ESTE - Permian Resources: The Best Permian Pure Play On The Market

2023-10-08 02:17:04 ET

Summary

- Permian Resources recently announced plans to acquire Earthstone Energy, creating one of the largest oil and gas producers in the Permian Basin.

- Permian Resources is undervalued relative to its Permian peers, and the recent Exxon Mobil announcement to buy Pioneer will cause valuations to increase.

- Permian Resources has a disciplined balance sheet and a track record of strong growth in annual cash flows. The Earthstone acquisition will likely put the company's growth in overdrive.

- Permian Resources has an enviable position staked out in Lea and Eddy counties in New Mexico.

Permian Resources ( PR ) is an oil and gas exploration company solely focused on the Permian Basin. Before I begin, let me warn you not to look at the price of Permian Resources following oil's crash in 2020. It reached a low in 2020 of 30 cents. Today, the company trades around $13 per share and has a market cap of $7.33 billion. Don't worry, you wouldn't have been able to buy Permian Resources in 2020...you would have had to buy it in two parts. That's because the company Permian Resources was the result of a merger between Centennial Resource Development and Colgate Energy Partners (which was a private company) in 2022.

The company has many exciting things going for it, not the least of which is the fact that it is purely based in the Permian Basin. If you've read any number of my articles, then you know I am bullish on the Permian Basin. As I'm writing this article Exxon Mobil ( XOM ) is in talks to potentially buy Pioneer Natural Resources ( PXD ), making a huge move into the Permian Basin. And just like Exxon Mobil, I'm bullish because it is where companies are focusing the lion's share of their capital as it is delivering superior risk-adjusted returns relative to other projects around the United States and the world.

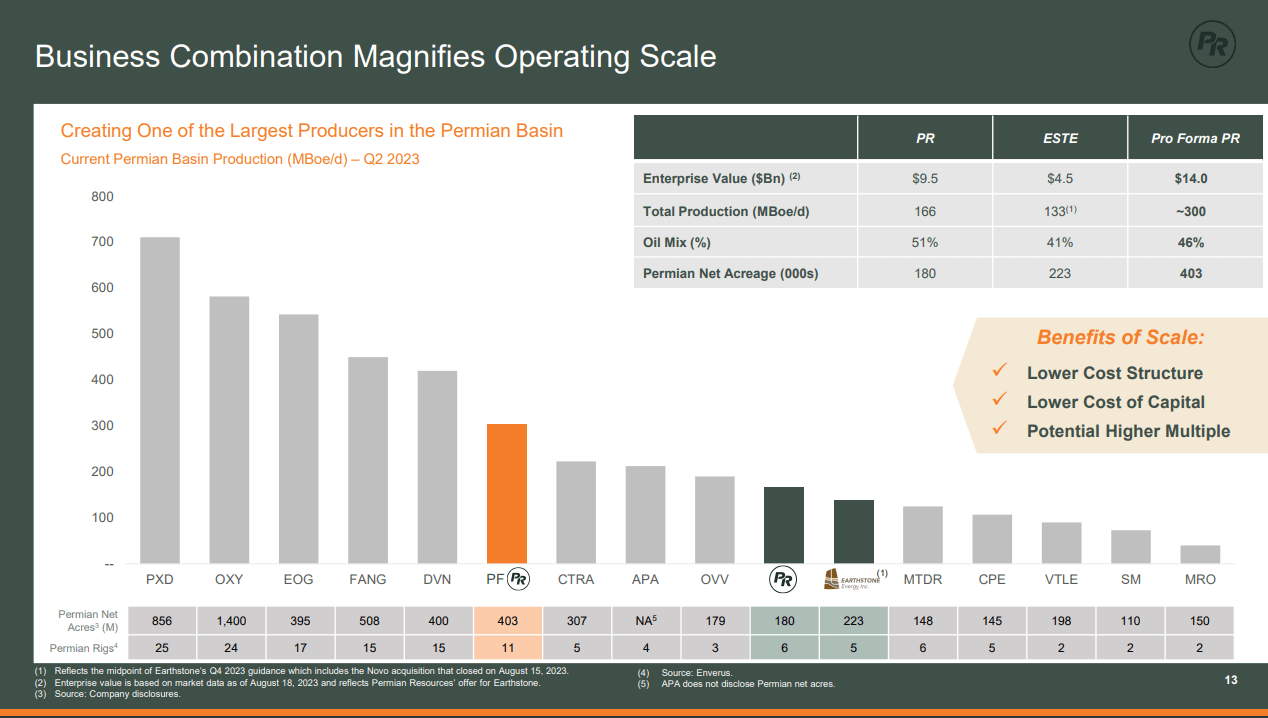

In August 2023, Permian Resources announced its own acquisition. Prior to the announcement, Permian Resources held 180,000 net leasehold acres and another 40,000 net royalty acres in the play while producing 137,000 barrels of oil per day. They were already one of the largest publicly traded Permian pure-plays available.

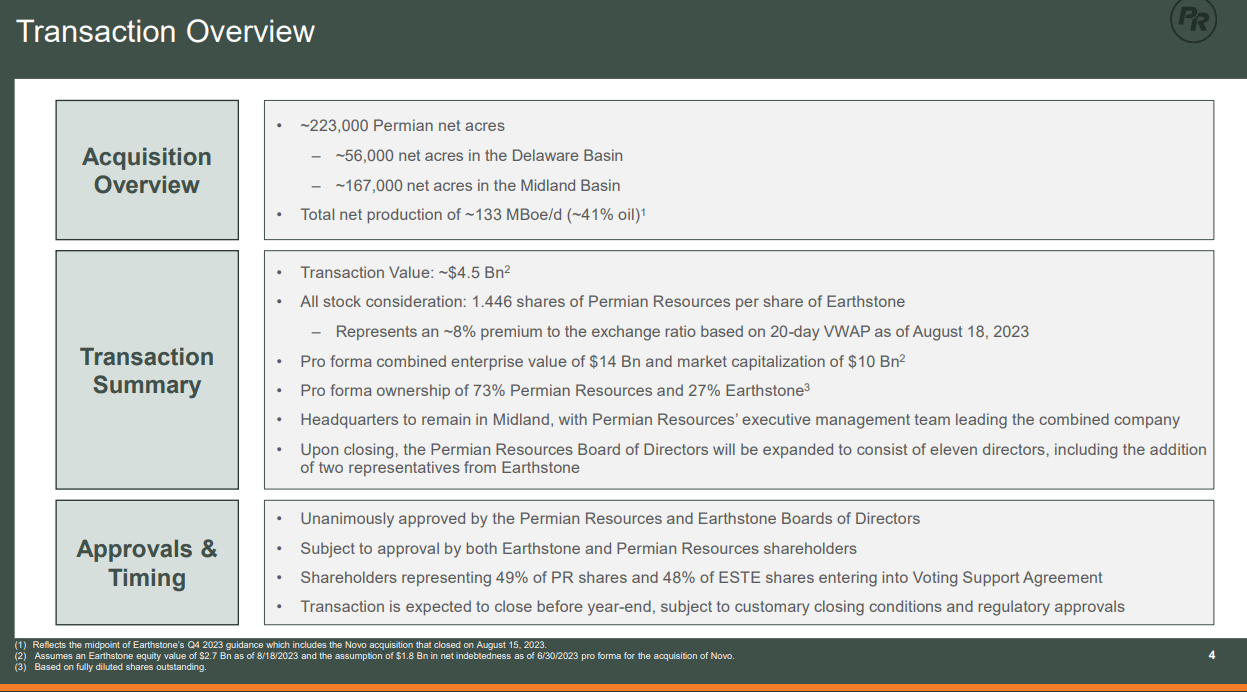

Then, the company announced that they were acquiring Earthstone in an all-stock acquisition. The company is expected to close on the acquisition sometime before the end of the year. The company is creating 1.446 new Permian Resources shares in exchange for each Earthstone share. Since the news of the acquisition occurred, the stock has traded relatively flat.

Here is a look at where the company was focused in the Permian Basin before the acquisition. Notice that one of the company's heavy focuses is in Lea and Eddy Counties. That is important to understand.

Permian Resources Areas of Operations (Permian Resources Website)

Here is the EIA's chart showing the growth in oil production from the Permian Basin. There was very little production from Lea and Eddy Counties prior to the shale oil/horizontal oil drilling boom but today, it has been one of the big stories from the Permian Basin, even grabbing the attention of the Energy Information Association.

EIA Permian Oil Production Chart (EIA)

Acquisition

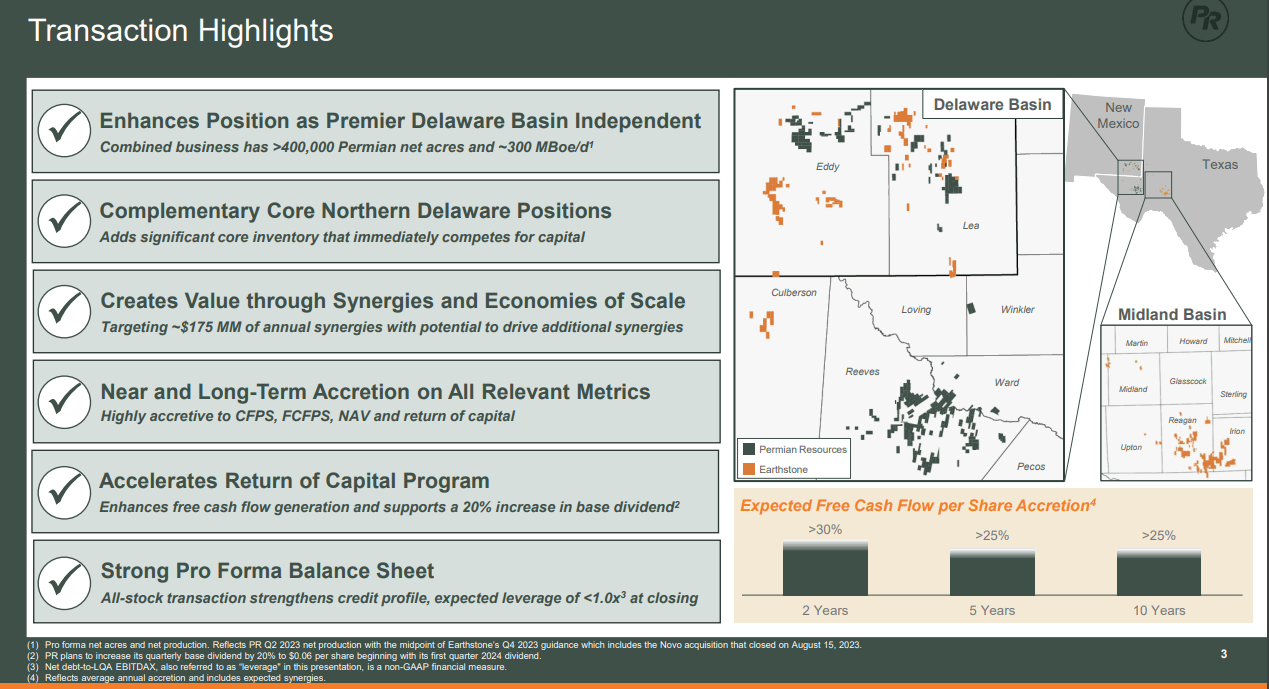

In the image below, Earthstone acreage is represented in the orange. Just from guessing, the company roughly doubled its footprint (not net) in Lea and Eddy counties(Northern Delaware). The other big addition was a chunk of acreage in the Midland Basin portion of the larger Permian Basin. All-in-all this increased Permian Resources acreage to over 400,000 net acres and more than doubled production to 300,000 barrels of oil equivalent per day.

{kind=link}

The headquarters of the company is located right in the heart of the Permian in Midland, Texas. The majority of the increase in "net" acres comes to the company in the Midland Basin as the Earthstone operating interests in the Northern Delaware were likely only a partial interest. Nonetheless, the addition of acreage in the Delaware Basin was still substantial.

Permian Resources Earthstone Transaction Overview (Acquisition Presentation)

{kind=link}

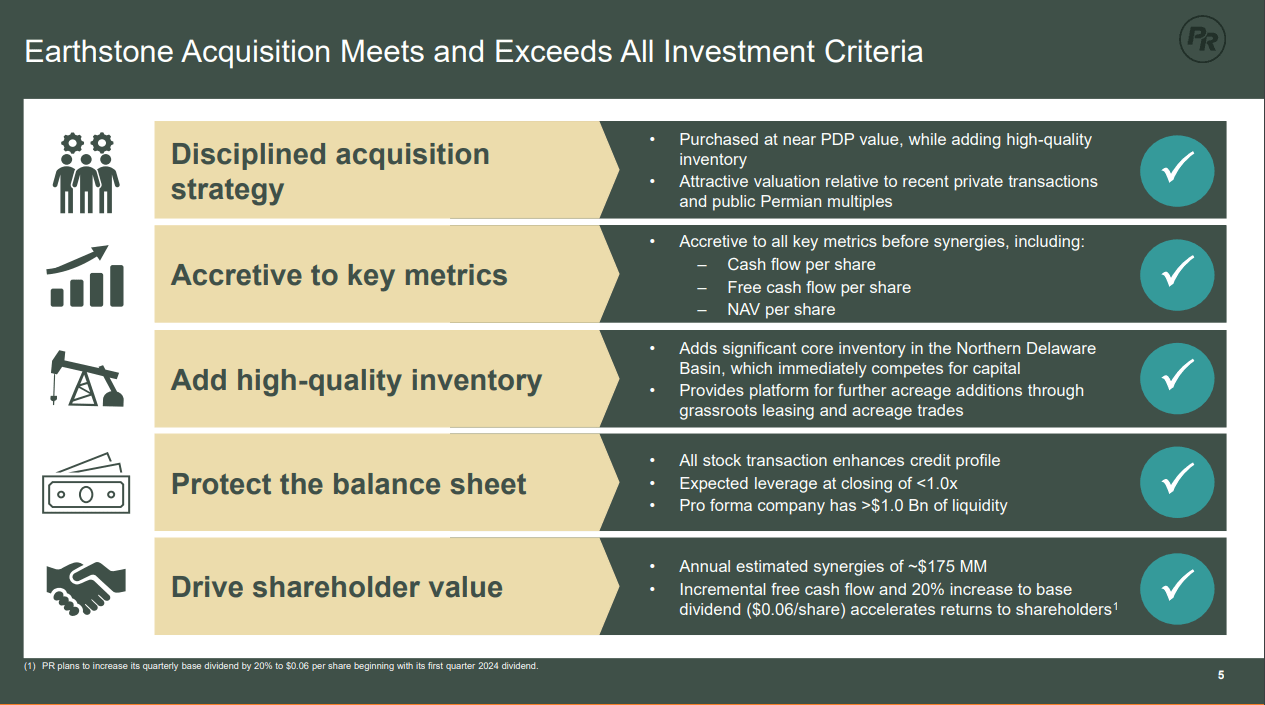

The management team believes the combination of these two companies unleashes the possibility for greater returns in the future. The company believes the acquisition, despite being funded with share dilution, will be accretive to cash flow per share, free cash flow per share, and NAV per share. As an investor, these are what we want to see from a company, especially if it took share dilution to make the acquisition.

Earthstone Acquisition Highlights (Acquisition Presentation)

{kind=link}

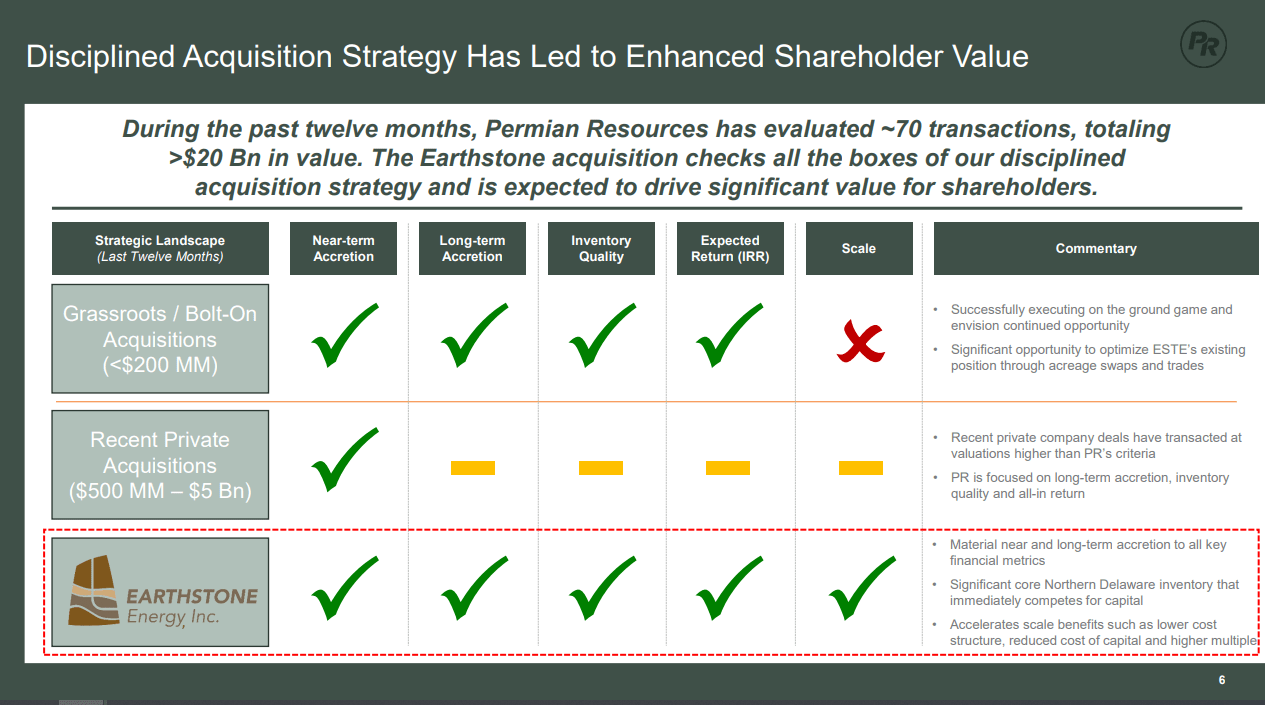

The Permian Resources team evaluated many different options to increase shareholder value and Earthstone was the acquisition that checked all of the boxes. Notice that the company was focused on acquiring acreage in the Northern Delaware region as they know that is the premier acreage in the play. As the slide says, it "will immediately compete for capital."

Earthstone Acquisition Checks the Boxes (Acquisition Presentation)

{kind=link}

Operating Cash Flows

The company's record of cash flows is about to dramatically change, however, it is still helpful to look at their prior cash flows to see if the management team has operated well. In 2018, before the companies were combined, the company was creating negative free cash flow as they were ramping up production with more opportunities to deploy capital than capital available.

We can see that following the plunge in oil in 2020, the company's cash flows continued on their upward trajectory. I would expect these growth rates to continue into the foreseeable future.

Permian Resources Cash Flows

| $ millions |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM 2023 |

| Operating Cash Flow |

| 670 |

| 564 |

| 171 |

| 526 |

| 1,372 |

| 1,803 |

| CapEx |

| (1,217) |

| (968) |

| (328) |

| (327) |

| (784) |

| (1,378) |

| Free Cash Flow |

| (547) |

| (404) |

| (157) |

| 199 |

| 588 |

| 425 |

Earthstone was a little behind Permian Resources in its growth trajectory. Whereas Permian Resource began outspending operating cash flow in 2018, Earthstone didn't begin to do the same until 2021-22.

Earthstone Cash Flows

| $ millions |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM 2023 |

| Operating Cash Flow |

| 102 |

| 126 |

| 131 |

| 230 |

| 1,018 |

| 1,158 |

| CapEx |

| (183) |

| (205) |

| (88) |

| (427) |

| (2,018) |

| (1,235) |

| Free Cash Flow |

| (81) |

| (79) |

| 43 |

| (197) |

| (1,000) |

| (77) |

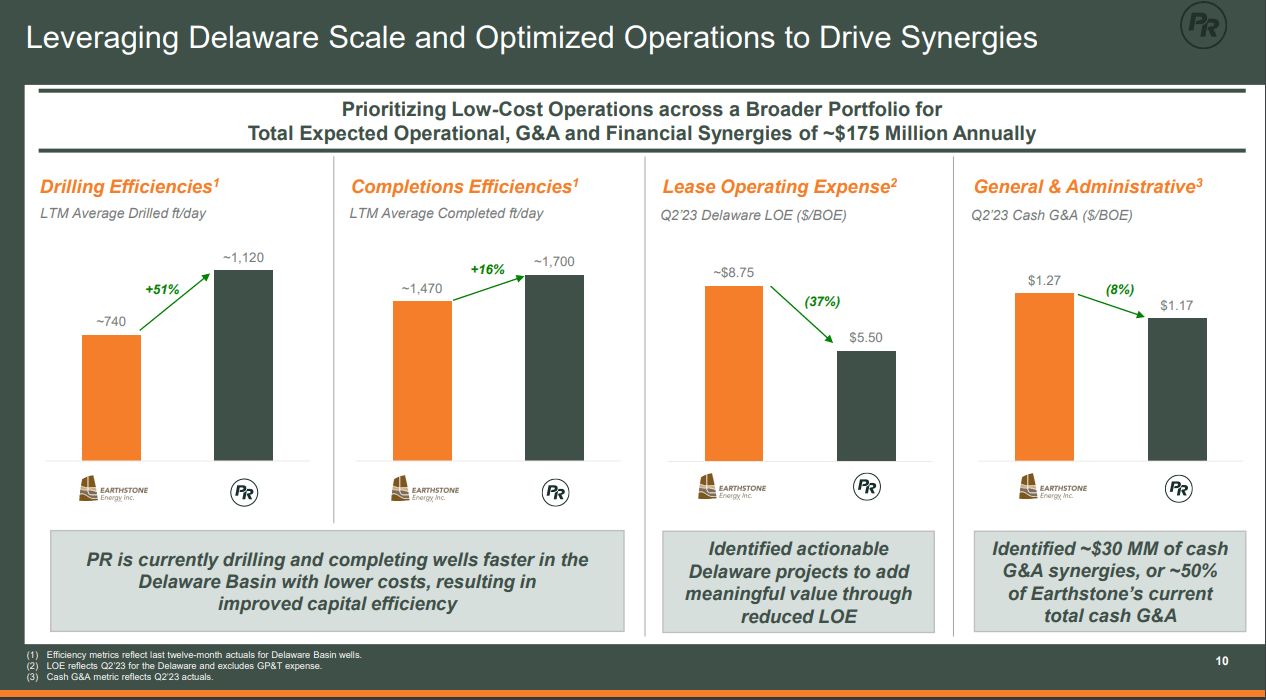

The combined company hopes to save $175 million annually through synergies. You can see here that according to these metrics, Permian Resources has been the more efficient operator. Naturally, as Permian Resources transfers this knowledge into savings for Earthstone operations, it should spell greater returns for investors.

Permian Resources Optimize Operations (Acquisition Presentation)

{kind=link}

Balance Sheet

The company has maintained a strong discipline with its balance sheet. In the acquisition, Permian Resources assumes all debt of Earthstone, which will change the table below. However, this gives you a picture of how the company has managed its balance sheet with strict discipline, even in the face of negative free cash flow during 2018 and 2019.

| $ millions |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Q2 2023 |

| Assets |

| 4,260 |

| 4,688 |

| 3,827 |

| 3,805 |

| 8,493 |

| 8,926 |

| Debt |

| 1,016 |

| 1,418 |

| 1,223 |

| 1,054 |

| 2,836 |

| 3,000 |

| Debt-to-Asset Ratio |

| .24 |

| .30 |

| .32 |

| .27 |

| .33 |

| .34 |

The combined company's balance sheet will have a debt-to-asset ratio of roughly .35, keeping in line with Permian Resources' debt-to-asset ratio prior to the acquisition.

Shares Outstanding

If you choose to invest in Permian Resources, understand that they have actively used share dilution as one of the tools in their tool belt to grow the company. This is a double-edged sword. If the company deploys the capital with discipline, then this is a fine strategy. But sometimes the market does not look favorably on this strategy.

If my math is correct, the new company will have roughly 488 million shares outstanding after the acquisition clears.

| millions |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Q2 2023 |

| Shares Outstanding |

| 267 |

| 277 |

| 277 |

| 310 |

| 323 |

| 335 |

Permian Resources Relative Scale

Permian Resources is currently valued at less than $10 billion and the combined company at today's share prices will have a valuation that still falls right at $10 billion. Compare this to the companies like Devon Energy, which have a market cap of nearly $28 billion. Granted, Devon Energy has other plays that it is involved in, but the Permian is Devon Energy's main focus just as it is for many E&P companies these days. One can see how Permian Resources has the potential to quickly scale to the size of Devon Energy ( DVN ).

Permian Resources Relative Footprint in the Permian Basin (Acquisition Presentation)

{kind=link}

Valuation

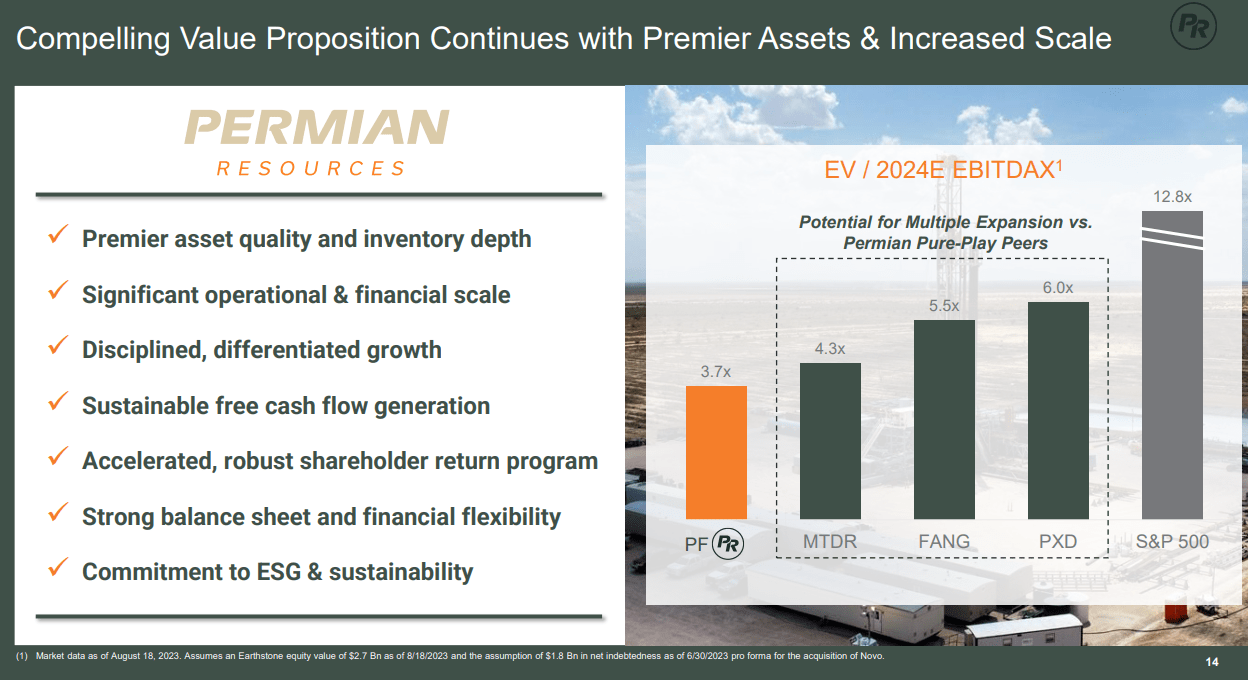

The company is currently undervalued relative to some of its peers. And now with Pioneer getting acquired by Exxon Mobil at a premium, it stands to reason that we will begin to see Permian Resources receive higher multiples.

Permian Resources Relative Valuation (Acquisition Presentation)

{kind=link}

Risks

Permian Resources is on solid footing. They have one of the better balance sheets in the industry and have an enviable position staked out in the Northern Delaware Basin where some of the best rates of return in the Permian Basin are found. But as with any investment, there are still risks involved.

First, there is always a risk that the merger doesn't go through. Given that they were able to announce their acquisition prior to Exxon's acquisition, they likely received a better deal acquiring Earthstone ( ESTE ) than they would have otherwise. This is a credit to the Permian Resources management team and their foresight. However, if the acquisition doesn't go through, then they will likely have to pay a higher price if they were to pursue the Earthstone acquisition further.

Second, oil prices could decline. However, I don't see that being a big risk. I've spoken about energy demand in previous articles , and it shows no sign of decreasing, even with the giant government-funded push towards electric vehicles. And when you do the math, depending on where you live, electric vehicles rarely justify the added cost to purchase. As the transition towards electric vehicles continues, it will take longer than we all expect.

Third, regulatory risk in the oil and gas industry is at the front of everyone's mind. It is keeping many people away from the undervalued oil industry, but I do not see this as a big risk in the near term. I would say that a person should be leveraged/invested in the Permian Basin for at least the next 5 to 6 years. The regulatory risks can be reevaluated then.

Fourth, as I already pointed out, share dilution will also be a risk when investing in Permian Resources.

Conclusion

Permian Resources is a strong buy at the moment. I currently do not hold any investments in the oil and gas sector, even though this is what I cover mostly. However, if I was going to invest in one company, it would be Permian Resources. Across the board, they have developed a track record as a company that understands the necessity to focus primarily on the rates of return on capital invested.

I didn't cover it in this article, but the management team at Permian Resources is young. Despite being young, you can witness that the decisions being made, show a maturity beyond their years. And if they remain an independent company, this management team may deliver some serious alpha to your portfolio during their careers. The best investments happen by knowing and investing in the people, and not just the projects themselves. After all, the capital projects are created/found by the people.

Furthermore, with the most recent acquisition of Pioneer Resources by Exxon Mobil undoubtedly makes Permian Resources a takeover target at some point. There's no telling when that could happen, but with around 400,000 acres in the Permian Basin, it would add scale to any existing major or mid-major oil company. The management team at Permian Resources is focused on driving value and so if the right opportunity presented itself, I'm sure the management at Permian Resources would capitalize on it. But again, this could happen next year, or it could happen 10 years from now.

Regardless, investors are sitting on one of the larger players in the Permian which will continue to pay out greater and greater dividends as their cash flows from the play continue to mature.

Once again, currently, Permian Resources is a strong buy.

For further details see:

Permian Resources: The Best Permian Pure Play On The Market