PEBO - Peoples Bancorp: Deposits Are The Key Strength

2023-05-11 16:39:36 ET

Summary

- Peoples Bancorp may perform better than its rivals in 2023.

- The net income margin is definitely high compared to other regional banks.

- The cost of deposits is still very low, almost as if the macroeconomic environment has not changed in the past year.

With a YTD performance of about -14%, Peoples Bancorp ( PEBO ) is significantly underperforming the S&P 500 in this first half of 2023. However, there is positive news: at least it has performed better than many other regional banks.

The turmoil in the banking sector triggered by the failure of Silicon Valley Bank is branching out to other financial institutions, and Peoples Bancorp is no exception.

Based on data from the latest quarterly report from a few weeks ago, in this article, I will analyze this bank's financial situation and its net interest margin in order to understand its future prospects.

Financial situation and profitability

As a first aspect, let's see what the bank's main sources of funding are.

{kind=link}

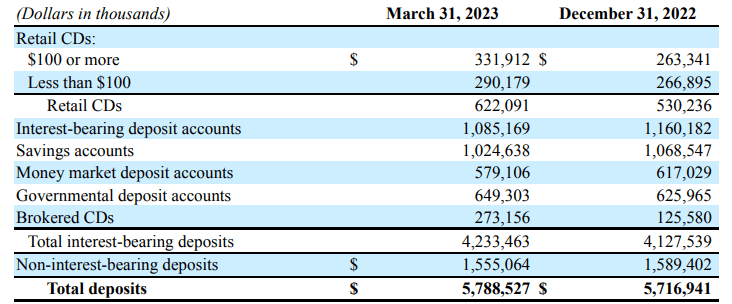

Starting with deposits, the first point to note is that they are up a little from the previous quarter despite the turmoil in March. Non-interest-bearing deposits dropped slightly in favor of Brokered CDs, but overall the situation remains stable and predictable according to the words of CEO Chuck Sulerzyski :

We have had inflated deposits related to COVID, so some of that decline was expected over time. We had outflows of savings and money market balances, but those were nearly offset with an increase in our retailed CDs, as we offered more attractive pricing.

But what has fostered this deposit stability ? There are a number of reasons.

85% of deposits come from rural markets, while only 15% come from urban markets. The Peoples Bancorp team has been educating its clients about FDIC insurance limits and available options so that they remain calm during periods of turbulence such as the current one. In fact, unusual deposit movements were inconsequential. In practice, the bank tried to prevent a bank run by educating customers.

Certainly, the fact that only 32% of deposits were uninsured helped the bank to avoid being in a situation similar to First Republic. What is more, if uninsured deposits covered by pledged investment securities are excluded, this figure is reduced to 19% of total deposits.

{kind=link}

What is most interesting about deposits, however, is that interest remains remarkably low despite the new macroeconomic environment.

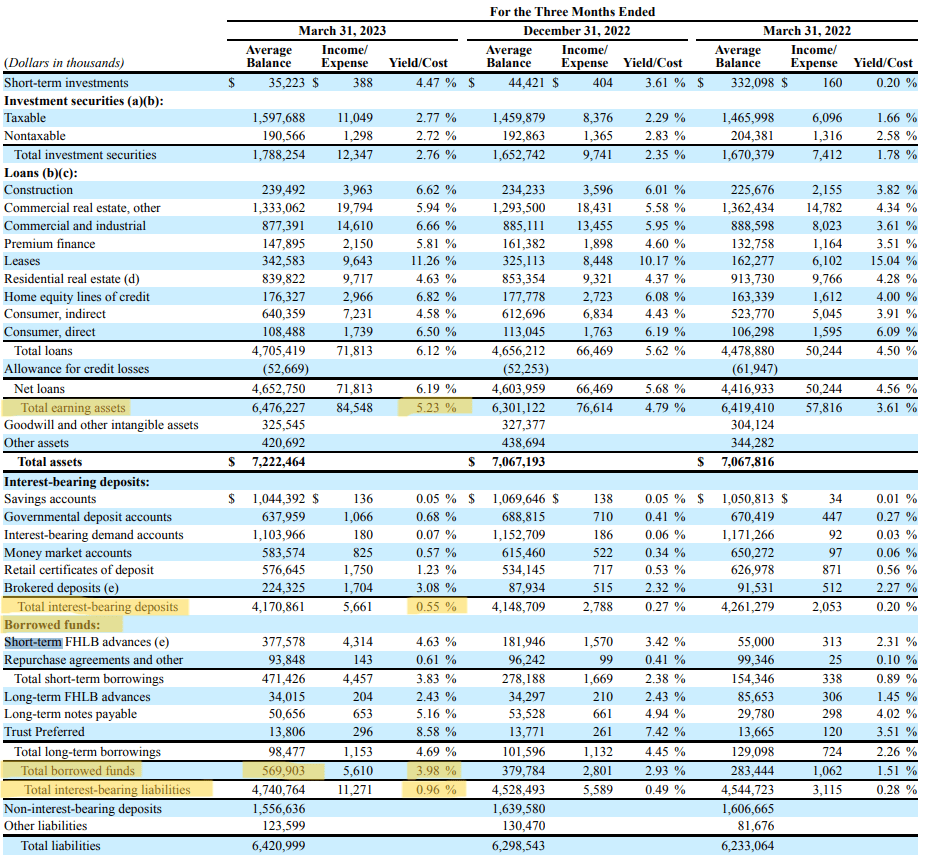

Total interest-bearing deposits presents a cost of 0.55%, not that different from 0.20% a year ago. Yet, now the Fed Funds Rate is at 5-5.25%. This is far better than the norm.

A few days ago I analyzed another regional bank , Valley National Bancorp, and in that case, deposits had reached an interest rate of around 2%, with deposit beta expected to rise. In this case, it's like a year ago in terms of the cost of funding. Certainly, total borrowed funds have increased to $569 million with an average cost of 3.98%, but it represents only a minimal amount compared to deposits. Peoples Bancorp for now still manages to finance itself at a low interest rate, in fact, it has not yet taken advantage of the Federal Reserve Bank term funding program, but does not rule out doing so in the future.

Overall, interest-bearing liabilities amount to $4.74 billion with an average cost of 0.96%, not too much above last year's 0.28%.

At this point, since the cost of liabilities has not increased much, one might expect the same for interest earned on assets, but it has not. Total earning assets have a yield of 5.23%, well above last year's 3.61%. The latter had an increase in yield of 162 basis points, in the case of liabilities the cost increased only 68 basis points. In short, the yield on assets is adjusting to the Fed Funds Rate much faster than the cost of liabilities.

{kind=link}

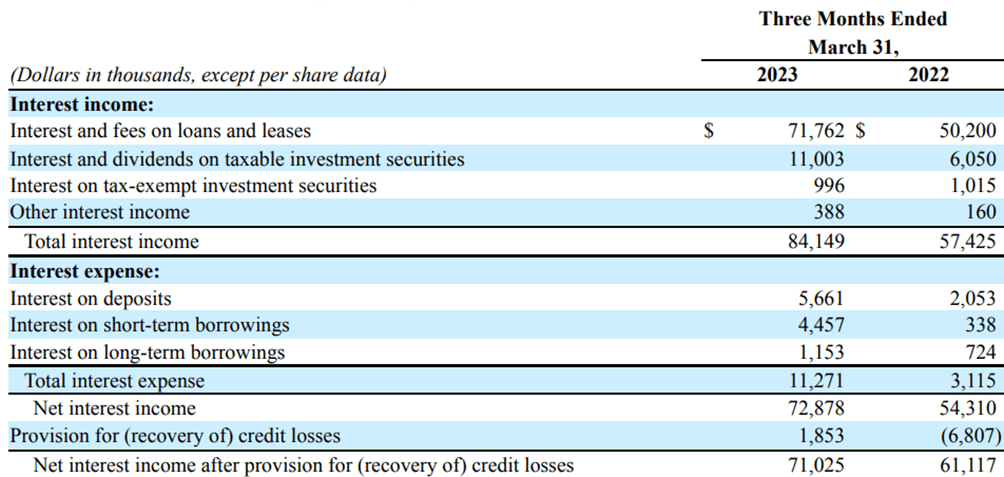

This is reflected accordingly in the income statement, which shows an increase in net interest income of $18.56 million compared to the previous year's quarter. What's more, the net interest margin also increased, 4.53% versus 4.44% in Q1 2022.

Our net interest income grew compared to the prior period, as the higher market interest rates benefited our interest income, outpacing the increase in our funding costs. Compared to the linked quarter, net interest margin grew 9 basis points.

{kind=link}

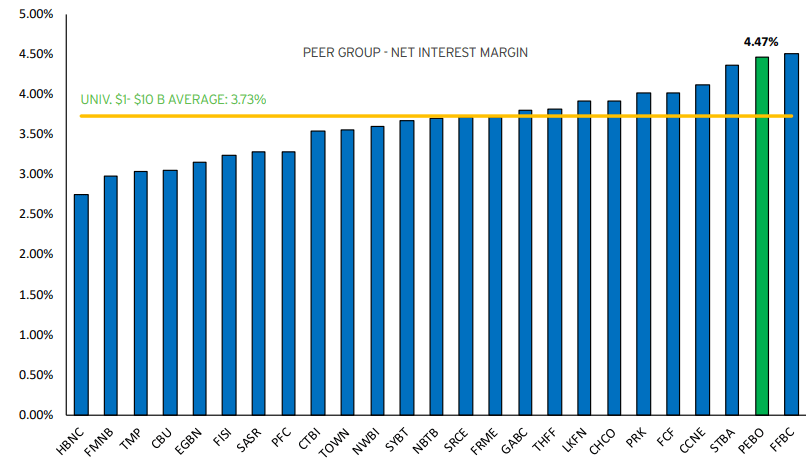

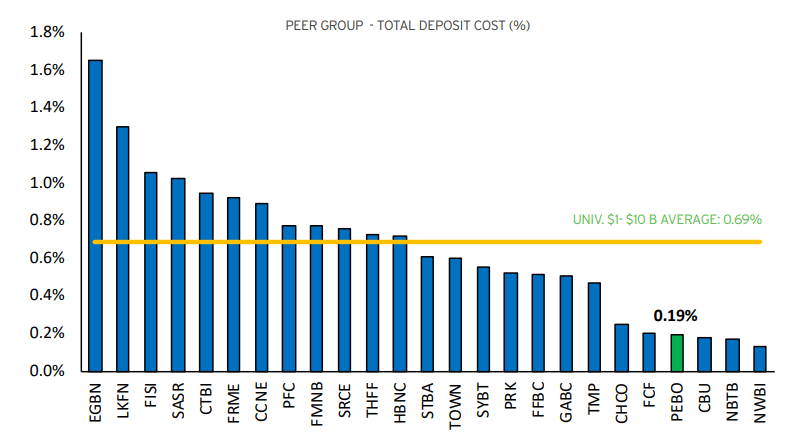

Overall, this is an excellent margin, in fact, much of the competitors are not even close to such a result. This image represents the picture as of December 31, and only First Financial Bancorp presented a slightly better margin.

In light of what we have observed so far, it is clear that the secret to Peoples Bancorp's high net interest margin lies not in the yield on assets but in the low cost of deposits.

{kind=link}

But how long will deposits be so cheap? No one can know for sure, but the guidance for the full year 2023 forecasts a net income margin between 4.40-4.60% and profits growing between 18-19% (partly due to the purchase of Limestone Bank); therefore, I assume that the cost of deposits will not increase that much otherwise margins would be seen downward. This would be a result against the trend of other financial institutions, but this does not seem to worry the CEO:

As far as bank performance, we understand that analysts are cutting earnings projections for institutions across the board, but we do not believe this to be an accurate indicator for investors of Peoples. We recommend that analysts look at each bank individually and inform the market based on their analysis.

Personally, although optimistic, I think the CEO's forecast may turn out to be correct. Interest rates have supposedly peaked and this bank is still paying a low interest rate to depositors, despite the fact that there are many other alternatives such as a simple 3-month U.S. bond that yields more than 5%. In short, if customers have accepted this situation so far, I don't see why in the future it should all change in the course of a few months. Apparently, depositors trust the bank and have no interest in considering more remunerative alternatives. Often, those who deposit their money give more importance to trust towards the bank and the usability of the services offered rather than the interest rate offered. As also stated by the CEO during the conference call, the deposit base is a key strength of Peoples.

Final Thoughts

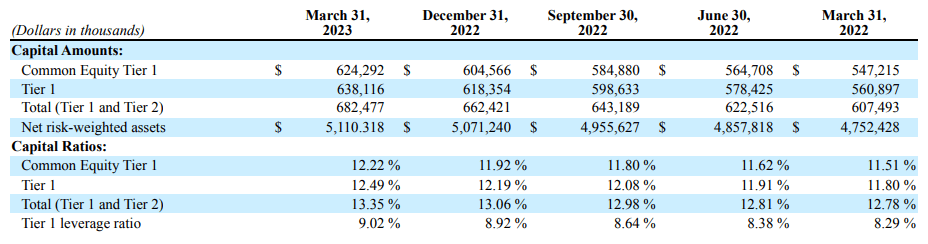

Like all regional banks, Peoples Bancorp is going through a complex time, but its profitability remains off the charts. Deposits have one of the lowest interest rates in the industry, and with a growing yield on assets, net interest income continues to increase. In addition, the bank is also hedged against liquidity and interest rate risk.

{kind=link}

Capital requirements are all fully met, even including unrealized losses of HTM securities. The loan-to-deposit ratio is 82%, and CRE loans belong mainly to A-tier developers representing 147% of risk-based capital. What if interest rates experience a violent fluctuation?

{kind=link}

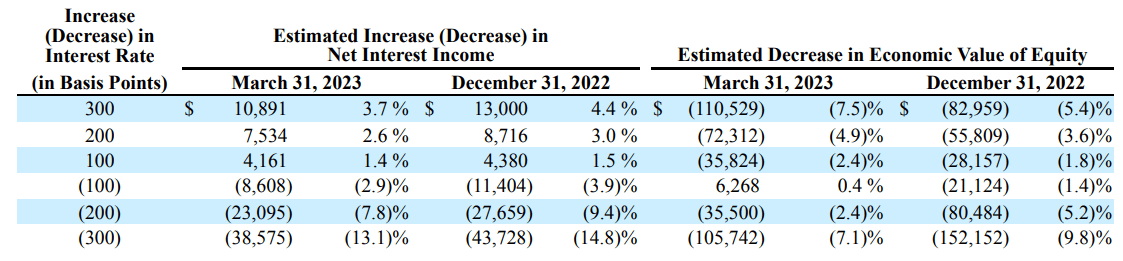

Again, there are no major concerns, as a fluctuation of plus or minus 100 basis points would not impact net interest income or equity too much. At present, the most likely scenario is a rate cut; in that case, up to 100 basis points would reduce net interest income by 2.90% and equity would increase by up to 0.40%.

In short, at least by analyzing the surface, this bank looks solid, and with an above-average net interest margin, it could perform better than its rivals. However, this does not mean that Peoples Bancorp is a buy. The average P/B over the past 10 years is 1.08x, multiplying this by the current BV per share ($29.42) gives a fair value of $31.77.

According to this metric Peoples Bancorp is undervalued, but wanting to be more conservative, making the same calculation with Tangible BV, the fair value would be $29.03. In short, it would still be undervalued but with a smaller margin of safety.

Personally, to invest in a regional bank at this time in history I need a huge margin of safety, which I don't think an investment in Peoples Bancorp has at the moment. Anyway, it remains an interesting bank and I will continue to follow it.

For further details see:

Peoples Bancorp: Deposits Are The Key Strength