PNNT - PennantPark Investment: A Growing 12%+ Yielder

2023-09-12 02:56:35 ET

Summary

- PennantPark Investment Corporation has seen a decline in the percentage of its portfolio included on the watch list, indicating improving credit quality.

- PNNT has a well-diversified portfolio, but with a substantial exposure to equities. However, management has committed to reducing the percentage of equity investments in the portfolio.

- PNNT offers an attractive dividend yield of around 12.71% and has a solid net investment income coverage ratio, supporting its dividend stability.

PennantPark Investment Corporation ( PNNT ) is a business development company ((BDC)) operating in what it describes as the core mid-market segment. The BDC offers a highly attractive dividend yield and has recently reported a substantial decline in the percentage of its portfolio included on the watch list. The reduction in the number of investments on the watch list could be an early indicator of improving credit quality and further reduces the risk of rising non-accruals, which have in either event generally been quite low at PNNT.

The portfolio

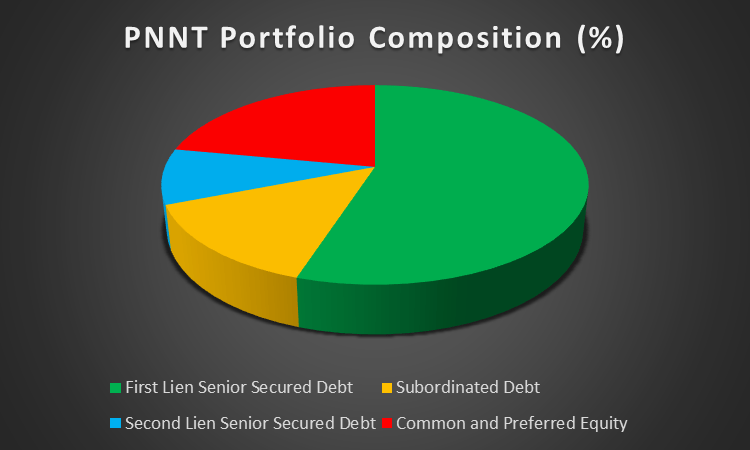

PNNT has a relatively well-diversified portfolio with around 55% of its portfolio being first lien senior secured loans and around 9% being second lien senior secured debt. However, it also has a fairly substantial exposure to equities with around 22% of its portfolio consisting of common and preferred equity. While this is not necessarily a problem, equity in smaller middle market companies can be extremely challenging to value accurately and often sees the market discounting such investments due to this inherent uncertainty.

{kind=link}

Author created based on data from company filings

Nevertheless, the equity portion of its portfolio is somewhat less significant when excluding its investment in the PennantPark Senior Loan Fund (PSLF). Excluding PSLF, its joint venture operation, the equity portion of its portfolio represents only 17% of its total portfolio. Importantly, PNNT’s equity investments have by no means performed poorly with its most recent earnings call indicating that the BDC has generated an internalised rate of return of around 26% on its equity investments.

Despite these reasonable returns the equity portfolio has likely been a drag on the stock and contributed to the discount to NAV. Management seems to be aware of this and has promisingly committed to reducing the percentage of its portfolio consisting of equity investments to around 10% of the overall portfolio value. This rotation out of equity investments is a positive development, in my view, and here I agree with BDC Buzz who recently observed that PNNT’s “[c]ontinued rotation out of equity positions into income-producing debt positions [could] likely result[…] in an upgrade over the coming quarters”.

The underlying companies to whom loans have been advanced have also largely performed in line with expectations save for isolated instances in certain industries such as retail. I am of the view that the challenges in the retail sector might persist for some time still given the trend of middle income consumers cutting non-essential expenditure driven by persistently higher-than-normal inflation levels. The diversified nature of PNNT’s portfolio will mitigate some of the potential adverse effects of its exposure to the struggling retail sector. Consumer products and services currently makes up around 13.6% of PNNT’s portfolio and likely presents the sector that should be monitored most closely by investors in upcoming quarters.

Management has also expressed some confidence in its underwriting to withstand a recession noting that –

In a normal environment, we would say sometime during our 5-year loan, we have to model in a recession. The reality is today, we model in a recession kind of in year 1 because that's how we should be underwriting credit. We should be feeling comfortable about our loans even in recessionary environments.

While only time will tell if there will be a recession or if PNNT’s underwriting has truly adequately factored in the risk, to me it does signal a management more focused on quality underwriting and portfolio quality.

Earnings and dividend stability

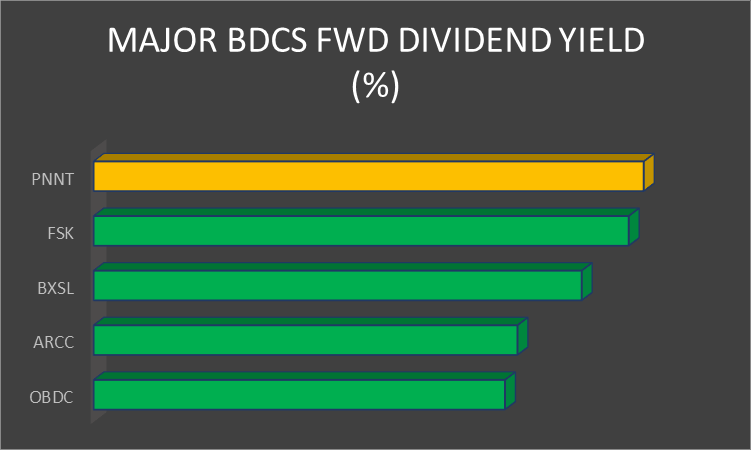

PennantPark Investment Corporation offers an attractive forward dividend yield of around 12.71% which is the highest of the major BDCs considered in the peer-comp chart below. In its most recent quarter, the BDC increased the dividend per share from $0.2 to $0.21 per share. This was also the sixth consecutive quarter in which the dividend per share for PNNT was increased having grown from $0.14 per share in March 2022 to the current $0.21 per share.

{kind=link}

Author created based on data from SA

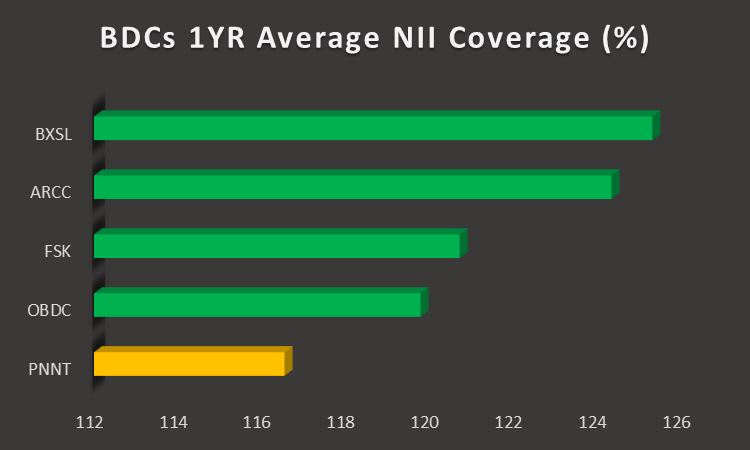

These dividend increases have been well supported by net investment income ((NII)). PNNT has a one-year average NII coverage ratio of almost 117%, which although lower than its peers in the peer comp chart below, indicates a well-covered dividend. In the third quarter, the BDC reported NII per share of $0.35 indicating that the dividend was covered by NII at a rate of 166%.

{kind=link}

Author created based on data from SA

This high coverage ratio may at first glance suggest substantial scope for further dividend increases. However, the NII was substantially higher than normal given the special dividend received by PNNT over the settlement obtained by Dominion Voting Systems from Fox News. Excluding this one-off item, the BDC generated core NII of $0.22 which makes for a NII coverage ratio of around 105%. This indicates that the scope for further dividend increases is likely to be more limited unless there are other expansions in NII.

There are also some positive signs from a growth perspective with management reporting an increase in deal flow. The JV in particular has continued to witness strong returns and growth with management observing that -

Over the last 12 months, PNNT earned a 17% return on invested capital in the JV. We expect that with the continued growth in the JV portfolio, the JV investment will enhance PNNT's earnings momentum in future quarters. Credit quality of the portfolio continues to perform well.”

Continued expansion of the portfolio could offer further opportunities for expanding NII and contribute to further dividend increases in the future. Nevertheless, in my view, the dividend is now at a comfortable level in relation to NII and should not grow at a pace exceeding growth in core NII.

Valuation

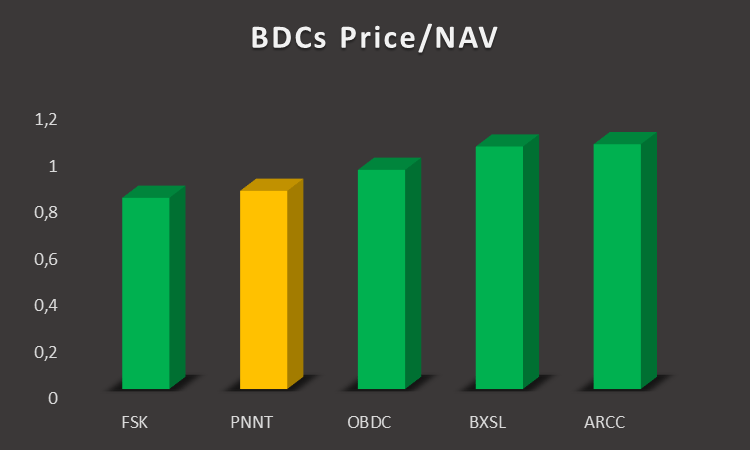

PNNT is trading at a discount to NAV of around 15% which is the second highest discount to NAV of the major BDCs considered in the peer comp charts below. Nevertheless, this is an improvement over its 3-year average discount to NAV of around 32%. While I do not believe that PNNT will trade at a premium to NAV in the near future, the reduction in the percentage of its portfolio in equities could contribute meaningfully to a rerating of the stock at a level closer to NAV.

{kind=link}

Author created based on data from SA

The recent growth in NAV would also support a rerating of the stock of this trend persists. Investors often discount BDC stocks to NAV on the basis of a perception that the price to NAV today is where NAV would be in the future. A growing NAV should accordingly reduce the need for a substantial discount to NAV. Investors in PNNT are, therefore, likely to monitor the NAV trajectory closely in the quarters ahead.

Conclusion

PNNT appears to offer an appealing investment opportunity for income investors with its strong 12%+ dividend yield supported by a solid net investment income coverage ratio. While there may be more limited room for further dividend increases in the short term, the company's growth prospects and expanding deal flow offer potential for future expansion. Its streak of six consecutive quarters of dividend increases is also impressive and signals a shareholder friendly management.

In terms of valuation, PNNT is currently trading at a discount to NAV, but recent improvements and a growing NAV could contribute to a potential rerating of the stock. As indicated, investors frequently discount BDCs with high equity exposure given the inherent difficulty in valuing that component of the portfolio. Management's continued reduction of this segment of the portfolio therefore bodes well for a long-term rerating of the stock.

For further details see:

PennantPark Investment: A Growing 12%+ Yielder