PSHZF - Pershing Square Holdings: Unloved Deeply Discounted Value Proposition

2023-06-22 00:24:30 ET

Summary

- Pershing Square Holdings is trading at a 37% discount to NAV, which is a deep discount for a fund that has shown an ability to drive strong portfolio returns.

- The PSH board has prioritized reducing the NAV discount and has executed various actions to achieve this, but the continued expansion of the discount is concerning.

- Arguments that the company lacks motivation to address the NAV discount lack merit.

- NAV growth combined with the potential for a narrowing of the PSH NAV discount creates the prospect of strong medium-term future share price gains and leads to a Buy rating for the stock.

Introduction

I first came across Pershing Square Holdings, Ltd. ( OTCPK:PSHZF ) ("PSH") in mid-2020, with my interest piqued by the stock then trading at a ~30% discount to NAV. Having casually monitored the company for a couple of years, and with the discount to NAV widening further, I decided that it was worth taking a closer look at what at first glance appears to be an attractive investment opportunity. Note that for ease of reading, in this article I use the terms 'discount to NAV' and 'NAV discount' interchangeably.

Company Background

Pershing Square Holdings, Ltd. is a closed-ended fund, listed on the London Stock Exchange ('LSE') and the Euronext Amsterdam exchange (I will refer to the company/fund as PSH from here on). PSH was incorporated in Guernsey in 2012 and commenced operations on 31 December 2012 as a registered open-ended investment scheme. In October 2014 the company converted into a registered closed-ended investment scheme. PSH commenced trading on Euronext Amsterdam in October 2014, with a subsequent listing on the LSE coming in May 2017.

PSH is a FTSE 100 index constituent, and currently ranks at around ~75 by market capitalization (which is ~£5.2bn). Despite being a market heavyweight, PSH seems to attract relatively little investor attention in the UK, perhaps due to the fact that the fund is run by a US-based manager and invests mainly in North American headquartered stocks.

The underlying strategy of the fund is to invest in a concentrated number of large capitalization companies (typically 8 to 12 holdings). The company's strategy is implemented by the appointed investment manager, Pershing Square Capital Management, 'PSCM'. PSCM was founded by Bill Ackman in January 2004. Ackman is a high-profile figure in the finance world and is perhaps best known for being an activist investor. Ackman stepped back from the CIO role at PSCM in FY22, but continues to be the group's CEO and retains ultimate control over decision making. Looking at the broader PSCM investment team, it is interesting that most of the analysts have a private equity and/or sell-side (notably Goldman Sachs) background. I would describe the investment team as experienced, with sufficient research capacity to manage a concentrated, high conviction portfolio.

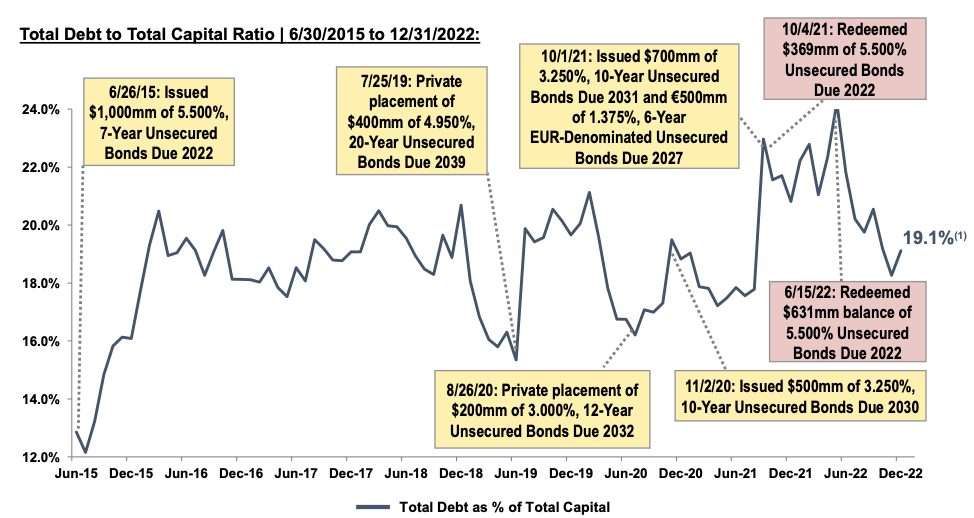

Other than the high level of portfolio concentration, there are two aspects of PSH worth noting that differentiate it from a more vanilla equity-based fund. The first is that the fund employs leverage. The second factor for investors to be aware of is that PSH will occasionally enter into hedging positions. Leverage and hedging both have potential to deliver higher rates of return, but equally these factors can also represent greater downside risk potential relative to an un-leveraged equities-only fund. I note that PSH redeemed $630m of bonds in FY22, which reduced the fund's debt ratio to a more comfortable level of <20% (refer to Exhibit 1).

Exhibit 1:

Source: PSH 2023 Annual Investor Presentation, slide 10.

{kind=link}

NAV History

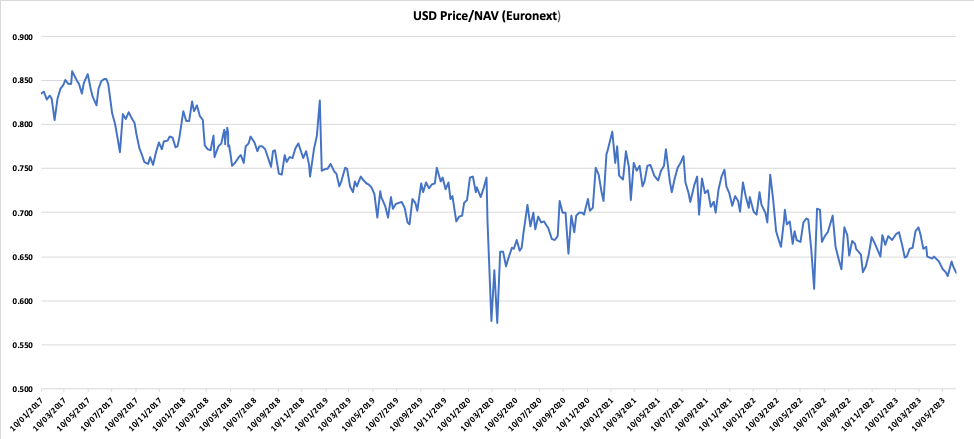

In Exhibit 2, I plot the NAV discount for PSH's Euronext Amsterdam listed, US$ denominated shares. The underlying data is taken from the regular NAV updates published by PSH. Excluding the sharp dip in March 2020 triggered by the pandemic, the current discount to NAV of around 37% is wide relative to prior periods.

Exhibit 2:

Source: analyst calculations based on PSH published NAV data.

{kind=link}

A narrowing of the NAV discount has the potential to drive a meaningful increase in PSH's share price. Given the depth of the current NAV discount, significant upside can be anticipated without relying on the delivery of heroic forecasts regarding the extent of the NAV discount closure. The average NAV discount over 2021 was ~26.4% - a recovery to that level of discount (all else held equal) would provide a return of ~16.5%. A narrowing of the NAV discount to 25% would deliver upside (all else held equal) of ~18.8%.

Could PSH Shares Return to NAV Parity?

In theory it is possible for PSH to entirely close its NAV discount. However, in practice this is a highly unlikely scenario. In my view, as a general rule (noting that there will always be exceptions to such) for a closed-ended fund to trade close to or above NAV two key conditions must apply: 1) investors must have a high conviction that the underlying portfolio will deliver strong future returns, and 2) management fees must be low.

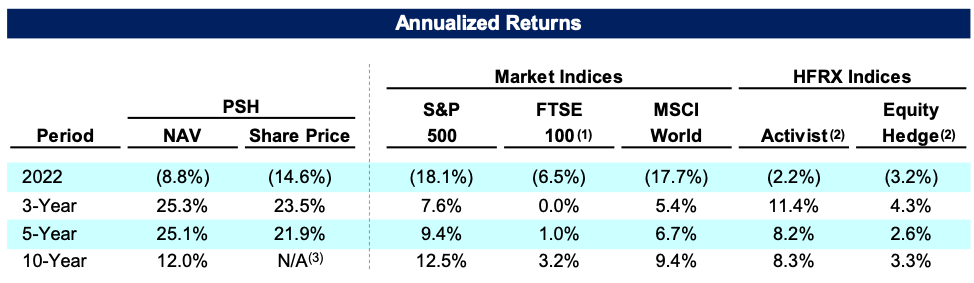

Whilst the PSH underlying portfolio (as measured by NAV) has delivered impressive investment performance (refer Exhibit 3), the fund's return can be highly volatile from year to year. I therefore do not think it likely that investors currently have a high conviction that the underlying portfolio will deliver strong future returns. PSH is a geared and concentrated portfolio, and the manager has a willingness to use derivatives, so we shouldn't be surprised about the historical year-to-year volatility.

Investment management fees for PSH are certainly not low - with a base investment management fee of 1.5% and a performance fee of 16%. That said, although I would not describe PSH's investment management fees as low, I do not consider them to be egregiously high given the nature of the fund's investment strategy.

Considering the above points, I therefore conclude that PSH shares should continue to trade at a discount to NAV. The inevitable follow-up question - what level of NAV discount should apply? - is next to impossible to answer with anything approaching confidence. If pushed to give a number, as things stand today, I would say that that a discount to NAV of ~20% is probably a reasonable guess at a lower bound. Relative to an NAV discount of 20%, the current NAV discount of ~37% implies a maximum potential NAV discount closure upside of ~27%.

Exhibit 3:

Source: PSH 2023 Annual Investor Presentation, slide 8.

{kind=link}

Arguments Against NAV Discount Closure Potential

It's often the case that when the topic of the PSH NAV discount is discussed, arguments are put forward as to why the company has little or no incentive to close the NAV discount. Let's have a closer look at a couple of these arguments. Note that I will use the term 'the company' very loosely in what follows - which is generally the case whenever these arguments are made (although sometimes Bill Ackman, or 'insiders' are referenced more specifically).

The 'It's All About Management Fees' Argument:

Buy-backs are frequently used as a tool to reduce NAV discounts. Sometimes such buy-back strategies work, but often they don't. There's no hard and fast rule as to how aggressive a buy-back strategy needs to be in order to positively impact an NAV discount. If a company implements a buy-back strategy and the NAV gap doesn't materially close, critics of the company will say that the strategy was not aggressive enough (implying that the company should have bought back more shares and/or paid higher prices). The next leg of this argument is the claim that the company wasn't aggressive enough with the buy-back because it did not want to shrink the NAV due to the negative flow-on impact that this would have on the investment manager's fee base.

So, to get specific, the suggestion here is that the PSH board has not pushed harder on the company's buy-back strategy because it wants to protect the fee income earned by PSCM. The implication being that PSCM, under the leadership of Bill Ackman, has sufficient clout with the PSH board to be able to protect its fee revenue.

I see a number of weaknesses in this type of argument. To start with, the PSH board is responsible to shareholders first and foremost. In reality, of course PSCM and Bill Ackman will have an influence on outcomes, but the board remains the ultimate decision maker (other than for matters requiring a shareholder vote).

Secondly, if the goal is simply to avoid reducing NAV, then why bother paying out dividends or increasing dividend payments further? PSH commenced dividend payments in 2019, and has recently committed to increasing dividend payments in line with NAV growth, with the additional intention not to reduce the dividend payment even if NAV reduces. Does this sound like a strategy designed to maximize retained NAV and pass more investment management fees through to PSCM? I don't think so.

Thirdly, this argument ignores the fact if the buy-back strategy is successful, PSCM and Bill Ackman may be able to use the positive investor sentiment associated with the NAV discount closure in order to launch other funds/products, thus increasing and diversifying PSCM's revenue fee base. Conversely, the reputational drag from an ongoing and wide NAV discount is likely to act as a hindrance for PSCM in gaining additional AUM in other funds/products.

The 'Last Holders Win' Argument:

The 'last holders win' argument starts with the fact that the wider the NAV discount is, the more value accretive a share buy-back becomes. Getting specific to PSH, the claim is that since Bill Ackman and other insiders will not sell into a buy-back offer, they will be beneficiaries of the value accretion of the buyback, and that they are therefore happy for the NAV discount to remain in place, and may even be pleased if it widens further. The ultimate end-game (rather unlikely in my view) in this scenario is that Bill Ackman and insiders eventually end up owning almost 100% of the company, thus capturing the full value accretion of the buy-back.

This argument strikes me as somewhat unrealistic and overly cynical. It ignores the negative impact of reputational damage to the PSH board members, Bill Ackman and PSCM insiders that would follow. Further, as soon as it became clear that Bill Ackman and insiders were attempting to execute the last holder wins strategy, strategically-minded investors would start to build positions in order to join the party, causing the NAV discount to narrow.

Whilst both of these arguments against the potential for NAV closure to occur are grounded in fact (fact 1: lower NAV = lower fee income for PSCM, fact 2: wider NAV implies greater buy-back value accretion), they ignore a number of issues/consequences that make them unlikely to occur in the real world. I would not entirely dismiss such arguments, but personally I do not find them persuasive.

Actions to Close the NAV Discount

In my view, there is plenty of evidence that PSH has been and remains focused on closing the NAV discount. A read-through of the Chairman's Statement section of PSH annual reports dating back several years highlights that the PSH board pays close attention to the NAV discount and is committed to closing it. I refer readers to Bill Ackman's 'Letter to Shareholders' set out in the PSH 1H22 Financial Statements (commencing page 5) which discusses the PSH NAV discount at length; whilst I do not fully agree with all of the points that Bill Ackman makes in this letter, on balance I find the contents well expressed and quite compelling.

In the company's FY22 Annual Report , the PSH board points to several actions already taken that stand as evidence of the desire to close the NAV discount:

- Securing a listing on the LSE, with a subsequent elevation to the FTSE 100 index.

- Returning a total of $1.4 billion of capital to shareholders since inception (as of 31 December 2022).

- Repurchasing 59.1 million PSH shares for $1,100.6 million in the six years to 31 December 2022, representing 24.6% of shares outstanding prior to the repurchases.

- Initiating a quarterly dividend in 2019, with subsequent increases to dividend payments.

- Increased marketing efforts aimed at reaching a broader array of potential investors (particularly UK retail investors).

- Obtaining a reclassification from The Association of Investment Companies ("AIC") for PSH from its Hedge Funds group to U.S. Equity, which more accurately reflects PSH's investment strategy.

As evidence of the board's continued desire to close the NAV discount, PSH announced a further $100m buy-back in early June 2023. The relatively small size of the renewed buy-back program will disappoint some commentators, and I would tend to agree with that sentiment given that the buy-back represents less than 2% of issued capital.

The PSH Portfolio

As there is no certainty that the PSH NAV discount will close, in order to buy or hold PSH, an investor should be comfortable with the fund's underlying investments. For a detailed overview of the current portfolio, I refer readers to the Seeking Alpha transcript of the PSH investor call in May 2023. The largest exposures held by the fund are listed below:

- Alphabet Inc ( GOOG )

- Canadian Pacific ( CP )

- Chipotle Mexican Grill ( CMG )

- Hilton Worldwide Holdings ( HLT )

- Howard Hughes Corp ( HHC )

- Lowe's Companies ( LOW )

- Restaurant Brands International ( QSR )

- Universal Music Group NV

Alphabet Inc is the latest addition to the portfolio. PSH purchased the stock in 1Q23, and the current holdings had an average entry price in the range of $94.00 to $94.50 (Alphabet Inc is currently trading at ~$121.00). PSH claim to have purchased Alphabet Inc at ~16x forward earnings, which compares favorably with the stock's mid-20's x historical level. This particular investment seems to have been nicely timed.

I don't have strong views on any of the PSH holdings. I'm aiming to do a deep dive on Lowe's Companies in the near future, as there are several aspects of LOW that appeal to me. I see the addition of Alphabet Inc as a positive in terms of the sector diversification of the portfolio. The sector concentration associated with the combination of Chipotle Mexican Grill and Restaurant Brands International is one aspect of the portfolio that leaves me feeling slightly uncomfortable. As things stand at present, I'm neither excited or concerned about PSH's major investment holdings.

Summary & Conclusion

PSH is currently trading at around a 37% discount to NAV. This represents a very deep discount for a fund that has demonstrated a solid investment performance capability and has management fees that are not egregiously high. The NAV discount has widened materially from the average level of ~25% observed in 2021.

Reducing the NAV discount remains a matter of priority for the PSH board. The board has already executed a range of non-trivial actions aimed at reducing the NAV discount, and I expect ongoing efforts in this regard. The continued expansion of the NAV discount is concerning, and a reversal of fortunes cannot be guaranteed. A number of arguments can be made to support the case that the NAV discount will not narrow and could even widen further, but after careful consideration I do not find these arguments particularly persuasive.

Looking at the underlying investments held by PSH, on balance I am comfortable with the fund's major exposures. The structure of the current PSH portfolio is such that I feel quite confident that PSH can deliver satisfactory NAV growth over time. Taking a medium-term perspective, combining this expectation of underlying NAV growth with the genuine potential for the PSH NAV discount to narrow leads me to land at a BUY rating for the stock.

For further details see:

Pershing Square Holdings: Unloved Deeply Discounted Value Proposition