EQNR - Petrobras: A Return To Bearish Ground As History Comes Full Circle

2023-10-02 11:07:08 ET

Summary

- Petrobras faces continued political risks, impacting its valuation and investor confidence, despite its recent stock performance.

- The significance of oil in the Brazilian economy remains crucial, and the company's future success depends on navigating challenges related to pricing policies and investments.

- While Petrobras has seen favorable conditions, including lower oil prices and FX rates, recent uncertainties and political pressures may pose challenges, leading to a bearish outlook for the company's long term.

- Valuations for Petrobras are influenced by political risks, resulting in significantly lower multiples than other global oil companies despite favorable financial metrics.

Over the past few months, I have been one of the few Seeking Alpha analysts who have maintained a bearish outlook on Petrobras ( PBR ) ( PBR.A ) due to various sources of political risks. However, this pessimism has not been validated on the stock as Petrobras continues to perform exceptionally well, even after experiencing a significant increase in value over the last 24 to 36 months.

My initial pessimistic stance was primarily rooted in concerns about shareholder control and the potential impact of government decisions on Petrobras, especially given the company's historical context. Legislative changes, such as the injunction that reduced government control over state-owned companies, could have substantial implications. It's worth noting that Petrobras' current CEO is a former politician from the same party as Brazil's current president, Lula.

One of the fundamental questions for the long term revolves around the behavior of oil prices in the coming years, as this factor plays a pivotal role in Petrobras' performance. To mitigate volatility, there might be a possibility of implementing price restrictions on gasoline and diesel, as has occurred in the past. Since March of this year, Petrobras has shifted away from the IPP (International Parity Price) policy, wherein it no longer closely follows the Brent price and instead operates with a lag in response to international prices.

In light of these factors, my outlook remains cautiously pessimistic. It's crucial to closely monitor future developments and their potential impacts on Petrobras and the broader oil industry. Uncertainty is an inherent aspect of this scenario, and observing how the situation unfolds in the coming years will be intriguing. Brazil's history with past left-wing governments, especially during Dilma Rousseff's administration, has led to long-term value erosion for Petrobras.

While it's still too early to make definitive predictions, I believe it's highly improbable that the company will thrive under a management that repeats the same mistakes as those made in the past, which clearly had a detrimental impact on its value.

The Significance of Oil in the Brazilian Economy

The significance of oil to the Brazilian economy is a topic that deserves careful consideration, in my opinion. The true nature of this resource is often misconstrued. Oil has served as the primary energy source throughout the past century and continues to hold that position. Despite the growing shift towards renewable energy sources, oil remains indispensable and is unlikely to become obsolete shortly.

However, owing to Petrobras being a state-owned company, there exists a misconception that the oil it extracts exclusively belongs to "the state." This misconception stems from a historical slogan in Brazil. Such beliefs lead people to expect low gasoline prices, complicating Petrobras' management and government decision-making. Society must grasp that while oil is indeed a valuable resource, it is not the sole property of Brazil, and international factors influence its price.

Oil and natural gas constitute the primary sources of revenue for the National Treasury, and this trend is expected to continue for many years. Oil plays an integral role in Brazil's trade balance, and its production is rising. In 2022, $42.6 billion of crude oil was shipped, representing 13% of total Brazilian exports, a share only one percentage point behind soybeans. Exploring new areas like the Equatorial Basin is imperative to maintain high production levels. Oil is critical in the economies of various nations globally, including Russia, where it remains vital even during conflict.

The Brazilian government often fails to comprehend the economic significance of oil and tends to focus primarily on fuel price-related issues. People need to recognize that oil is both lucrative and pivotal to the economy, and they must understand its relevance in the context of the global economy.

Petrobras' Reliance on Fortuitous Factors

Petrobras has delivered positive results thanks to effective management in recent years, particularly during the presidencies of Michel Temer and Jair Bolsonaro. This has proven advantageous not only for Petrobras' shareholders but also for the Brazilian economy.

The current government, led by President Lula, experienced some luck concerning the price of the oil barrel. From January until July, the price fell to approximately $70 to $73 per barrel, enabling Petrobras to lower gasoline and diesel prices. However, starting in July, prices increased again, surpassing $90.

Fortunately, once again, the exchange rate between the Brazilian real and the U.S. dollar declined, offsetting one factor against the other. Petrobras still operates with some delays in price adjustments, but these favorable factors have contributed to its stock performance.

Now, shifting to the diesel issue, the Russian war has significantly impacted the diesel market due to sanctions imposed on Russia. These sanctions have led Russia to sell diesel at a much lower price than domestic diesel. Approximately 80% of Brazil's diesel imports come from Russia, which has been beneficial. However, I have concerns about Petrobras' future.

There was a period when Petrobras encountered significant difficulties, particularly during the transition of government leadership from President Dilma's departure to President Temer's assumption of office in 2016. The company faced a challenging situation, even holding the world's highest debtor title. Additionally, Petrobras faced at the time complications due to an unfavorable exchange rate between the Brazilian real and the U.S. dollar, which stood at R$4.

Petrobras' recovery from 2016 has relied on implementing a development plan, cost reduction, and capital management. However, these measures appear to have been neglected recently, which raises concerns for me. I am concerned about the possibility of Petrobras investing in unprofitable refineries or oil fields. Additionally, there are questions surrounding Petrobras' pricing policy. The company discontinued its Import Parity Prices policy (IPP) in May and introduced a new pricing policy that is not entirely clear.

As Brent crude oil prices have been climbing since July, Petrobras reached a nearly 30% lag on fuels under the new pricing policy, which recently compelled the company to raise fuel prices in the country. However, the discount persists, with Brent crude oil continuing its upward trend.

By the end of September, the prices set at Petrobras refineries currently show a 13.6% discount on diesel and a 2.3% premium on gasoline compared to the international market price parity. This marks a change from the previous week when diesel and petrol had discounts of 13.6% and 5.5%, respectively, compared to international prices.

The premium on gasoline is due to Petrobras' price increase, which coincided with decreases in prices at international fuel hubs. This increase was partially offset by strengthening the U.S. dollar during the week, which rose 1.4%. Diesel prices remained relatively stable over the week.

Concerns About Petrobras Investment Policy

Petrobras needs a clear investment plan, but it seems this is currently on hold under the new management.

Petrobras has announced a possible investment in offshore wind energy. Firstly, Brazil lacks regulations for offshore wind energy investments. This means that the company is subject to congressional approval, which can be uncertain due to the lack of a clear government majority. In addition, over the last 20 years, Petrobras has accumulated a series of destructive projects, such as Pasadena, Abreu e Lima, and others, resulting in significant losses.

In my analysis, Petrobras should focus on its core activities, such as deepwater oil production, rather than venturing into new projects. Resources are scarce, and investing in offshore wind energy may not be the smartest choice. Another point to consider is the energy transition. Brazil already has a clean energy matrix, emphasizing hydroelectric power. Investing in offshore wind energy may not be necessary since the country has already made its energy transition.

The idea of exporting energy is also questionable, as it would require investments in transmission infrastructure to export energy to Europe and the US, which is not feasible now. Data show that offshore energy production is one of the most expensive and least efficient. Therefore, investing in something that spends a lot and produces little doesn't seem wise. Also, many concerns exist, from the lack of regulation to allocating scarce resources.

Parallel to this, Petrobras recently reported that its board of directors had approved a new dividend policy , reducing the free cash flow distributed to shareholders from 60% to 45%.

The company's investment cash flow for the upcoming years is still uncertain. Petrobras has not yet released its investment plan, which is expected to be disclosed along with the strategic plan 2024 and beyond in the coming months.

Over the last five years, Petrobras achieved an average operating cash generation of approximately R$ 160 billion annually, while the average cash flow from investments was R$ 40 billion. Half this amount was allocated to maintaining operations, while the other half went to growth and new business lines (approximately R$ 20 billion each).

Oil Price Trends for the Year Ahead

I believe it's crucial not to attempt to predict the future with absolute certainty but rather to engage in analysis. We are witnessing higher oil prices in the second half of the year, although they are not as high as they could be, primarily due to factors like China's slower growth. Oil plays a pivotal role in the economy, as energy catalyzes economic growth. Completely forsaking fossil fuels, especially when oil consumption is expected to rise in the coming years, and supply remains limited, is not a viable option.

Moreover, there are two major players in oil production, namely Saudi Arabia and Russia. Brazil needs to expedite its oil production to capitalize on the growing demand and avoid overreliance on these major players. However, it's essential to acknowledge the environmental discourse. Countries like the UK are enacting legislation to phase out the use of fossil fuels. Nevertheless, Brazil should not follow a contradictory path by importing liquefied natural gas from the United States while financing a gas pipeline from Argentina instead of developing its production.

Carbon capture technology is advancing and could contribute to mitigating the environmental impact of fossil fuel production. The challenge lies in finding ways to use fossil fuels more cleanly while simultaneously promoting the utilization of renewable energies. Renewable energy sources are becoming increasingly accessible and efficient, but it's essential to recognize that oil will remain a significant energy source in the foreseeable future.

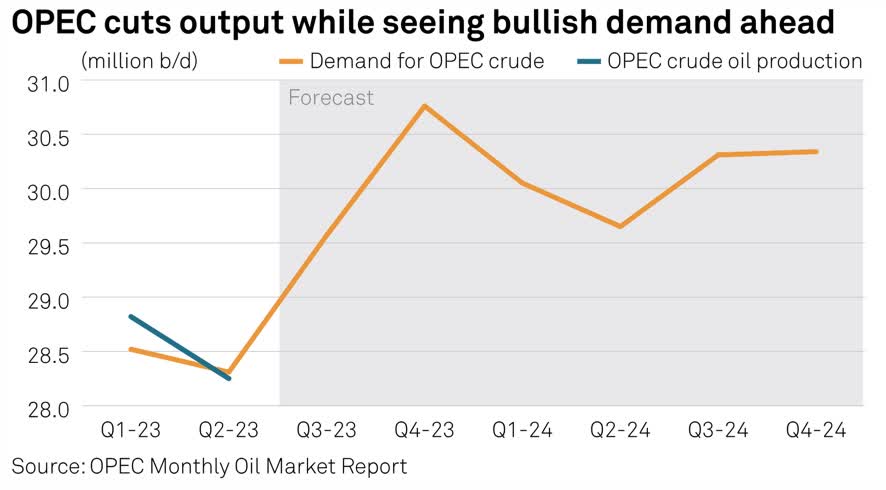

While OPEC anticipates a strong demand for oil in 2024, traders have shifted their concerns from under-supply to potential oversupply due to the structure of the global benchmark Brent futures contracts. This shift comes as expectations of weak economic growth outweigh Saudi Arabia's output cuts.

As a result, I believe it is unlikely that oil will experience a sharp drop to very low prices, such as $30 or $40, in the coming years. Oil will continue to play a significant role in the global energy landscape.

{kind=link}

Limited Ability to Quantify Political Risk in Valuation

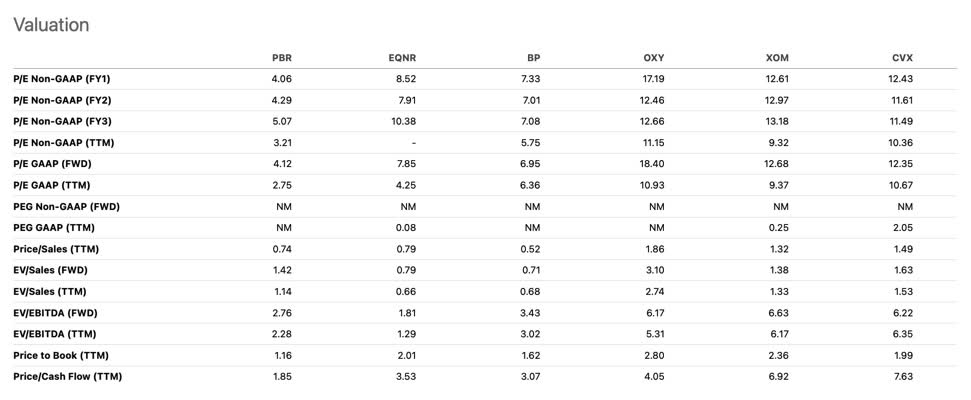

Petrobras continues to trade at exceptionally low valuation multiples compared to other global and domestic private oil companies, with a P/E ratio 4x versus the sector average of 10x. However, it's essential to clarify that this 60% discount is primarily due to the significant political risk associated with the company.

Furthermore, when considering the forward EV/EBITDA, Petrobras trades at a premium compared to Norwegian state-owned Equinor ASA ( EQNR ), and political risks influence both companies' valuations.

{kind=link}

Political risk cannot be quantified as it hinges on government decisions that can swiftly and dramatically impact the company's stock, eroding investor confidence. Petrobras has changed its CEO 17 times in the last 30 years, starkly contrasting privately-owned oil companies.

At current price levels, Petrobras is trading at 2.8x forward 2024 EV/EBITDA, with a 20% cash flow yield for 2024. These levels may appear attractive but do not account for the risks associated with potentially harmful investments or unwise acquisitions. Additionally, there is pressure on refining margins compared to well-managed private peers with successful track records.

Furthermore, recent measures, such as curtailing international parity and reinitiating investments in non-core initiatives, have raised additional concerns. Frequent changes in shareholders and presidents, often driven by political pressure and fuel price concerns, should not affect Petrobras' management.

Satisfying Petrobras' shareholders also equates to serving the broader society, as all Brazilians are indirect stakeholders in the company. Petrobras generates dividends, which the government can allocate to investments in critical areas like education, healthcare, or national debt reduction.

However, the generous dividends distributed last year are expected to diminish. The forecast for 2024 and beyond is regressive due to the implementation of the new dividend policy and potential challenges stemming from price gaps and investments in non-core businesses.

{kind=link}

Conclusion

It's crucial to acknowledge that Petrobras is profoundly influenced by the international market, with oil prices playing a pivotal role. If oil prices surge, it will present a substantial challenge for the company. Nevertheless, I believe Petrobras can rebound by taking the appropriate measures. Ideally, the company should acknowledge its past mistakes and rectify them. However, the abandonment of development strategies and an uncertain pricing policy are sources of concern.

I do not see the current government making the optimal decisions for Petrobras, and there remain numerous uncertainties about the company's future. The energy transition is also crucial, but oil remains significant in the Brazilian economy.

Petrobras' stock seemed to have encountered a resistance of around $15 per share in mid-September, relying on favorable conditions, including lower Brent crude oil prices in the year's first half. Even as oil prices rose since July, the foreign exchange rate variation favored Petrobras, which I view as primarily the outcome of fortunate circumstances rather than reflecting the company's improved fundamentals.

Considering that at the beginning of the year, amid political uncertainties becoming more evident in the market, Petrobras was stuck in limbo, struggling to break the $12 support until May. And that's where I predict the stock is heading, especially as more discouraging news continues to emerge, with the company trading at a forward P/B that is 17% above its historical average. Consequently, I maintain a bearish outlook on Petrobras for the long term.

For further details see:

Petrobras: A Return To Bearish Ground As History Comes Full Circle