PETQ - PetIQ: Well-Positioned To Grow And Capitalize On The Pet Economy

2023-08-23 00:30:48 ET

Summary

- PetIQ is on track to earn record-breaking revenues and FCF due to successful execution and strategic partnerships.

- The company's success is driven by its diversified product offering and is clearly capitalizing on previous investments - both on Capex and M&A.

- Scaling and competition pose risks, but there is still significant growth potential, and PETQ stock offers over 100% upside.

PetIQ ( PETQ ) is a company focused on the pet economy, providing both products and healthcare services. We think that the company executed well, and is now on track to earn record-breaking revenues and FCF. This success was primarily driven by their execution abilities and by successfully striking strategic partnerships with distributors. PETQ now has a diversified and strong product offering, plus an outstanding distribution network.

We think that this positive trend can continue and PETQ could possibly earn eye-popping figures of FCF in the upcoming years, which makes the current price undervalued.

The drivers of the recent PETQ success: products and services

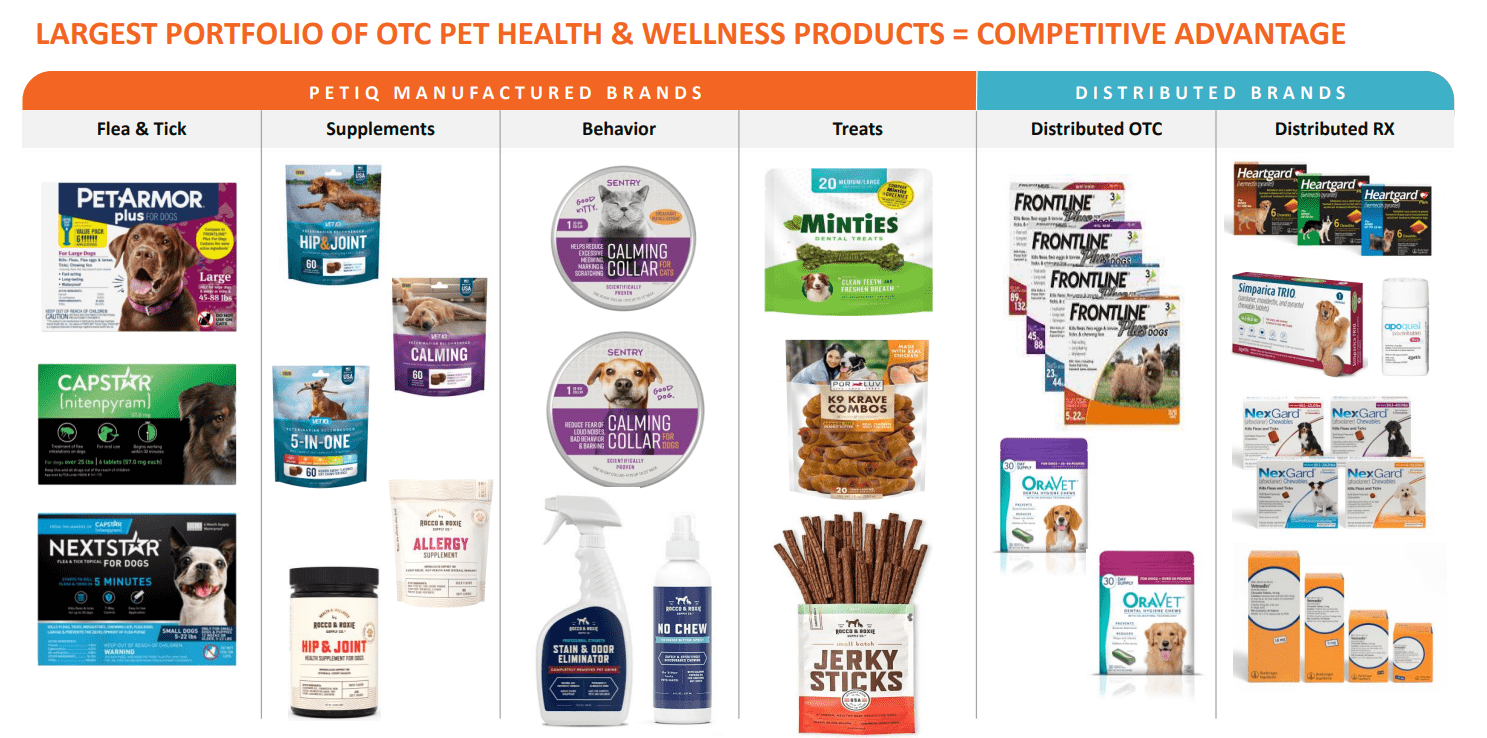

PetIQ has two main segments: products and services. They distribute pet medications and other wellness products through their sales channels, which also include the centers they operate. At the moment services account for around 10-15% of total revenue, making the products segment way more relevant.

{kind=link}

They provide a diversified range of products that go from behavior control to treats to actual drugs for pets. The company manufactures various brands which are later sold through a capillary network of distributors from pet specialty stores to e-commerce to retail pharmacies. We think that the bulk of the value of PETQ from a shareholder's perspective lies in its ability to market its products and underwrite partnerships with the key players in the industry.

{kind=link}

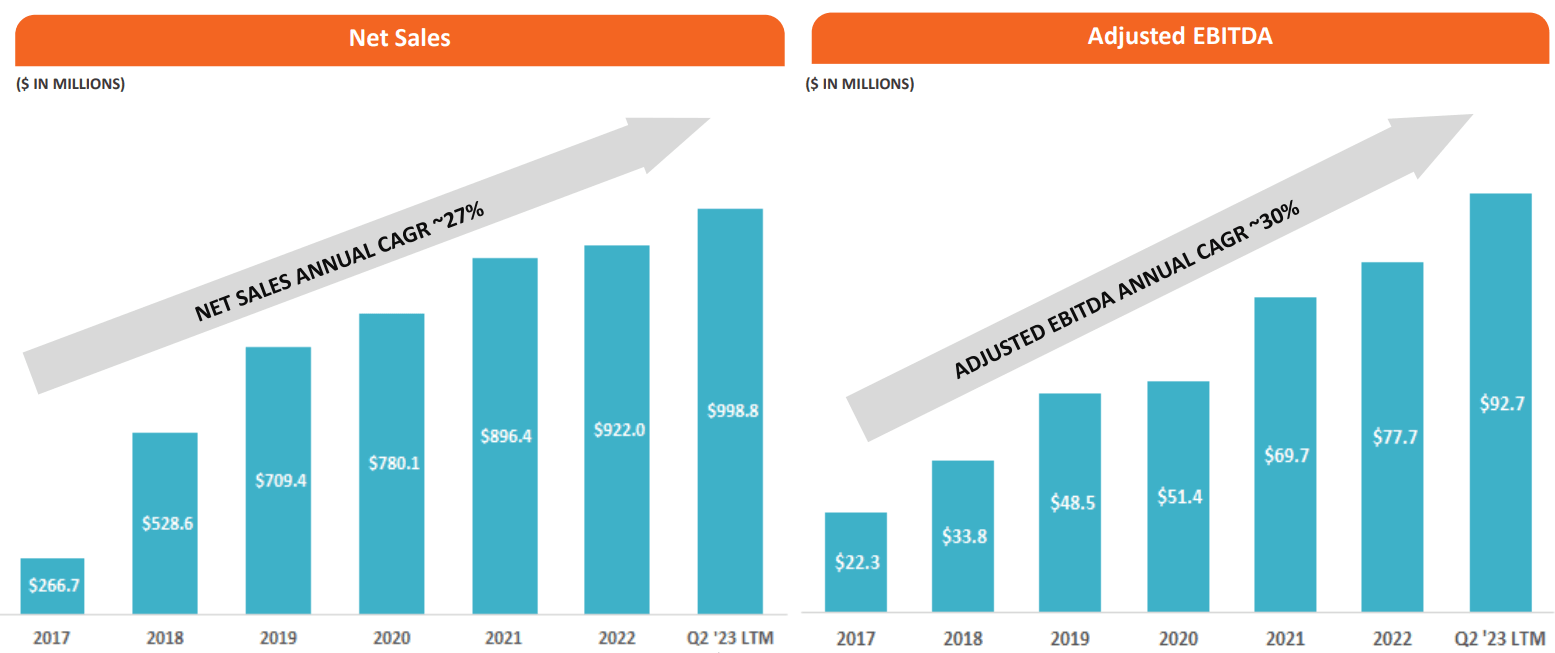

The results of this ability have been clear: 27% net sales CAGR and 30% EBITDA CAGR over the last 6 years. We think that this success can continue in the next years, with the economies of scale of larger and more efficient distribution meeting higher demand.

The company relied on some acquisitions to drive growth, including some large spending that took place between 2018 and 2019 when PETQ spent more than $280 million in M&A. This definitely helped the expansion efforts and seems to be repaying now, as FCF came in close to $90 million in the last 12 months.

The services segment has been lagging behind the desired performance a bit, which is actually falling short of the 27% growth of products to only 19%. This is likely driven by staffing challenges as vets are very difficult to recruit on a large scale as supply is very limited. We think that the incoming expansion from products will be enough to make PETQ attractive at the current valuation.

Risks: scaling is hard

There are several risks we can highlight that need to be accounted for when evaluating the company. First of all, scaling is actually hard and expensive. The company spent more than $80 million in Capex in the last years to build the clinics and it is still facing huge staffing challenges. This means that that segment may face hurdles that are so big to make the expansion not worth it, thus reducing the overall TAM and target revenues/EBITDA.

We are also pointing out that products may face competition. While it is true that PETQ has a significant competitive advantage due to its distribution and marketing abilities, competitors may arise. This could primarily come from pricing competition, thus creating some unwarranted and unneeded pressure on margins.

Forecasting growth and the fair value

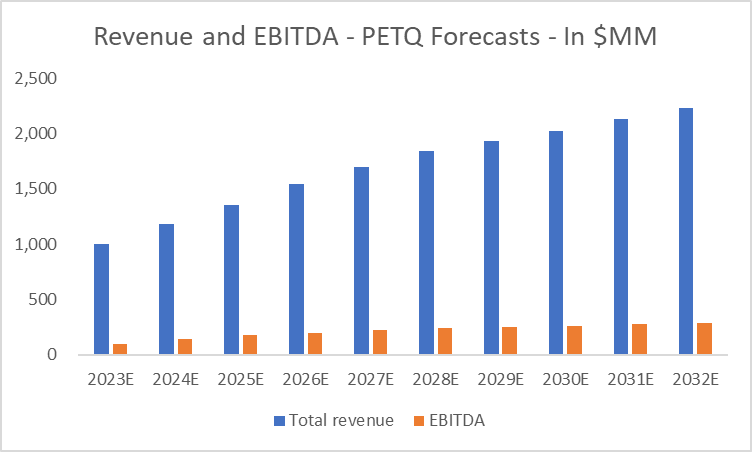

We will employ a standard DCF model to evaluate PetIQ's fair value. We will make several assumptions based on recent developments and the overall company's strengths and weaknesses. We believe there is still significant growth to be unlocked from increasing demand, and their ability to capitalize on the existing partnerships.

Assumptions include:

- Revenue growth between 18% and 10% throughout 2026. The company will gradually grow at a slower pace as they scale even more.

- EBITDA margin between 10% and 13%. PETQ is currently targeting $100 million in EBITDA with around $1 billion in sales. These margins should be reflective of their current and expected targets.

- The discount rate for the model is set at 10%, reflecting the relatively high cost of capital that the company currently faces, along with some idiosyncratic risks arising primarily from competition.

{kind=link}

The result is a fair EV of around $1.6 billion, which after adjusting for roughly $400 million in net debt yields a fair equity value of $1.2 billion. This means that we are expecting a fair value per share of $42 and that the stock offers an upside potential of more than 100%.

For further details see:

PetIQ: Well-Positioned To Grow And Capitalize On The Pet Economy