PETS - PetMed Express: The Competitive Landscape Is A Tough Hurdle To Overcome

2023-04-06 05:14:21 ET

Summary

- PetMed Express is a leading national pet pharmacy with a long operating history and a solid reputation.

- While the company has benefitted from industry growth, they've been hurt by the competitive landscape.

- Their newly initiated AutoShip program is promising, but its share of net sales still has a long way to go beyond management's internal target.

- At current trading levels, shares offer an attractive dividend payout. But the upside potential in the stock appears to be challenged due to near-term competitive threats.

PetMed Express ( PETS ) is a leading nationwide pet pharmacy that offers prescription and non-prescription pet medication.

The company has a long operating history with a stable reputation of serving customers across the U.S. In recent years, the industry has grown, especially throughout the COVID period. At present, it's estimated that approximately 70% of households have a pet.

Moreover, close to a third of total spending on pets pertains to veterinary care and Rx medications. While the demand trends bode well for PETS, the rise in the number of entrants, specifically high growth, more diversified retailers, such as Chewy ( CHWY ), does not.

In recent periods, the company has reported declining sales. Increased costs to compete are also pressuring margins. While they've made some progress in certain areas, there is still a long way to go. For investors, shares are currently trading near their 52-week lows at a scaled back valuation. In addition, their dividend is yielding in excess of 7%. While the company is worth a deeper dive, I view the competitive landscape as a challenging hurdle to overcome.

The Business

PETS offers a broad selection of products for dogs, cats, and horses. Their primary product line, however, is prescription and non-prescription medications that are sold direct to consumer ("DTC") via their website/mobile app and/or through their toll-free telephone number.

While their customers are located throughout the U.S., approximately 50% of their customers reside in 8 states: California, Florida, Texas, New York, Pennsylvania, North Carolina, Georgia, and Virginia. In 2022, the average purchase price was approximately $93. This was up a few dollars from $89 in 2021.

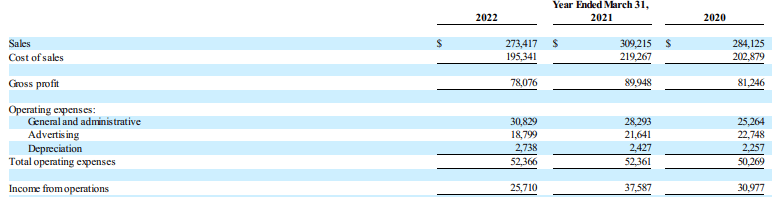

PETS operates on a March 31 fiscal year. In fiscal 2022, the company reported +$273.4M in total sales and recognized +$25.7M in operating income, representing an operating margin of 9.4%. That was down from 12.1% in 2021 and 10.9% in 2020.

FY22 Form 10K - Operating Summary For The Past Three Years

{kind=link}

They ran at about 28.6% gross margins in 2022, which, too, was down from the 29% earned in 2021, but comparable to 2020 levels.

Recent Performance

In their third fiscal quarter ended December 31, 2022, PETS reported total revenue of +$58.9M. This was down 3% YOY and shy of consensus estimates . The decline was primarily attributable to higher seasonal discounts and competitive pressures. The declines during the quarter added to the YTD decline, which, on a nine-month basis, are now down 6.2% from last year.

While higher promotions did weigh on sales, it resulted in increased conversion, which in turn reduced advertising costs associated with acquiring a new customer. During the quarter, for example, the cost of acquiring a customer was $64, down from $66 in the same period last year.

Granted, customer acquisition costs are still up significantly on a YTD basis, at $74 versus $59 last year. The promotions, however, have helped bring those costs down. And as a percentage of sales, advertising expense is flat from 2021, at 7.6%.

On the flip side, promotions did take a sizeable bite out of gross margins. During the quarter, gross profit decreased 14%. And as a percentage of sales, it landed at 25.9%. That's down 330 basis points ("bps") from last year.

They are, however, realizing some benefit from these higher costs, at least from a quarterly perspective. The company, for example, acquired 72K customers during the current quarter. This was up from 66K in the same period last year. But on a YTD basis, they've acquired 202K customers, which is notably down from 260K over the same period last year.

Overall, the company reported a net loss during the quarter and has posted YTD net income of +$5.3M. This is down markedly from the +$15M reported over the same period last year.

The AutoShip Program

In July of 2021, PETS launched their AutoShip & Save subscription program ("AutoShip"). The program is intended to provide several benefits; for the customer, it provides a convenient way to have their pet medications and other supplies delivered directly to them without having to place an order each time. This ensures they receive their products on a regular schedule.

For PETS, the program may increase loyalty and retention, which may improve revenues over the long term as adoption increases. In addition, it may reduce costs associated with processing and shipping, as the company could simply consolidate orders and ship them out on a regular schedule.

The program thus far has proven to be successful. In the most recent quarter, for example, 42% of net sales were attributable to AutoShip. That is up from 39% on a sequential basis and from 20% in the same period last year.

As a goal, the company has set a target of 50% of net sales for their AutoShip program in fiscal 2023. Given the progress they've shown thus far, it's possible they could in fact hit this target. Compared to key competitors, however, they still have some work to do in ramping up the program

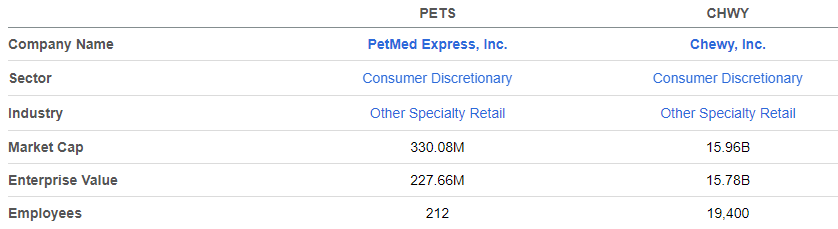

How PETS Compares To CHWY

PETS operates in an intensely competitive environment, one that is seeing an increasing number of entrants. In addition to direct competitors, such as CHWY and Petco ( WOOF ), the company also faces competition from larger retailers such as Walmart ( WMT ) and Amazon ( AMZN ).

With respect to CHWY, PETS has a longer operating history, but they are significantly less capitalized. CHWY's market cap, for example, is 5x greater than PETS.

Seeking Alpha - Market Cap Comparison Of PETS And CHWY

{kind=link}

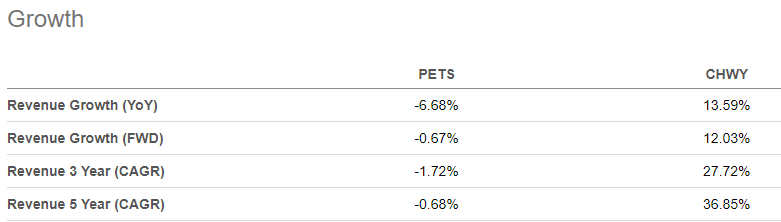

And the growth rates are markedly out-of-step, with CHWY growing revenues at a 5-year compound rate of nearly 40%, while PETS has essentially remained flat over the same period.

Seeking Alpha - Revenue Growth Comparisons Of PETS And CHWY

{kind=link}

In addition, about 73% of CWHY's net sales were through AutoShip in fiscal 2022. That's well above the 50% target that PETS is currently aiming for.

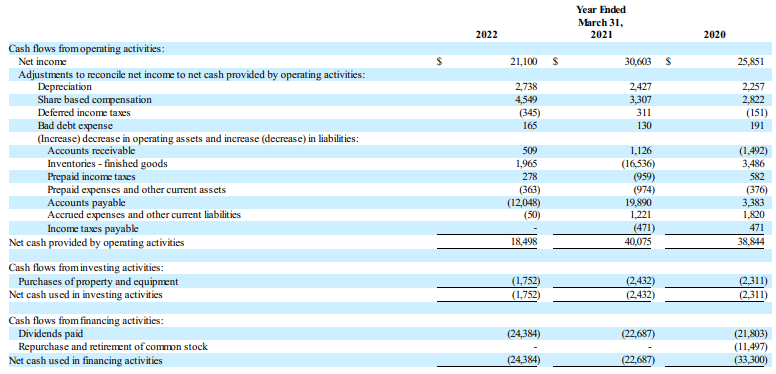

CHWY is a cash burner, however. In 2022, for example, CHWY generated +$350M in cash from operations, yet they spent +$230M of that on capital expenditures. And in the prior two years, they had even less free cash flow.

PETS, on the other hand, carries no long-term debt and has minimal, if any, need for capital expenditures. This enables them to utilize any cash generated on dividend payouts and/or share repurchases.

FY22 Form 10-K - Cash Flow Summary Over The Past Three Years

{kind=link}

Dividend Safety

PETS has a strong dividend track record. And over the past ten years , the company has grown their payout at a compound rate of 7%. Most recently, the payout was increased by about 7% in early 2021 to its currently level of $0.30/share.

Seeking Alpha - Recent Dividend Payout History

{kind=link}

At current trading levels, the dividend yields nearly 7.5%. While hurdle rates for most income investors are up, this may be appealing to many.

Supporting the payout is their strong balance sheet, which is comprised of over +$100M in cash on hand and no long-term debt burden. Additionally, there are limited, if any, CAPEX requirements. This enables the company to return any excess cash flows to shareholders via dividends and share repurchases.

Despite the limited obligations and their stable cash flows, dividend coverage appears stretched. As it is, they are already paying out over 100% of net income. But through nine months of the year in fiscal 2023, they've generated +$18M in operating cash, yet paid out just over that in dividends over the same period. While they have sufficient cash reserves to cover the remaining balance, it still doesn't bode favorably from a coverage standpoint.

While the payout has proved resilient, I would hesitate to view it as sacrosanct.

Final Thoughts

PETS has a long operating history with a solid reputation serving pet owners. In recent years, however, their business has been challenged by the rise of fast-growing competitors, such as CHWY. Additionally, as the demand for pet-related products has risen, so has the number of industry entrants.

Not only is the company reporting declining sales as a result, but they are also incurring increased costs to compete, which is putting downward pressure on margins. Some of their efforts, however, have yielded results.

They increased their number of customers in the current period, for example. In addition, their customer acquisition costs have declined and advertising as a percentage of sales has also remained flat from prior years.

The implementation of their AutoShip program has also proved successful, as evidenced by its growing share of total net sales. Compared to CHWY, however, the company still has some ways to go.

But working in their favor is their strong balance sheet, which is free of interest-bearing debt and rooted upon a sizeable cash balance and stable liquidity position. Their dividend offering is also a draw that cannot be matched by their most direct competitors.

At a forward multiple of 40x earnings, the stock does appear to be trading at a premium. Even with the recent pull-back to new 52-week lows, the valuation is still above 5-year averages .

True, the multiple appears more attractive when compared against a competitor such as CHWY, who currently commands a 75x multiple. But they are significantly larger and have more a more diversified product offering than PETS.

Given the competitive landscape and what PETS will need to do to get on par, I would need to see significantly more progress, perhaps in their AutoShip program, before I consider any new initiation on the stock. Until then, I will maintain a "hold" view on the shares.

For further details see:

PetMed Express: The Competitive Landscape Is A Tough Hurdle To Overcome