APPS - Perion Network: Challenging The Short Thesis - Making An Informed Decision

2023-06-12 14:30:36 ET

Summary

- I make the case that Perion Network Ltd. stock is undervalued. The business holds no debt and is reporting substantial free cash flow.

- Concerns regarding Perion's CEO transition and potential dilution of shareholders are acknowledged.

- Perion is cheaply valued as investors presently shun adtech stocks. Not because of anything ''negative'' with its business model.

Investment Thesis

Perion Network Ltd. ( PERI ) is a stock that I continue to believe is cheaply valued. I've been arguing that Perion is cheaply valued for more than 2 years .

My thesis points to its clean balance sheet , with no debt. Also, the fact that Perion is making significant free cash flow. I believe that Perion is priced at about 15x forward free cash flows. A valuation that I believe is cheap, particularly since we are likely facing trough free cash flows.

Meanwhile, Perion has become the subject of a short report by Spruce Point Capital Management, LLC. I believe that I am knowledgeable enough about both Spruce and Perion to lay out a knowledgeable analysis of where Spruce is right and where they are not.

But overall, I believe that Spruce is wrong in this case. And I reaffirm my rating on Perion stock.

Spruce Point's Handful Of Short Positions

I have a ton of respect for Spruce Point.

I've followed their work over the years, and they have led many superb short positions. But like many investors (longs or shorts), they have made a few blunders from time to time.

For example, here is the second round of their short on WD-40 Company ( WDFC ).

Spruce Point called for ''management to step down and admit failure'' and that WDFC would be headed for ''$69.00 - $95.00.''

If the day that the second short thesis came out, investors had done the exact opposite, investors would be up more than 26%, versus the S&P 500 Index (SP500) which is up 15% in the same time period.

What's more, as you know, the S&P 500 is presently being led by a tiny, tight group of AI-related names. Countless sectors, including advertising, outside of AI-related baskets are performing quite badly. And yet, WD-40 still outperformed the S&P 500 over the same time period.

And this brings me to my second argument. On the 17th of February , Spruce made a huge clamor about their short thesis on C3.ai, Inc. ( AI ).

Here, things get more nuanced.

Because there's the argument to be made that some of the points Spruce made are right. In fact, admittedly, I, too, made similar assertions to Spruce on C3.ai.

And I, too, was wrong and the stock is up significantly. Was Spruce right about the validity of their argument? I don't wish to become too philosophical about investing and dealing with counterfactuals. The fact of the matter is that Spruce's call for the stock to fall by ''40% to 50%'' was wrong.

What About Perion's Short?

I don't wish to throw mud on Spruce. I fully acknowledge their ability to call countless shorts right. I also highlight how we both thought the same when it came to C3.ai (and how we both ended up being wrong on that stock).

Furthermore, in an effort to complicate my argument further, I'll be the first to admit that I previously wrote myself,

Perion's very successful CEO Doron Gerstel will step down. On the surface, this was a surprise.

I was taken aback by the timing of Gerstel's transition. And this was something that Spruce was quick to latch on to and make a whole contention about. Spruce goes on to make some further allegations about Lumenis LTD back in 1999, which I don't have a view one way or another.

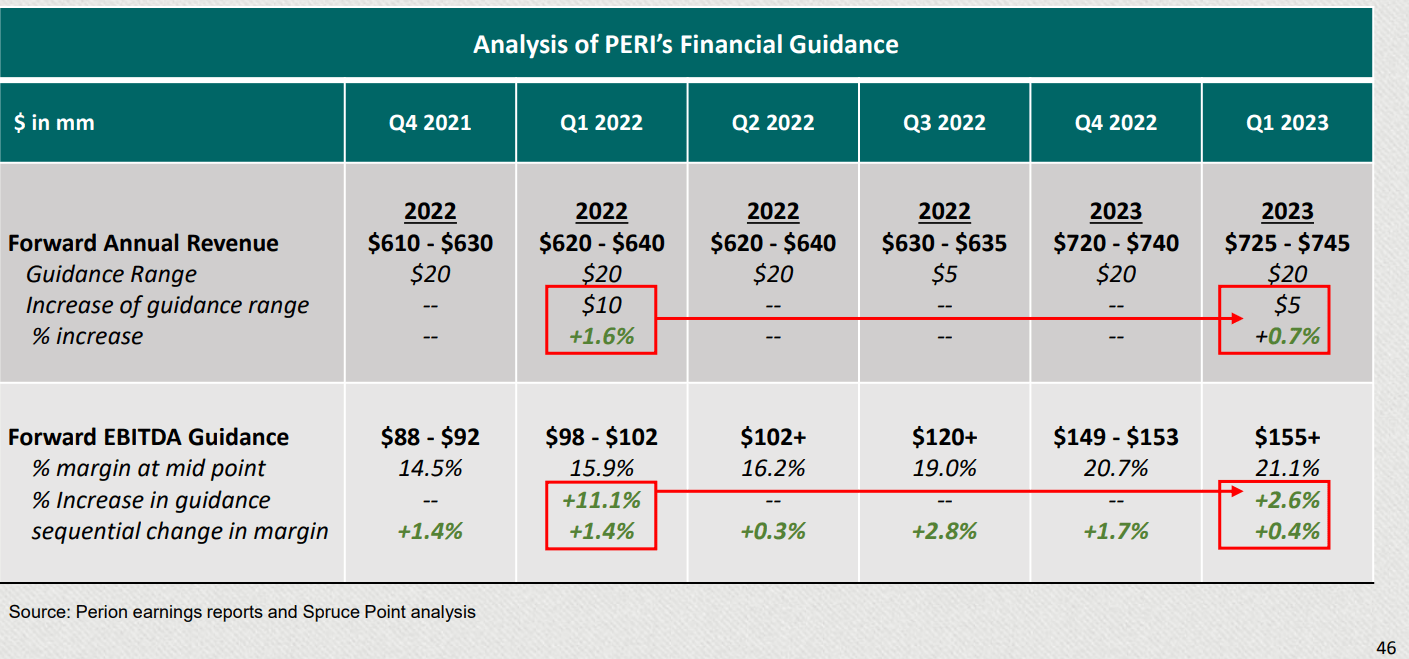

Then, about a third of the way into the short presentation, Spruce gets to where I believe they could have a valid argument:

{kind=link}

This is factually accurate, as the size of the increases has become smaller for Perion. While I believe this has more to do with the common sense argument that the advertising sector is in a tough place right now, I don't wish to simply push this argument under the carpet.

A lot of the bull thesis is focused on the significant growth rates in Perion's EBITDA growth rates. And if the growth rates were to slow down, this would have a considerable impact on the multiple that investors would be willing to pay for Perion.

All that being said, Spruce believes that the stock is about 40% overvalued and should trade closer to $19.10 - $23.85/sh. So, it's not that Perion has structural problems. It's simply that they believe the stock is overvalued.

But is Spruce Totally Wrong?

This is where the story gets a little murkier.

Perion has a history of diluting shareholders to raise capital. For instance, about 18 months ago , Perion diluted shareholders. Spruce doesn't mention this in their research, but it does mention the newest motion to dilute investors by up to 20 million shares .

And in fact, with more than $430 million of cash on their balance sheet, I too question this very poor capital allocation decision.

If Perion's market cap is $1.6 billion, and a quarter of its market cap is made up of cash, it does appear to me to be foolish to even propose this capital raise.

On the other hand, just because it's a foolish capital allocation strategy, doesn't necessarily mean that there's something nefarious.

What About Other Risks?

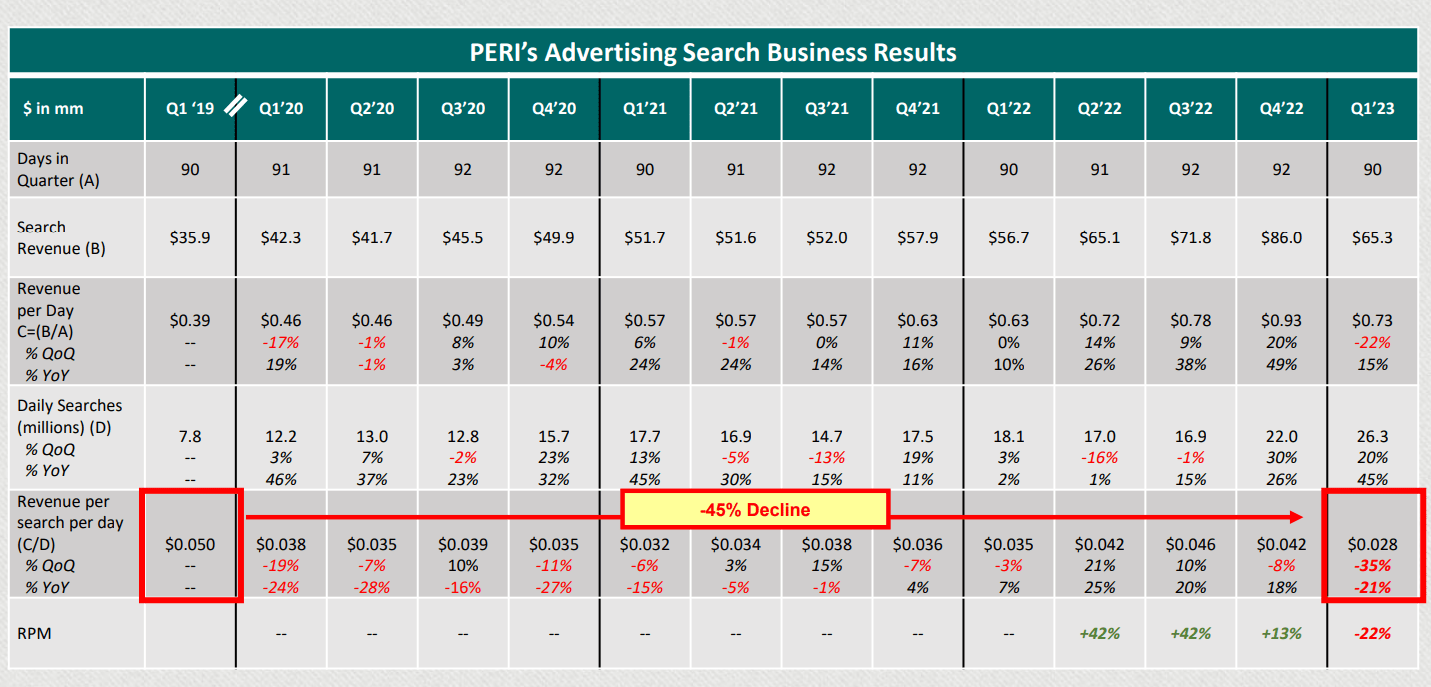

{kind=link}

Spruce highlights a decline in revenue per search per day. And this is true. But the comparison that Spruce makes with 2019 is fundamentally misplaced. Everyone knows that in 2019 the adtech space was dramatically more profitable. If you want to find out more, just ask Digital Turbine, Inc. ( APPS ) and how things have progressed for them.

The Bottom Line

In this analysis, I argue that Perion is a cheaply valued business with a clean balance sheet.

Also, I acknowledge the surprising timing of Perion's CEO change. Furthermore, I plainly question Perion's capital allocation strategy and find it perplexing. While Perion could be more active in using the cash on its balance sheet to buy up its undervalued shares, I don't believe this derails my bullish investment thesis.

Although Perion's EBITDA growth rates do appear to be slowing down, I believe that this has more to do with the advertising sector's challenges than something structurally wrong with Perion. Overall, I view Perion Network Ltd. stock as undervalued.

For further details see:

Perion Network: Challenging The Short Thesis - Making An Informed Decision