PKI - PerkinElmer: Capital Budgeting A Key Factor To The Investment Debate

Summary

- PerkinElmer continues to offer long-term upside potential with its management of capital and acquisitions.

- The economic value of its transactions has created a healthy return on investment over the time period.

- Even factoring for goodwill, the economic profit has compensated for this.

- Net-net, we reiterate PKI as a buy.

Investment summary

Firms can create value for their investors in many different ways, ranging from capital appreciation of equity, return of capital (dividends, buybacks), and through acquisitions. Each scenario is typically underpinned by the fundamental drivers of growth, namely, a high return on invested capital ("ROIC"), positive spread of ROIC above the hurdle rate, and, capital budgeting towards high-growth opportunities.

Acquisition-heavy firms with surplus capital are able to use their balance sheet effectively to generate additional growth down the line. Still, a company needs to invest this capital into projects/acquisitions at a return that exceeds the cost of capital. Hence, acquisitions should not only generate earnings growth (accounting profit) but also generate free cash flow to shareholders (economic profit, ("EP")). As such, high ROIC with positive ROIC/WACC spread means less equity is required to support earnings growth, leaving more residual income for investors.

We've covered PerkinElmer, Inc. ( PKI ) extensively in the past (see: here , and here ) and found there's value to be had in the name. Yet, shares are down 15% in the last 6 months and have failed to catch a bid amid the January rally of the broad indices. This is despite robust top-line and earnings growth across this time. That in mind, here I'll explain why we believe this has been the case, but I'll also run through how PKI has generated extensive EP over the past decade through its acquisition trail. Net-net, we continue to rate PKI a buy, reiterating our valuation of $155 per share.

Understanding why PKI is a good steward of capital

Back in August, we covered PKI's planned divestiture of its Applied, Food and Enterprise Services businesses ("AFES") to New Mountain Capital ("NMC"). The transaction, to be completed on a ~$2Bn net transaction, is set to close first quarter this year. Proceeds will be used for a variety of corporate activities. Per PKI's CEO Prahlad Singh on the Q3 earnings call:

"We are very happy with the strength of our balance sheet and we'll look to redeploy the nearly $2 billion of after tax proceeds we will receive from the divestiture through a combination of funding upcoming debt maturities, opportunistic share repurchases and of course continued strategic and value creating M&A."

Unfortunately, the price response from the market after the carve-out was announced was flat, suggesting investors are searching for more in the name.

Intelligent investors value an investment in corporate securities based on the distributable free cash flows they can receive on their capital (hypothetical, or tangible in dividends of buybacks). The market usually does the same. This, combined with the ROIC/WACC spread is a very important concept to grasp in terms of valuation. I mentioned earlier that a high ROIC means less residual income is reinvested as additional capital to support growth, leaving more free cash flow for equity holders. The more free cash available, the higher the valuation in most cases.

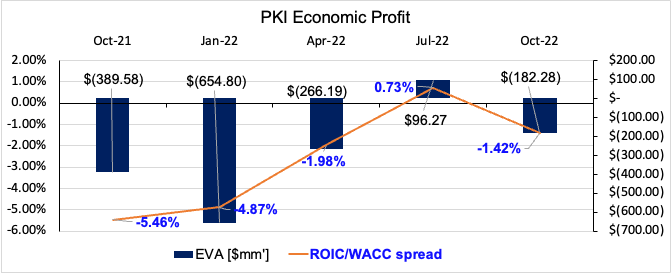

This is only true, however, if the ROIC exceeds the hurdle rate. Otherwise, growth, whilst good for the company, is destructive to value for equity holders. You'll see this was apparent for PKI over the period from FY21-Q3 FY22, where the level of EP remained negative over this time.

Exhibit 1. PKI Negative EP from Q3 FY21-Q3 FY22 (rolling TTM figures)

{kind=link}

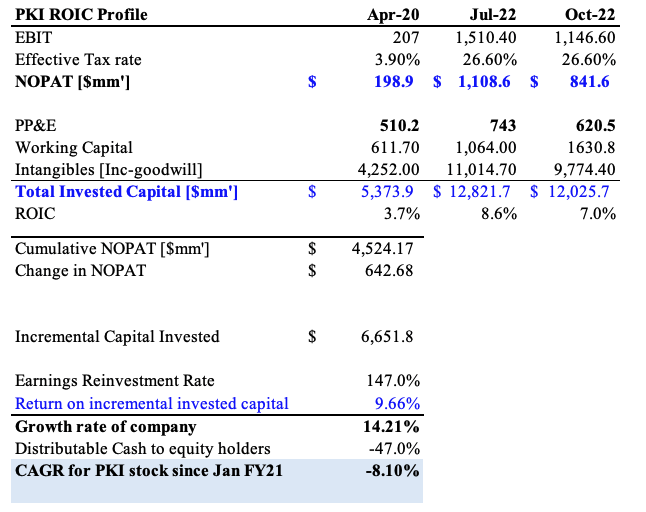

PKI managed to grow its top-line from $3.78Bn to $5Bn in FY19-21, and, despite a wind-back in Covid-19 sales, is forecast to clip $4.59Bn in FY22E, a 9.5% YoY decline. The divestiture will surely have an impact in 2023 as well. These don't explain the ~8% CAGR decline in its share price since January 2021, however. You'll note in Exhibit 2, that, over the period from Q1FY20-Q3FY22, the company generated $642 in additional growth in NOPAT. But it required $6.6Bn in investment to do this, a 9.6% ROIIC, resulting in a growth rate of 14.2%. The problem with this, however, is that it took a reinvestment of 147% of post-tax earnings to achieve this, leaving a negative balance left for shareholders. No wonder there was a re-rating.

Exhibit 2. PKI incremental return on invested capital with heavy reinvestment required to grow

{kind=link}

We'd note that the company is still valued at more than $21Bn in enterprise value, however. And this has a lot to do with PKI's acquisitions over the previous years. PKI has managed to grow its top line and earnings over the last 10 years at a steady pace, and we'd estimate it knows how to manage its asset base well, strategically acquiring high-margin or complementary businesses to tuck-in to its portfolio. However, we need to measure its ability to make value-accretive acquisitions. Credit Suisse (2014) present a framework to value this, that links EP, ROIC and the value-add from acquisitions. We use this process in evaluating the value accretion a firm has generated from its acquisitions and will do this here for PKI.

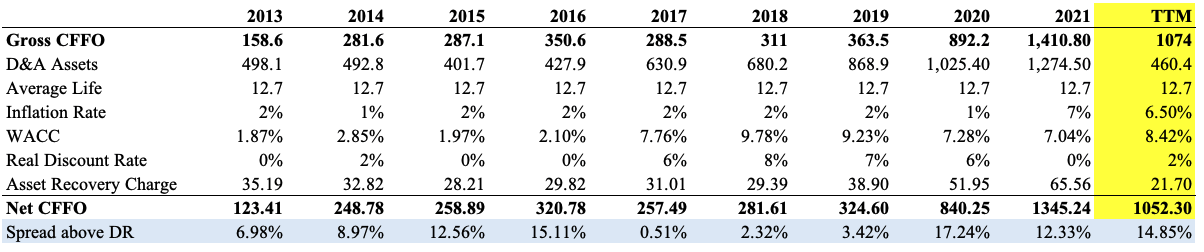

First, we calculate the cash-flow return on investment ("CFROI") of acquisitions per year and then use this to estimate a transaction CFROI, and transaction EP. Remember, growth below the cost of capital is destructive to value, whilst growth at the cost of capital is 'value-neutral'. So we need a positive CFROI to justify its worth in the company. We calculate CFROI by taking the gross CFFO per period, then recalibrating it to a net figure by removing the asset recovery charge at the real discount rate (Exhibit 3). Note, we took the average weighted life of both depreciating and amortizing assets for PKI from its 10-K's since 2013, and the last report in Q3 FY22, and assumed this across the entire testing period.

You can see that PKI supports a high and growing CFROI from its transactions (Exhibit 4). It is presented as a spread above the real discount rate in the Exhibit 3. Moreover, the cash acquisitions are shown in Exhibit 4, where 2017 and 2021 were heavy years. Thankfully, the CFROI from the transactions has been positive, as mentioned.

Exhibit 3. Net CFFO with CFROI less the real discount rate ("DR")

Note: For more on asset recovery charge, net CFROI, see: Credit Suisse (2014): "Wealth Creation Principles Introducing HOLT Economic Profit". Inflation rate taken as annual per year. Prior to 2017, discount rate used as yield on UST 10-year. (Data: PKI SEC Filings 2013-Q3 FY22)

{kind=link}

Exhibit 4.

Data: PKI SEC Filings

PKI isn't averse to paying a hefty premium for its transactions, however, evidenced by the goodwill acquired. Goodwill represents the premium in which a firm 'overpays' for an asset, whilst also factoring in non-measurable assets, such as customer relationships, reputation, branding, etc. Goodwill also represents a transfer of wealth from PKI to the target company's shareholders and is unrecoverable. Hence, as investors, we are penalized for goodwill. Alas, we need to understand if the acquisition EP generated from PKI's acquisitions has compensated us for this penalty.

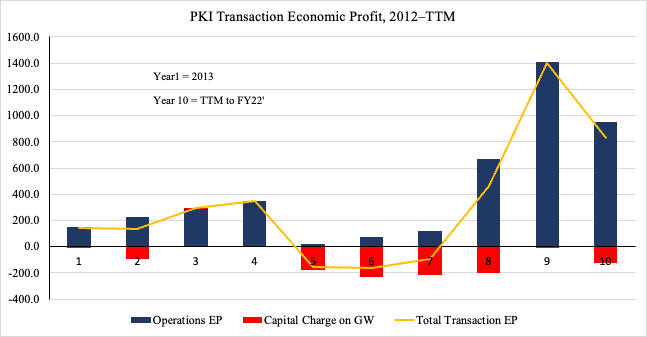

The above calculations fail to capture goodwill, and so we need to factor this in order to do so. Moreover, goodwill is a sunk cost - and our transaction EP calculations will have these sunk costs anchored into it. Cumulative goodwill grew from $2.1Bn in 2013 to $35Bn in the TTM, a 1,500% increase. This is large, but, the question is, has PKI converted this into value for equity holders?

You'll see in Exhibit 5 the company has generated more in EP for its operating assets than what was paid to acquire these. Operations EP grew from $150 in 2013 to $1.4Bn in 2021 and is at $951mm for the TTM. The total EP for its transactions sat at ~17% in the TTM as well. Hence, the EP growth from each acquisition more than covered the investor penalty for goodwill over this time.

Exhibit 5. Most of the transaction EP derived from operations, not acquisition of goodwill

{kind=link}

Consequently, whilst the heavy reinvestment of post-tax earnings is noted, we'd also highlight PKI is generating substantial value from the allocation of capital to acquisitions, and these may yet to flow through until years to come, as seen in the trends of Exhibit 5. This supports our buy thesis.

In short

Whilst it's been a difficult 12 months for PKI on the chart, its recent moves to free up additional liquidity should reduce its capital intensity and promote a re-appraisal from the market, once completed. This move could leave more distributable cash to equity holders. PKI is also a good steward of capital in allocating towards its acquisitions, generating substantial EP over the years, compensating for the goodwill acquired. Net-net, we continue to rate PKI a buy, with a price target at $155.

For further details see:

PerkinElmer: Capital Budgeting A Key Factor To The Investment Debate