BTDPY - Persimmon: Challenging Times Ahead As Housing Market Weakens

Summary

- UK based house builder Persimmon has seen a 16% jump so far in 2023 after an awful 2022. Can it sustain the increase?

- The UK housing market is poised to weaken both this year and the next, and signs of slowing down are already visible for the company.

- Weakening financials and subdued forward sales indicate that it's best to hold off for now than buy despite its relatively low P/E ratio.

Despite dire forecasts for the stock markets in 2023, it has started off on a pretty decent note. The S&P 500 ( SP500 ) is up by more than 4% in January so far. The FTSE 100 ( UKX ) is up by a slightly stronger 5%. Some stocks or ADRs, depending on the markets we are trading on, as would be expected, have outperformed the broader markets. One of them is Persimmon ( OTCPK:PSMMF ), one of the largest house builders in the UK. Its price is up by 16%.

This gain in momentum is interesting after an awful 2022 for it. Even now, it's down by 59% over the past year. By comparison, the S&P 500 is down by just 15% and the FTSE 100 is actually up by 3%. This brings up the question of whether this rise is sustainable for Persimmon. To analyse, I look at the prospects for the UK housing market, the company’s own financials and its market multiples.

House prices poised to fall

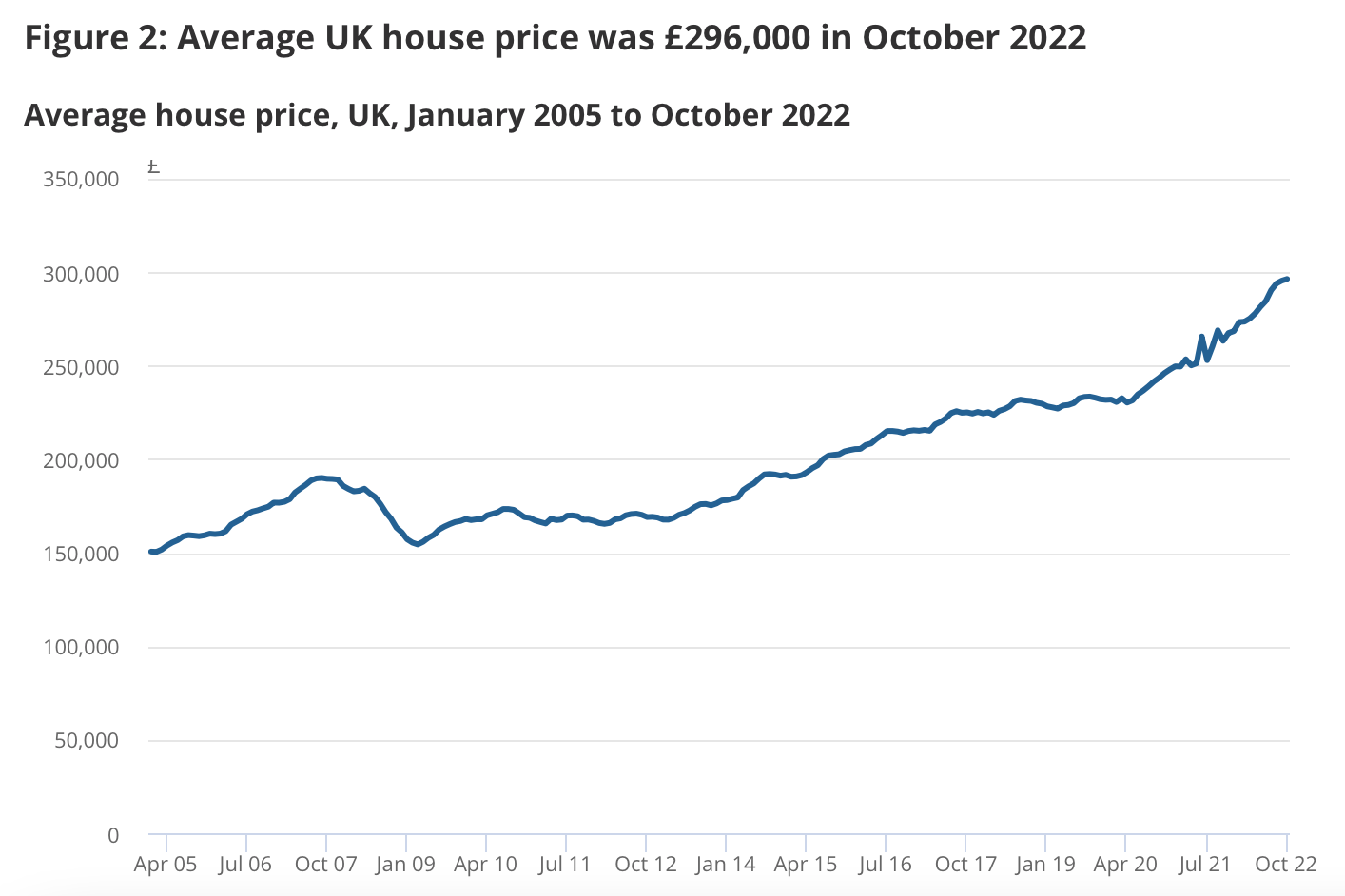

House prices in the UK have largely been rising over time (see chart below) but their growth has been particularly strong in the recent past. As of October 2022, the average house price climbed to a record high of £296,000 as per the Office of National Statistics [ONS]. This is a growth of 12.6%, even higher than the already strong growth of 9.9% up to September 2022.

{kind=link}

However, this is likely due to an artificially low house price figure last year at this time, when the stamp duty holiday was still ongoing. Moreover, with the ongoing cost of living crisis, rising interest rates and an economy that could be teetering on recession, the prospects for the year ahead don’t look quite as robust as the figures indicate. Some signs of a slowing down in the property market are already visible, with the number of days it takes to sell a house rising from 32 days in May to 45 days in November 2022. Figures released for house prices since October also show some signs of softening, as do official estimates for 2023 and into 2024 .

Positive trading in 2022

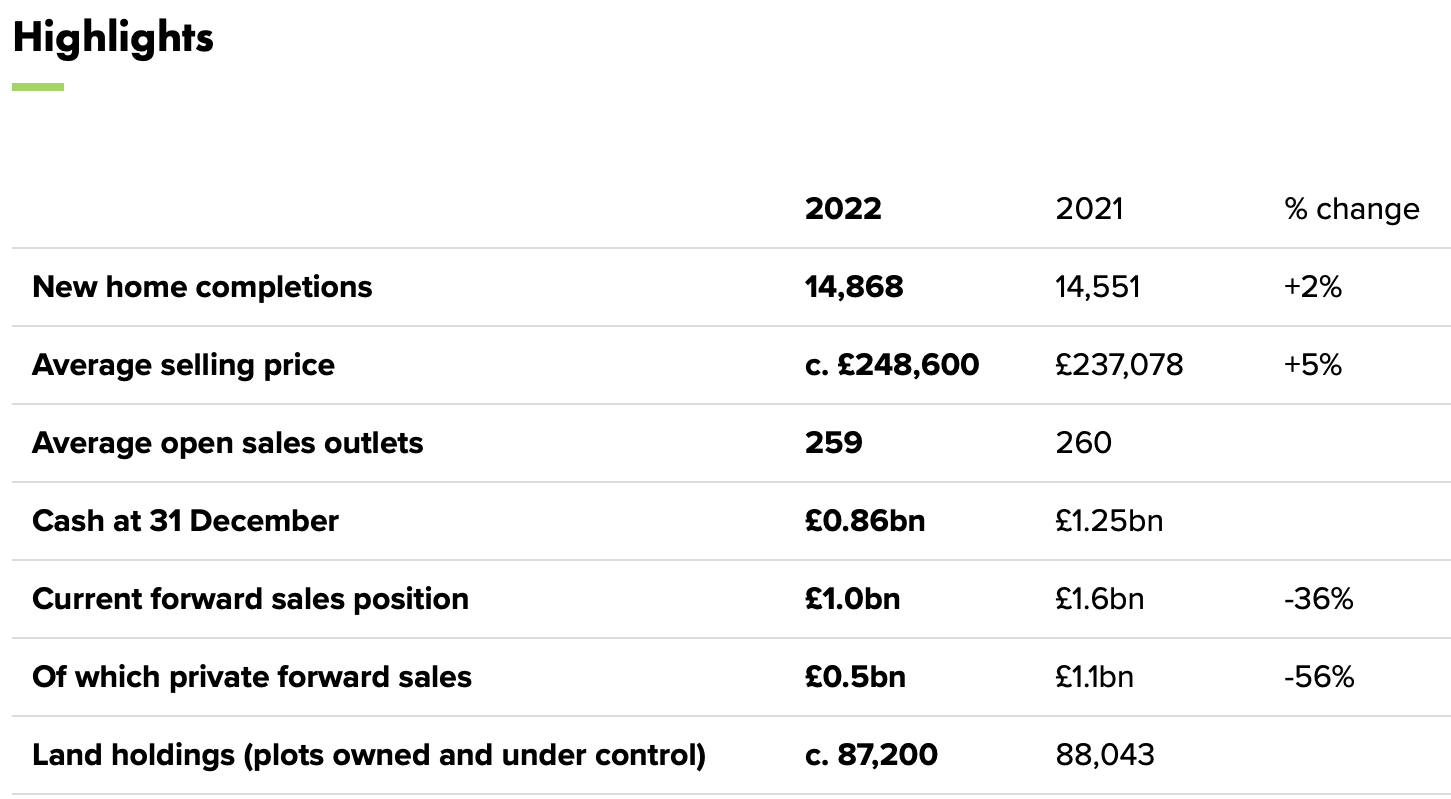

For Persimmon, however, the going is strong for now. For the full year 2022, its average selling price rose by 5% YoY to £248,600. New home completions were up 2% as well. The company also says that it has been able to maintain its high margins, where the gross profit margin stood at 30% at the end of June 2022 and the operating margin was also strong at almost 26%. This suggests that its financials for the full year 2022, which are due to be released on March 1, may not be poor.

{kind=link}

Financials and outlook weaken

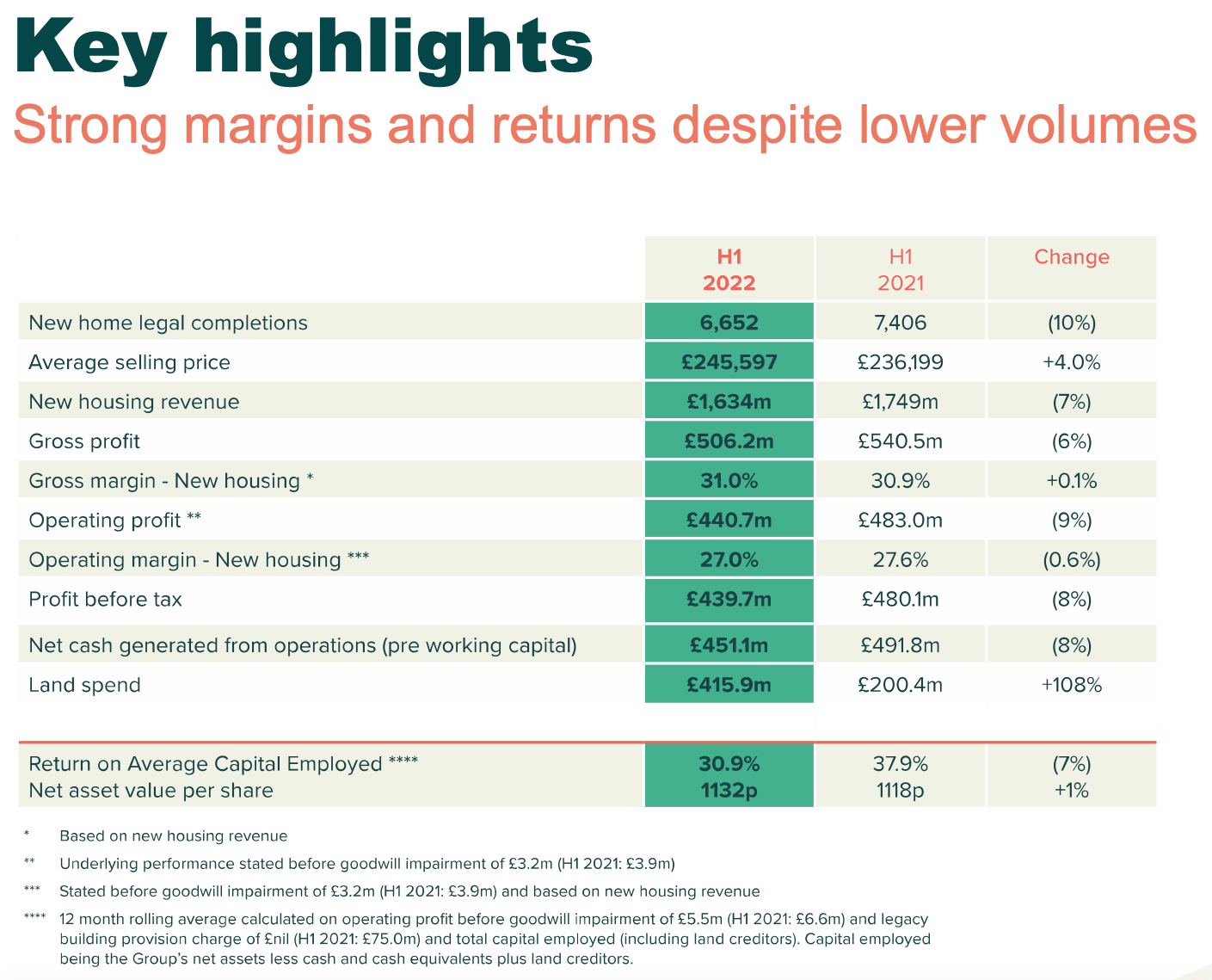

That remains to be seen though. For the first half of the year (H1 2022), the company did report a decline in revenues of 8.3%, which reflected down to its net earnings even as its margins stayed strong. It was still optimistic about the rest of the year, though, with a strong start to sales and a 90% forward sales rate.

{kind=link}

However, signs of a slow down as evident from the latest trends in broader house prices are becoming visible for Persimmon too. In its trading update, it mentions that private net sales have fallen to 0.3 per outlet per week in the final quarter of 2022, down from 0.69 during the quarter before. Its forward sales have also reduced to £1 billion compared to £1.6 billion in 2021.

Fairly valued as per market multiples

It's little wonder then that its price-to-earnings (P/E) ratio is sagging at 6.2x compared to more than double 14.4x for the consumer discretionary sector. It's also lower than Persimmon’s own long-term P/E of 11.6x . It also lags behind its UK-based peers like Taylor Wimpey ( OTCPK:TWODF ) at 7.7x and Barratt Developments ( OTCPK:BTDPY ) at 9.2x.

The comparison with peers, however, at the first glance suggests, that there could be some more room for Persimmon’s price to inch up. The reason is that the challenges it faces now have to do with the sector as a whole, and both its peer companies are in the same boat too. Or not.

Barratt Developments stands out for continued revenue growth as well as earnings increase, which explains why it commands a relative premium. While Taylor Wimpey is more comparable to Persimmon to the extent that it also saw a fall in revenues in H1 2022, the difference was in terms of profit outlook. In my recent article on it, I pointed out that it was optimistic about a 13% growth in operating income for the year. By contrast, Persimmon saw a decline in operating profit in the first half, and it seems unlikely to have risen in the second half either.

Also, Persimmon’s price-to-sales (P/S) at 1.3x also exceeds the consumer discretionary sector at 0.93x as well as its peers Taylor Wimpey and Barrett Developments, which are both at around 1x.

What next?

In sum then, it’s tough to make a case for a sustained price rise in Persimmon’s price except for the fact that it’s trading at lows not seen in a really long time. So investors who are interested in it for the long haul might find it a good one to buy now when it looks dirt cheap. It is an established company with a history of healthy financials.

It is affected because it’s in a cyclical sector in a year when economic weakness is expected to continue showing up. It doesn't help that its peers are performing better. Mortgage rates are high too, as Persimmon notes, that for some first-time buyers, they have doubled in the past year. With interest rates expected to stay elevated through 2023 however, it’s hard to imagine its numbers looking any better. If anything, they’ll probably look worse. This in turn means that there may just be a better opportunity to buy its ADRs. I already own Persimmon, but if I didn’t, I’d hold off on uncertainty regarding both its financials and the housing market outlook.

For further details see:

Persimmon: Challenging Times Ahead As Housing Market Weakens