VNQ - Perception Is Not The Reality: 2 REITs I'm Buying All The Way Down

2023-10-13 08:00:00 ET

Summary

- Investors are pulling out of the stock market and into lower-yielding investments like T-bills, causing stock prices to drop.

- REITs, such as Agree Realty and Realty Income, have seen their prices decline, presenting an opportunity for investors.

- Agree Realty has a strong balance sheet and no exposure to office properties, while Realty Income has acquired a stake in the Bellagio and has potential for growth in the gaming industry.

- The perception that REITs are bad investments is not the reality and are now offering investors the potential for massive upside.

Introduction

I'm sure many investors probably have felt like the guy in the picture above the last couple of months. I consider myself a pretty experienced investor now and one thing the market has taught me is patience. But I'll admit it's hard looking at your brokerage account week after week and seeing all your gains gone and your account constantly in the red. It starts to wear on you mentally. You start to second guess your investment decisions. You start shuffling your portfolio into investments you think are safer, or now higher-yielding ones such as bonds. You constantly hear the news saying negative things about the stock market, so you start asking yourself "What am I doing wrong?" Maybe I should take my money out of the market and hold cash until everything settles down. That is a sure way to miss out on some nice capital gains. That's called market timing and it can get a lot of investors burned in the future.

Serving over 21 years in the Navy has prepared me to deal with almost anything. I've been on quite a few ships, destroyers mostly. You get used to operating in chaos and I've really gotten used to doing just that. I honestly think that's what prepared my psyche to deal with the current turmoil in the sector ( VNQ ). In the Navy upper leadership would always say "Perception is reality!" I absolutely hated this saying and never used it during my time as a leader. To me this was an excuse for them to convince themselves they were right in their thoughts. So no matter how dumb it sounded, or if they didn't have evidence to back up their claim, whenever you justified or debunked this, they would say "Perception is Reality." In my eyes a good leader would never say that, but do their due diligence to actually find the truth.

I look at the sell-off in the REIT sector the same. Investors should do their due diligence to actually see, "have the fundamentals changed, or has the stock sold off because many are now panicking?" Let's get into two REITs I'm actually buying hand over fist.

Long-term Outlook

In my opinion, if you invest in the stock market, you should have a long-term outlook. But everyone doesn't share that same sentiment, some investors prefer to trade in and out of the market. I used to do that and it's all fun and games and ultimately you're most likely going to lose money gambling that way. Now I buy and my plan is to hold my investments forever unless the fundamentals of the company change. And it's hard to keep that mindset, and stick with the plan when you constantly see the price dropping on your favorite stocks.

But you have to reassure yourself that that is not the case. Whether that's looking into the financials of your stocks every day or every week. Although that can be very overwhelming. Like I previously mentioned, I used to day trade and it's emotionally draining. That's why I adopted dividend investing for the long-term. It may not be as fun to some, but I really enjoy watching dividends hit my brokerage account on schedule. So my advice to readers is buy stable, quality companies with strong fundamentals, and stay invested. We've all heard the saying from Warren Buffett. The stock market is the only place where people run from a sale. And now investors have been running into T-bills while they wait out the storm.

Why I'm Buying

Investors have been rotating out of the market from lower-yielding investments, and into higher-yielding ones like money markets, T-bills, and certificates of deposits. Right now those are currently paying more than a lot of REITs. But those aren't the only stocks that have seen their prices drop. Consumer staple stocks like Coca-Cola ( KO ) and PepsiCo ( PEP ) who both have 5-year average dividend yields of roughly 3% have also sold off in the last month. And this could continue well into 2024. I don't know when the market will bottom, but I know I'll be running to the Black Friday Sale and taking advantage of this opportunity.

Many stocks are now reaching GFC price levels which has also caused investors to get spooked. We've all heard the saying, "Scared money don't make money" and I agree. I've always been a risk taker and this time I'm staying put. As you can see BDC's prices have held steady during the same time. I hold both Ares Capital ( ARCC ) and Capital Southwest ( CSWC ) in my taxable account and their prices haven't moved much. It's because of their yields. Their fundamentals have nothing to do with it, same as REITs.

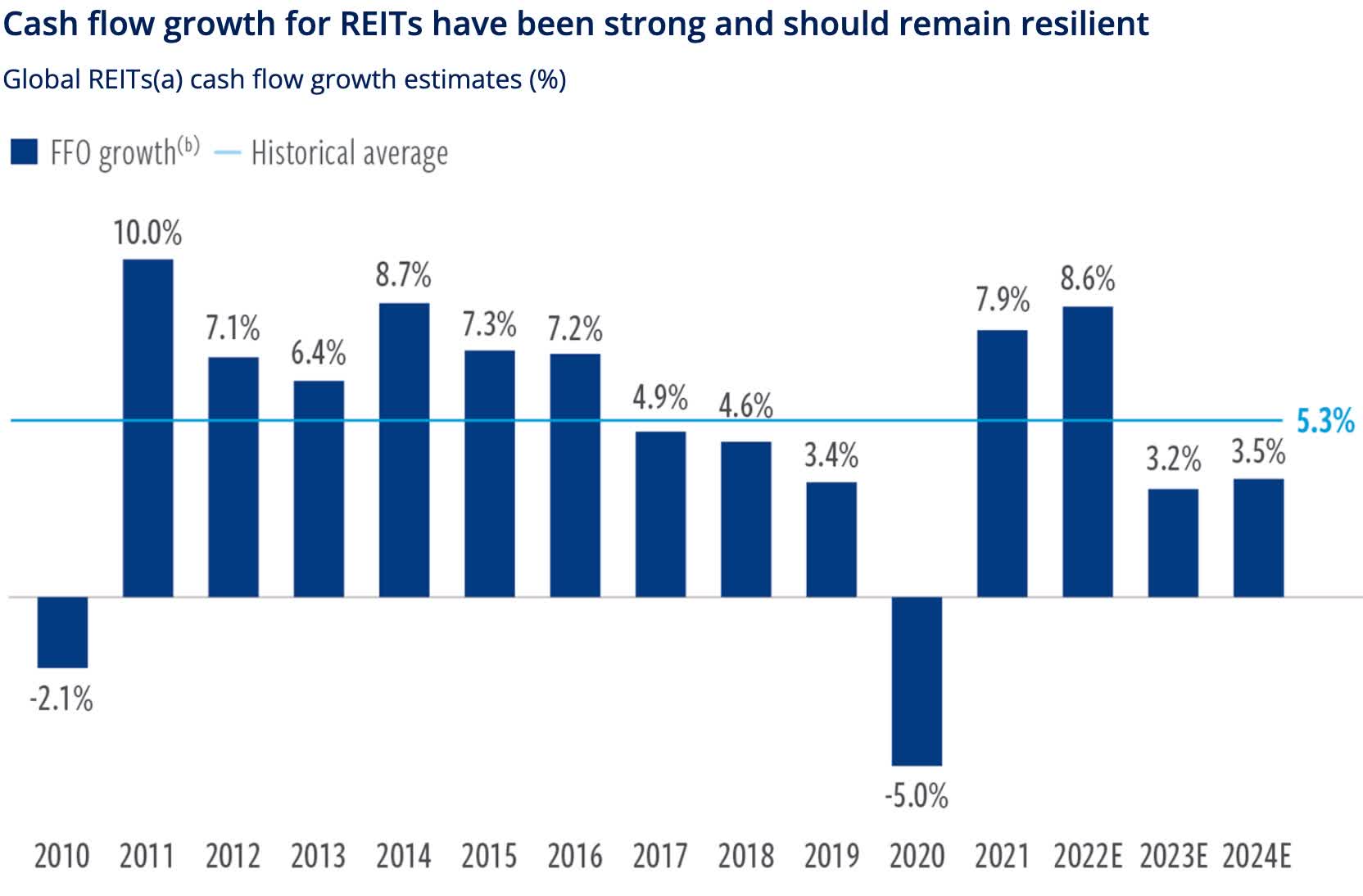

Cohen & Steers' Head of Real Estate & Research, Rich Hill, recently said: First, we believe that commercial real estate fundamentals are on strong footing. Consider that listed REITs generated same-store net operating income (NOI) growth of 7.2% in Q123, compared to the historical average of 2.4% since 2000. Listed REIT fundamentals are decelerating but remain resilient. We've lowered our growth expectations amid the slowing economic backdrop but they have entered the economic slowdown in relatively healthy positions.

As you can see below, REITs have an average historical FFO growth of 5.3%, but this is expected to come in at 3.5% next year. Not the same as prior years, but growth is still growth. Like I previously mentioned, my goal is to hold my investments forever and collect enough income to live off of in the upcoming years. The way I see it this will happen quicker than I thought with the attractive entry points REITs are now offering. In my opinion, REITs will make new highs when interest rates start to decline. When that will be I'm not sure, but my guess is sometime in 2024.

{kind=link}

Why I'm Buying Agree Realty

Since my start as a Seeking Alpha analyst in May, I've written a few articles on Agree Realty ( ADC ). I've been a fan of them for quite some time and always preferred them over Realty Income. I know O gets a lot of love here on SA and for good reason. But I just always thought ADC was the better REIT, although O is definitely more popular. But in my eyes, this isn't a popularity contest and never was. I could care less about that and just thought that ADC was of higher quality.

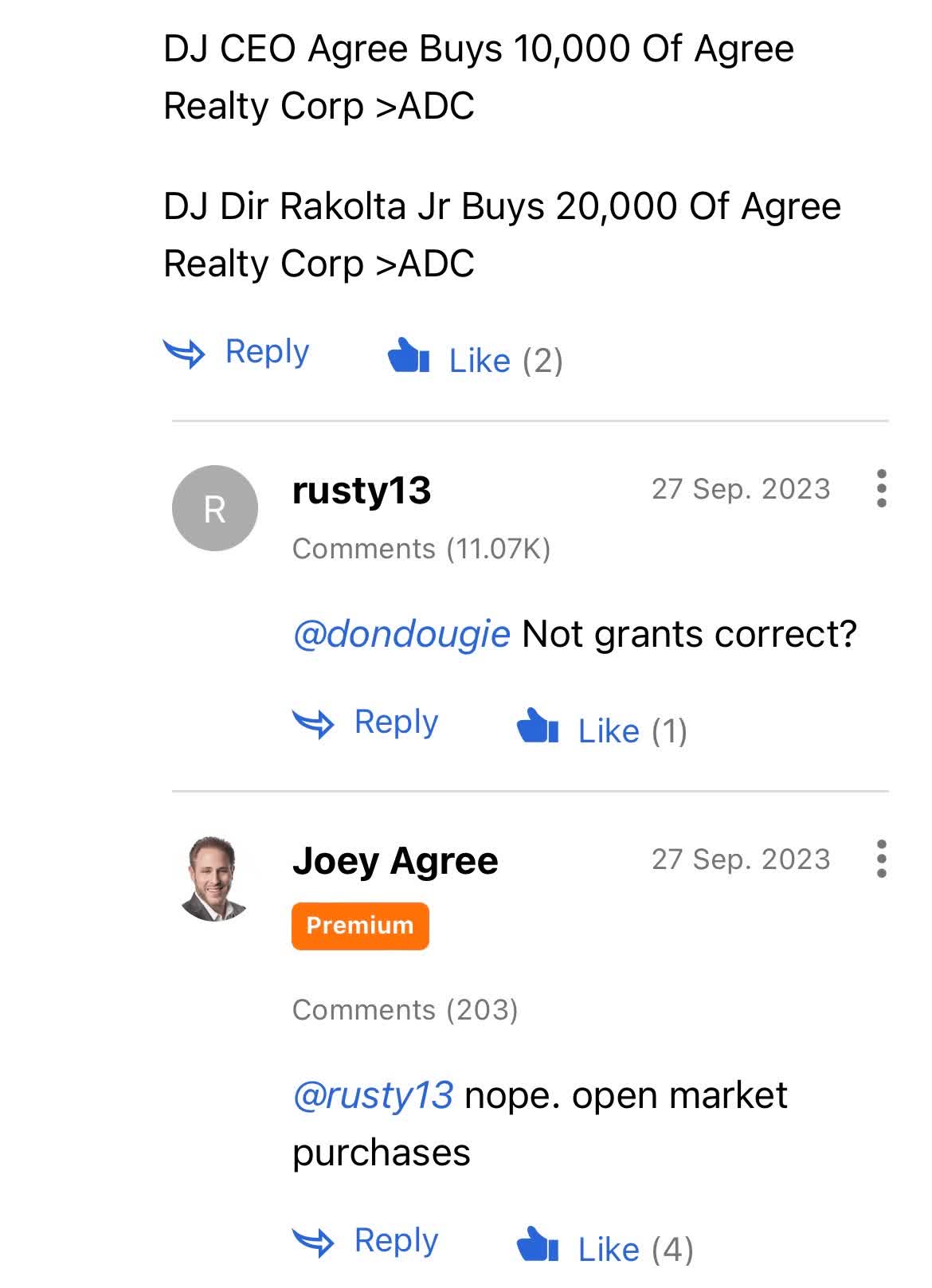

And I think the market sentiment is showing that. ADC is down 10.75% in the last month while O is down 11.33% during the same time. In my article, Agree Realty: Putting Their Money Where Their Mouth Is , a reader shared this:

{kind=link}

As you can see ADC's CEO commented these were open market purchases. Insider buying is one way to tell management is confident in their company and should give investors conviction. It definitely has been giving me that as I've been buying all the way down. The stock has been reaching new 52-week lows for the last few weeks but that hasn't deterred me one bit. And I will continue buying no matter what as long as the fundamentals remain strong.

Fortress Balance Sheet

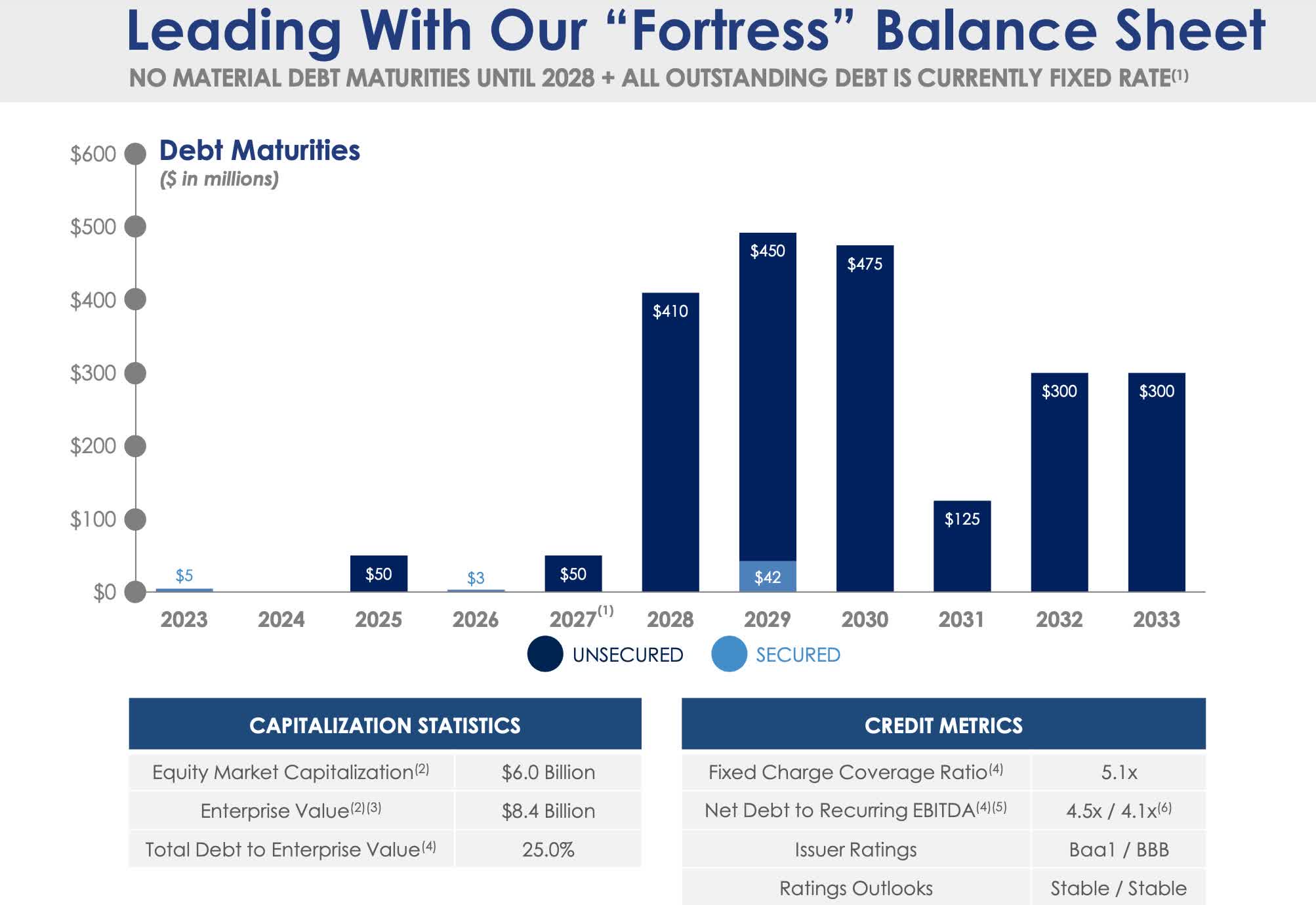

We all know what's going on in the economy right now so there's no need to repeat it. One of my favorite things about ADC over any REIT right now is their debt maturity schedule. Off the top of my head I can't think of any REIT who has a better balance sheet right now. Looking at their schedule you'd think they have an A credit rating. The company has no significant debt maturities until 2028, 5 years from now. Besides that they also have a very low Net debt to EBITDA of 4.5x and a fixed charge coverage ratio of 5.1x. This is lower than the favorite Realty Income who has a net debt to EBITDA of 5.3x. I like to see this below 6, below 5.5x is even better.

{kind=link}

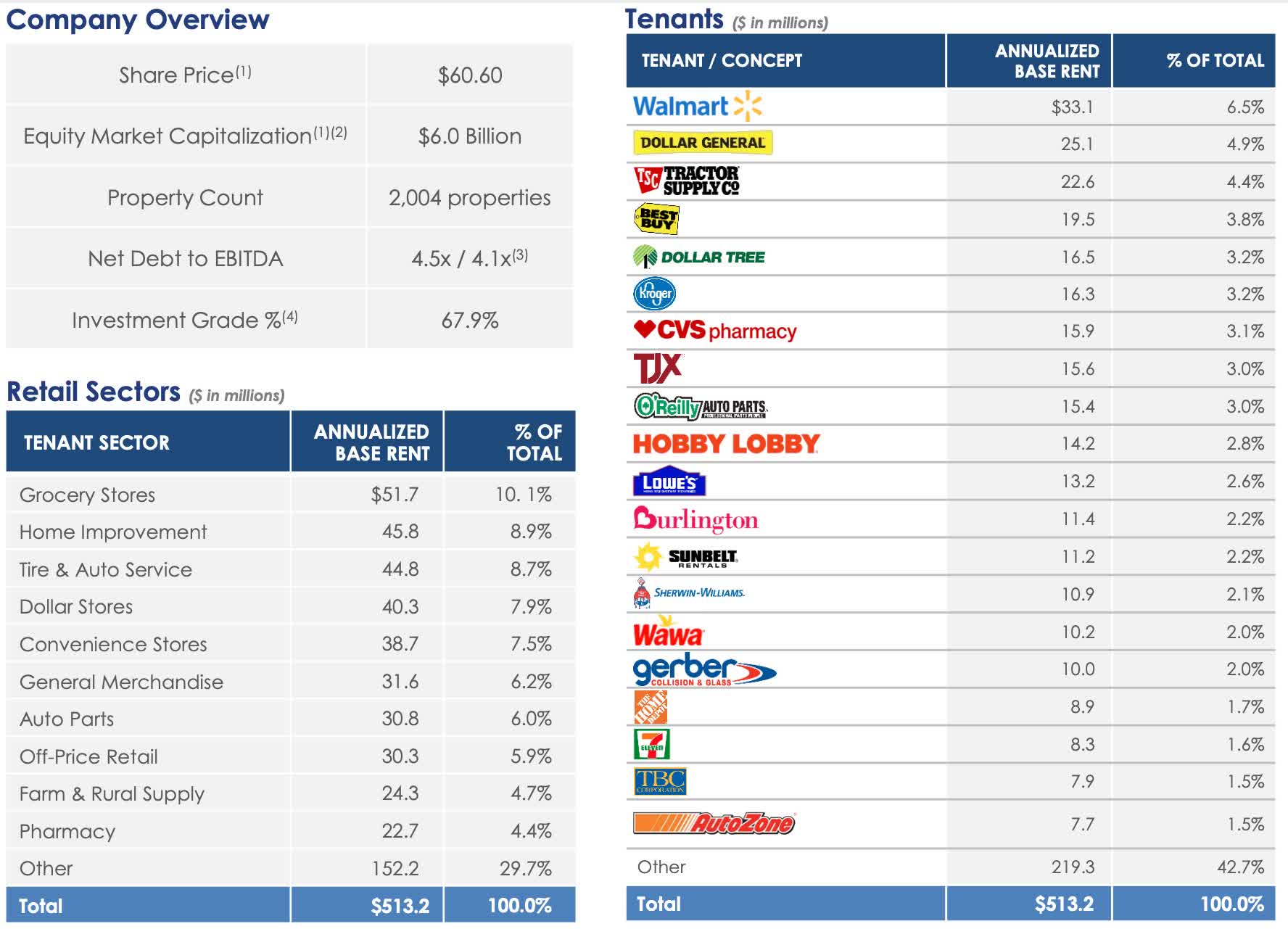

They also have no exposure to office properties. I know everyone is worried about that now, especially with the announcement made by W. P. Carey ( WPC ) about spinning off their office properties later this year. That probably spooked investors even more seeing that WPC was also a favorite among those here on SA. ADC has no office exposure and derives most of its ABR from recession resistant tenants such as Walmart ( WMT ), AutoZone ( AZO ), and Lowe's ( LOW ). 68% to be in fact. The other 29.7% in their portfolio includes companies like Davita Dialysis ( DVA ), CarMax ( KMX ), Fresenius Medical Care ( FMS ), Esporta and Planet Fitness ( PLNT ) to name a few.

They also have ground leases which account for 11.9% of total portfolio ABR. These typically have longer lease terms and 87% of these tenants are investment grade. And with ground leases if the tenant defaults on rent payments, ADC gets to keep the building and rent it out to the next tenant.

{kind=link}

Why I Am Buying Realty Income

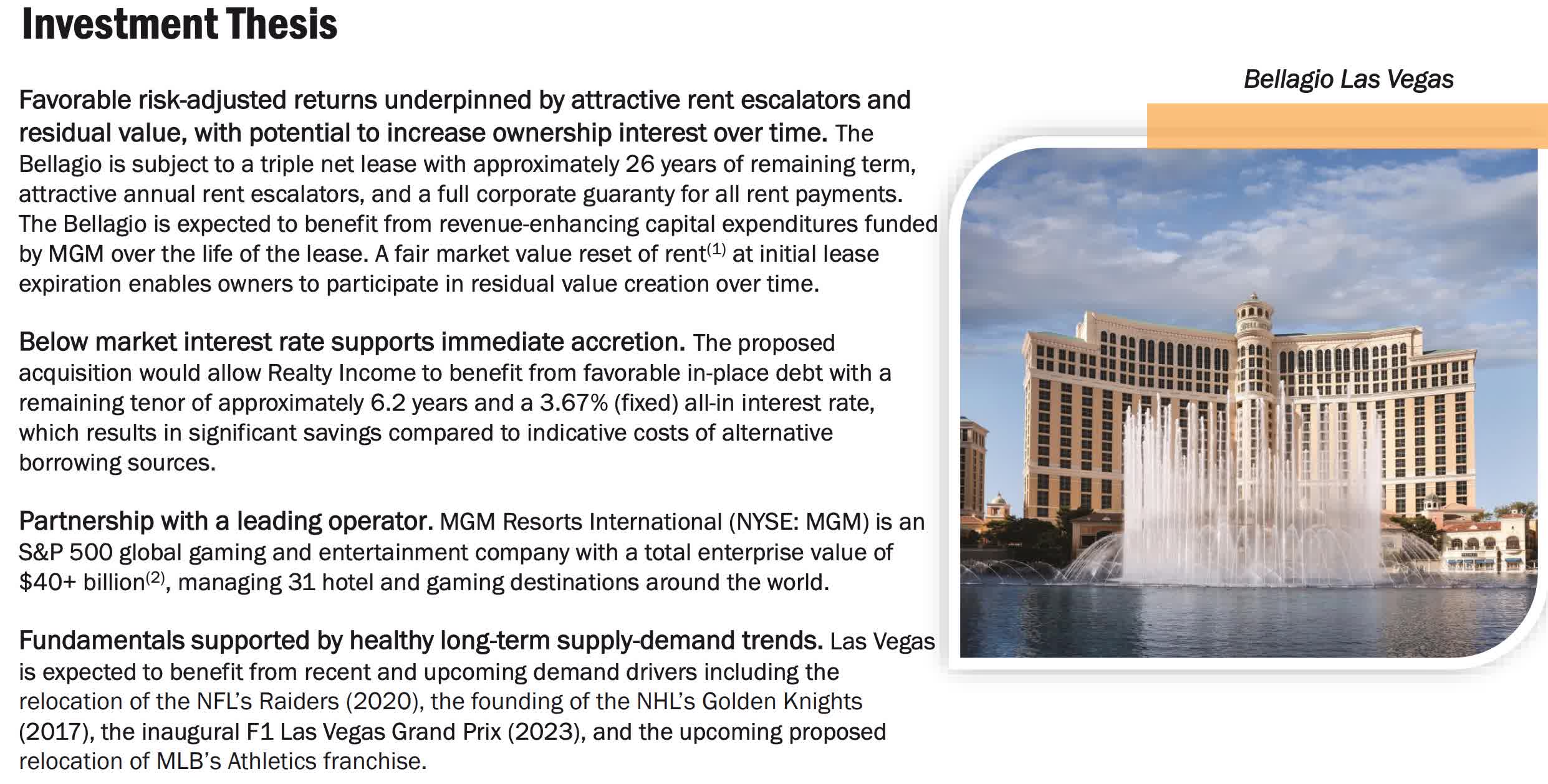

So, O is a newcomer in my portfolio. I held them once before years ago but sold. I recently acquired them again because of their valuation; it was just too good to pass up. I've always preferred ADC but saw an opportunity to have two monthly payers in my portfolio, both trading at significant discounts. O recently announced a deal acquiring a 21.9% stake in the Bellagio from Blackstone ( BX ) back in August. They agreed to invest $950 million. But it didn't seem like many shareholders were very fond of the deal.

One of the reason I sold O and acquired ADC was because I thought they had better growth prospects. I still do think that, but just because I prefer one, doesn't mean the other one is a bad investment. I actually wasn't surprised that they took the deal. I speculated it would be either them or VICI Properties ( VICI ). VICI already owns a significant percentage of the Las Vegas Strip so I thought to myself "Why Not?" And even discussed this possibility back in August with, "Worried About Record Home Prices? Buy Realty Income Instead . BX had put the deal on the table and I mentioned that O could possibly take the it as they had recently moved into the gaming space.

Bellagio investor presentation

{kind=link}

I actually didn't mind the deal. I'm a frequent visitor of Las Vegas and have been for the last decade. I see the cash flow that goes through there so for O who was getting too big, it wasn't a surprise they ventured outside of retail for the second time. The REIT is large and has to keep growing somehow, and what better way than jump into the gaming space. It's a billion dollar industry and isn't going anywhere anytime soon. Formula 1 racing is expected to start in November of this year as well.

They're literally turning the Las Vegas Strip into a racetrack which will be huge for the city. Hotels will be booked and most likely see increased revenues during the event. There's also talk of the Oakland Athletic's moving there soon as well and possibly even an NBA team. Additionally, the city has $4.5 billion in new projects coming in the next two years and this will most likely benefit O in the process. Las Vegas has been seeing strong growth in 2023 . Visitor volume increased 13.6% and convention attendance increased 68.9% year-over-year. Gaming revenue and hotel occupancy also rose during the same time.

A-Rated Balance Sheet

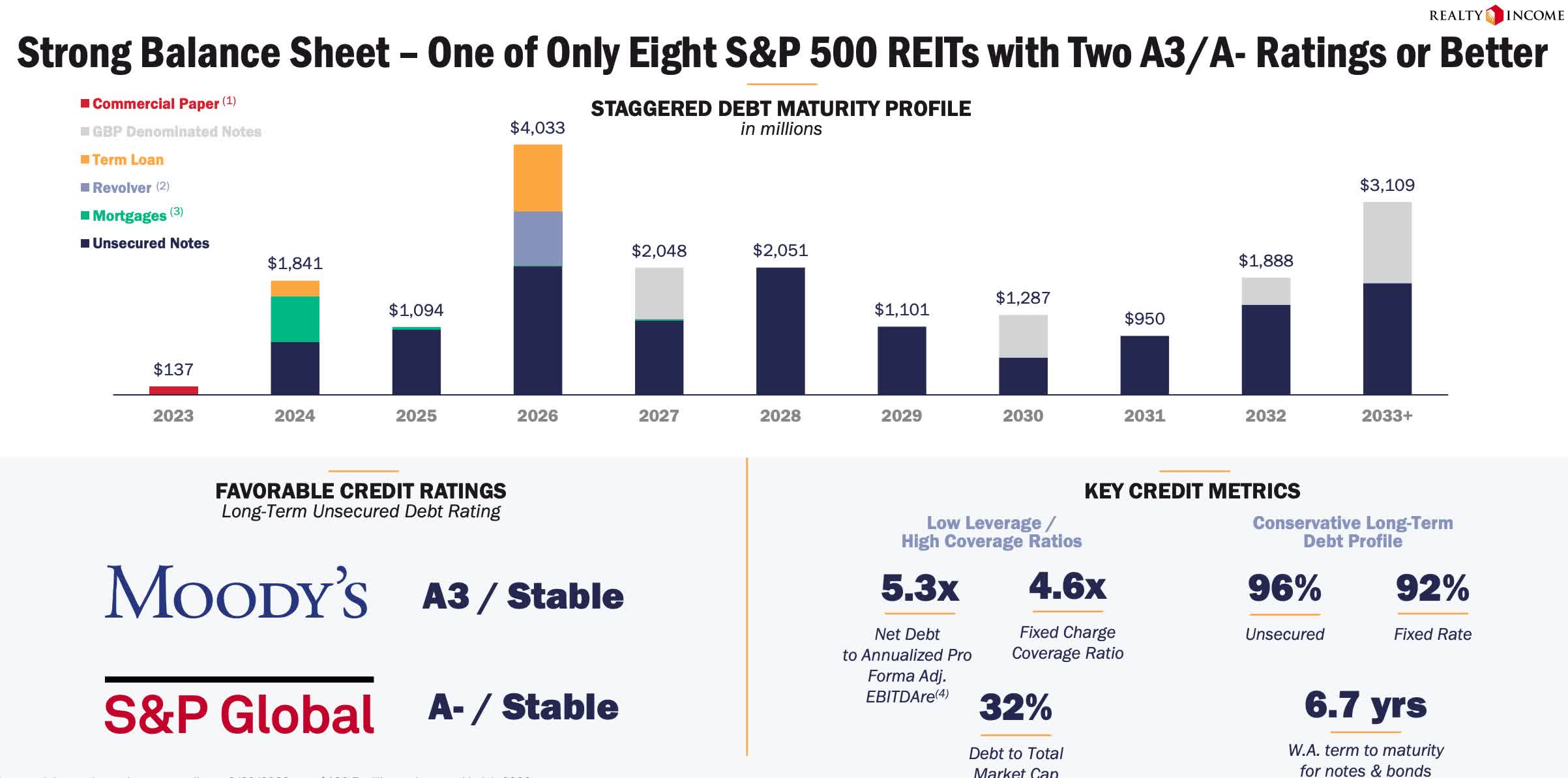

One thing that may have investors worried is O does have a substantial amount of debt maturing in 2024. The company has $1.8 billion in debt due in then. Most of their debt is fixed rate at 92% and they currently have a Net debt to EBITDA of 5.3x. Another reason for O's price drop is their motion to sell up to 120 million of its shares. So shareholders weren't happy with the REIT's announcement.

The purpose of this was to raise capital to repay some of its debt and expand certain properties in the portfolio. To be honest I think it was mostly to repay debt. Realty Income plans to use the capital to pay down its debt maturing next year. This is not out of norm for REITs but it's easy for investors to get riled up about something with one of their favorite stocks. Like I previously mentioned, you'd think ADC has the A-rated balance sheet looking at their debt maturity schedule but I think O will be just fine. They do have even more debt maturing in 2026 but I think interest rates will be much lower by then.

{kind=link}

Monthly Compounders

Another reason I've been buying these two is now I get to combine the dividends to grow my dividend snowball even faster. Both ADC & O pay around the same time on a monthly basis, and are scheduled to pay out the 13th of this month. So not only am I getting two checks, I get more dividends to reinvest to continue towards my goal of supplementing my income. The sector is offering some of the best entry prices in years and buying now not only gives you a margin of safety, but faster steps towards your investment goals. To put this into context, O has a 10-year price return of 34.11% or roughly 3% when broken down annually. Using a 3% annual DGR and an expected 2.0% annual price return, my forecasted portfolio would increase by 4% in 5 years and by over 72% in 10 years with dividends reinvested.

My Valuation & Risks

Both REITs currently offer over 30% upside to their price targets right now. ADC has a price target of over $72 and Wall St rates it a strong buy. Even if the stock hits its lower target of $58, this still offers 5.7% upside. O offers roughly the same upside of $17 to its price target of $67.27. They also have a low target of $52 so investors are getting some upside investing in both REITs right now.

For REITs I like to use the Dividend Discount Model ((DDM)). I typically like to be a little more conservative than other analysts in my valuations. According to Cohen & Steers, REITs are expected to see slower growth ahead, slightly over 3% going forward. Using next year's dividend estimates of $3.02 for Agree Realty and $3.15 for Realty Income, and an expected 8% annual return, I have a price target of $60 for ADC and $63 for O.

The major risk both of these REITs could face is if the Fed continues to raise rates. This would further cause pessimism in the sector, most likely sending their prices even lower. If the Fed decides to hold, I see their prices remaining stable here. This would also mean O would have to refinance their debt at a higher rate next year.

Conclusion

Both stocks are currently trading well-below their 5-year average P/AFFO ratios and offer investors a great entry price into well-established, high quality real estate. The sector has suffered in the last year due to their low-yields but fundamentals remain intact. Although growth is expected to come in lower because of the economic back drop, I think the market sentiment is overblown. When interest rates do start getting cut, I think REIT prices will rise, some to new-highs as investors gain more confidence to leap back into the market once again. ADC & O are two REITs of the highest quality, and when sentiment starts to shift, I think these two will be the first to see their prices appreciate.

For further details see:

Perception Is Not The Reality: 2 REITs I'm Buying All The Way Down