PNR - Pentair: Fairly Valued After A Strong Rally Better EPS Growth Seen In 2024

2023-07-06 12:26:22 ET

Summary

- UK stocks have underperformed compared to the S&P 500 in recent months, but London-based water treatment company Pentair has bucked the trend.

- Pentair's Q1 results beat estimates, with operating EPS of $0.91 beating consensus by $0.14 and revenue rising 3% YoY to $1.03 billion due to supply chain improvements and consumer trends.

- Despite a hold rating on Pentair due to potential macro-level risks, the company's forward earnings growth is robust and its valuation appears fair, with a potential for consolidation of first-half gains.

- I gameplan key price levels to watch ahead of its early August Q2 earnings report.

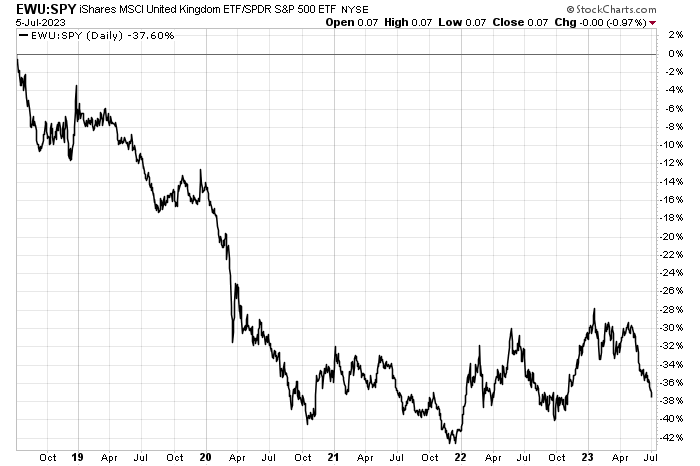

UK stocks posted strong relative returns compared to the S&P 500 from Q4 2022 through early this year. That alpha was short-lived, however. The last two months have seen dreadful performance out of the iShares MSCI United Kingdom ETF ( EWU ) compared to SPY. One London company has bucked the trend lately.

After a robust rally in the last 9 months, I have a hold rating on Pentair ( PNR ) for both fundamental and technical reasons.

UK Stocks Suffer Compared to the S&P 500 In Q2

{kind=link}

According to Bank of America Global Research, PNR is a residential and commercial pure-play water treatment company. Pentair generated $4.1bn of revenue in 2022 from its two segments: Consumer Solutions (residential pool and water filtration, 66% of segment adjusted income) and Industrial and Flow Technologies (industrial filtration, irrigation, and commercial pumps, 34% of segment adjusted income).

The London-based Industrial Machinery & Supplies & Components industry company within the Industrials sector trades at a high 21.2 trailing 12-month GAAP price-to-earnings ratio and pays a low 1.4% dividend yield, according to Seeking Alpha. Implied volatility is low at 23% and short interest is low at 2.4%.

Back in April , Pentair beat on both its Q1 top and bottom-line estimates and provided key updates to this FY 2023 outlook. $0.91 of operating EPS beat the consensus handily by $0.14 while revenue rose a modest 3% YoY to $1.03 billion. Stronger operating profits were the result of supply chain improvements and solid execution from the management team.

Still, a key risk for this consumer-sensitive business is what happens in the coming months at the macro level. Slowing residential and commercial construction demand could be in the works, but that risk keeps getting pushed out, hence the strong share price performance this year. Spending on pools, though, has been softening and the credit markets are showing some signs of cracking via corporate defaults.

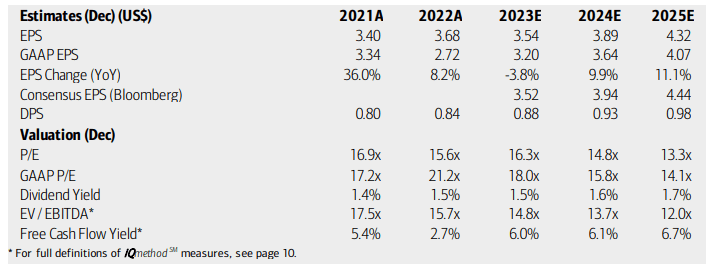

On the bright side, guidance was increased during the Q1 update, full-year 2023 GAAP EPS is now seen at around $3.25 to $3.35 and on an adjusted basis to approximately the $3.60 to $3.70 range compared to the consensus estimate of $3.57.

On valuation, analysts at BofA see earnings falling about 4% in 2023 while per-share profits are seen rising in the out year through 2025. The Bloomberg consensus forecast is slightly more sanguine compared to what BofA projects. Dividends, meanwhile, are seen as climbing at a steady pace over the coming quarters.

Considering near double-digit earnings growth ahead, and the current trough earnings figure, a 17 forward operating P/E is somewhat attractive at a high level. Digging further, we find that the company trades with an EV/EBITDA ratio near that of the S&P 500 (higher than the UK market's) while the free cash flow yield is solid at better than 6% on a forward basis.

Pentair: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

{kind=link}

The current non-GAAP estimated earnings multiple is on par with the sector median and priced very close to PNR's long-term average. On a dividend yield basis, the stock is a touch to the expensive side. Other valuation metrics suggest the company leans to the expensive side.

But if we use the PEG ratio, assuming a 17 P/E today and a normalized 10% EPS growth ahead, then we are talking about 1.7 figure, which is not too pricey, but no bargain either. Assuming per-share profits of $3.80 over the next four quarters and using a 17 P/E, the stock should be near $64, so I am a hold on valuation. If PNR can achieve $4.35 of EPS by 2024, then the stock could be valued in the low to mid-$70s come later next year.

PNR: Some Expensive Valuation Metrics

Seeking Alpha

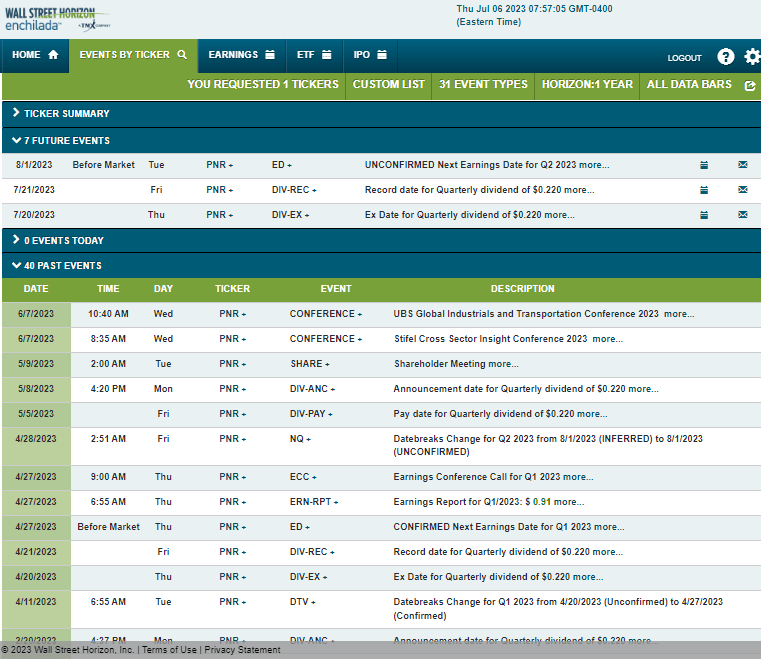

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2023 earnings date of Tuesday, August 1 BMO. Before that, shares trade ex-dividend on Thursday, July 20.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

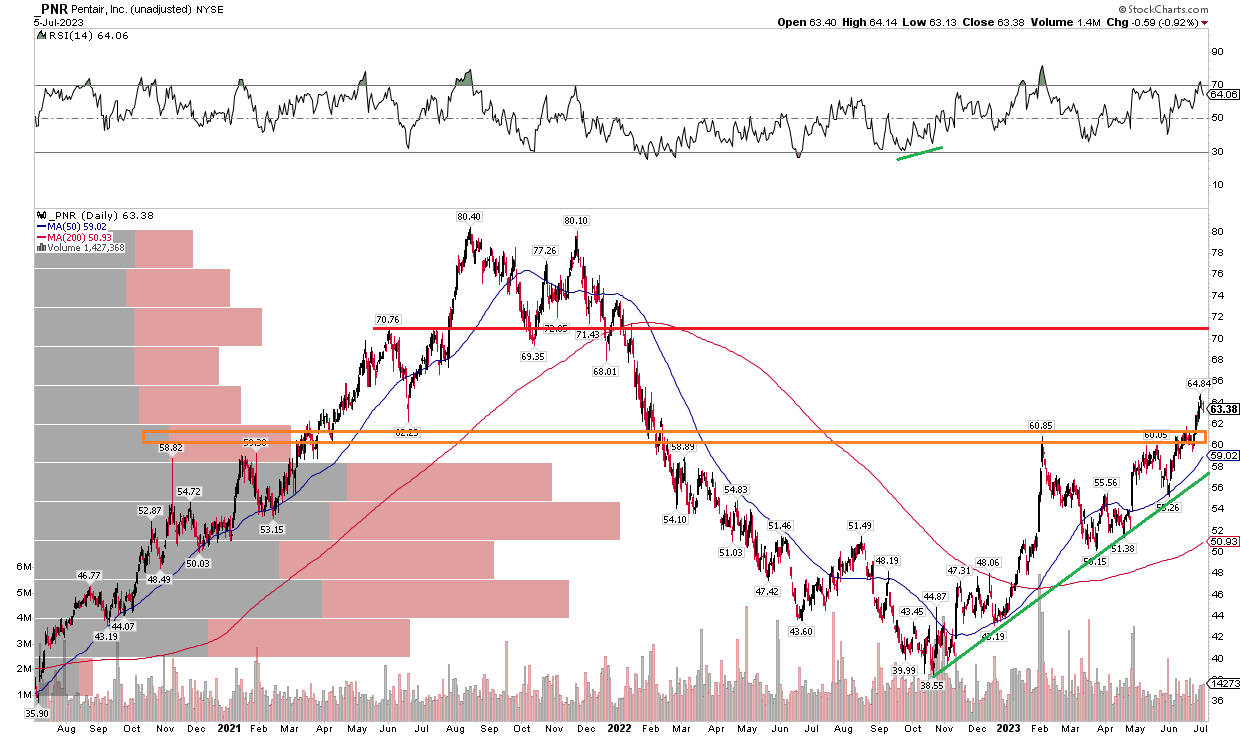

With PNR near its intrinsic value in my view, the chart is slightly more optimistic. Notice in the graph below that the stock has broken through what had been resistance in the $59 to $62 range. I see the possible layer of selling pressure at its second-half of 2021 range lows between $68 and $70. Investors who bought in during that time may look to sell at their breakeven price from a behavioral perspective. So, we are in a bit of a no-man's land here in the mid-$60s.

What's positive from a bullish take, though, is that the long-term 200-day moving average is upward-sloped, indicating that the bulls are in charge. Moreover, there is ample volume by price starting at the $59 price point and lower from there, so any pullbacks should have some cushion. Lastly, PNR has been holding an uptrend support line from the October 2022 low below $40 nicely.

Overall, it has been a stout run for the Industrials sector stock, but we may see a consolidation here without a ton of downside risk. So, it is a hold on the chart too.

PNR: Strong 9-Month Uptrend, Nearing Resistance

{kind=link}

The Bottom Line

I have a hold rating on Pentair. The valuation appears fair in my view while forward earnings growth is robust. The chart is likewise impressive, but some consolidation of first-half gains could be in the cards.

For further details see:

Pentair: Fairly Valued After A Strong Rally, Better EPS Growth Seen In 2024