PNR - Pentair: Nearly Fairly Valued Following Earnings

Summary

- Pentair offers a range of water-based solutions, most notably to the pool industry.

- Despite mixed results, shares rallied higher following their earnings release, and they are now up 22% YTD.

- Contributing to the YTD outperformance has improved sentiment on Wall Street, resulting in higher price targets.

- The company is also seen expanding margins in future periods via their transformative initiative. While this certainly is a positive, it may not be enough to push the stock materially higher from current trading levels.

- While Pentair makes for a solid long-term holding, investors may find better opportunities elsewhere.

Pentair ( PNR ) is a Dividend Aristocrat with 47 years of consecutive increases. Their business revolves around a range of water-based solutions, with a particular emphasis on the pool industry.

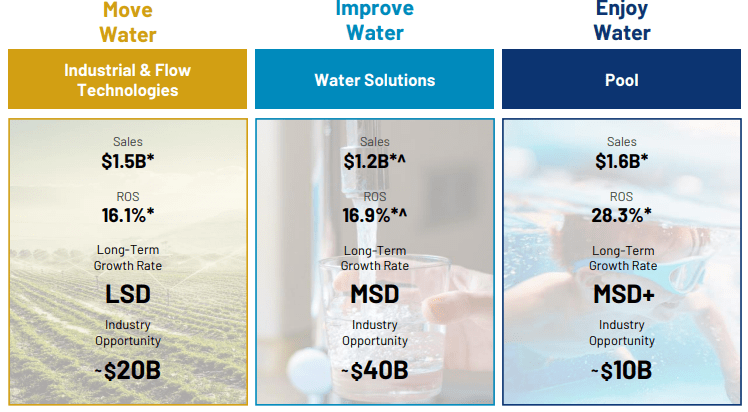

As of 2023 following a realignment in segment presentation , the company operates in three business segments: Industrial & Flow Technologies ("IFT"); Water Solutions; and Pool. Together, the three segments contributed to total consolidated sales of +$4.1B in fiscal 2022.

Q4FY22 Investor Presentation - Segment Disaggregation

{kind=link}

While the pool industry may instill concerns among some due to its discretionary nature, it's important to note that just 20% of the industry pertains to the sale of pools. The rest is largely attributable to repairs and maintenance. And on this, 75% of PNR's products are replacement-based with over 75K trade partners.

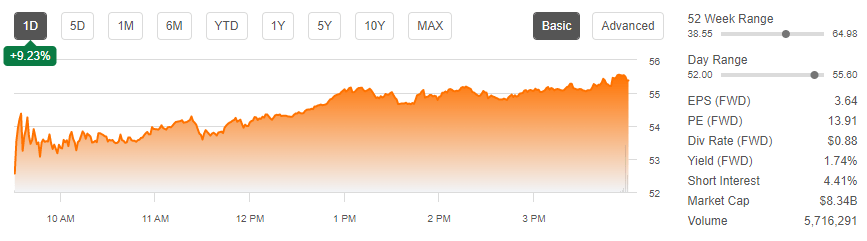

The emphasis on replacements ensures stability and predictability in their recurring cash flows and results of operations. While the demand environment did soften in the current year, this was due in part to challenging comparatives to the prior year. And despite the challenging environment, the company still ended the year strong with better-than-expected results. This sent shares higher by 9% on the day of the release.

Seeking Alpha - Basic Trading Data Of PNR

{kind=link}

While there is some upside left in the stock, it may not be enough to appease most investors. Though the outlook is promising, better opportunities exist elsewhere.

Q4 FY22 Earnings Recap

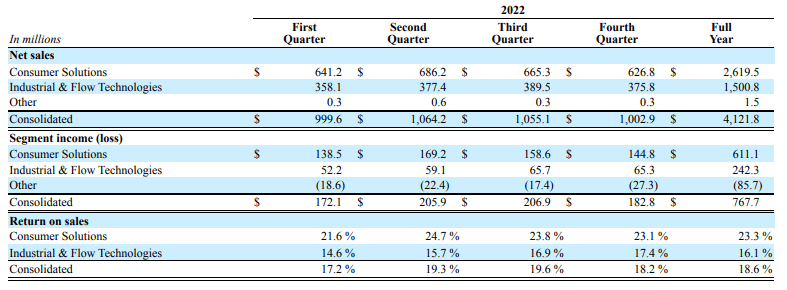

PNR's reported net sales in Q4FY22 came in at +$1.0B. This was up 1.4% YOY and about +$6.0M better than expected . Core sales, however, which exclude the impacts of currency fluctuations and the effects of recent acquisitions, were down 3%, as volume declines more than offset a favorable pricing environment.

Q4FY22 Earnings Release - Summary Of Operating Performance By Quarter

{kind=link}

Driving core sales down was their Consumer Solutions segment, which was down 11% on 26 points of volume decline, offset by 15 points of price contribution. Contributing to the weakness was a difficult comparative environment, in addition to inventory normalization across many of their product lines in their residential channels.

While the segment's core sales were down for the quarter, they were still up 4% for the year. In addition, during the quarter, segment income grew 7% and return on sales ("ROS") bumped higher by 150 basis points ("bps") to 23.1%.

Though income growth in the segment contributed favorably to full year growth of 10%, the improvement in ROS during the quarter was not enough to turn the metric positive for the year, as it was still down 40bps YOY.

Offsetting weakness in their Consumer segment was their IFT segment, which was up 5% during the quarter and 11% on a core basis. Furthermore, segment income grew 21% and ROS expanded to 17.4%. This is up 240bp. It also represents the second consecutive quarter of greater than 200bps improvement.

On the year, IFT was up 6%, with core up 10%. This resulted in full year segment income growth of 14% and ROS of 16.1%, a 110bps improvement YOY. Within the segment, the company realized strong sales growth contribution from industrial solutions, which posted 10% growth. This was supplemented by more modest growth of 3% and 6% in their residential and commercial flow units, respectively.

All considered, adjusted EPS came in at $0.82/share for the quarter. While this was down 6% compared to last year, it still exceeded guidance for the quarter.

Overall, PNR ended fiscal 2022 with full year growth in sales and segment income of 9% and 12%, respectively. This contributed to a 40bps expansion in ROS and an overall 8% increase in adjusted EPS.

And looking ahead, management detailed their transformative initiative, which is intended to drive ROS from 18.6% at present to approximately 23% in fiscal 2025. The over 400bps of margin expansion is up from the 300bps discussed at their investor day.

Driving these improvements is the focus on material costs, which represent 40% of their sales. In addition, the company is expecting to realize value through supply base reduction and inventory solutions, with an emphasis on lean processes across all their operations.

More immediately, total sales are expected to come in flat to up 1% in Q1FY23 and in the range of up 1% to down 3% for the full year. This is paired with expected segment income growth in the upper-single digits for both the quarter and the year. Overall, this would translate to adjusted EPS of approximately $3.50 to $3.70/share. This would be down 5% on the low end and 1% on the upper.

Q4FY22 Investor Presentation - FY23 Guidance

Post-Earnings Insights

Analysts at Stifel recently upgraded their view on PNR with a higher price target, citing the probable end to a challenging operating year with difficult comparatives to a prior year period that included an elevated degree of demand pull forward.

This demand disparity could be seen in Q4 results, which included an 11% decline in core Consumer sales on a 26-point decline in volumes. Additionally, management did acknowledge that 2023 will likely be a catch-up year for the excess demand that was realized from 2020 through the first half of 2022.

Despite softer performance, the company still has favorable tailwinds on their side. For one, 75% of their products are replacement driven. This is paired with a large installed base of approximately 5.4M pools with an average age of 20 to 25 years. Furthermore, just 20% of the industry is new pools. Therefore, demand is likely to be more recurring and predictable even through down business cycles.

This is evidenced by their strong free cash flow growth over the past five years. In this timeframe, they've generated +$2.0B in free cash flow on 8% compound growth in revenues. And looking at 2023, PNR is likely to be in an even better cash flow position due to working capital improvements resulting from a more normalized supply chain.

This should enable them to generate free cash flow growth in line with their historical performance of 100% of net income. And consistent with prior periods, this will lead to further dividend growth. As it is, they've already increased their dividend for 47 consecutive years. And there is minimal conviction that the growth streak is at risk.

Leverage is a bit higher, and this does tie up their capital allocation priorities. They also have a high degree of variable rate exposure, which increases their interest rate risk. But this is offset in part by limited maturities over the new few years.

Probable margin expansion in future periods will also improve their current capital positioning. It is also one of the primary catalysts for future share price appreciation. At present, however, shares trade at about 13.9x forward earnings and near the target levels set by Stifel.

Furthermore, it is only 8% shy of the fair value estimated in a prior analysis . While upside exits, it may not be enough for most investors. Though the outlook is favorable, better opportunities are likely to be found elsewhere.

For further details see:

Pentair: Nearly Fairly Valued Following Earnings