PRNDY - Pernod Ricard: Quality Spirits Company Trading At An Undemanding Valuation

Summary

- The news flow from Pernod has been positive in recent months, closing accretive acquisitions and kicking off the fiscal year with a solid set of results.

- The balance sheet capacity should support more buybacks or M&A, though the net debt levels also need to be managed given the hawkish rate environment.

- Relative to the earnings growth potential and to peer valuations, Pernod stock still offers ample upside potential.

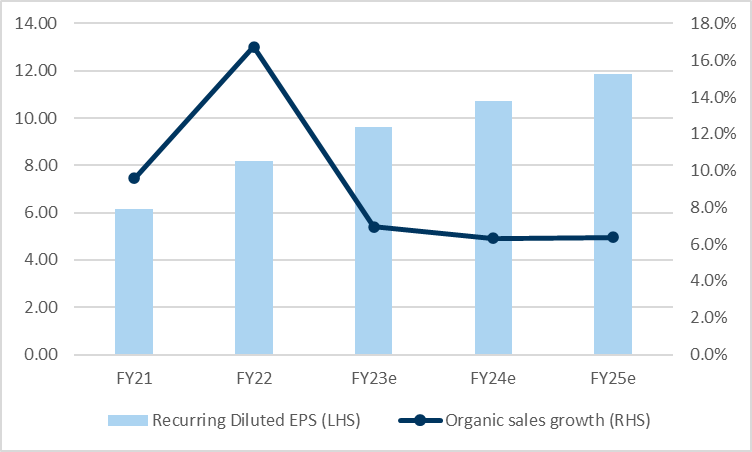

Having grown into its position as the second-largest global wine and spirits company through a combination of organic growth and M&A, the Pernod Ricard ( PDRDF ) growth runway remains compelling. In the mid to long term, Pernod Ricard continues to offer investors a steady double-digit % EPS growth algorithm, along with consistent FCF generation through the cycles. With the net debt/EBITDA already within a comfortable range of around 2.5x, there is also ample capacity for more capital return beyond the EUR500-750m of buybacks set for FY23. Alternatively, bolt-on acquisitions are on the table as well, with the recent Sovereign Brands and Código deals signaling management's appetite here. While concerns about slowing premiumization trends in a weaker macro are perhaps warranted, valuations are also well below prior highs, and thus, I still see a favorable risk/reward. Continued momentum on the growth and margin delivery should drive a narrowing discount relative to key peer Diageo ( DEO ).

{kind=link}

Ramping Up M&A to Strengthen the US Portfolio

Pernod has announced two key transactions in recent months - the consolidation of the Sovereign Brands wine and spirits portfolio from November, as well as the purchase of the Co?digo 1530 ultra-premium and prestige tequila portfolio. The expanded stake in Sovereign Brands (note the original minority stake was acquired in September 2021) is particularly interesting. Like Co?digo 1530, it moves Pernod up the quality ladder, although the Sovereign Brands deal also gives the company full control over their joint incubation projects months before an initial brand launch.

The financial terms were not disclosed, but per current guidance, the consolidation of the Sovereign Brands portfolio will yield low-single-digits % accretion to group adj EBIT. This seems reasonable, given the acquisition adds quality and scale to Pernod's US portfolio offering, a key laggard in recent quarters. In addition to extending the US segment's growth runway, the Código and Sovereign's premium brands could potentially help to scale the broader portfolio as well. It remains early days, though, and pending color on the potential synergies, I wouldn't pencil in too much beyond the official guide. Going forward, expect more growth M&A to rejuvenate the long-term prospects of the US portfolio (a source of relative weakness in recent times), as well as to build out the innovation pipeline further.

A Better-Than-Expected Start to the Fiscal Year

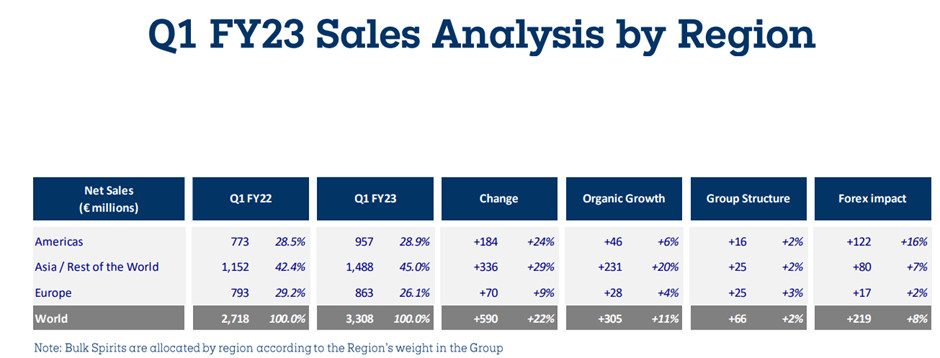

If the Q1 trading update was anything to go by, Pernod is off to a great start to FY23. The report was headlined by an above-consensus +11% organic sales growth, helped by ~7% of pricing gains. The underlying numbers would have been even better as well, were it not for the effects of phased shipments in the US. Asia continues to be the key growth driver, led by India (+21% growth), where consumer confidence is at an all-time high. China was also strong at +9%, as a strong Mid-Autumn Festival and double-digit % Martell Cognac growth more than offset the COVID headwinds.

{kind=link}

Higher energy cost increases will continue to weigh on costs, but Pernod management believes it has enough pricing power to offset much of the impact, citing the "strong +7% price effect" seen in Q1. While there was no quantified EBIT range provided, I view the commentary as an implicit guide of the double-digit growth in Q1 extending into the coming quarters as well. In addition, the commitment to the EUR500-750m buyback program (previously announced with its FY22 results) despite the recent M&A activity bodes well for the capital allocation outlook. While the buyback won't be needle-moving at <2% of the total market cap, the increasing balance sheet capacity bodes well for an upsized capital return in the coming quarters.

Sustainability-Linked Bond Issue Highlights Rate Headwinds

While Pernod has a sizable cash balance, it still runs a net debt balance sheet - the headline net debt to EBITDA stood at ~2.4x in FY22 but would have increased to ~2.5x if we include lease debt. Thus, management's decision to prioritize capital return and M&A over debt paydown means the risk of rate headwinds from higher floating and fixed-debt rate obligations is worth monitoring. Case in point - Pernod's recently issued EUR1.1bn sustainability-linked dual-tranche bond (comprising a 3.25% EUR600m six-year maturity and another 3.75% EUR500m ten-year maturity) came with a higher coupon than the group average of ~2.1%. The good news is that any earnings impact will be minimal from this issuance and that the next significant maturity is only in 2024, so Pernod still has some runway.

{kind=link}

Quality Spirits Company Trading at an Undemanding Valuation

Amid concerns about the state of the consumer and its appetite for premium brands heading into a potential recession next year, Pernod's diversified brand and geographic portfolio could prove invaluable in navigating the challenges. With Pernod also enjoying a good line of sight to achieving a double-digit earnings growth algorithm through FY25, the high-teens P/E valuation offers good value to long-term-oriented investors. Finally, the strong FCF generation presents incremental upside, paving the way for accelerated share buyback support (beyond the EUR500-750m in FY23), as well as more bolt-on acquisitions. There aren't any immediate catalysts to support a re-rating toward Diageo's premium valuation multiple, but good execution should be enough to narrow the gap over time.

For further details see:

Pernod Ricard: Quality Spirits Company Trading At An Undemanding Valuation