PMT - PennyMac Mortgage Investment Trust: This 11% Yielding mREIT May Cut Its Dividend Soon

2023-12-07 14:45:54 ET

Summary

- PennyMac Mortgage Investment Trust has significant investments in Mortgage Servicing Rights but has a weak long-term track record in book value and recently cut its dividend.

- PMT may face another dividend cut in 2023 as it has paid out more in dividends than it has produced in income.

- With the potential for the central bank to change its interest rate policy next year, PMT is not an attractive investment for passive income investors.

PennyMac Mortgage Investment Trust ( PMT ) is a mortgage Real Estate Investment Trust that runs a number of credit- and interest-rate sensitive strategies that include the investment in Mortgage Servicing Rights (MSRs).

Though Pennymac Mortgage Investment Trust has considerable investments in MSRs, the mortgage trust does not have a strong long-term track record in book value and has just last year slashed its dividend by 15%.

In 2023, the trust has paid out in dividends than it produced in income, making another dividend cut probable. With the central bank also likely set to change its interest rate policy next year, I think that PennyMac Mortgage Investment Trust is not an attractive investment for passive income investors.

Portfolio And MSR Exposure

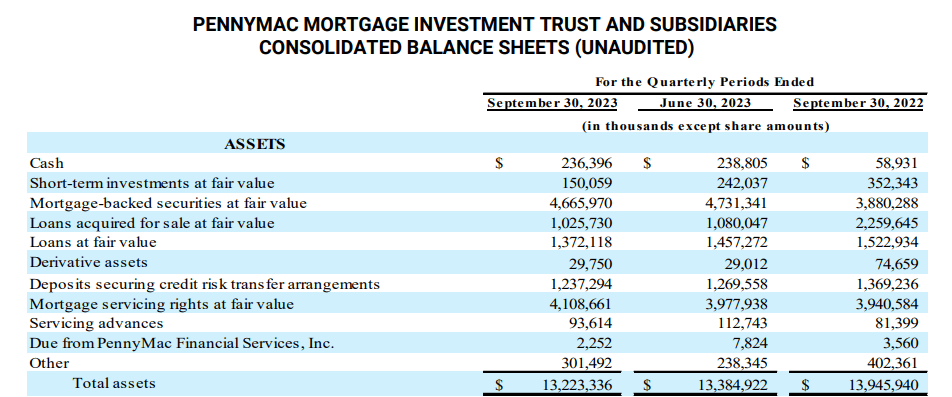

PennyMac Mortgage Investment Trust primarily invests in residential mortgage loans and mortgage-related assets, including MSRs. The three biggest assets on the mortgage trust's balance sheet at the end of the third quarter were mortgage-backed securities, MSRs, and residential mortgage loans.

Mortgage Servicing Rights Exposure (PennyMac Mortgage Investment Trust)

{kind=link}

MSRs are unique assets for mREITs because they are interest-sensitive assets that increase in value when interest rates rise. Contrary to mortgage-backed securities, for instance, the values of MSRs increase during high-rate environments and decrease during low-rate environments.

However, due to the fact that inflation is moderating , a fact that I have discussed a number of times lately, chances are the central bank will start to slash key interest rates next year, thereby making MSRs less attractive as investment vehicles for mortgage Real Estate Investment Trusts.

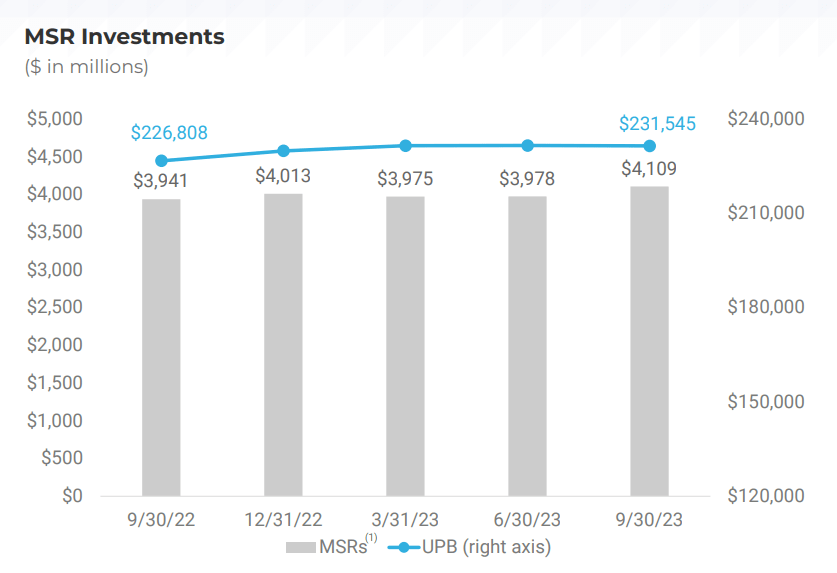

PennyMac Mortgage Investment Trust owned $4.1 billion worth of MSRs at the end of the third quarter, reflecting an increase of $169 million compared to last year's third quarter. MSRs were the second-largest investment category after mortgage-backed securities.

Mortgage Servicing Rights Investments (PennyMac Mortgage Investment Trust)

{kind=link}

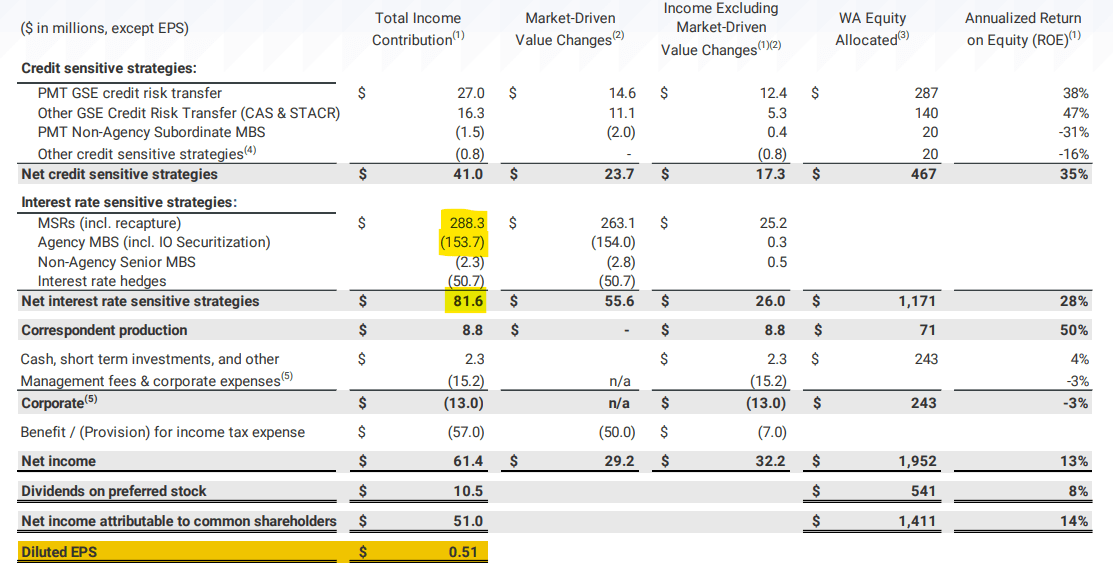

Though the mortgage Real Estate Investment Trust also owns agency mortgage-backed securities and buys, sells, and securitizes prime credit quality loans, MSRs made by far the largest income contribution to PennyMac Mortgage Investment Trust in the third quarter.

MSRs produced $288.3 million in total income, which was primarily due to fair value changes. Agency MBS, whose values suffer when interest rates rise and spreads widen, offset some of those gains.

Mortgage-Backed Securities (PennyMac Mortgage Investment Trust)

{kind=link}

Set For A Dividend Cut

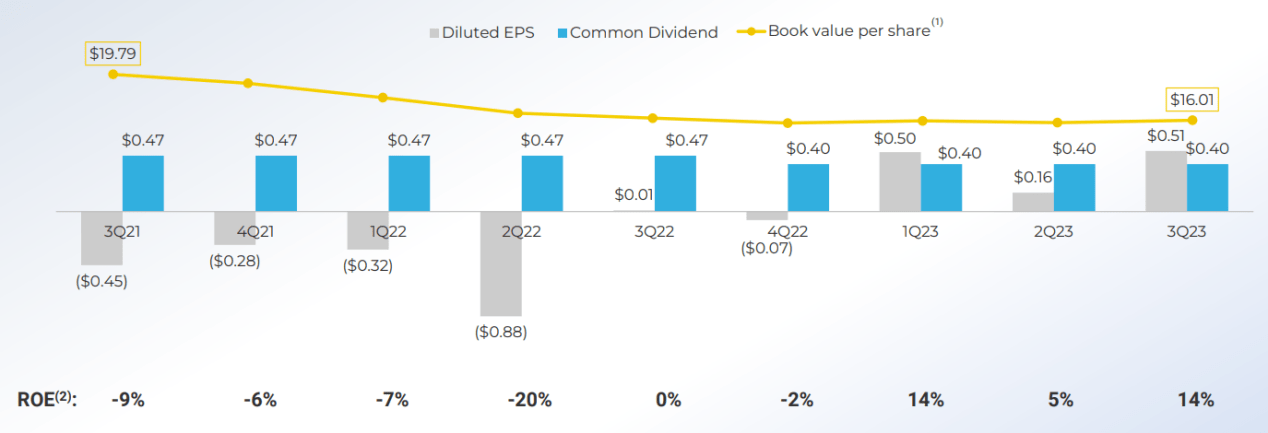

PennyMac Mortgage Investment Trust earned $0.51 per share in diluted earnings per share in the third quarter, and thus, managed to cover its dividend of $0.40 per share (implied dividend coverage ratio: 128%).

However, the trend so far in 2023 is not too convincing, and the trust has a record of slashing its dividend payout. In December 2022, PennyMac Mortgage Investment Trust cut its dividend by 15% from $0.47 per share to $0.40 per share due to an underwhelming performance of its mortgage-backed securities in a rising-rate environment.

Year-to-date, PennyMac Mortgage Investment Trust earned $1.17 per share in net income and paid out a total of $1.20 per share in dividends, which means the dividend coverage ratio for the first nine months of the year dropped below 100% to just 98%. In short: PennyMac Mortgage Investment Trust might be set for yet another dividend decrease in the short term.

Unattractive Long-Term History Of Book Value Growth

The long-term history of PennyMac Mortgage Investment Trust's book value growth is less than compelling. The mREIT's book value declined rather consistently in the last eight quarters, and management reported, despite substantial MSRs exposure, only three quarters of positive returns on equity.

PennyMac Mortgage Investment Trust's book value slumped from $19.79 per share in 3Q-21 to $16.01 per share in 3Q-23, which reflects a substantial decline of 19%.

Book Value Per Share (PennyMac Mortgage Investment Trust)

{kind=link}

PennyMac Mortgage Investment Trust is presently selling at a 10% discount to book value whereas Rithm Capital Corp. ( RITM ) is selling at a 15% discount to book value despite being bigger, more diversified, and offering passive income investors a much higher margin of dividend safety.

MSR Risks

PennyMac Mortgage Investment Trust is set to see higher earnings from its mortgage-backed security portfolio and lower earnings from its MSRs investments in a lower-rate environment. The trust owns both kinds of mortgage assets, though the mREIT overall remains a positive net exposure to rising interest rates.

Taking into account that inflation is moderating, MSRs might not be great assets to be invested in, particularly not if the central bank starts to slash key interest rates next year. As such, MSRs assets pose a considerable risk with regard to negative fair value changes for PennyMac Mortgage Investment Trust.

My Conclusion

PennyMac Mortgage Investment Trust's 11% yield is not something that I would fall over myself to buy. Though investments in MSRs are promising in a rising-rate environment, the recently reported decline in inflation strongly tilts the odds in favor of falling key interest rates next year, which will make MSRs much less attractive from an investment point of view.

The mortgage Real Estate Investment Trust does own other mortgage assets like mortgage-backed securities, which would profit from a narrowing of MBS spreads and lower interest rates.

With that being said, however, the mREIT does not have a particularly convincing long-term record in growing its book value, and it achieved only three quarters of positive returns on equity in the last eight quarters, which I am afraid is just not good enough to convince me to buy.

For now, I am staying with Rithm Capital, which offers passive income investors a much more diversified investment portfolio, strong dividend coverage, and a larger discount to book value.

For further details see:

PennyMac Mortgage Investment Trust: This 11% Yielding mREIT May Cut Its Dividend Soon