PNR - Pentair Is A Good Buy Post Recent Decline

2023-10-26 13:59:27 ET

Summary

- Pentair's sales declined in Q3 2023 due to headwinds in its pool business, but other segments saw growth.

- I expect PNR's pool business to return to growth in FY24, supported by easing comparisons and inventory destocking ending.

- Pentair's margin outlook is also positive and valuations are reasonable.

Investment Thesis

Pentair plc ( PNR ) recently reported better-than-expected results with both sales and EPS beating sell-side estimates. While the stock has been under pressure in recent months due to a slowdown in pool segment sales due to macroeconomic headwinds, the company is executing really well and has been able to post margin improvements last quarter despite of sales declines.

Looking forward, FY23 should mark the bottom for the company sales and we should see a return to growth from FY24 onwards as inventory destocking ends in the pool business, IIJA funding helps IFT business, and the company sees easing comparisons. The company's margin prospects also look good with management working on price increases and cost-saving initiatives. The company's good growth prospects coupled with reasonable valuations make it a good buy.

Revenue Analysis and Outlook

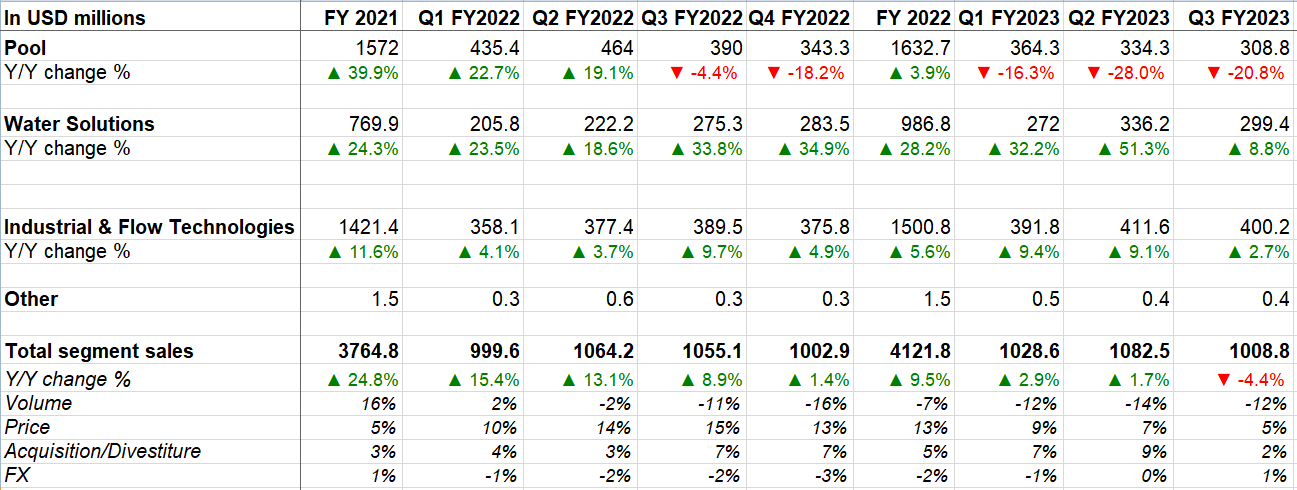

After seeing good growth over the last couple of years, the company’s sales turned negative in the last quarter due to continued headwinds in its pool business.

In the third quarter of 2023, the company’s Industrial & Flow Technologies (IFT) segment’s sales grew 2.7% Y/Y to $400.2 million attributed to a 1.1% Y/Y increase in core sales driven by commercial sales growth of 8% and industrial sales growth of 12% which more than offset a decline in residential sales of 7%.

The Water Solutions segment’s sales increased 8.8% Y/Y to $299.4 million driven by gains from the Manitowoc Ice acquisition and price increases. Excluding currency translation, acquisitions, and divestitures, core sales were flat Y/Y as the higher sales volume in the commercial business was offset by lower sales volume in the residential business.

In the Pool segment, sales declined 20.8% Y/Y to $308.8 million attributed to a volume decline of 28.1% caused by continued channel inventory reductions, partially offset by a Y/Y pricing benefit of 7.3%.

On a consolidated basis, lower sales volume in the Pool segment more than offset the increased sales volume in the IFT and Water Solutions segments and resulted in a 4.4% decline in net sales to $1,008.8 million with a 7.3% decline in core sales.

PNR’s Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Moving forward, while FY23 has been a tough year for the company’s Pool business, this business should return to growth in FY24. On its last earnings call , management noted that while Q3 sales declined primarily due to the volume headwind in the Pool business, the negative volume impact on Pentair and Pool improved sequentially from Q2 indicating the worst is behind us. What happened over the last few years is that consumers were spending a lot of time at home due to the lockdown and spending quite a bit on home improvement. This significantly increased demand for new pool construction sales in FY21 and FY22. As the economy started opening up, this demand began normalizing which negatively impacted the company’s pool sales in FY23. In addition, there was a good deal of channel inventory destocking at the company’s distributors which further exacerbated this decline. So, FY23 was a year of normalization as well as inventory destocking for the company’s pool business.

I expect destocking to be completed by the end of FY23 as distributor inventory levels align with the end market demand. So, this should be one less headwind going into FY24.

Further, the large number of new pools built during the COVID-19 lockdown period has resulted in a good increase in the installed base, and they are going to help the company’s repair and replacement demand in the coming years. A pump replacement is somewhat non-discretionary in nature - if a pump breaks, it has to be fixed. So, repair and replacement demand is expected to be relatively stable despite macro uncertainty. Around 60% of the company’s pool business comes from repair and replacement, 20% from major remodels, and 20% from new construction. Even without a meaningful uptick in new construction, inventory destocking ending and strength in repair and replacement should help the company grow its pool business sales in FY24.

On the IFT side, the company’s business is poised to benefit from Infrastructure Investments and Jobs Act (IIJA) funding which is expected to help the company’s fire suppression, wastewater, and flood control business. The demand in this business has continued to remain resilient and I expect further acceleration moving forward as municipalities continue to deploy funding under IIJA.

For IFT business, the company is also benefiting from a revised go-to-market strategy where it is moving away from project-led business to standardized solutions which is increasing ease of doing business with distributors.

In the Water Solutions segment, the company has also done a good job in terms of integrating the Manitowoc acquisition which, according to management, is exceeding expectations and I believe the near-term focus in this business would be to continue integrating Manitowoc and realize synergy benefits.

If we examine the sales performance from the previous year, the company experienced a significant deceleration in sales growth, which began in Q4 of the previous year. This slowdown in sales was particularly pronounced in the Pool segment, with a notable 18.2% year-over-year decline in Q4 FY22 compared to a 4.4% year-over-year decline in Q3 FY22. As a result, the company's sales growth rate decreased from 8.9% year-over-year growth in Q3 FY22 to 1.4% year-over-year growth in Q4 FY22. Therefore, the comparisons are easing from the current quarter onwards, which should also help sales growth.

So, overall if we look at easing comps, the pool business bottoming in FY23, benefits from IIJA funding for the IFT business, and the Manitowoc integration exceeding expectations, the overall growth outlook is positive and I believe the company should return to growth in FY24.

Margin Analysis and Outlook

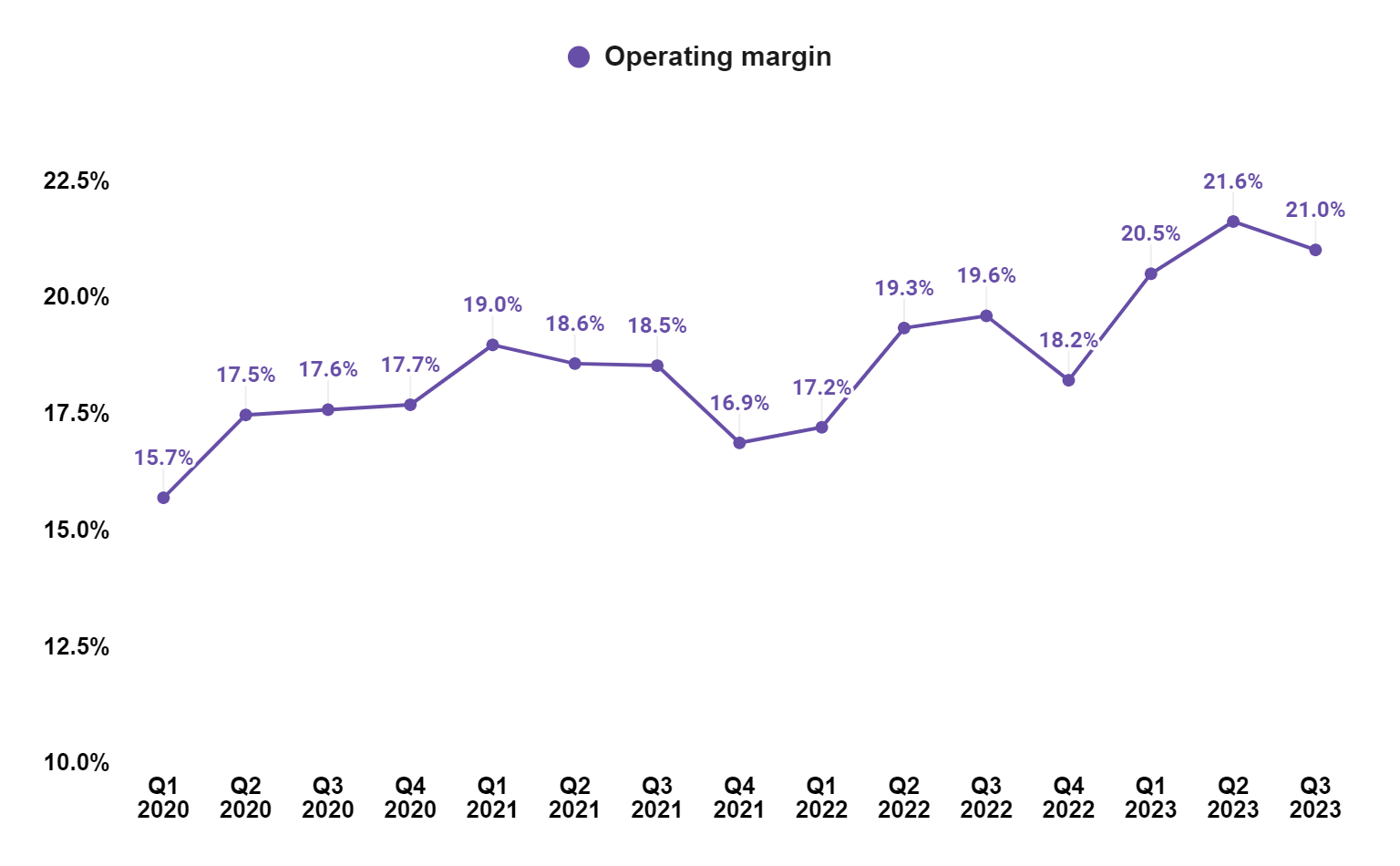

In Q3 2023, the company’s operating margin expanded by 140 bps Y/Y to 21% driven by higher pricing, productivity gains, and contribution from the acquisition of Manitowoc Ice which outweighed the inflationary cost increases related to labor costs and raw materials.

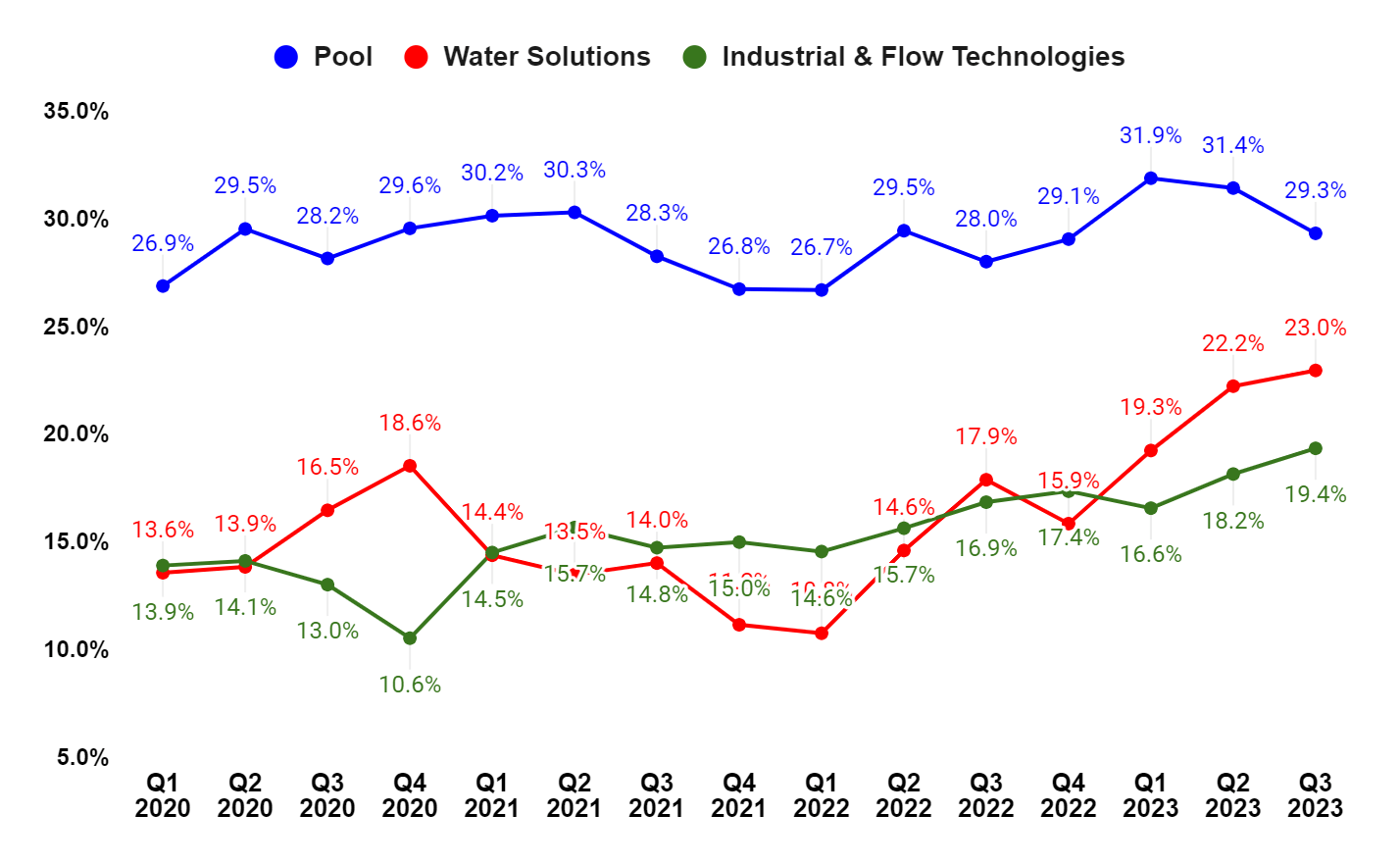

Segment Wise, IFT margin improved by 250 bps Y/Y helped by increased productivity due to manufacturing leverage and transformation initiatives and higher pricing. The Water Solutions’ operating margin increased by 510 bps Y/Y attributed to the contribution from the Manitowoc Ice acquisition and productivity gains in the residential business as a result of transformation and restructuring initiatives. Despite the decline in net sales, the Pool segment’s margin expanded by 130 bps Y/Y due to benefits from pricing actions and improved productivity driven by transformation initiatives. The margin expansion across all of its business segments drove a Y/Y increase in total operating margin for the company.

PNR’s Operating margin (Company Data, GS Analytics Research)

{kind=link}

PNR’s Segment Wise Operating margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I expect continued good execution by management on transformation initiatives which include price increases, strategic sourcing, operations excellence, and organizational effectiveness. This should help the company’s margins. The fact that the company was able to post a Y/Y increase in pool segment margins despite a sharp decline in sales is a testament that management cost reduction initiatives are working really well.

Once the sales bottom in FY23 and resume growth in FY24, the company’s margins should also benefit from operating leverage. Management has given a target of reaching 23% operating margins by the end of FY25 which indicates a meaningful upside from the current levels. So, I am optimistic about the company’s margin growth prospects.

Valuation and Conclusion

PNR is currently trading at a 15.33x FY23 consensus EPS estimate of $3.74 and a 13.60x FY24 consensus EPS estimate of $4.22, which is at a discount versus the company’s average forward P/E of 17.50x over the last 5 years.

While the sales decline in the Pool segment has disappointed investors this year leading to a low valuation, this business is likely to return to growth next year which should help improve sentiments and the stock's valuation can see a potential re-rating. The company is doing a good job in terms of improving margins and there is a further scope of improvement if we go by management targets. The valuation is also low indicating most of the headwinds related to the slowdown in the pool business are likely getting reflected in the stock price at the current valuations limiting the downside risk. Given the company's good growth and margin expansion prospects, along with low valuations, I have a buy rating on the stock.

For further details see:

Pentair Is A Good Buy Post Recent Decline