PETQ - PetIQ: Growth Is Back But Getting Pricier Too

2023-11-06 22:49:05 ET

Summary

- PetIQ is a company that produces and distributes pet medication and wellness services through various retail locations and e-commerce channels.

- The company's stock has experienced significant fluctuations but has been recovering in recent years, up 141% year-over-year after dropping almost 80% last year.

- PETQ has shown strong financial results, with sales and adjusted EBITDA increasing, and has the potential for further growth in the pet wellness market.

- One risk could be the company's over-reliance on acquisitions and partnerships for growth.

PetIQ ( PETQ ) is a company that produces and distributes pet medication as well as pet wellness services through its distribution channels and partners including 60,000 retail locations including national chains such as Walmart ( WMT ), Costco ( COST ), Petco ( WOOF ), Kroger ( KR ) and Walgreens ( WBA ) as well as e-commerce channels such as Amazon ( AMZN ). The company also offers veterinary service platforms in 2,600 locations in 41 states. The company offers more than 1,000 different products focused on pet health and wellness, many of which are sold over-the-counter. This stock could offer a lot of opportunity for investors in the long run if the management continues their good execution.

The company's stock has been on a pretty wild roller coaster ride in recent years. From the spring of 2021 until the end of last year, the company's stock took a heavy beating, dropping as much as 80% at one point because the company's revenue growth stalled for a year. All it took was one bad year with flattish revenues to pretty much erase all of the premium in the stock.

The stock has been recovering for the last year and up 141% year-over-year and the initial panic seems to have disappeared and investors are coming back to the stock. Even after this rally, the stock is still down about 56% from its 2021 high though.

Despite a small hiccup in its revenue growth last year, the company's revenues are up 400% since its IPO in 2017 which was 6.5 years ago.

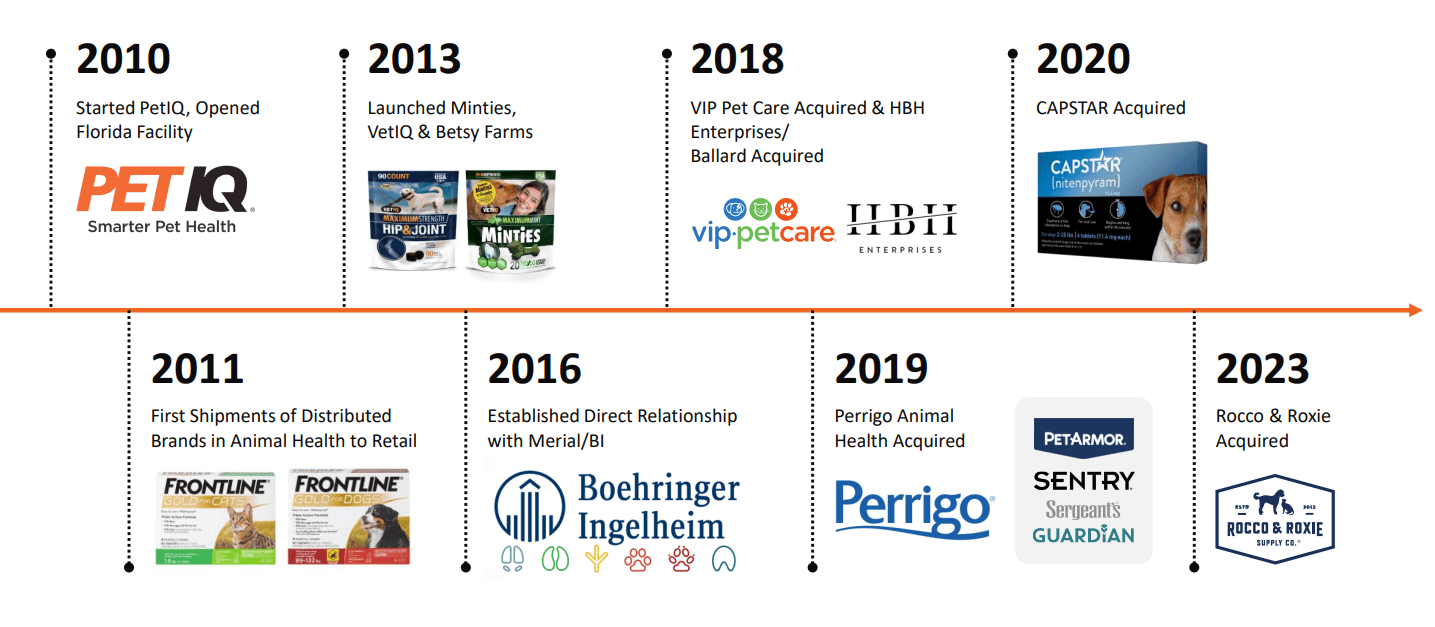

To be clear, not all of this growth was totally organic. In fact, the company has a history of acquisitions and establishing strategic partnerships in order to grow its total reach and sales. The company used a good portion of its IPO money to make acquisitions and form strategic partnerships as well as launch new products. For example, it acquired VIP Pet Care and HBH Enterprises in 2018, Perrigo Animal Health in 2019, CAPSTAR in 2020 and Rocco & Roxie in 2023. Each acquisition brought either new product lines, new service offerings or new partnerships into the company's portfolio.

PetIQ Acquisitions History (PetIQ )

{kind=link}

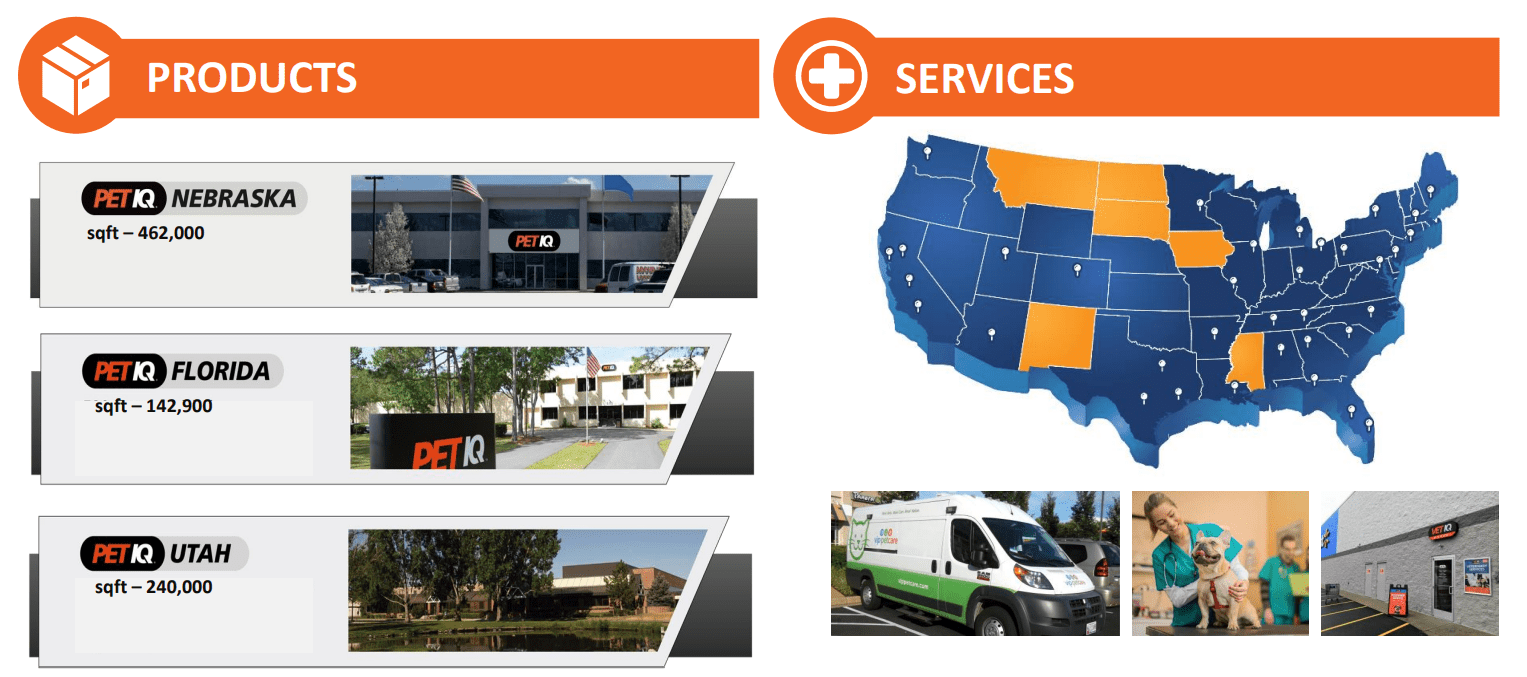

Through its acquisitions, partnerships, and new investments. The company is quickly becoming increasingly vertically integrated. For example, the company owns its own brands of pet medicines, produces them within its own manufacturing facilities located in Florida, Utah and Nebraska, uses its own distribution network to distribute them to locations to be sold. In addition, its pet clinic platforms in 2,600 locations allow the company to administer its medicine products to pets directly. Many of these clinics are located either inside of or next to major retail chains such as Wal-Mart and PetSmart which tend to be in locations that are highly visible and receive a lot of volume. The company's clinics typically offer quicker services such as vaccinations, nail trims, microchipping and heartworm testing but don't include more complicated procedures such as surgeries and it generally employs veterinarians who are generalists. The company is not fully vertically integrated but it's coming close to it.

Company's business segments (PetIQ)

{kind=link}

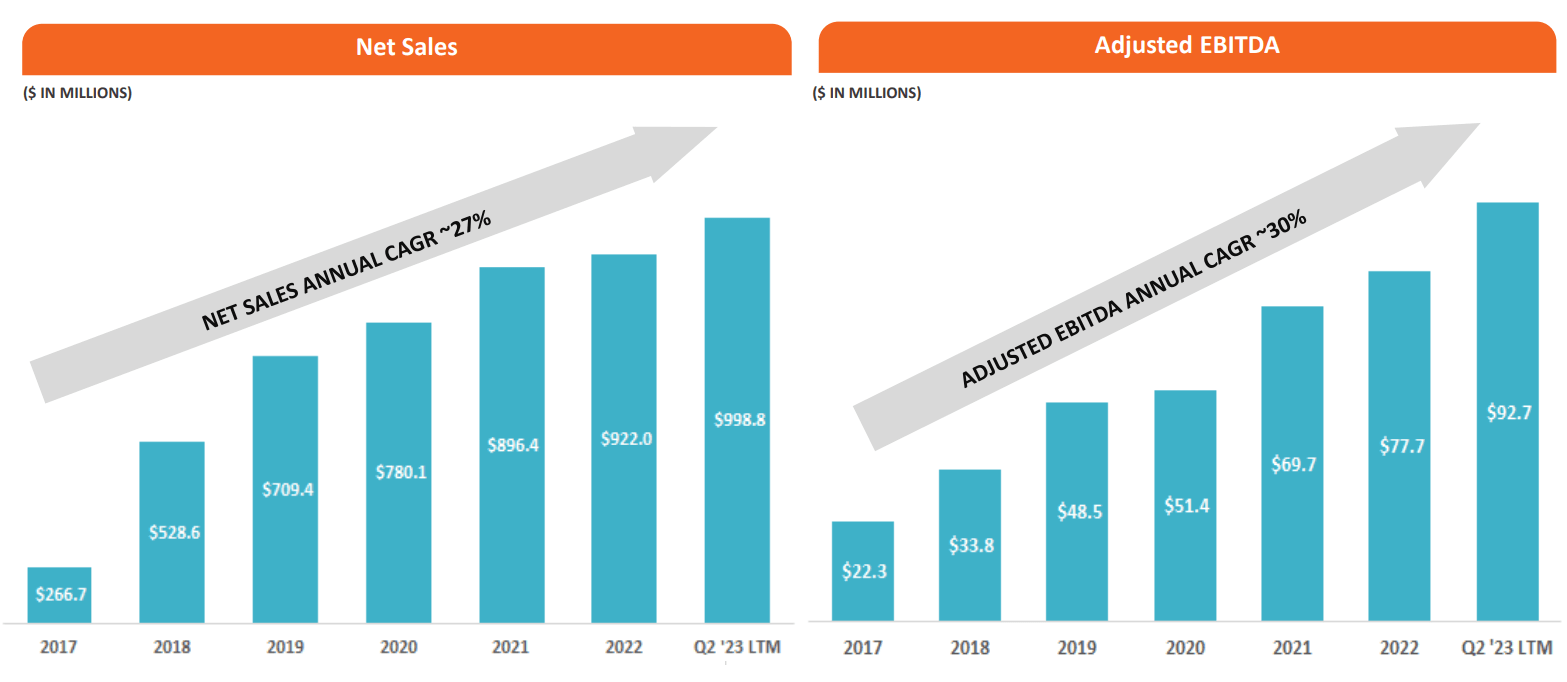

Last quarter the company posted pretty strong results as its sales were up 25% year-over-year and its adjusted EBITDA was up 36% year-over-year, indicating that its growth story is nowhere near over and what we saw in 2022 was likely just a temporary hiccup. The company also announced exceptional growth in flea and tick products, an increase in overall revenue per clinic and revenue per pet visit to each clinic. The company was able to pass its higher costs to customers without an issue and it solved some of the issues in its distribution network which allowed it to have more profitability. Moreover, the company reduced its net leverage ratio from 5.0 to 3.6 as compared to the same quarter a year ago. Last quarter the company also raised its guidance for the full year calling for 12% growth in sales and 22% growth in adjusted EBITDA for the full year.

Results including last quarter (PetIQ)

{kind=link}

The company still has an addressable pet wellness market of $55 billion and its revenues approaching $1 billion is just a fraction of the total available market. It also has very minimal exposure to international markets. Outside of the US, PetIQ has some presence in Canada but less than 1% of the company's revenues come outside of North America. The company ships a small amount of wellness products to European markets through its retail partners and e-commerce channels but it hardly has any presence there. There are both positives and negatives to this. One positive is that the company is focusing on one market heavily (the US) where it is the strongest and where it can have most return on investment. Another positive is that the company has a lot of room to expand when and if it decides to go after European markets. On the negative side one could say that the company is not diversifying its markets enough, totally dependent on the health of the American market and the American economy and that it's leaving a lot of money on the table by not chasing other markets. Considering how the company grows through acquisitions and partnerships, I see it only a matter of time before the company makes one or more international acquisitions in order to enter foreign markets.

In recent years, the company started to do a lot better in terms of generating cash flow from its operations. In the last 12 months, the company generated $128 million of cash flow from its operations which is not only the highest ever for the company but higher than the last 3 years combined. Only time will tell if this was a one-time thing or if it's sustainable but if the company can keep its operating cash flow at healthy levels it will be able to reduce its leverage further and have more ammo to make strategic acquisitions to further fuel its growth.

Having said that, the company's valuation is getting a little richer after this year's rally. Now it trades at a forward P/E of 24 as compared to 12 at the beginning of the year. It's still lower than the company's long-term average of 30 but this all depends on how much growth the company can bring in for the next few years. One thing is for certain though. After losing their faith in the company last year, investors are showing signs of faith in this company again.

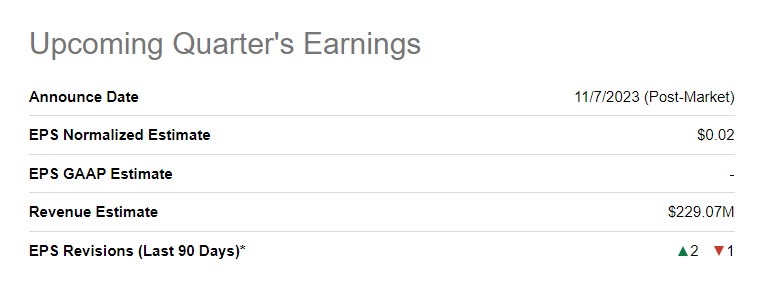

The company has another earnings report coming this week where analysts estimate it to post 2 cents of gains on $229 million of revenues. The company has a history of beating estimates and it can probably beat these as well but it won't matter much to long-term investors. What will matter most is the company's guidance for the future and if it can keep its guidance up like how it raised its full-year guidance 3 months ago.

{kind=link}

The company has an impressive growth story and still has a lot of addressable markets which it can expand into both in the US and other countries but it also relies a lot on acquisitions and partnerships for its growth so the company's future growth also depends on being able to make more acquisitions and form more partnerships. This could pose a serious risk for the company's growth story in the long term as acquisitions and partnerships become harder to come by or become increasingly expensive. Nevertheless, this is an interesting growth story worth at least watching.

For further details see:

PetIQ: Growth Is Back But Getting Pricier Too