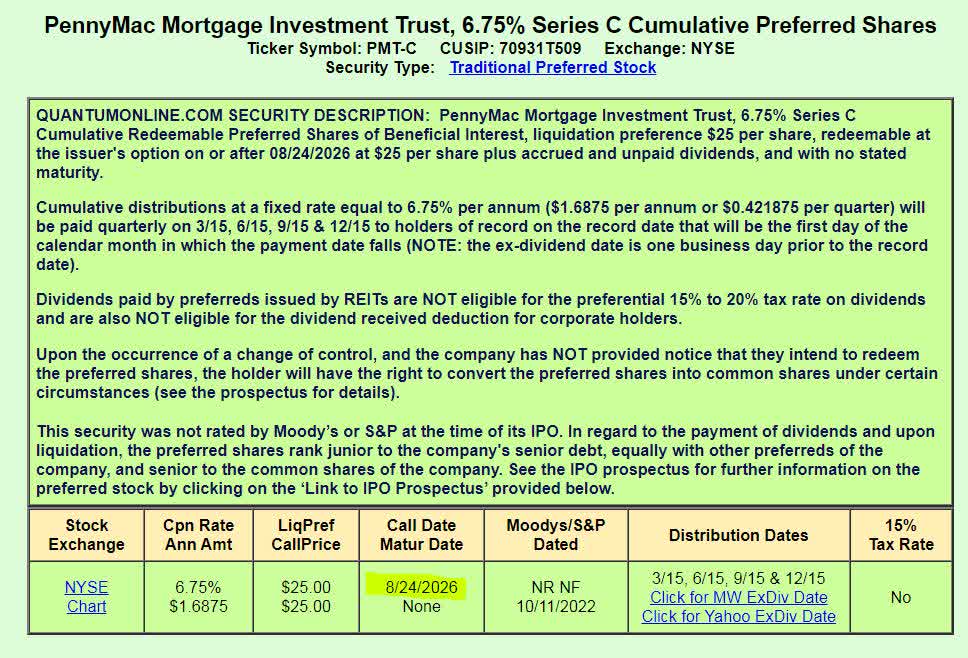

PMT - PennyMac C Series Preferred Yielding Over 9.7%

2023-04-24 23:12:29 ET

Summary

- PennyMac is a mortgage REIT (mREIT) that specializes in loan origination and servicing.

- The company has been quietly shifting its balance sheet to meet the challenges of higher interest rates.

- While not bulletproof, its role as a mortgage servicer provides an additional layer of diversification.

PennyMac Mortgage Investment Trust ( PMT ) has seen its shares plunge with the mREIT sector as mortgage originations have declined and the real estate market has cooled from the pandemic era surge. The company’s C series preferred shares have sunk to a dividend yield of greater than 9.7%. Since the C series have the longest call duration and highest income of the company's various preferred share offerings, I believe they are the best option for income investors.

{kind=link}

{kind=link}

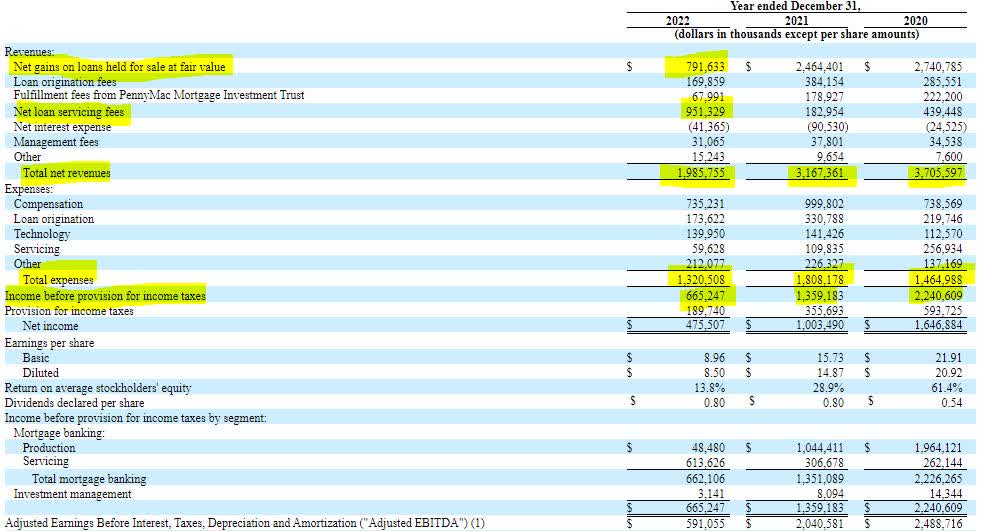

PennyMac’s income statement is indicative of the struggles facing the industry. Revenue from loans held for sale and origination fees dropped notably in 2022 due presumably to the origination of few mortgage loans. Overall income fell by a third or more than $1 billion to just under $2 billion. Expenses pulled back as well, but not enough to substantially impact income before taxes, which was cut in half to $665 million.

{kind=link}

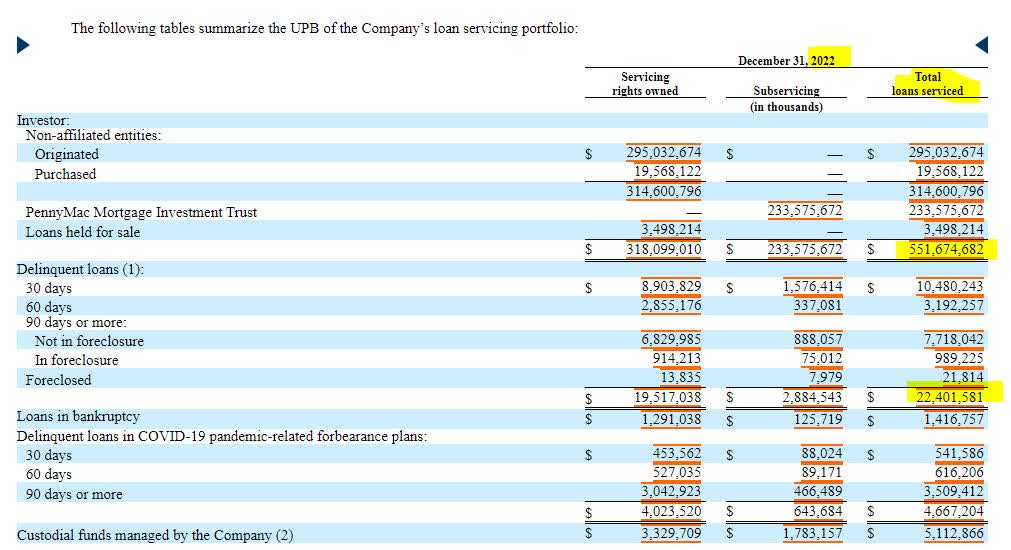

PennyMac’s income statement also highlights a differentiating factor between it and the industry. Loan servicing fees surged in 2022 from $183 million to $951 million. This is because PennyMac engages in mortgage servicing, where it facilitates the payment of mortgages from borrower to owner of the mortgage. These rights become more lucrative as interest rates rise and serve as a great hedge to the unrealized losses incurred by holding mortgages as an investment. PennyMac serviced loans with $551 billion in unpaid principal in 2022.

{kind=link}

{kind=link}

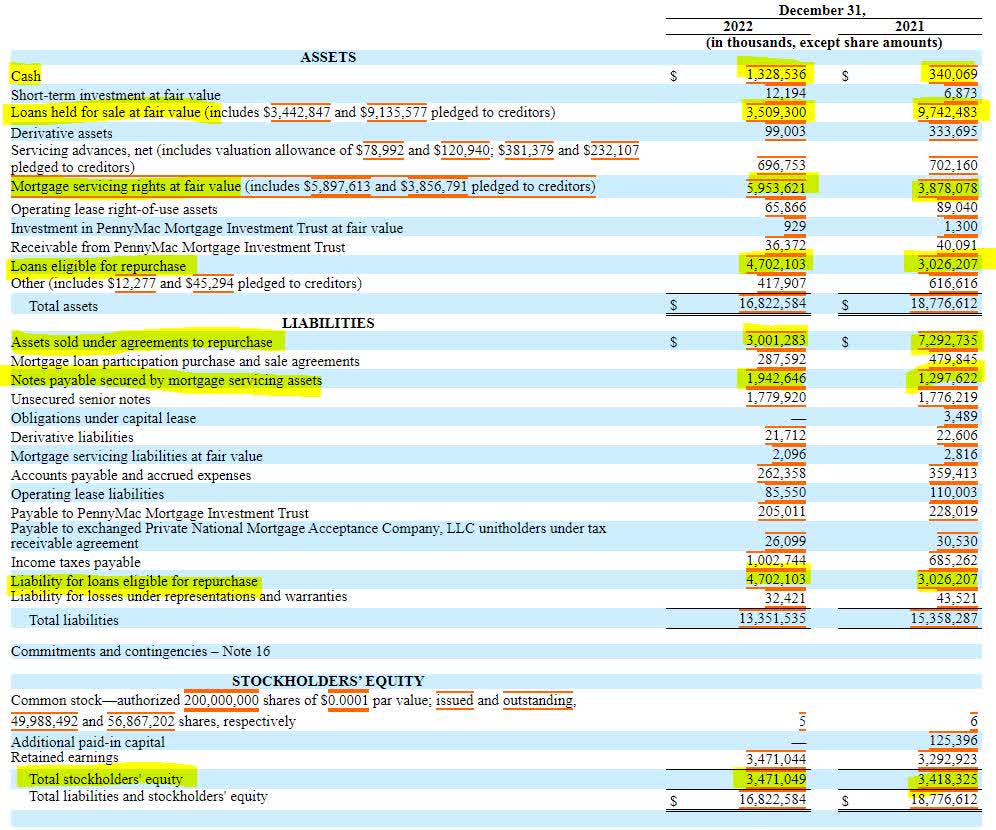

PennyMac’s balance sheet went through a transformation as the industry faced higher interest rates in 2022. The company sold off a large swath of loans and since mortgage demand declined, the company shifted that cash towards mortgage servicing rights. The company’s repurchase liabilities fell from $7.2 to $3 billion as those liabilities are typically collateralized against loans. The company did increase notes payable borrowing to help cover the growth in mortgage servicing rights. Despite the shifting around of the balance sheet and the volatility in the industry, PennyMac’s shareholder equity increased slightly to just under $3.5 billion and they were able to build their cash balance to over $1.3 billion.

{kind=link}

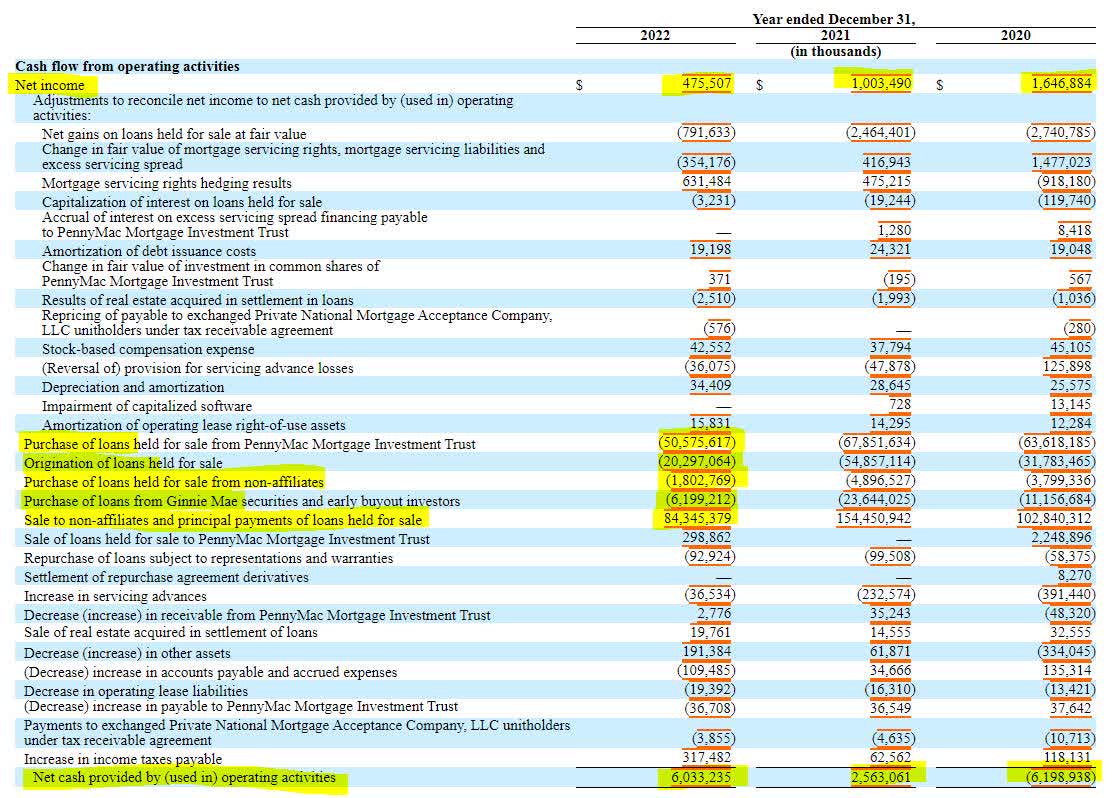

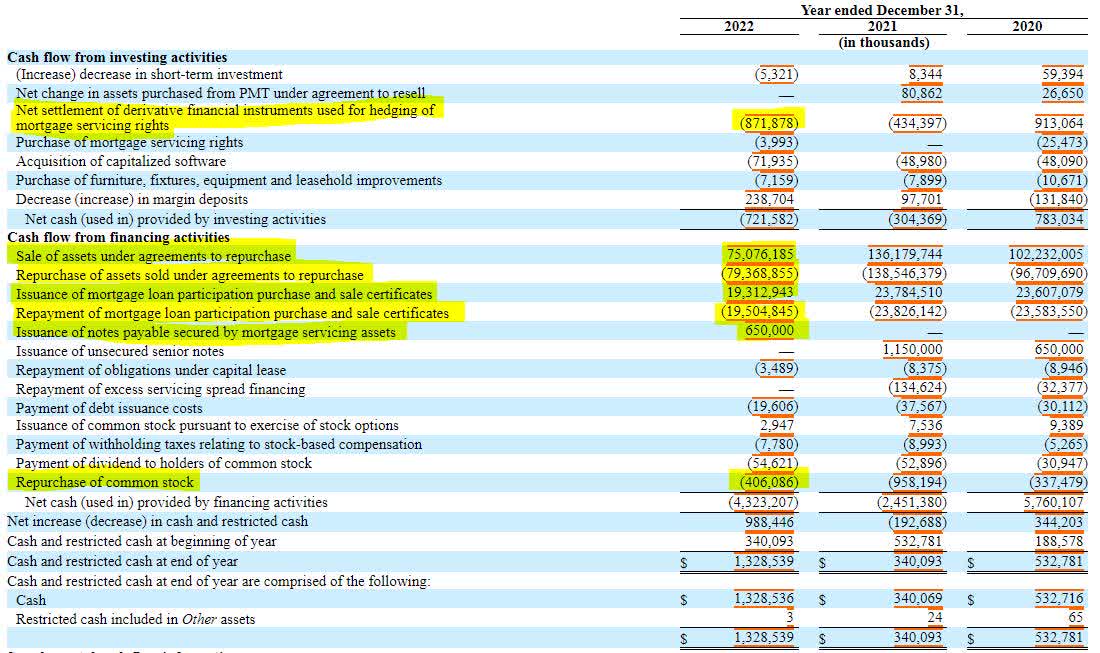

PennyMac’s cash flow sheds a similar light as the balance sheet on the company’s activities. As loans were sold and principal payments were made, the company did not re-invest dollar for dollar, which led to $6 billion in cash flow from operations. Of the $6 billion generated from operations, $4 billion was used to pay down repurchase agreements, $1 billion was used to hedge mortgage servicing rights with derivatives, and the last billion was retained in cash. Should PennyMac find its cash flow constrained, it can reduce its share buybacks or common share dividends before touching preferred share dividends, freeing up over $400 million in cash flow.

{kind=link}

{kind=link}

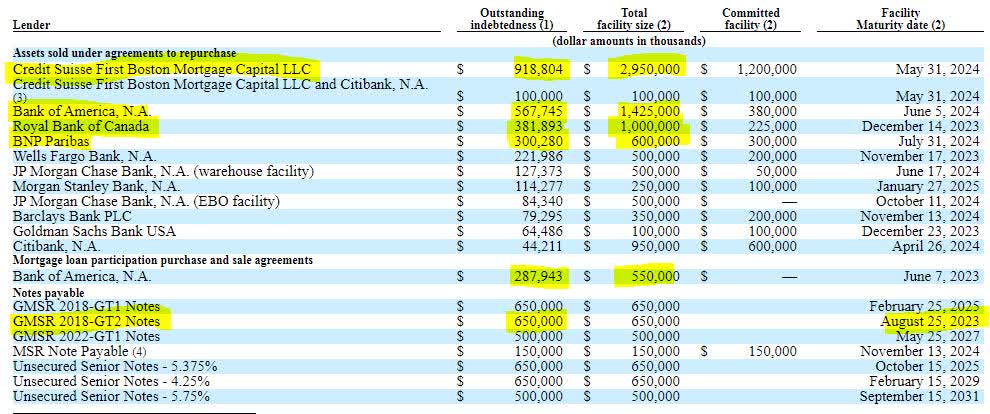

PennyMac is also sitting in a great position should interest rates fall and real estate/mortgage demand bounce back. The company has over $4 billion in additional borrowing capacity under its repurchase agreements. The company’s cash on hand is also enough to pay down its 2023 and 2024 notes should it opt not to seek additional financing.

{kind=link}

While PennyMac's diversification strategy is helpful, the company does face risks to its mortgage servicing if default rates were to rise. While many mortgages are insured by GSEs, mortgage servicers sometimes have to step in and provide advance cash flows when a default occurs. They also do not receive revenue for servicing a defaulted mortgage. If higher defaults put stress on the cash flow of mortgage servicing, it’s important to note that more than $400 million in stock buybacks and common share dividends can go away and help finance the $5.9 billion in mortgage servicing without impacting preferred shares.

PennyMac also has two short term debt offerings that are publicly traded with yields of greater than 10%. This can be an option for investors seeking greater safety, but the returns are shorter in duration and I have been unable to find the prospectus of the bonds (so I cannot verify if they are convertible) and some brokerages do not carry this bond.

{kind=link}

Either way, PennyMac’s proactive shift in the face of changes in the mortgage market leave me confident the preferred shares will remain a good option for income investors.

For further details see:

PennyMac C Series Preferred Yielding Over 9.7%