PKI - PerkinElmer: Remains A Buy For Long-Term Positioning

2023-04-26 06:24:40 ET

Summary

- PerkinElmer remains a long-term buy based on business economics and valuation.

- The firm looks set to profit from a leaner cost structure and less capital-intensive makeup.

- Returns on capital are strong and could benefit from the above point as well.

- Net-net, rate buy.

Investment Summary

There still appears to be capital appreciation in the engine for PerkinElmer, Inc. ( PKI ) over the long-term in my informed opinion. In my last publication in January, an illustration of how PKI has generated value through M&A activity was provided. I'd encourage you to read it, because the same investment tenets apply for the firm today.

For starters, PKI will fully divest its analytical and enterprise solutions arm this year. I've got Opex, CapEx requirements cooling right off from this.

The firm's leaner operating structure from FY'23 is a torque-generator to operating leverage. Variable costs will shrink compared to total business expenditures, leaving fixed expenditures to hold up company growth. I believe PKI can do $3.1Bn in top-line revenues this year as Covid-19 turnover finally diminishes, and key divestitures settled. I'd call earnings of $691mm or $5.48 per share on this, after 10% YoY growth in operating income and 17% YoY growth to $844mm in NOPAT.

PKI is more expensive than the healthcare sector as I'll show, but if all goes well, in FY'23 could spin off $855mm in owner earnings at the end of this year. Consensus has it valued at 26x forward earnings and I do see some upside on this at 28x consensus earnings, or 20x my own estimates, and that's about what I'd be prepared to pay. Net, net, I rate PKI a buy at $143 per share.

PKI Unit Economics

PKI will complete the divestiture of its analytical and enterprise solutions arm in FY'23. One less artery to feed from the business heart chamber is not a bad thing in my opinion. The leaner cost structure with less capital intensity could easily translate to gross margin upside and earnings growth. That, plus the smaller CapEx and NWC requirements to free up capital for growth initiatives. Two-billion in freed up capital, to be precise:

Once the deal is closed...[w]ith these proceeds and the cash we expect to generate, we will have more than $2 billion of additional unencumbered cash available to deploy over the next three years without taking on any new debt.

OpEx lifted to $1.18Bn in FY'22 and reflected the contribution of Covid-19 revenues, typically a lower margin business [now that we're out of the pandemic, we should stop hearing these kind of headwinds]. Growth CapEx also pushed lower to $85.6mm, but surged as a percentage of revenues to ~2.6% [Figure 2].

Regarding the better cost structure - segmentally, I'd be looking for another push above $1.2Bn in EBIT this year to signal PKI's success on this. I also project $75mm in CapEx this year with additional $341mm in NWC density. Since FY'21, the firm has compounded its discovery & analytical solutions ("DAS") segment at 29% [Figure 1] and this could surprise across earnings this year. I've got the firm to hit $3.1Bn at the top-line in FY'23, above management's and consensus' $2.95Bn. I am not worried about this, as PKI consistently beats the Street's numbers.

Fig. 1

Note: Segment Operating Income presented gross of Amortization, Depreciation, and other operating and non-operating expenditures. (Data: Author, PKI 10-K's)

{kind=link}

Fig. 2

Data: Author, PKI 10-K's

Looking at the balance sheet, $7.3Bn of equity is holding up $14.1Bn assets, totalling 0.5x leverage. The firm turns inventory over 6-7x each year and I project this trend to continue. Cash conversion cycle was 143 days last year, likely to stay around 120-140 over the next 3-years in my estimations. That PKI can grow revenues with this level operating efficiency is bullish. Further, cash collection is now integral, given:

- Cost inflation for manufacturers

- Tightening payment terms/cycles

- Working capital and liquidity thinning up on tight money.

It is paramount for intelligent investors to scrutinize their companies on the merits of cash generation. In particular, those who've had Covid-19 exposure will likely revalue inventories and free up income on the margin as a result. On the other hand, those firms with tight cash collection will front-run those struggling to convert sales at the CFFO line. In my opinion, PKI is set to have less cash tied up in working capital in FY'23-'25 after restructuring (see: Figure 6). I believe this could take a few years to be fully realized, but is a good sign nonetheless.

Fig. 3

Data: Author, PKI 10-K's

PKI Business Economics

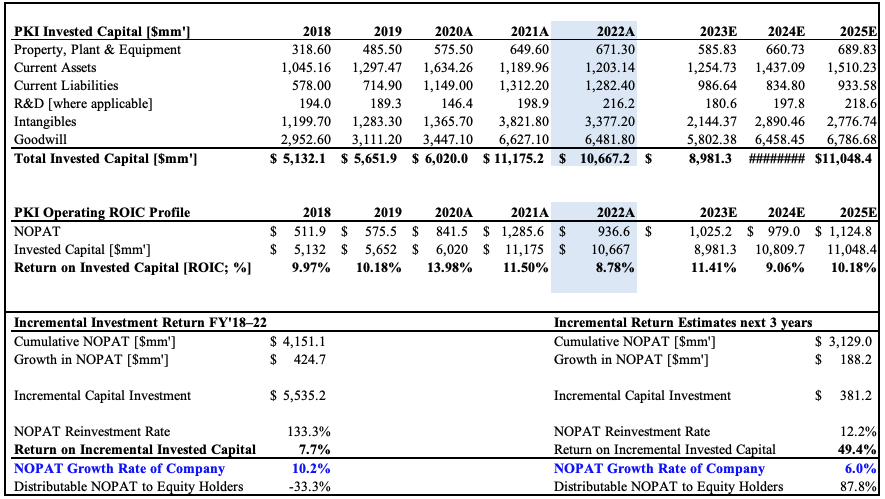

Over the last 3-years PKI has generated simply exceptional returns on incremental capital. In FY'19, it was 13.1%, in FY'22, it was 72% - appetising change of numbers in my opinion. Further, the returns on existing capital are commendable too. From FY'18, the company has averaged 10.8% per year on its invested capital, generating an average 4.6% profit above the cost of capital [Figure 4].

My numbers estimate a much lower capital density for PKI going forward, with the divestiture settled. It isn't unreasonable to see 10-11% in ROIC per year into FY'25 in my opinion. This would call for a $381mm additional investment, to grow NOPAT by $188mm and cumulative NOPAT of $3.1Bn over the 3-years. With lower capital intensity, less NWC requirements and smaller reinvestment rate, capital productivity is the main beneficiary. PKI can focus on returning cash to shareholders without jeopardizing its growth efforts.

Contrast this from FY'18 - 7% return on incremental capital with incremental investment of $5.5Bn, with $424mm in NOPAT growth. This took a lot of free cash flow from shareholders, despite the firm's dividends. By leaning up, I'd call for 87% of NOPAT to remain distributable to equity holders - promoting strong earnings growth, and potentially a higher multiple from the market. I believe the firm can generate $730mm at the bottom-line in FY'25, and throw off $1Bn in free cash to shareholders in the same year (figure 6).

Fig. 4

{kind=link}

Such strong returns cannot go unnoticed. The opportunity cost of risk capital now resetting again. Investable companies must generate a return on the capital it invests above the market's return to create shareholder value. By any means, 9-11% projected ROIC from PKI could generate 2-3 points of economic profit each year if:

- The firm's WACC hurdle remains at 7-8%, and

- The hurdle rate (UST 10-year yield + S&P 500 forward earnings yield) remains at 9-10%.

My numbers also point to the firm compounding NOPAT at 6% per year over the time period in Figure 4.

Valuation

PKI looks to be placed at a premium to peers at 24x forward earnings and 2x book value (note, this is 24x my FY'23 numbers, equating to 26x consensus eps estimates). Related to the cash flow points raised earlier, it trades at just 13x forward CF, below the sector's 16x.

The question I'd like to know is whether PKI is cheap versus the sector or not. In order to find this, it's not suffice to just compare the two sets of market multiples. A deeper analysis is required. Importantly, the healthcare sector is actually very cheap at the moment, despite trading at 23x earnings. Let me explain why.

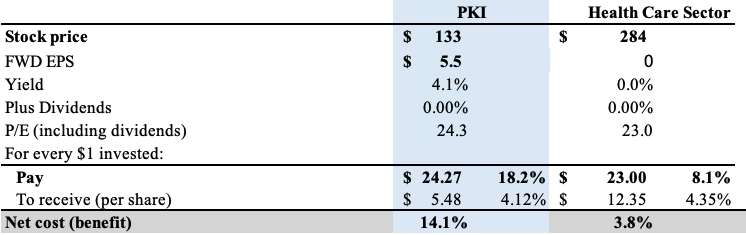

The P/E ratio tells us many things. One medium it shows what investors are paying for every $1 of a firm's future earnings. A 24x P/E says that investors are paying $24 for every $1 in future earnings for PKI. This underlines what we are really investing in the business for. Recall, the valuation of a business to an equity investor is the cash he or she can pull from it over the investment horizon. Naturally, we'd want to buy each $1 of forward earnings for as cheap as can be. For that, we'd receive 4.12% in yield on these profits.

There's a net-cost/benefit, however. If we buy PKI today, and pay $24 per $1 or earnings, we'd be paying 18.2% of its quoted market price of $133 at the time of writing to buy 4% earnings yield ($24/$133 = 0.182). So, paying 18.2% to get 4.1%, otherwise a net cost of 14.1% (18.2% - 4.1% = 14.1%). For the health care index ( IYH ) the net cost is just 3.8% [Figure 5]. Subsequently, the healthcare index is cheaper by a far wider margin than what's shown in the basic P/E differences, 3.8% net cost versus 14.1% net cost. It is critical to know the cost of $1 of earnings is, just as it is to know what $1 of investment will yield in terms of ROIC and earnings growth.

Buffet touches on this with the $1 test. You invest $1,000, the opportunity cost/cost of capital is 7%. The investment needs to produce $70 in earnings to perpetuity to breakeven, and >$70 for profit. For instance, $100/0.07 = $1,428; $060/0.07 = $857. Said another way, it needs to return at least 7% - $1,000 x 0.07 = $70. If you get 8+%, you've created value, below, you've eroded value. In that vein, it's clear that PKI is coming towards the top of its valuation to warrant a strong buy.

Fig. 5

{kind=link}

Projecting owner cash flows out to FY'28 at a 3% terminal rate, and 10.6% cost of equity, I see upside in PKI to $143 per share, of $18.15Bn market cap. This throws off a 20.8x P/E, which could be a risk factor given the market's multiples. I'd be looking for ~5% forward yield on FCF to shareholders if this comes to fruition. At 11% hurdle rate the stock is valued at $137, also a point of contention.

Fig. 6

{kind=link}

Conclusion

The investment debate can best be summed up with the following points:

- PKI will have a leaner cost and maintenance CapEx structure going forward.

- This could reduce capital intensity and lift profitability, including operating leverage and ROEs.

- The rate at which PKI collects cash is sound and I estimate this to continue going forward.

- PKI's business economics are attractive with high returns on capital that outpace the hurdle rate.

- This means it can continue distributing cash to shareholders whilst continuing its growth rate.

- The firm is pricier than the Healthcare sector, especially when looking at a per-dollar of earnings basis.

- There's upside potential to $137-$143 per share in my estimation.

With these points in mind, I continue to rate PKI a buy. I will be watching the price differentials closely at the $140-$145 mark any position will need tending to. I look forward to providing further coverage.

For further details see:

PerkinElmer: Remains A Buy For Long-Term Positioning