PEN - Penumbra: Future Upside Drivers In Fundamental Sentimental And Valuation Factors

2023-06-22 00:34:20 ET

Summary

- Penumbra, Inc. continues pushing higher, and I have revised my price target of $490.

- The company's fundamental drivers, sentimental factors, and valuation all indicate further value could be obtained.

- PEN is expected to see 25% growth at the top in FY'23, with high sentiment, and thus warrants a reiterated buy rating.

Investment Summary

There is reason to believe the best is still ahead of Penumbra, Inc. ( PEN ). There may be tremendous risk capital yet to be unlocked via the company's operations in my view. This publication will discuss, in extensive detail, why. As a reminder, I have been long PEN since mid-2020.

Since my April publication, shares have clipped another 23% gain, and after meeting my price target of $338 at the time I write– it is time to revise the expectations for the company.

First principles investing looks at the critical facts underpinning a firm's intrinsic valuation, and, therefore, long-term market view of a company. This includes, but is not limited to, 1) fundamental drivers, 2) sentimental drivers, and 3) valuation drivers. All three are intertwined, and for PEN, my estimates suggest that value can be obtained from all categories. Net-net, findings in this analysis corroborate that PEN is a buy in my investment criteria. I have revised the price target to $490mm under these revised expectations.

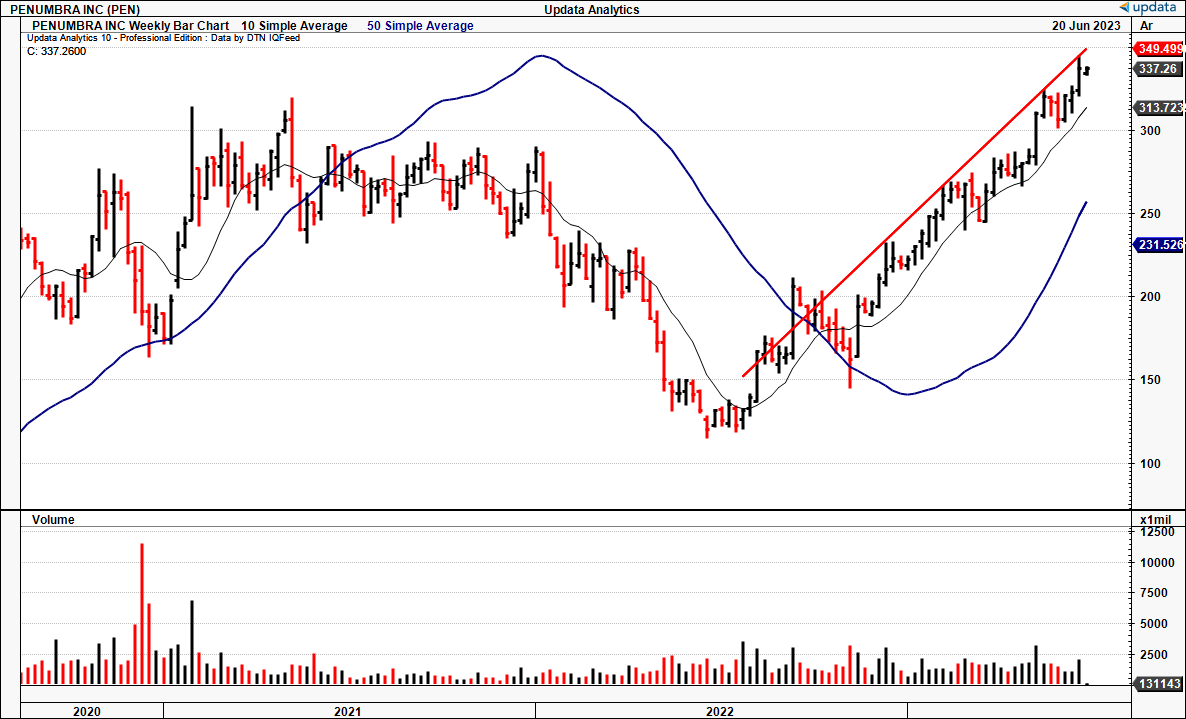

Figure 1. PEN long-term price change, with 2022–'23 rally

{kind=link}

Data: Updata

Critical facts forming PEN investment

In the last publication, I performed a deep dive into the desirable economic characteristics that have seen PEN attract substantial investment over the next 12 months. That is worth a read to understand the company's ability to appreciate capital over the long-term. Whilst the previous analysis sunk right into the "meat and potatoes" of the company's business economics, margins, asset utilization, earnings power, and other asset factors, this report will look at adjacent features. That involves analysis of the fundamental, sentimental and valuation-based factors underpinning the investment thesis.

1. Fundamental drivers to PEN

One of the most cheaply parsed terms in the English language would have to be that of "growth company". My thoughts on labelling a firm this way are simple– show us long-term growth, or you're out. Simple YoY growth percentages, whilst important, do little to convey the actual scale of change, nor what lies ahead.

PEN is a regular member of the growth club, frequenting its luxurious yet expensive lounges since 2017 at least. Looking ahead, top and bottom-line estimates are outstanding and could imply a substantial re-rating if they come to fruition.

Table 1. PEN Forward estimates

{kind=link}

Data: Author, Seeking Alpha

The fundamental outlook can be broken down into the following sub-components:

Q1 FY'23 financials

- Top-line analysis

- PEN clipped total revenues of $241.4 mm in Q1, a YoY increase of 18.4%, in-line with historical rates.

- Growth was underlined by the vascular segment's 16% change, contributing a 16% YoY change in revenue.

- Q1 also saw its Lightning Flash mechanical thrombectomy system's successful launch, which surpassed expectations by management's account. It was labelled on the call as PEN's most important product launch in the company's history.

- Despite facing supply constraints, Lightning Flash was pivotal in driving a 23% YoY growth in PEN's U.S. vascular business in Q1. It also was central to driving the 26% YoY growth in the U.S. vascular thrombectomy sales during the same period.

- Operating Profitability

- The company grew quarterly EBIT of $10.6mm in Q1, ahead of a negative print last year.

- TPEN also booked gross margin at 63.17% of turnover in the TTM, in line with historical range.

Table 2. Q1 FY'2 revenue change drivers

Note: Shows YoY change in revenues (Data: Author, PEN SEC Filings)

Asset factors

Meanwhile, the company has compounded its book value per share from $17.15 in 2020 to $26.79 at the time of writing, a 56% incremental gain in value. This tells me of the company's residual earnings that have been reinvested back into the business to create future value. You see this in the fact that PEN trades at 12.9x its book value, indicating that each $1 investment into the company's net operating assets has created $12.90 in market valuation– tremendous market return on investment.

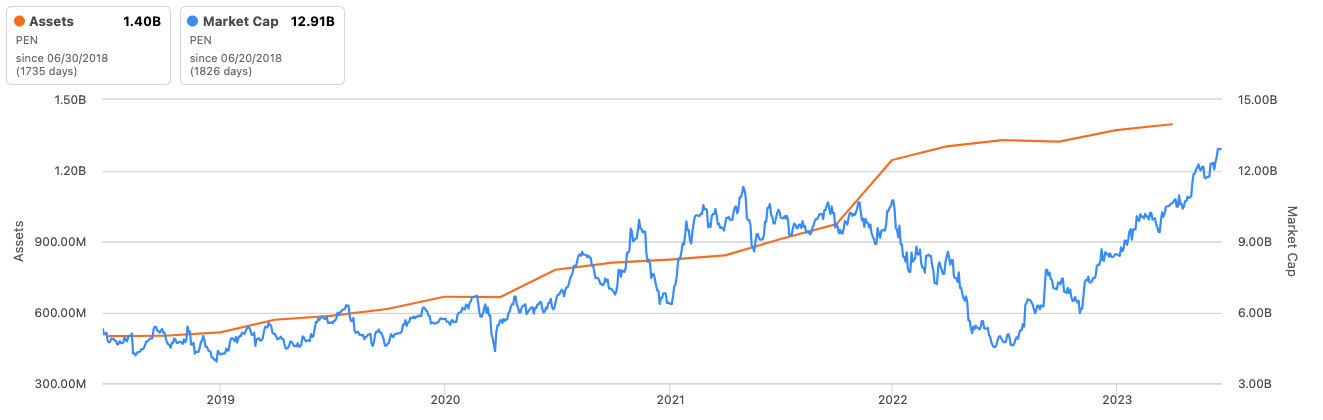

In addition, you can see the company growing fixed and operating assets across the 2019–2023 period (2023 is shown in the TTM), with a tremendous uptick coming into FY'22. Note the latency between the selloff in equity (within the 2022 bear market) and the gradual recovery in market value to a more "fair" value.

Perhaps the reason for the correlation between asset growth to market value is the company's capital productivity. Since 2019, it invested an additional $598.4mm into productive assets to produce an additional $186.9mm in gross profit. Most of the investment was into net working capital, particularly inventory and accounts receivable ($258mm versus $155mm in tangible assets).

That indicates that for every additional $1 of investment PEN made in this time, it produced an additional $0.31 in gross profit over the testing period. From 2021–2023 (using TTM figures) the return was $0.14 on the dollar. Such data is telling on PEN's future earnings power. Should this continue, a 10% increase in net operating assets to $1.25Bn could produce an additional $387mm in gross profit, bringing the figure to $945.9mm, or 69% increase on the TTM figure of $558.9mm.

Figure 2. PEN operating asset growth vs. market valuation

{kind=link}

Data: Seeking Alpha

Whilst this doesn't plot the company's intrinsic value, it does show 1) the incremental investments PEN is making, 2) the markets return on investment on these, hence, the value it places on PEN's investments, and 3) the implied profitability on PEN's capital, as shown by the changes in market value.

Divisional performance

- Vascular

- In Q1, Vascular sales were up to $142.8mm or 16.3% growth on last year. U.S. sales were the takeout with 23% YoY growth.

- However, management spoke of some variability in international distributor region revenue– not that this had a meaningful impact, but worth noting for the next quarter.

- Neuro

- In the neuro business, PEN spiked quarterly revenues by 21.5% to $98.5 mm.

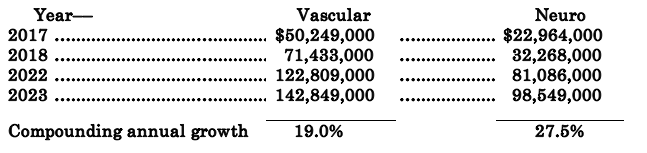

In the theme of analysing long-term growth, you'll note the longer-term performances in corresponding Q1 periods of both the vascular and neuro segments below. Critically, PEN has compounded revenues at an annual rate of 19% and 27.5%, respectively, since 2017.

Table 2. Q1 segment growth at 19% YoY

{kind=link}

Note: All figures showing Q1 in each respective year shown. (Data: Author PEN 10-Q's)

Better outlook on guidance

The firm has revised its FY'23 guidance, given the outlook on core segments such as Lightning Bolt 7, RED 72 with SENDit technology, RED 43, and BnX81. It also aims for a long-term 70% gross margin.

It now expects $1.04Bn–$1.06Bn at the top-line in FY'23, calling for strong YoY growth of 23%–25% in turnover. It looks to have an operating margin of 10% on this.

2. Sentimental factors for price change

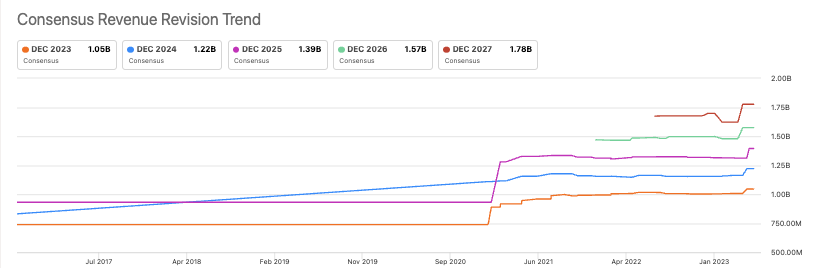

There is clear evidence sentiment is shifting higher for PEN. Investors are piling into the stock and turning more bullish, so that data says.

One, there's been 12 EPS and revenue target changes from analysts over the last 3 months, with no downsides. The market expects exceptional earnings growth this year and 24% growth in turnover, and 17% in FY23. That the sell-side is turning more bullish on the company's growth prospects is critical to see the company trading at higher market values in my view.

Figure 3.

{kind=link}

Data: Seeking Alpha

Two, the bulk of open interest in the PEN options chain, for contracts in the money at June expiry, contracts are centered around calls with a strike price of $420 per share. This tells me investors expect the company to shoot to this mark at least. Meanwhile, put activity is negligible relative to the calls side of the ladder.

Third, despite tremendously high market multiples, investors are paying these prices. With the stock trading above all three moving averages – Key psychological numbers. It is trading above the 50/100/200DMA's and is riding these levels as support. Across all time frames, the price performance is in the green, too, as an indication of the breadth of momentum.

3. Valuation factors

To show you the value the market puts on the capital PEN has at work (including intangibles and net working capital), note the firm trades at~ 13x book value, as previously mentioned. This tells me the company has produced ~$13 in market value for every $1 of net assets the firm has invested– or that investors have rewarded the firm's investments by this multiple. I would consider this valuable information going forward, as mentioned.

The reason is due to the market's consensus. Regarding its expectations, it would appear the market is expecting these kinds of growth figures in the future too. In the last publication, I came to the previous valuation figure with a rigorous discounted cash flow that spun off $338/share. I am now looking for a more aggressive growth rate and would accept bids on PEN shares at $490, considering a ~6% equity charge and a 4% growth rate. The revised numbers form the crux of the reinstated by rating, and could hit another 26% return on investment if they come through.

Figure 4. Sensitivity analysis is taken from the previous PEN publication, note the $489 target with a 4% growth rate and c.6% equity charge.

Data: Author, previous PEN analysis

In short

Net-net, the latest investment findings corroborate a reiterated buy rating on PEN. The company is growing its gross profitability, and the sales ramp is steep going forward. It expects 25% growth at the top in FY'23, putting it in good stead to continue adding market value. Further, sentiment is tremendously high, which is further supported by valuation factors.

This report illustrated the additional factors for investor thinking in the PEN investment debate. Chiefly the fundamental, sentimental and valuation-based elements. Combined with those outlined in the previous analysis, these points form a significant part of the PEN buy thesis. I have revised the price target to $490, another 26% upside potential at the time being. With these points in mind, I reiterate PEN as a buy.

For further details see:

Penumbra: Future Upside Drivers In Fundamental, Sentimental And Valuation Factors