PSNL - Personalis: Collaborations Should Ignite Growth Narrative

2023-09-06 08:27:34 ET

Summary

- Personalis is a small-cap stock specializing in cancer genomics, with an advanced cancer diagnostics platform.

- The company reported significant losses in Q2 earnings but maintains a robust financial standing and expects future revenue growth.

- Personalis has partnerships and collaborations in place to drive revenue growth and is well-positioned in the growing field of personalized cancer diagnostics and therapies.

Earlier this year, I added Personalis ( PSNL ) to the top of my watch list after recognizing it as an undervalued small-cap stock with significant upside potential, primarily due to the company's specialization in cancer genomics. For me, the company’s advanced cancer diagnostics platform, Personalis NeXT Platform, has immense promise both clinically and commercially. However, PSNL's value has declined by more than 90% since its IPO and 20% for the year, making it technically oversold and undervalued. In fact, PSNL is currently trading with a negative enterprise value in the face of a ~1x price-to-sales and promising long-term upside potential. Indeed, the company reported significant losses in their Q2 earnings; however, it still beat expectations and maintains a robust financial standing that might provide a runway for establishing a presence in the $30+B market. Therefore, I still believe the company’s current condition and prospects justify a higher valuation than its current market value. I see the prolonged sell-off and current turbulence in the stock as a favorable chance to add to my embarrassingly small PSNL pilot position in my Compounding Healthcare "Bio Boom" portfolio.

In this article, my intention is to provide a concise background on Personalis and review the company's recent Q2 earnings. I will then delve into reasons why I still believe a turnaround is possible. Afterward, I will outline a couple of key risks associated with PSNL that prospective investors must take into account. Finally, I will detail my strategy for managing a speculative position in PSNL as we head into Q4 of 2023.

Background on Personalis

Personalis is dedicated to unlocking the potential of next-generation precision cancer therapies and diagnostics. Founded by former Illumina ( ILMN ) executives, Personalis is dedicated to unlocking the potential of next-gen precision cancer therapies and diagnostics. This technology and its associated tests could revolutionize the fight against cancer by providing valuable insights from a single sample.

With a range of approved tests, including NeXT Personal, NeXT DX, NeXT Liquid Biopsy, and ImmunoID NeXT, Personalis has established a solid market presence. Additionally, NeXT Personal DX is scheduled for launch in the latter half of this year. The company derives a significant portion of its revenue from the U.S. Department of Veterans Affairs Million Veteran Program "VAMVP" contract, which involves testing genetic samples collected from VA sites.

Sequencing over 170K whole human genomes, Personalis claims a leadership position in whole genome tumor-informed minimal/residual disease “MRD” testing, showcasing impressive sensitivity levels.

Q2 Review

Personalis' Q2 earnings report revealed earnings and revenue that surpassed expectations. The company pulled in $16.7M in revenue, which was actually an 8.2% decrease year-over-year but was still beat by $0.21M. Personalis saw most of their revenue come from pharma tests, enterprise sales, and other sales of about $14M, and the remaining revenue came from primarily population sequencing.

Personalis reported a net loss of roughly $103M, down from $113M in 2022 as a result of a change in headcount. The company’s cash usage was reported to be ~$70M, down from $119M in 2022. The company finished the quarter with $137.2M in cash, cash equivalents, and short-term investments.

In terms of guidance, Personalis expects their Q3 total revenue to come in at about $17M, which is under the Street’s expectations of $17.76M. However, the company expects its full-year 2023 total company revenue in the range of $70M-$72M, which is superior to the consensus of $69.45M.

Q2 Progress Points to Future Growth

Indeed, investors should be focused on the company’s 10-Q and the financials. However, most small-cap biotech, pharma, and healthcare companies require additional research and analysis to help determine the company’s quarterly performance. In some cases, we are looking at pipeline developments or clinical milestones. There are also updates on timelines and regulatory decisions. These companies are typically pre-commercial or are very speculative, so investors need to divide their attention on the company’s cash position, and “how the company’s plan to stop burning cash”.

For Personalis, we are looking at revenue growth generated from their partnerships and collaborations. The company expects to pursue near-term milestones to drive revenue growth. In addition, they are looking to deepen collaborations for their product, NeXT Personal, which is a tumor-informed personalized liquid biopsy test for cancer. These collaborations include partnerships with AstraZeneca ( AZN ), Trace, Royal Marston, Vall d'Hebron Institute of Oncology “VHIO”, and others. Personalis is also actively engaging with global biopharma customers, including collaborations with National Cancer Center Hospital East and Ono Pharmaceutical Company. The partnership with Moderna ( MRNA ) for personalized therapy is expected to drive significant revenue in the future. Furthermore, the next-year option for the Population Sequencing for VAMVP is being exercised, which is a significant source of revenue.

The company is also working hard on developing and refining their technology. Personalis is well-positioned to benefit from important developments in oncology, including the growing trends for personalized diagnostic tests to screen cancer patients and the advancement of personalized therapies. The company's platform is highly sensitive, aiming to detect cancer at extremely low levels with the intention of guiding treatment verdicts and monitoring recurrence. It appears that the company's strategy is focused on strengthening evidence and advocating coverage in specific cancer indications, such as early-stage breast cancer, early-stage lung cancer, and immunotherapy monitoring. In fact, the company has collaborations with some very prestigious institutions TRACERx for lung cancer, Royal Marston for breast cancer, and VHIO for I/O therapy monitoring.

I should also note that Personalis is making progress with a path to reimbursement with a goal to obtain reimbursement for NeXT Personal in "at least one disease area" by the end of next year.

Another point to highlight is the company’s efforts to expand their patent portfolio. Personalis is ready to defend their IP, including patent infringement lawsuits against Foresight Diagnostics.

So Why Should We Expect Growth?

Well, Personalis has a platform with enhanced sensitivity and has the potential to impact cancer management and treatment decisions. The company has made significant progress in improving the clinical and commercial performance of their technology with powerful collaborations, platform development, payer relationships, IP defense, and improved financial performance. Therefore, I believe they are positioned to take advantage of the growing field of personalized cancer diagnostics and therapies. Essentially, if the cancer screening industry is going to continue growing… Personalis has the position to benefit from this growth.

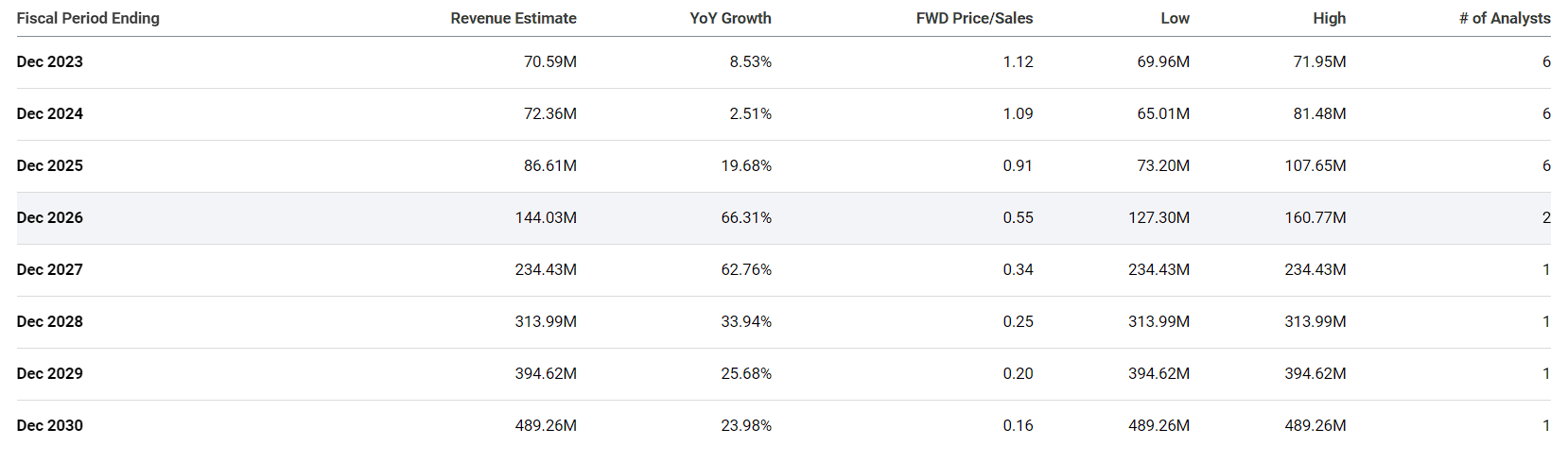

Personalis Growth Drivers (Personalis)

{kind=link}

Thankfully, I am not alone in this view as some Street analysts expect Personalis to report single-digit growth through 2024, but will experience strong double-digit growth into the next decade.

Personalis Annual Revenue Estimates (Seeking Alpha)

{kind=link}

So, I think there is more than enough evidence to suggest that Personalis has the ingredients to record significant growth in the upcoming years… and I am not the only one with this viewpoint.

Lingering Risks

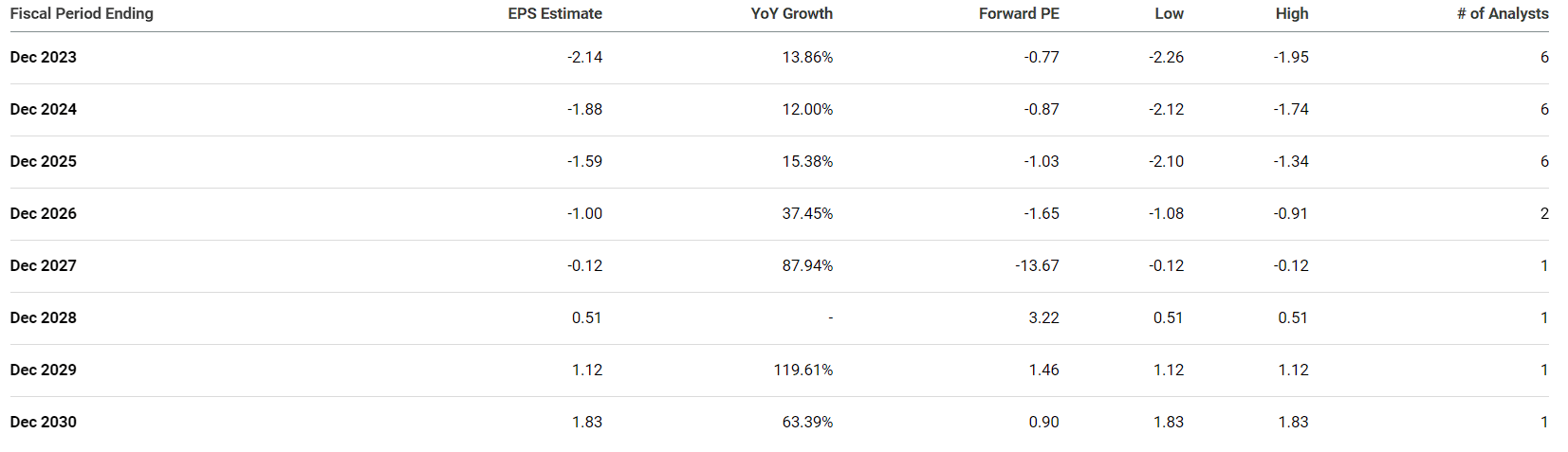

As with most small-cap healthcare tickers, PSNL has more than one risk that investors need to consider when managing a position. Primarily, Personalis is still reporting losses and is expected to continue to do so for a few more years.

Personalis Annual EPS Estimates (Seeking Alpha)

{kind=link}

Although the company finished the quarter with $137.2M in cash, cash equivalents, and short-term investments, they also reported a net loss of roughly $103M, and cash usage was reported to be ~$70M. Even if the company were to report significant growth in the upcoming quarters, we have to expect they will have to raise money at some point in the near future to continue to fund operations and fuel growth. So, investors have to expect some form of dilution, and possibly multiple offerings until the company is able to get to breakeven.

Another point to consider is competition, which comprises of vast number of lab services companies as well as some of the biggest and best diagnostics companies. Some of these companies include Illumina ((ILMN)), NeoGenomics ( NEO ), Fulgent Genetics ( FLGT ), and Myriad Genetics ( MYGN ) just to name a few. It is possible that Personalis will struggle or fail to report growth despite their ability to secure big contracts, and partnerships, and advance their technology.

Considering these two points above, I keeping PSNL in the Compounding Healthcare “Bio Boom” portfolio with a conviction level of 2 of out of 5 .

Remaining Bullish

Despite the market’s prolonged punishment of PSNL, I still believe the ticker offers significant upside potential. For the near term, I will point to PSNL’s undervalued state relative to its current and projected revenues. The NeXT Personal test is poised to become a leading MRD test in the market, which could drive substantial revenue in the years ahead. Market expectations indicate strong double-digit growth for Personalis in the next several years, with a potential revenue of approximately $489M by 2030, translating to a forward price-to-sales ratio of 0.16x.

While it's important to acknowledge that the industry average price-to-sales ratio ranges from 4x to 5x, the apparent discount at which PSNL is trading in relation to its future revenue estimates is noteworthy. If PSNL were valued similarly to its peers, its share price could potentially reach around $50 by the end of the decade. Admittedly, the company is currently incurring losses, making it likely that some form of dilution will be necessary. As such, while these projections underscore PSNL's upside potential, they should be interpreted with caution. Nevertheless, this assessment underscores the inherent potential of PSNL as a Compounding Healthcare “Bio Boom” stock.

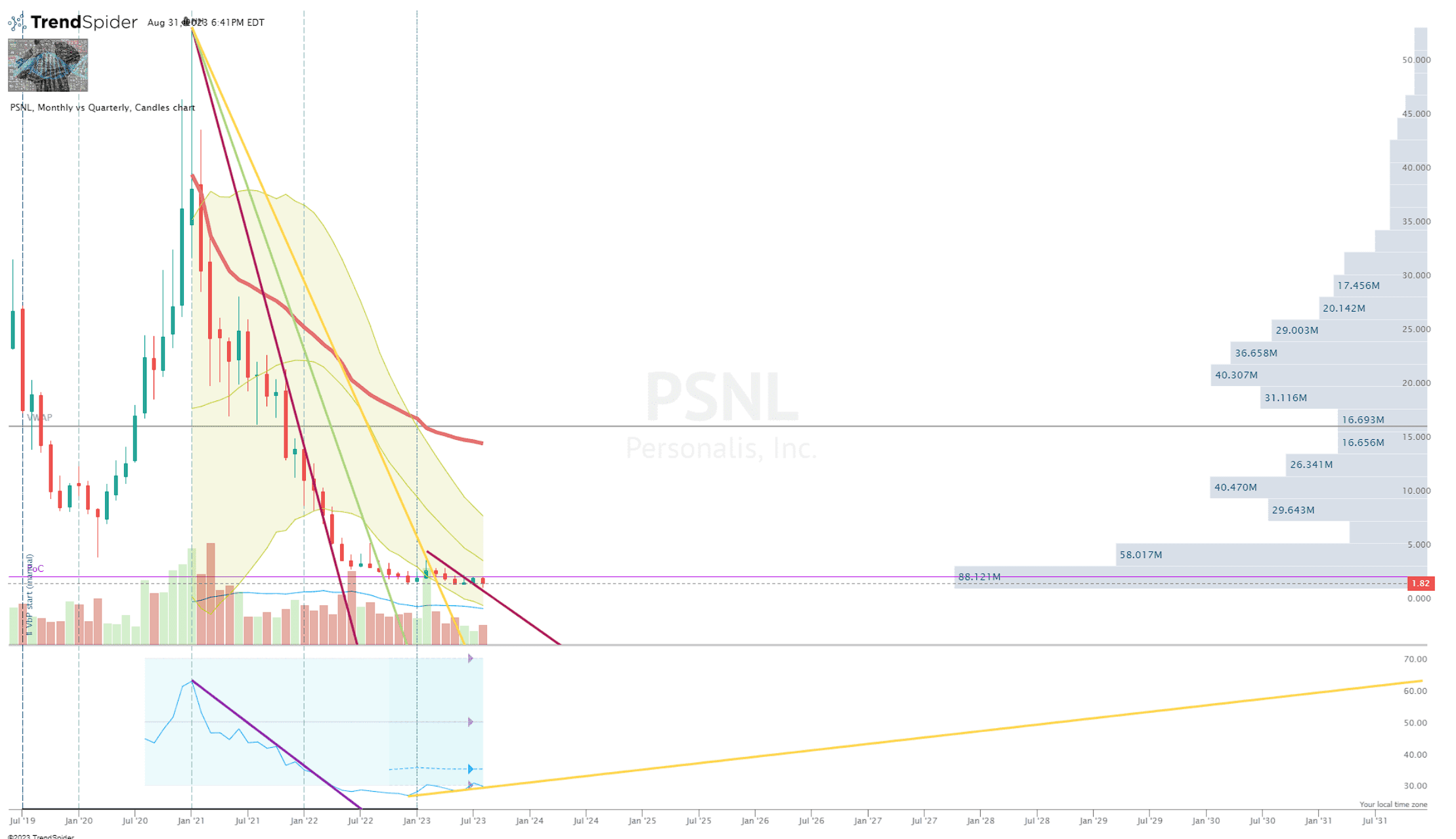

Another key consideration is PSNL's oversold status, a result of the disproportionately impacted small-cap healthcare stocks. PSNL's value has failed to really rally this year and has fallen by roughly 46% over the past twelve months. Keep in mind, that PSNL was trading over $53 back in early 2021.

PSNL Monthly Chart (Trendspider)

{kind=link}

PSNL Monthly Chart Enhanced View (Trendspider)

The small-caps have been punished, so it is possible these tickers experience a resurgence in the coming months, PSNL could witness a significant upward movement once it breaches the anchored volume between $2.00 and $2.50 per share.

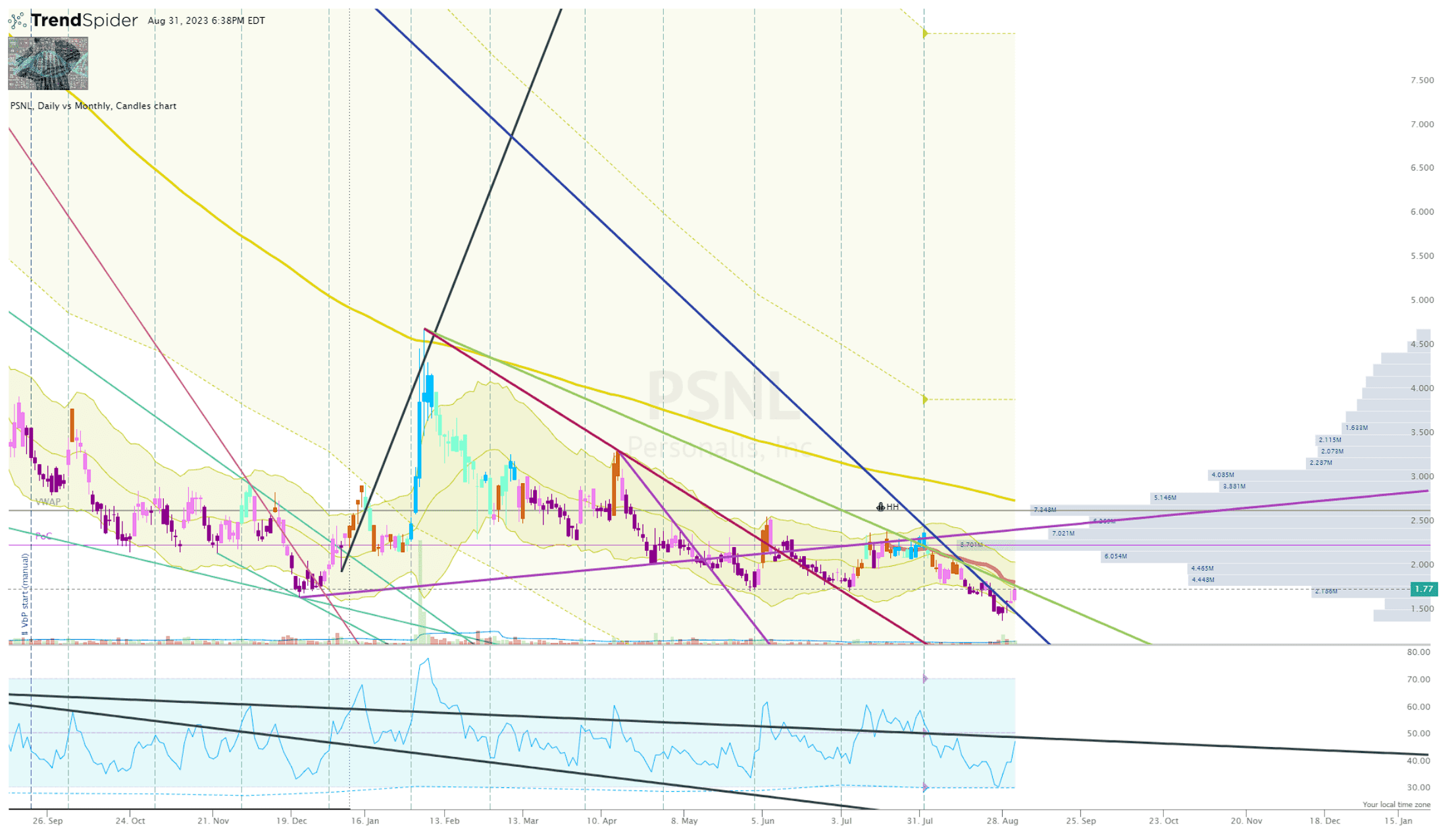

PSNL Daily Chart (Trendspider)

{kind=link}

Essentially, I can see how PSNL could show a quick resurgence under the right conditions. Certainly, the share price could continue to deteriorate, or possibly trade sideways for a protracted period of time. However, I am leaning toward the potential of a strong double-bottom setup with a bullish divergence on the Daily RSI, while the Monthly RSI is rising. A break above the July anchored-VWAP could signal a potential short-term bottom and the beginning of a potential reversal.

For the long-term, I am considering the company’s product portfolio that positions it as a formidable contender in the cancer genomics sector, Personalis' healthy cash reserves offer the flexibility to demonstrate sustained growth. This, in turn, could attract higher valuations, potentially positioning the company as an acquisition target.

My Plan

Indeed, tickers in the Bio Boom Portfolio are speculative because they typically lack profitability and are typically very volatile. Despite this, these stocks offer substantial upside potential due to impending catalysts, projected revenue growth, or possible turnarounds. Typically falling within the small to mid-cap range, these stocks present numerous trading opportunities, potentially leading to significant gains while gradually accumulating a "house money" position over time. These stocks are traded until they either exit the portfolio or transition to the "Bioreactor" growth portfolio.

I believe PSNL is a great example of a Bio Boom ticker because if “all goes well”, the company should report growth into the next decade and become a leader in its industry. Not only should the ticker react positively to the growth trajectory, but we should expect some speculation about Personalis possibly being acquired.

So, my current plan for my PSNL position is to remain vigilant and look for high conviction reversal setups below my Buy Threshold and look to start booking profit around my Sell Target 1.

Long-term, I will continue to trade PSNL until the bull thesis is broken, or the ticker graduates to the “Bioreactor” portfolio.

For further details see:

Personalis: Collaborations Should Ignite Growth Narrative