CANO - PennantPark: Big Win From Dominion/Fox Settlement

2023-06-11 08:45:00 ET

Summary

- Plenty of good news for PennantPark Investment Corporation shareholders, including upcoming higher NAV per share, recently improved watch list, and huge earnings from the Dominion dividend.

- Dominion Voting Systems and Fox News agreed to settle the defamation lawsuit, resulting in dividend income for PNNT's equity position.

- PennantPark is currently trading 23% below NAV (before upcoming NAV increases) and yielding almost 14% (before upcoming dividend increases).

- For these reasons, plus the ones discussed below, are likely why PennantPark management has been actively purchasing shares.

- Also included are comparison charts/tables, list of positive and negative considerations, important/relevant issues, management notes, etc. used for setting target prices.

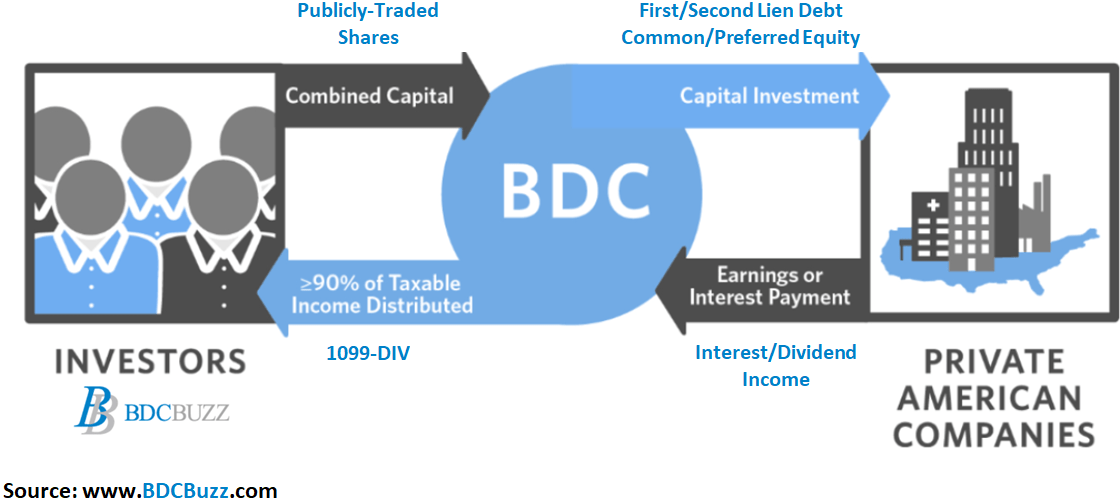

Quick Introduction To Business Development Companies

Business development companies ("BDCs") invest shareholder capital in privately owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds. Anyone can invest in BDCs, as they are public companies traded on major stock exchanges. Also, many BDCs have investment grade ("IG") bonds/notes for lower-risk investors building a balanced 60/40 portfolio (composed of 60% to 70% stocks/equities and 30% to 40% bonds or other fixed-income offerings).

{kind=link}

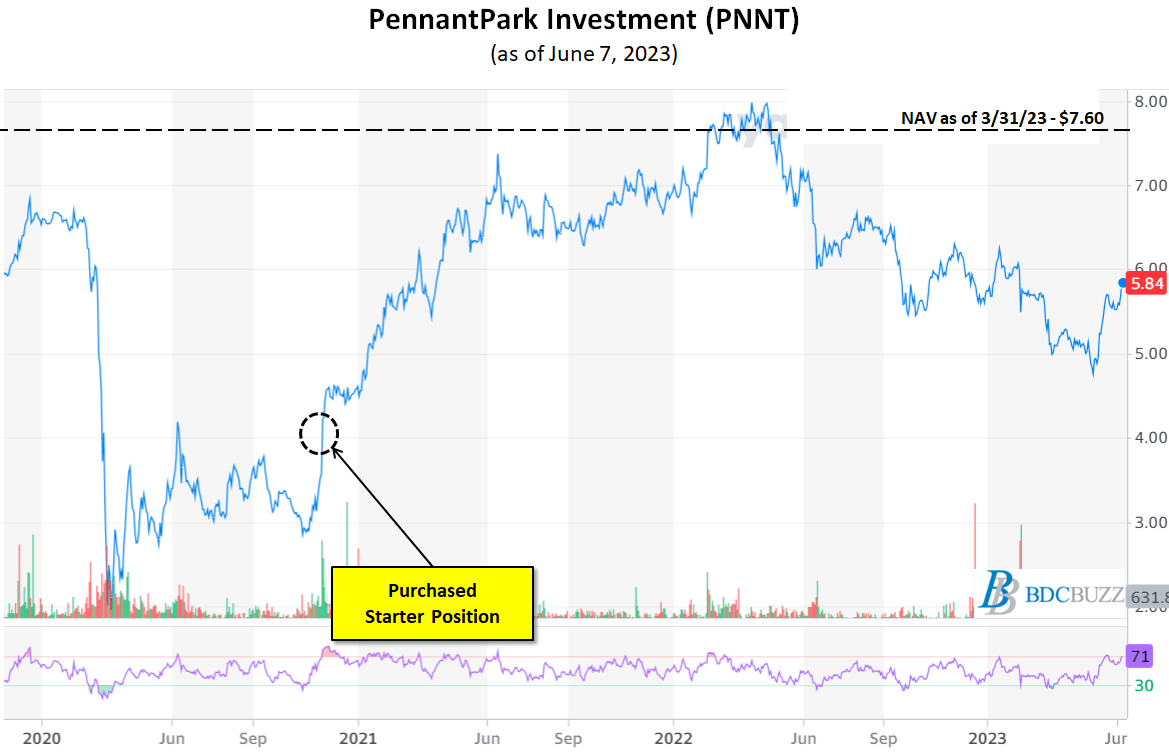

This article discusses PennantPark Investment Corporation ( PNNT ) which I purchased in November 2020 at $4.06 (currently $5.84) per share, as discussed in a previous article:

At the time of the article, PNNT was trading 42% below book value or net asset value ("NAV") compared to the current 23% discount.

PNNT has paid $1.39 per share in dividends since my purchase for a total return of 78% ($3.17/$4.06), or around 25% annualized.

This article discusses the following for PNNT:

- Portfolio mix and changes in book/net asset values

- Dividend coverage

- Recent insider purchases

- Pricing and valuation

- Positive and negative considerations.

PNNT Dividend Coverage

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with three quarters of financial projections using base, best, and worst-case assumptions to test the sustainability and potential growth of the current dividend for PNNT .

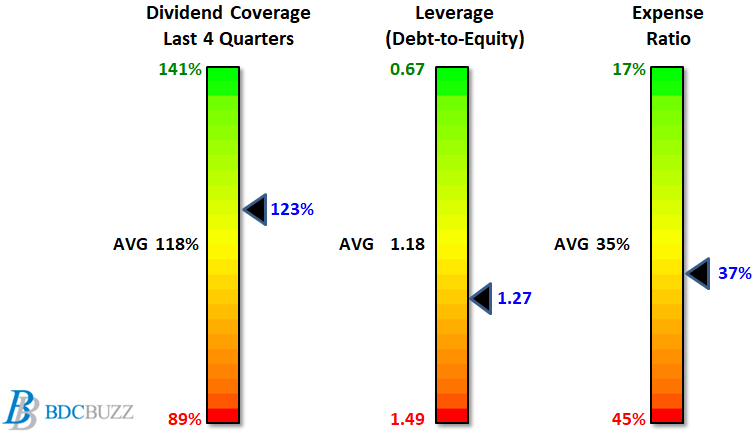

The following charts compare PNNT to the other 25 BDCs that I cover to help establish target prices (discussed later). BDCs with lower expenses and higher potential (different from historical shown below) dividend coverage typically have stable to growing dividends, and investors pay higher prices.

{kind=link}

{kind=link}

Higher-yield investments have become even more attractive given the inflationary, as investors are seeking additional income from invested capital. Similar to Real Estate Investment Trusts ("REITs"), Business Development Companies are regulated investment companies ("RICs") required to pay at least 90% of their annual taxable income to shareholders, avoiding corporate income taxes before distributing to shareholders. This structure prioritizes income to shareholders (over capital appreciation), driving higher annual dividend yields currently ranging from around 9% to 15%.

As mentioned in " Dividend Increase Coming For PNNT ":

the average BDC pays dividends of around 9% of NAV, which would be $0.88 per share annually or $0.22 per share quarterly compared to the current $0.12 per share quarterly dividend.

Since that article, PNNT has increased its regular quarterly dividend six times, from $0.12 per share (as of Q4 2020) to $0.20 per share (as of Q2 2023) driving a current dividend yield of almost 14% (before additional increases).

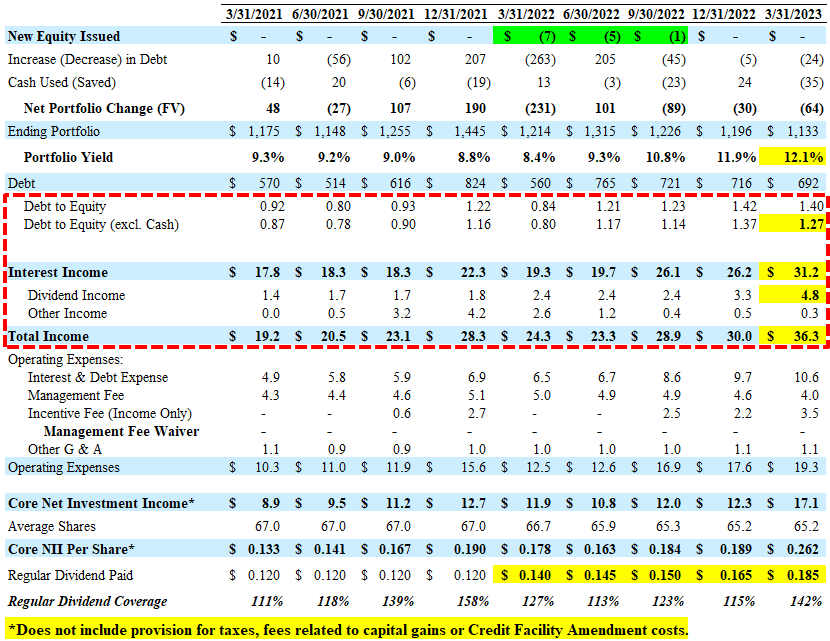

PNNT continues to improve its dividend coverage partially due to higher portfolio yield, maintaining the portfolio with higher leverage, selling and reinvesting of many of its equity positions, and continued increased returns from its PennantPark Senior Loan Fund (“PSLF”) joint-venture with Pantheon Ventures . Last month, the company increased its quarterly dividend from $0.185 per share to $0.200 per share for Q2 2023, which was projected in my previous best case projections .

Our debt portfolio continues to benefit from rising base rates, as of March 31st, our weighted average yield to maturity was 12.1%, which is up from 11.9% last quarter and 8.4% last year. As a result of a stable debt portfolio and growing net investment income. The board of directors has approved another increase in the quarterly dividend to $0.20 per share. This is an 8% increase from the prior quarter and the 38% increase from a year ago. We are confident that with the continued strong credit performance, the increased dividend will be more than fully covered by net investment income .”

During calendar Q1 2023, PNNT easily beat my best case projections (again) mostly due to much higher-than-expected dividend income of $4.8 million partially offset by lower other income driving earnings of $0.26 per share (excluding provision for taxes) covering the quarterly dividend by 142%. There was a meaningful decrease from a debt-to-equity of 1.37 to 1.27 (net of cash) due to higher-than-expected repayments of $106 million.

{kind=link}

There was another increase in the amount of dividend income from its PSLF, from $2.4 million in calendar Q3 2022 to $3.7 million, for calendar Q1 2023, which is considered ‘recurring’ and taken into account with the updated projections:

On March 31st, the JV portfolio equals $748 million and together with our JV partner we continue to execute on the plan to grow the JV portfolio to $1 billion of assets. We believe that the increase in scale and the JV is attractive double-digit ROE will also enhance PNNT's earnings momentum.”

Q. “Is the current dividend run rate at the JV that's being upstreamed to the BC sustainable? Or is there sort of a onetime non-recurring dividends received this quarter?”

A. “There's no non-recurring . It's a sustainable dividend. In fact, we're -- same thing we ever in the dividend and the JV.”

{kind=link}

The company did not repurchase additional shares, mostly due to be near the upper end of its targeted leverage. The stock is currently trading around 23% below its NAV per share and I am projecting additional shares repurchased (in the base and best projections) which would be highly accretive to NAV per share and upcoming earnings. Management discussed on the previous call mentioning higher amounts of repurchases depending exits of portfolio investments (emphasis added):

We're always considering a stock buyback program. I think this might be our second or third program we've done. We are now 1.4 times levered at PNNT, which is a bit above our target leverage , and we're working with the rating agencies on our ratings. So stay tuned. Nothing really to announce at this point.”

On April 18, 2023, Dominion Voting Systems and Fox News Network agreed to settle the defamation lawsuit filed by Dominion against Fox News. As part of the settlement, Fox News agreed to pay Dominion $787.5 million. Dominion is a portfolio company of PNNT, which holds a minority equity interest in the company. While Dominion may retain some of the settlement proceeds for corporate purposes, the company communicated its intention to distribute a substantial amount portion of the proceeds, net of estimated taxes and expenses, to its equity holders and PNNT's portion is estimated to be approximately $12 million [$0.18 per share] . The timing and amount of any distribution is uncertain and subject to change. Q. “I just want to make sure I understand this right. But the settlement that you guys announced in the press release last night that $12 million. So, are we looking at potentially like an $0.18 sort of one-time payment in a future quarter” A. “Yes, that's correct. That'll come through as a dividend income.”

It should be noted that the dividend income of $12 million from Dominion would be around $0.184 per share. After incentive fees, this would be around $0.161 per share of additional earnings , compared to its regular quarterly dividend of $0.200 per share.

PNNT Portfolio Risk Profile & Credit Quality

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with a constantly updated full risk profile and rankings for PNNT .

The following charts compare PNNT to the other 25 BDCs that I cover to help establish target prices (discussed later). Investors pay higher prices for BDCs with higher quality credit platforms and management as they typically have higher quality portfolios and a stable to growing NAV per share.

{kind=link}

{kind=link}

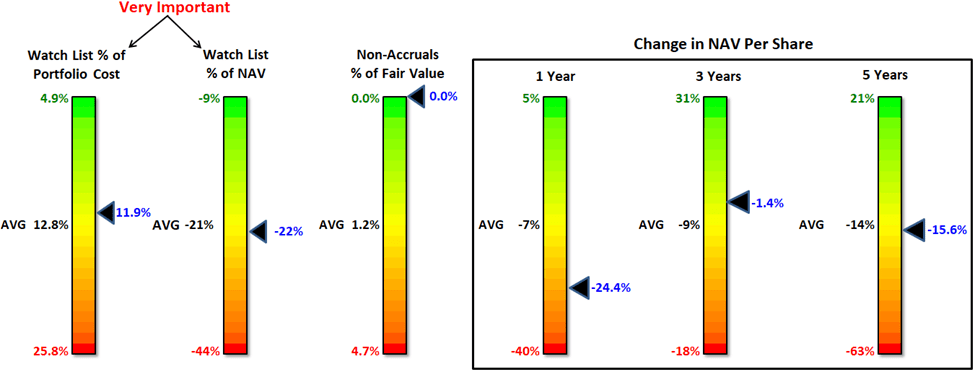

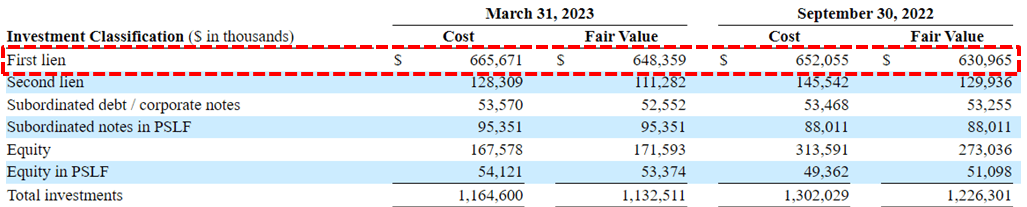

As anticipated in previous articles, PNNT finally exited its legacy investment in RAM Energy , likely resulting in an upgrade over the coming quarters, especially if there is continued progress in the amount of investment considered watch list, as discussed later. The amount of first-lien investments has increased from 51.5% to 57.2% of the portfolio fair value over the last two quarters. Equity investments (excluding the PSLF) have declined from 36% of the portfolio (as of March 31, 2021) to 15% (as of March 31, 2023) closer to the 10% management is targeting.

I think we hope that over the next year or two, we're going to be able to get some reasonable exits and bring it down. We are starting to see buyers and sellers get together and our deal flow is picking up. No guarantees as to what's going to close between now and June 30th. And what's going to close after June 30, but it does feel like the second half of 2023 will certainly be busier than the first half.”

{kind=link}

During calendar Q1 2022, PNNT sold its equity position in PT Network (Pivot Physical Therapy), generating $2.11 per share of realized gains. However, during calendar Q1 2023, there was around $148 million or $2.27 per share of realized losses mostly related to exiting RAM Energy and restructuring Walker Edison Furniture .

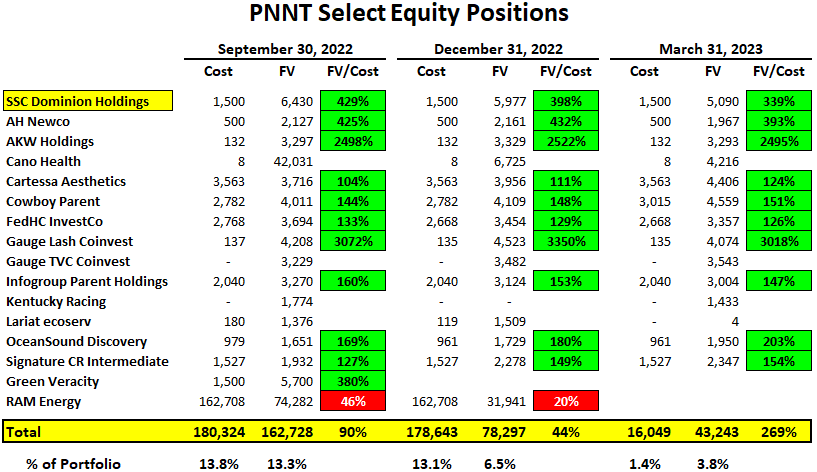

The following table shows some of PNNT’s equity investments accounting for around 4% of the total portfolio fair value with over $27 million of unrealized gains. If these investments were sold at their current fair values, it would generate around $0.42 per share of realized gains.

We typically participate in the upside by making an equity co-investment. High returns on these equity call investments have been excellent over time. Overall, for the platform from inception through March 31st. We've invested over $394 million in equity co-investments, have generated an IRR of 26% and a multiple on invested capital of 2.2 times. So, it's been very accretive. And just like the sponsor, there's an M&A exit, there's potential IPO exit. And then there's certainly dividends that can come out of that, the Dominion voting situation, that'll be a dividend coming at us out of a company, because we're an equity shareholder. So, we’re really aligning ourselves I guess we could sell our equity to the sponsor, if we need or want liquidity.”

{kind=link}

The valuation for its equity position in Dominion as of March 31, 2023, did not reflect the settlement proceeds (currently valued at $5 million as shown above):

Q. “Okay. Is that reflected in any way in the March 31 mark.”

A. “No, it is not reflected in the NAV for the March quarter, because we did not know it was an event as of March 31st. You could have put that $12 million into the mix and said, your equity percentage is higher than 15%. And that would have been right although this was a positive surprise out of the blue.”

The publicly traded shares of Cano Health ( CANO ) have increased by almost 50% (from $0.91 to $1.35 per share) so far in calendar Q2 2023. However, this investment only accounts for $0.06 of its NAV per share as of March 31, 2023, implying an impact of around $0.03 per share in Q2 2023.

Cano Health itself, it's a mark-to-market. Deal is not done yet. They're the largest competitor. Oak Street Health announced yesterday that they were getting bought by CVS at a very high price. There is a bit of a turf grab going on in that primary care space. So we're not done yet. I would remind you that Humana is a minority shareholder of Cano Health. Whether they or other parties see value in Cano Health company, that the company itself yet to be determined. It has been a volatile stock. It has been painful to watch the stocks trade lower over the course of the last three-six months. But we're not done yet on Cano Health and our belief is, over time, this company will ascertain real value above and beyond where it's being marked today.”

During calendar Q1 2023, PNNT’s NAV per share decreased by 1.4% (from $7.71 to $7.60) mostly due to net portfolio depreciation partially offset by over-earning the dividend. Some of the largest markdowns were many of its ‘watch list’ investments including DermaRite Industries ($0.03 per share), Express Wash , and Beta Plus , but also some of its equity positions including Cano Health ($0.04 per share) and Lariat Ecoserv ($0.02 per share).

Walker Edison Furniture was previously considered a ‘watch list’ investment but added to non-accrual status, as predicted in previous reports. This is a position held by other BDCs that was previously benefitting from COVID-related consumer spending habits but now faces headwinds related to supply chains and changes in consumer spending as discussed on the recent call including an “equity cushion by the large private equity sponsor” and “restructuring conversations going on as we speak”. However, Walker Edison was restructured during calendar Q1 2023, resulting in decreased non-accruals declining from 1.1% to 0.0% of the portfolio fair value and was discussed on the recent call:

The credit quality of the portfolio continues to perform well as of March 31st. we had one non-accrual out of 135 different names a PNNT. This represents 1.1% of the portfolio cost and 0% at market value. Our investment of Walker Edison has returned to accrual status after completing a balance sheet restructuring.”

Q. “The restructured loan of Walker Edison, my understanding is that it's 100% pick, did you consider leaving it on nonaccrual for the time being, until such a point in time as the company is able to turn that into more of a cash pay instrument?”

A. “I think the independent valuation firms are marking that instrument at par. It's not -- by the way, it's not really material in PNNT at this point anyway. I think our valuation firm said, hey, it's a par instrument. Grant granted, if in a couple quarters, the company doesn't perform well, and it starts to get marked down. I think. I think we'll take another look at that. Again, thankfully, it's not that big of an investment for us at this point, it's underperformed, we're certainly hopeful that the company will find its footing and people will buy furniture from this company, and it will have a steady EBITDA. And at some point, we certainly hope our debt is paid off and our equity has value. But it's early days.”

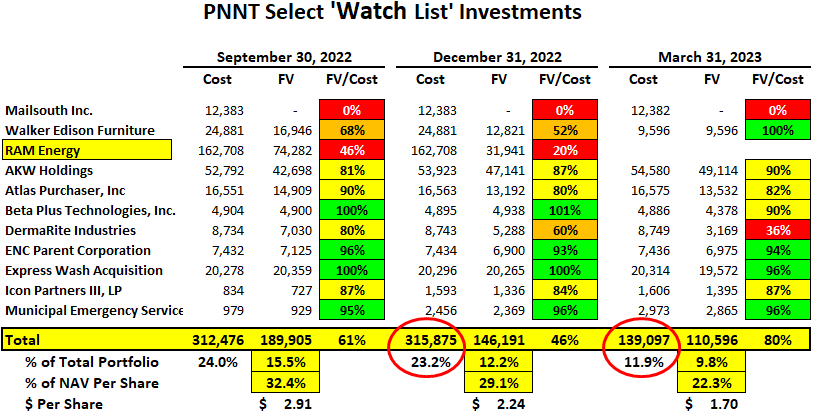

Historically, PNNT has had a much higher amount of investment considered watch list but is actively rotating its portfolio into safer investments, including the final and full exit from RAM Energy and recent restructuring Walker Edison Furniture . It is important to note that PNNT’s NAV per share has declined by over 24% over the last four quarters. However, the amount of watch list investments has recently declined from 23% to 12% of the portfolio at cost, as shown below.

Mailsouth was previously considered a "watch list" investment but added to non-accrual during calendar Q2 2022 and remains the only investment on non-accrual status. AKW Holdings has currency-related exposure.

{kind=link}

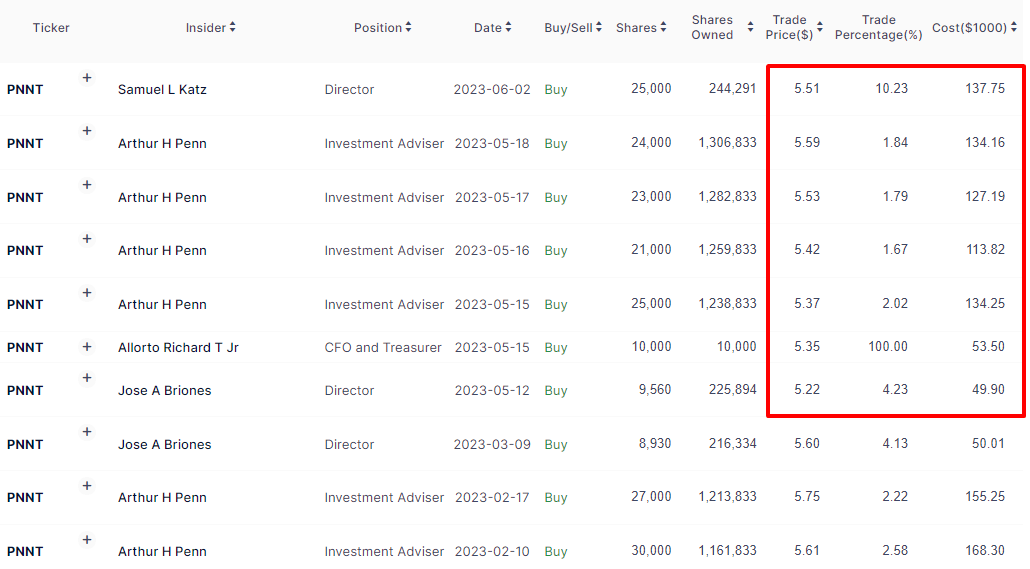

Recent Insider Purchases

{kind=link}

Insiders, including Art Penn, have recently purchased additional shares at prices between $5.22 and $5.59:

{kind=link}

{kind=link}

BDC Pricing & ROEs

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with updated target prices and suggested limit orders (for making purchases) for PNNT .

There are very specific reasons for the prices that BDCs trade driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage).

- BDCs with higher quality credit platforms and management typically have higher quality portfolios and investors pay higher prices. This drives higher multiples to NAV and lower yields.

- BDCs with lower expenses and higher potential dividend coverage typically have stable to growing dividends and investors pay higher prices. This drives higher multiples to NAV and lower yields.

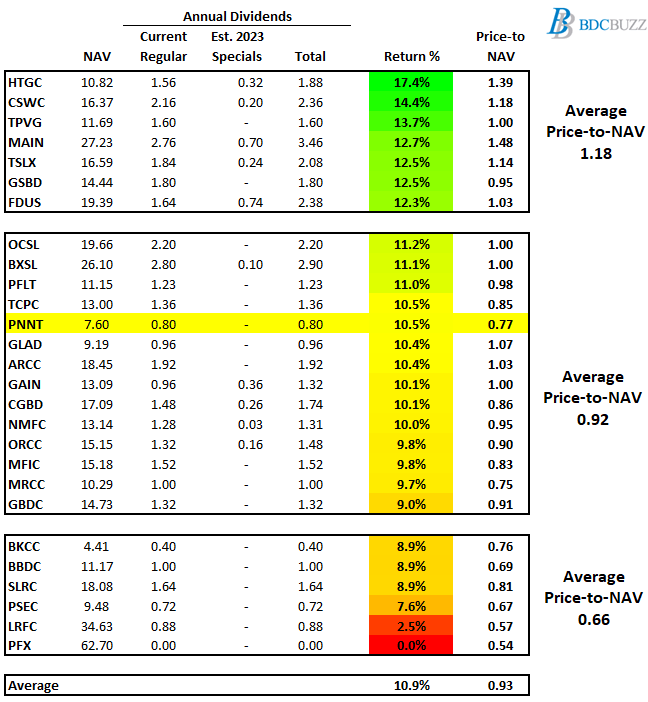

As mentioned earlier, PNNT has increased its regular quarterly dividend six times, from $0.12 per share to $0.20 per share, which is $0.80 annually and 10.5% of its current NAV per share ($0.80/$7.60).

{kind=link}

The average BDC was previously paying around 9% of NAV in annual dividends (also mentioned earlier) which has increased to almost 11% (as shown below) mostly due to the positive impacts from higher interest rates as BDC assets are primarily at floating rates.

Over the coming quarters, I am expecting PNNT's NAV to 'reflate' closer to previous levels for many reasons, including a partial reversal of unrealized depreciation, over-earning the dividend, and potential share repurchases. Higher NAV per share has many positive impacts including the ability to use higher leverage and its incentive fee “hurdle rate” of 7.0% which is applied to “net assets” to determine “pre-incentive fee net investment income” per share before management earns its income incentive fees.

The following table shows the current annual dividends divided by NAV per share as a simple proxy for current returns on equity (“ROE”) to shareholders. BDCs with higher risk portfolios should be able to deliver higher returns through higher portfolio yields. Conversely, lower-risk BDCs have lower portfolio yields due to safer assets/investments. However, many of the other BDCs with lower return ratios are due to higher operating costs and/or credit issues driving lower prices paid by investors. As PNNT continues to increase the amount of dividends paid, its stock price will follow higher.

{kind=link}

Summary & Recommendations

The following are many of the positive considerations for PNNT, most of which were discussed earlier:

- Recent insider purchases

- Finally exited its legacy investment in RAM Energy

- Upcoming dividend income from Dominion of $12 million or $0.16 per share of additional earnings after incentive fees

- Walker Edison Furniture has been restructured and added back to accrual status

- Relatively lower non-accruals at 0.0% of portfolio at fair value

- Equity investments (excluding the PSLF) have declined from 36% of the portfolio as of March 31, 2021, to 15% as of March 31, 2023 closer to the 10% management is targeting

- First-lien investments have increased from 51.5% to 57.2% of the portfolio fair value over the last two quarters

- The amount of ‘watch list’ investments has recently declined from 23% to 12% of the portfolio at cost, which is slightly better than average

- The valuation for its equity position in Dominion does not reflect the settlement proceeds (currently valued at $5 million)

- The publicly traded shares of Cano Health have increased by ~50%

- Six quarters of consecutive dividend increases from $0.12 to $0.20 per share per quarter

- Meaningful increase in the amount of dividend income from its PSLF, from $2.4 million in calendar Q3 2022 to $3.7 million, for calendar Q1 2023

- Undistributed taxable income (“UTI”) was previously around $0.71 per share

- Base management fee of 1.00% for assets in excess of 1.00 debt-to-equity

- Previously waived incentive fees

- The stock is currently trading 23% below its NAV per share and additional shares repurchased would be highly accretive to NAV per share and upcoming earnings

- Continued rotation out of equity positions into income-producing debt positions likely resulting in an upgrade over the coming quarters

The following are many of the negative considerations for PNNT, most of which are discussed in this report:

- NAV per share has declined by over 24% over the last four quarters

- Net realized losses of almost $200 million or $3.03 per share over the last 10 years

- Relatively higher leverage currently with a debt-to-equity ratio of 1.27

- Fewer share repurchases due to being near its upper targeted leverage

- Slightly higher-than-average expense ratio due to 1.50% management fee and 7.00% hurdle rate (should be 8.00% given the higher yield portfolio)

- Lack of "total return" hurdle or "look back" provision when calculating income incentive fees to protect shareholders from capital losses. However, management previously waive incentive fees during periods of material capital losses

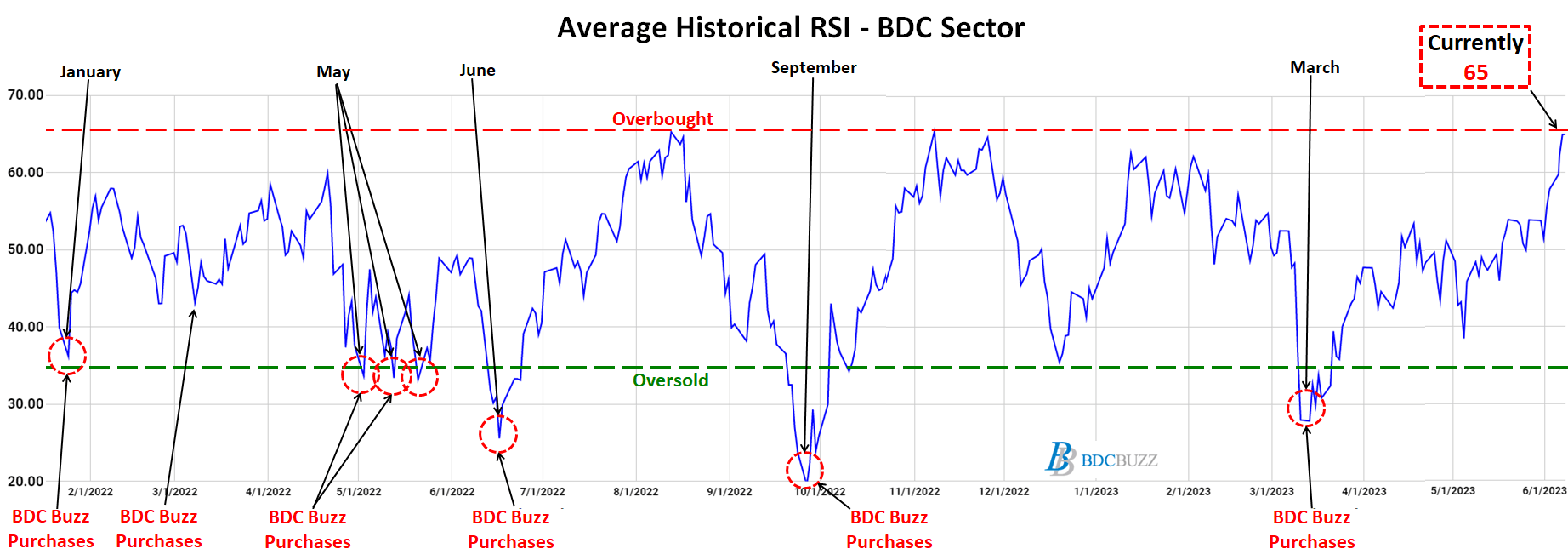

One of the many reasons that I like to invest in the BDC sector is taking advantage of market volatility to lower my weighted average purchase prices, driving much higher returns. I closely watch for general market pullbacks to make purchases of higher quality BDCs. Some indicators that I follow include the S&P Volatility Index ( VIX ), Fear & Greed Index, and the Relative Strength Index ("RSI").

The following chart is from my BDC Google Sheets so that investors can see in real time if the sector is overbought or oversold. When the entire sector is oversold, there's nothing wrong with "your stock" and it means that you should buy more at these levels. BDC pricing is often driven by changes in investors' attitude about risk.

BDC prices continue to rally from the March 2023 lows likely due to reporting strong Q1 2023 results with average dividend coverage of around 125% even after taking into account the massive amount of dividend increases for the sector (90% of all BDCs have increased their dividends recently). Also, most BDCs reported stable to growing NAV per share.

After each general market and BDC sector pullback, BDC pricing quickly rebounds, giving investors little time to make additional purchases, which is why it is important to set appropriate target prices and limit orders.

As shown below, the average RSI has rebounded again from the most recent low in March 2023. Also shown are my previous purchase points, as I continue to take advantage of market volatility to make additional purchases of my smaller positions, which have provided excellent returns that will be discussed in upcoming articles.

{kind=link}

Clearly, BDCs are currently in overbought territory. I would suggest making smaller purchases of the best-priced BDCs and waiting for another general market pullback to make larger purchases. The Relative Strength Index or RSI is an indicator that I use only after I already know which BDC I would like to purchase but waiting for a good entry point. I consider target prices to be much more important when adding to current positions. Also, I would suggest that investors ignore RSI when starting small positions and then use it for timing additional purchases to build your position.

PennantPark currently has an RSI of 71, implying overbought, with an upcoming ex-dividend date for its regular quarterly dividend of $0.20 per share on June 14, 2023 , which could be a buying opportunity, especially if there is also a general market pullback at some point.

{kind=link}

For further details see:

PennantPark: Big Win From Dominion/Fox Settlement