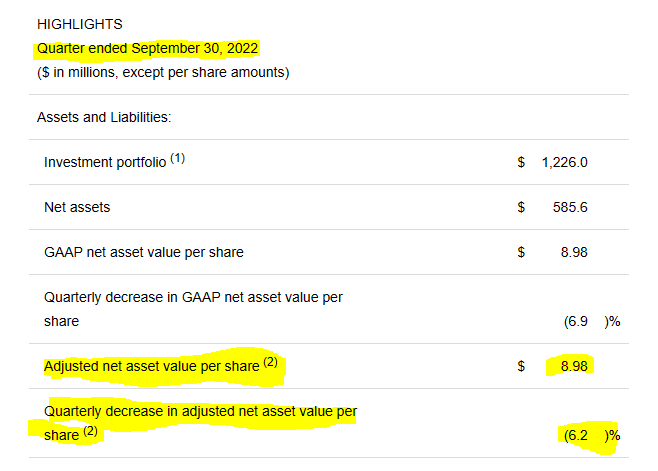

This was driven by poor performance of investments in Cano Health ( CANO ) and Ram Energy. Previous to that PNNT's NAV had fallen 6.2% in the fourth quarter of fiscal 2022.

{kind=link}

This has been quite the ride for PNNT investors and the performance over the last 12 months on NAV has been near the bottom of the barrel. We have shown Main Street Capital Corp ( MAIN ), OCSL, and FS KKR Capital Corp ( FSK ) are comparatives.

Interestingly through sale and purchase of multiple investments, PNNT's current non-accrual levels are low.

As of March 31, 2023, we had one portfolio company on non-accrual , representing 1.0% and zero of our overall portfolio on a cost and fair value basis, respectively. As of March 31, 2023, the portfolio had net unrealized depreciation of $32.1 million. Our overall portfolio consisted of 135 companies with an average investment size of $8.4 million, and a weighted average yield on interest bearing debt investments of 12.1%.

Source: PNNT Press Release

But you can find the impact of these "errors" in the income statement.

For the three and six months ended March 31, 2023, net realized gains (losses) totaled $(148.7) million and $(144.7) million, respectively.

Source: PNNT Press Release

You can compare the $148.7 million in losses vs. the $16.6 million in net investment income this quarter. So these are poor numbers, especially at a stage of the cycle where defaults have still been on the low side. This suggests poor underwriting quality and a focus on reaching for yield rather than managing risk. We mentioned this the last time when we wrote about it. PNNT was swinging for the fence by moving aggressively into non-debt investments. It had 36% in equity investments in Q2-2021.

PNNT Q2-2021 Presentation

What kind of outcome did you expect?

After running aggressively right into that storm PNNT is now trying to flee this same area.

As of March 31, 2023, our portfolio totaled $1,132.5 million, which consisted of $648.4 million of first lien secured debt, $111.3 million of second lien secured debt, $147.9 million of subordinated debt (including $95.4 million in PSLF) and $224.9 million of preferred and common equity (including $53.4 million in PSLF).

Source: PNNT Press Release

Preferred and common equity are down to a shade under 20%. But that move in and out has cost investors valuable equity and it has cost management valuable credibility. PNNT is going to continue middling in the BDC group until this changes.

Distribution Increases and Verdict

So we did get a third consecutive distribution hike and the number went from 15 cents a quarter to 20 cents a quarter. The yield is now over 16%. That stands out, even in the high-yielding BDC sector.

The stock is at a notable discount to its NAV.

These two positives are offset by some really poor underwriting and decision making by PNNT management. As with all our verdicts we don't go scrolling through tons of minute details to look for the last couple of cents. We weigh the macro outlook as the biggest driver, and since we think we are in for a recession, we're not chasing the riskier stuff here. We rate the stock a hold and think total returns will be positive but poor, from this point ($5.15 stock price as we write this).

One to Consider

Currently about 67% of the investments are first or second lien secured debt for PNNT. This percentage is very close to that of FS KKR Capital which has about 68.7% here . FSK trades at a smaller discount but recent performance on its investments has been far better. Also, the median portfolio company EBITDA is far higher than what PNNT invests in. So despite the slightly smaller yield, we think FSK wins out here. If we had to buy one very high yielding BDC here, it would be FSK.

We actually did not buy either as we think this is not the stage to reach for any yield. We did highlight one FSK corporate bond in our Marketplace Service that seemed cheap to us.

These are rated Baa3 (lowest rung of investment grade) by Moody's and traded at a very solid 7.89% yield to maturity on April 21, 2023.

Interactive Brokers, April 21, 2023

Two year bonds from investment grade BDCs generally offer a shade under 7% on average but this one got abnormally cheap.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

PennantPark: 3 Distribution Hikes Push Yield To 16%