PETS - PetMed Express: Recovery Prospects Amid Financial Concerns

2023-10-02 14:40:08 ET

Summary

- PetMed Express, Inc. has demonstrated a promising financial recovery with strategic acquisitions and partnerships in the online pet care sector.

- The company faces competition from veterinarians and traditional retailers but has diversified its offerings and aligned with rising pet care expenditure trends.

- The pet care market's trajectory and the convergence of telemedicine and pet insurance indicate a potential for long-term growth and market share acquisition.

- PETS's recent financials show a turnaround, with significant year-over-year revenue growth and strong customer retention, but underlying financial concerns remain.

- My valuation model suggests PETS is slightly undervalued, but coupled with its concerning EBIT margins, I ultimately give it a neutral rating.

PetMed Express, Inc. ( PETS ), an established online pet pharmacy in the US, has demonstrated a commendable financial journey, with its strategic acquisitions and partnerships strengthening its standing in the market. The company's business outlook, performance indicators, competitive environment, and overarching trends in the pet care market make it an intriguing investment consideration. This is particularly true given that consumers prioritize their pets' well-being, making businesses in this sector relatively stable even during economic challenges. However, it's essential to note some financial intricacies. Specifically, PETS's revenues have declined since 2021, and its EBIT margins have significantly diminished since 2018. These factors bring forth questions regarding the company's long-term viability. While the stock might seem undervalued based on the assumption that PETS will regain its previous revenue levels and EBIT margins, it's crucial to approach it cautiously. Given the current data, I believe it's reasonable to give PETS a neutral rating, though I'm slightly optimistic due to the early indications of a potential recovery.

Business Overview

PETS runs a prominent online pet pharmacy in the US, offering around 15 thousand SKUs of various products and services for dogs, cats, and horses. Their range encompasses Non-Prescription (OTC) and Prescription Medications (Rx), Premium Pet Foods, and Telemedicine services via VetLive, partnered with Vetster. Strategic moves such as the acquisition of PetCareRx in April 2023 and pet insurance partnership with Pumpkin Insurance Services have broadened PETS's offerings and customer reach, solidifying its foothold in the online pet care sector.

PETS generated $257 million so far in 2023 through direct-to-consumer sales, principally through well-structured online platforms that produced 86.4% of the sales. Navigating the pet medication and food market, PETS faces competition from veterinarians online and traditional retailers. I think that the expansion of its catalog of products and services, paired with a reasonable pricing strategy, not only diversifies its revenue streams but also aligns the company with the rising pet care expenditure trend.

Moreover, the pet care market's trajectory, underpinned by the humanization of pets and rising pet ownership, notably during the pandemic, reflects a behavioral shift towards holistic pet care, mirroring broader consumer health trends. The projected global pet care market growth , from $235.32 billion in 2022 to $368.88 billion by 2030, underscores the expansive potential and hints at evolving consumer values towards pet welfare. I believe the surge towards dietary pet food, aimed at curbing pet obesity, mirrors the broader consumer trend of health-conscious spending.

Latest Earnings Slides.

The convergence of telemedicine and evolving pet insurance reflects a paradigm shift in pet healthcare, mirroring human healthcare trends. The adoption of telemedicine, expedited by the pandemic, intersects with the broader acceptance and enhancement of pet insurance, illustrating a synergistic effect. In my view, this melding underscores the elevated status of pets in households and the infusion of technology in veterinary care. The ease and expanded coverage of pet insurance could fuel the telemedicine sector further, as pet owners may be more inclined to seek remote consultations, knowing they have financial backing. This interplay could foster a more holistic, accessible, and technologically driven veterinary healthcare system, aligning with modern societal and technological trends. This positions well-entrenched players like PETS at a vantage point to capitalize on these emergent consumer trends, potentially driving a robust market share acquisition and revenue growth in the long term.

Latest Earnings Slides.

Strategic Acquisitions and Short-Term Repercussions

PETS's Q1 2024 financials present a notable dip in cash and cash equivalents from $104.09 million to $61.53 million, largely attributed to the $35.86 million acquisition of PetCareRx . Yet, despite a YoY sales uptick to $78.24 million from $70.19 million, the gross profit margin is squeezed as the cost of sales rises. A net loss of $887.00 million contrasts the net income of $2.78 million in Q1 2023, with G&A expenses surging to $15.71 million from $9.35 million.

This scenario hints at strategic investments for long-term growth, albeit with short-term financial repercussions, necessitating keen monitoring of subsequent cash flows and market response. In PETS's latest earnings call , the discussion emphasized the need to leverage operational and cost synergies between PetMed and PetCareRx to enhance financial performance, aligning well with the financial scenario presented in Q1 2024, where strategic investments play a pivotal role.

Latest Earnings Slides.

Furthermore, PETS's latest quarterly results showcased a favorable turnaround in its performance. This growth is particularly significant given the company's prior struggle with declining new customer numbers for two and a half years. The consistent growth in new customers over the past three quarters suggests that the company's strategies and offerings have successfully resonated with its target audience. In my view, this positive shift indicates a well-executed business strategy that has managed to address and rectify past challenges.

The data reveals that reorder sales comprise 87% of the business and have seen a 7% growth year-over-year. This growth rate underscores a strong customer retention rate. I infer that once customers engage with the company, they find substantial value in its offerings, leading them to make repeat purchases. This is a testament to the company's ability to build and maintain customer trust and satisfaction in my view.

Recovery Potential and Valuation Analysis

Looking at PETS's financial profile, its latest quarterly results suggest a nascent recovery, with sales growing 11.0% YoY to $78.00 million. This growth, largely organic, was enhanced by the PetCareRx acquisition , which added $2.40 million to the revenue and diversified the product and customer base. The company's emphasis on value, savings, and bulk offerings has broadened its appeal. Furthermore, the company's shift towards recurring revenue is clear with the expansion of its AutoShip and Save program. There has been a modest improvement in the company's gross profit margin. While a net loss was reported this quarter, it was primarily due to costs related to the acquisition. Without these costs, the company would have recorded a net profit. I believe that having $61.50 million in cash and no debt, even after the PetCareRx acquisition, is a testament to the company's prudent financial management.

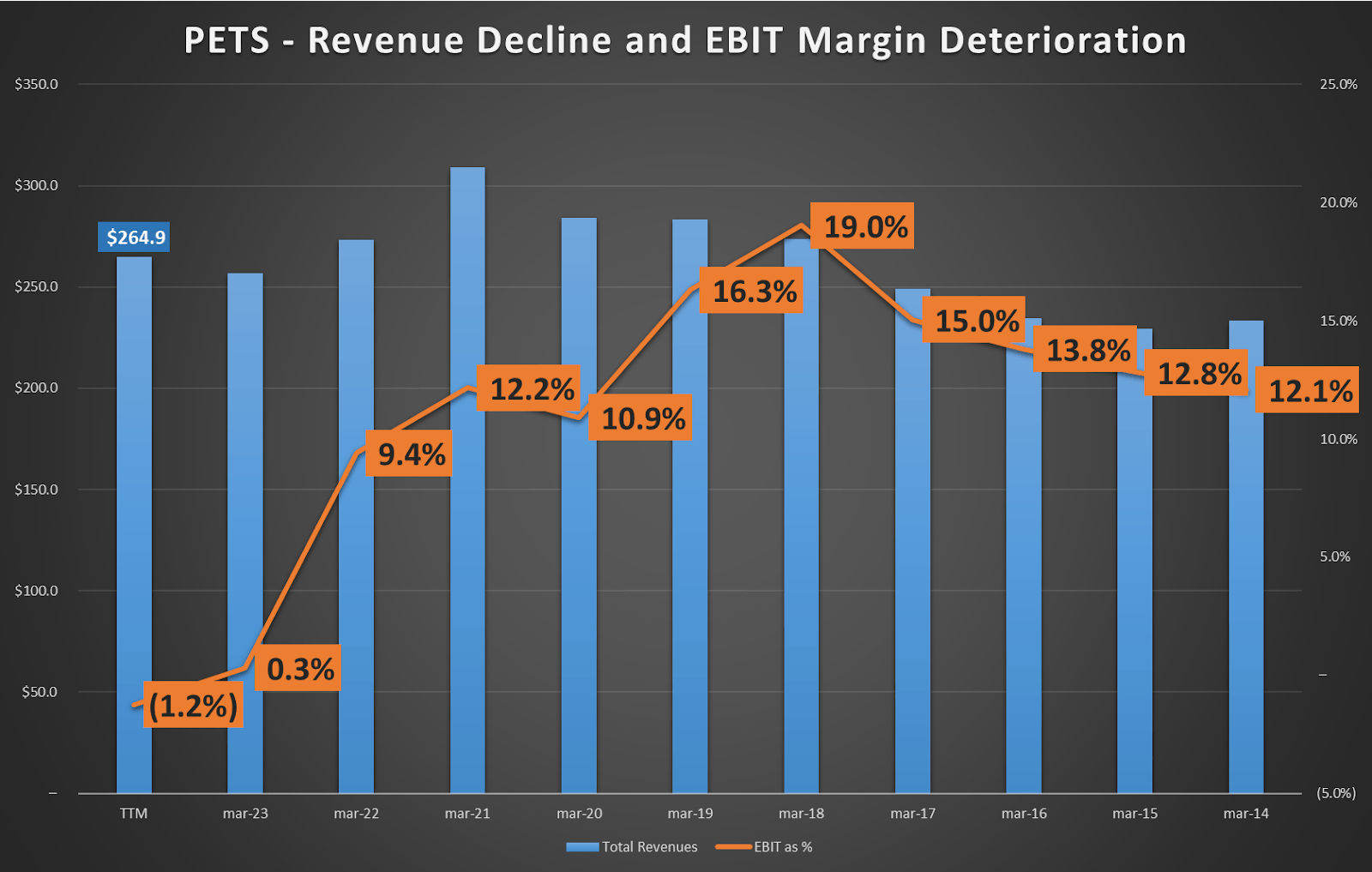

However, I feel that it's essential to highlight that despite these positive signs, the company's revenues are still below their 2021 figures. In my view, the consistent decline in EBIT margins, from 19.0% in 2018 to the current -1.2% for the trailing twelve months, indicates underlying issues that must be addressed to ensure the company's long-term financial well-being.

{kind=link}

Nevertheless, PETS's recent TTM figures indicate an uptick in revenues for PETS compared to the year ended in 2023. While it's not an entirely apples-to-apples comparison, these figures hint at a recovery trajectory for PETS in conjunction with the company's latest quarterly results. In my view, the fact that nearly half of the company's revenue stems from recurring sources is a strategic advantage. I believe this provides PETS with a more stable revenue profile and fortifies its position against potential market volatility, making it a more consistent investment option.

Over the long term, PETS's revenue CAGR since 2014 is a modest 1.1%. Its recent EBIT margins have declined, settling at -1.2%, but when we look at the historical average since 2014, it's at 11.0%. In my view, this indicates that while the company's revenue growth may be gradual, its EBIT margins have significant potential for improvement. Drawing from PETS's historical data, I believe the company can grow its revenues and enhance its EBIT margins. I've used the company's historical data to discount the implied FCFFs at an implied CAPM rate of 8.0%. This approach provides a balanced perspective on the company's financial trajectory, considering its past performance and future potential.

Author's elaboration.

Based on my valuation model, I believe the company appears to be undervalued by roughly 20.1%. This assessment largely hinges on the expectation that PETS will revert to its historical EBIT margins of around 11.0%. While there are emerging signs of recovery, I feel it's essential to approach this valuation cautiously. Considering the company's ongoing recovery trajectory and apparent undervaluation, yet factoring in potential execution risks, I assign the company a neutral rating but lean towards a slightly bullish perspective. In my opinion, a single positive quarter doesn't conclusively indicate a sustained EBIT margin recovery. However, I think it's an encouraging indication of the company's potential trajectory.

Conclusion

Reflecting on the data, PETS has shown its ability to navigate the competitive online pet care industry by adopting strategic measures to strengthen its market position. While the company's recent financial metrics indicate promise in some aspects, they also reveal concerns, particularly the decline in revenue since 2021 and the decreasing EBIT margins since 2018. These observations suggest that investors should approach PETS with caution. I believe that, although there's room for optimism considering the company's potential for recovery, it's essential for investors to weigh the inherent risks against the potential benefits. Given PETS's slight undervaluation and prevailing EBIT margins, I think assigning PETS a neutral rating is prudent. However, I feel that the initial signs of a positive shift, combined with the robust nature of the pet care industry, suggest a moderately positive future trajectory for the company, making it worth keeping an eye on.

For further details see:

PetMed Express: Recovery Prospects Amid Financial Concerns