EQNR - Petrobras: Very Cheap Highly Profitable And Returning 17.6%

2023-07-29 01:49:26 ET

Summary

- Petrobras is undervalued, trading at only 2.3x FCF, due to its political past and government entanglements.

- Despite this, the company has been generating impressive profits and is likely to continue doing so.

- Selling put options on Petrobras stock is the best way to get involved in the company, either building a position at a better price, or earning solid cash-on-cash returns.

Petrobras (PBR), the renowned Brazilian oil company, stands as a prominent firm in the global energy market that continues to pump out profits, quarter after quarter.

Despite PBR's robust market presence and impressive track record of generating free cash flow, the company currently appears undervalued, trading at only 2.3x FCF. Normally, we would argue that this is a market oversight that should mean-revert, however due to the firm's sordid political past and government entanglements, we think the discount is warranted.

That said, it doesn't mean that the stock is a bad investment. PBR has taken full advantage of the recent energy boom, producing staggering TTM profits of $36 billion, on a revenue base of $124 billion. While the company doesn't consistently pay dividends, it seems likely that continued profits will find their way back to shareholders.

With earnings coming up, we think that selling puts on PBR stock is the best way to get involved in the company. By employing this option strategy, traders either stand to earn a hefty cash-on-cash premium, or acquire shares at even more attractive price.

Let's dive in.

Financial Results

As we just mentioned, PBR's recent financial results have been excellent.

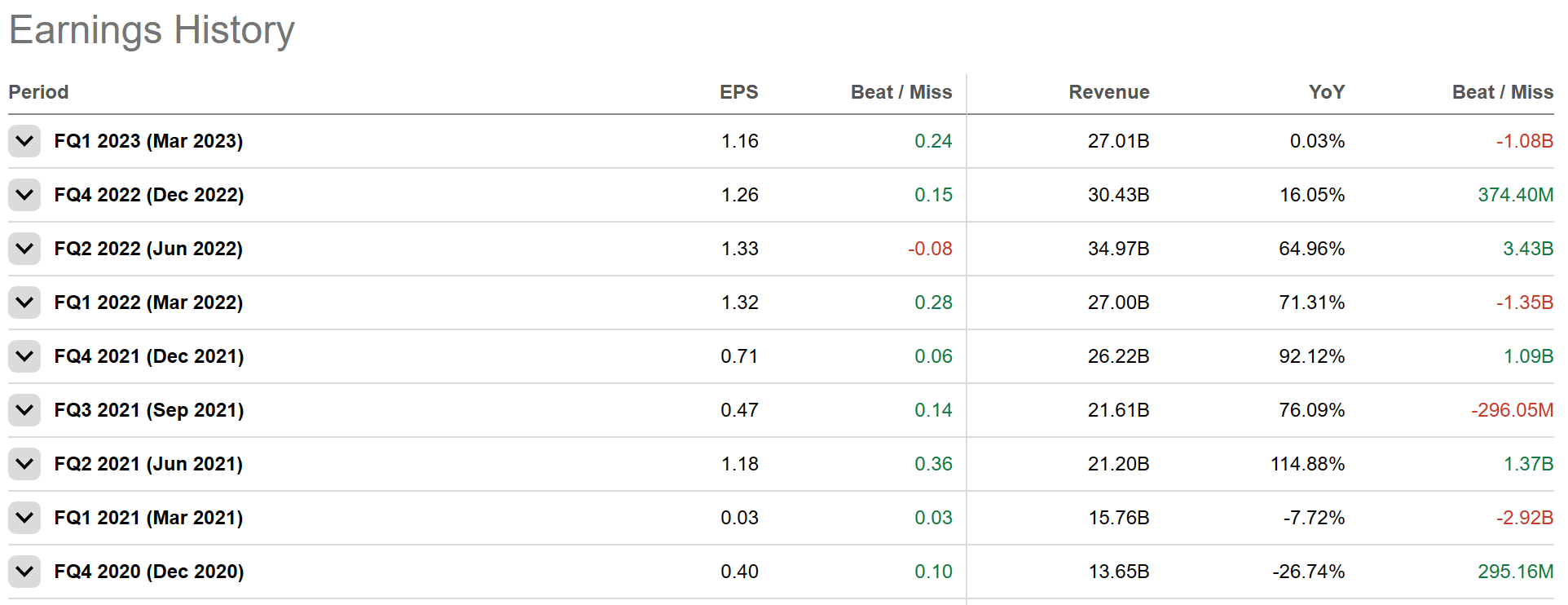

In the company's most recent quarter (now almost three months ago), PBR reported EPS of 1.16, which reflected a beat of more than 0.24 cents per share. Given that the stock is currently trading close to ~$14, the 0.24c surprise actually had an impact on the company's baseline multiple.

This kind of performance has been relatively consistent as well. Revenue beats have been a little spotty, but the company has continued to outperform on EPS, while growing the top line considerably since the 2020 lows:

{kind=link}

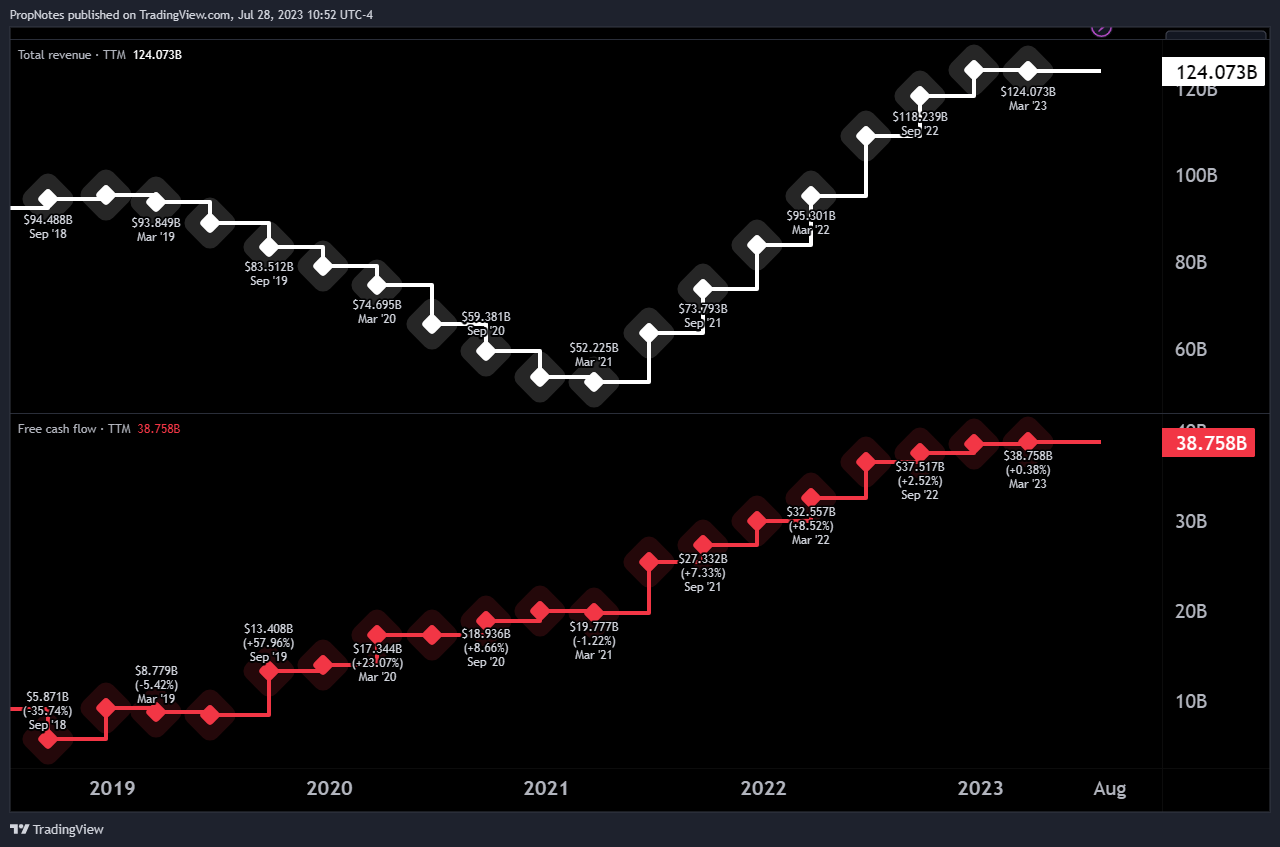

Zooming out, the FCF growth is what has our attention.

Revenue has ebbed and flowed along with the global energy market, but FCF has grown like clockwork, increasing from one TTM period to the next:

{kind=link}

This growth has recently flatlined along with the market, as supply has fully come back online following Covid, and demand has tapered somewhat given the pricing environment.

That said, we expect things to continue to improve slowly now that the market has stabilized.

PBR's Monopolistic Position

PBR has been able to earn these kinds of profits as a result of its efficient drilling and refining operations.

As remarked by fellow Seeking Alpha Author Jordan Sauer in his recent article , PBR has an extremely low per-unit cost of production:

In commodity businesses, where there is no product differentiation, the key moat is being the low-cost producer. Enter Petrobras, which owns some of the world's best offshore oil assets. Petrobras extracts pre-salt oil at a very low cost . The company's chief exploration and production officer, Fernando Borges recently said:

"Breakeven is nearly US $20 per barrel ."

This gives the company a huge cost moat over global peers.

This cost strength is complemented by extensive reserves and a nearly monopolistic network of refineries, pipelines, and more. This allows the company to set prices and unfairly compete with smaller players in the region.

Doesn't investing wisdom say that we should be looking to invest in monopolistic businesses?

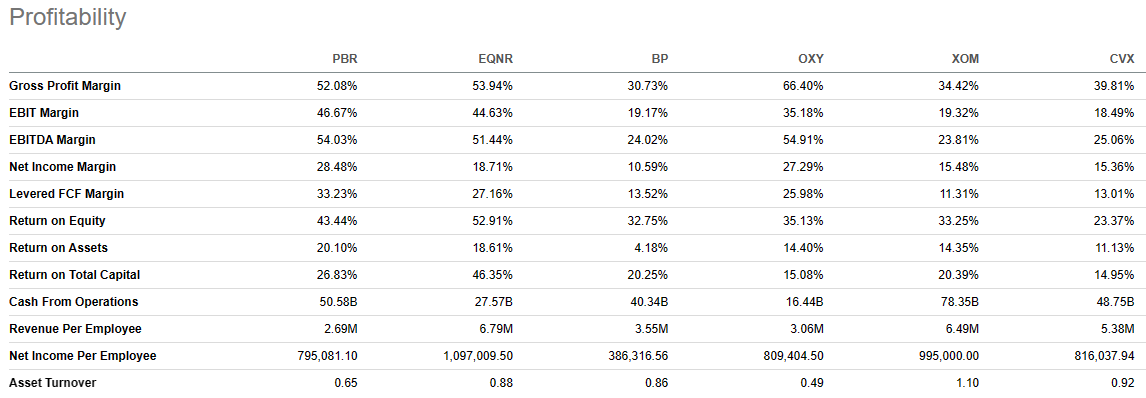

These competitive advantages show up in the company's profitability profile, especially when compared with global peers:

{kind=link}

When compared with Equinor ( EQNR ), BP ( BP ), Occidental ( OXY ), Exxon ( XOM ), and Chevron ( CVX ), Petrobras actually scores the highest marks in almost lots of categories.

PBR remains the most profitable in terms of EBIT margin, Net Income margin, Levered FCF margin and Return on Assets.

It also scores second place in a number of other metrics.

Clearly, having a stranglehold on a nation's energy infrastructure has its perks.

The Valuation

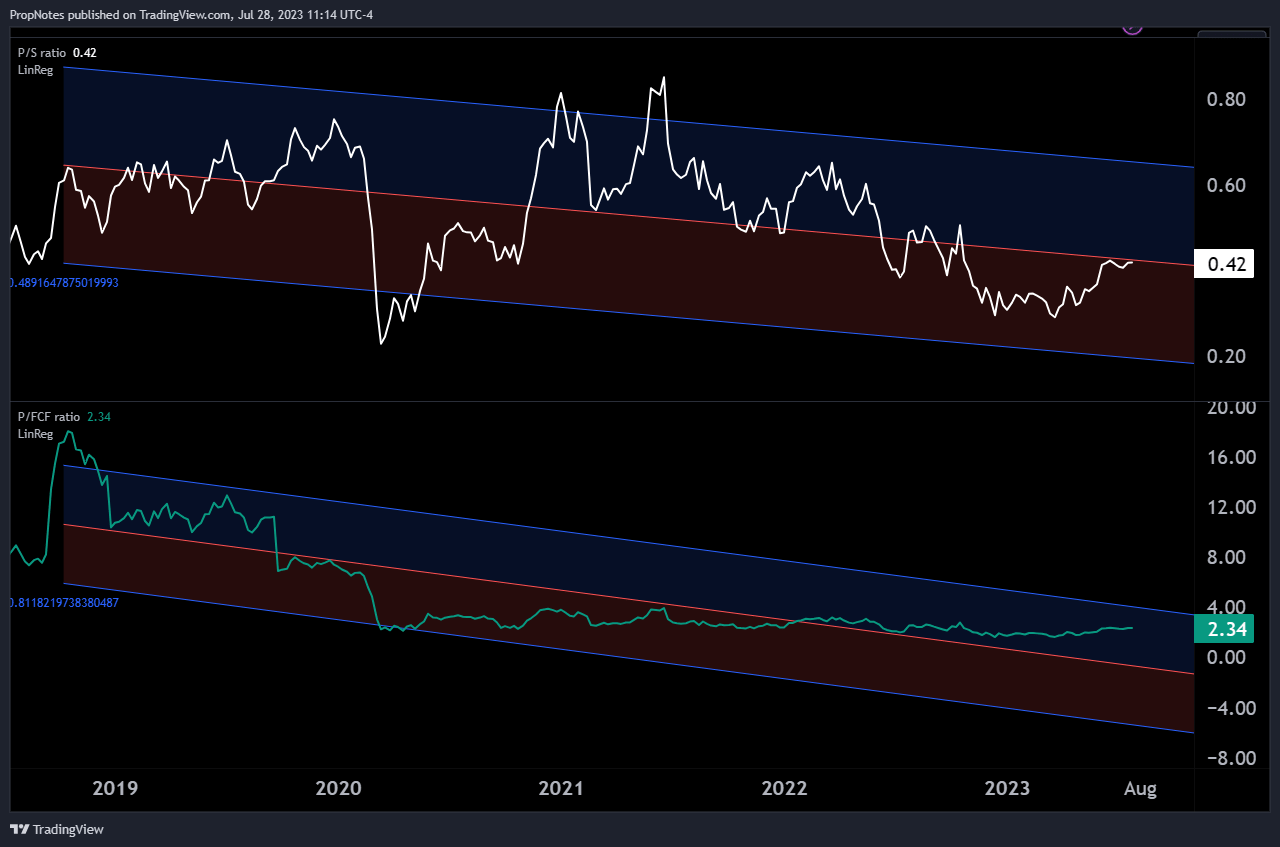

However, as we alluded to earlier, the company remains very cheaply valued, trading at only 0.4x sales and 2.3x FCF:

{kind=link}

While some of this discount (relative to peers) is due to the fact that a majority of the company's business is done in a 'developing' country, the much larger issue is that of politics.

As many may know, PBR is partially owned by the Brazilian government, which recently saw a liberal administration elected with Lula da Silva at its helm. This compares with a more conservative Bolsonaro government, which is what existed previously.

The main fear among investors now is that profits will shrink as a result of the new government, which has less interest in market capitalism and more interest in lower prices for constituents and green tech investments that benefit the country as a whole.

This should, in theory, weigh on profits, thereby reducing potential shareholder returns.

However, we don't see this as an existential risk. While Lula's government sees PBR as an instrument of national transformation, the company will still retain all of its assets, including many of its cost advantages.

Thus, even if things get worse, a majority of potential risk is currently baked into the stock price.

The Trade

PBR remains cheap and profitable; two things that are likely to persist for the foreseeable future.

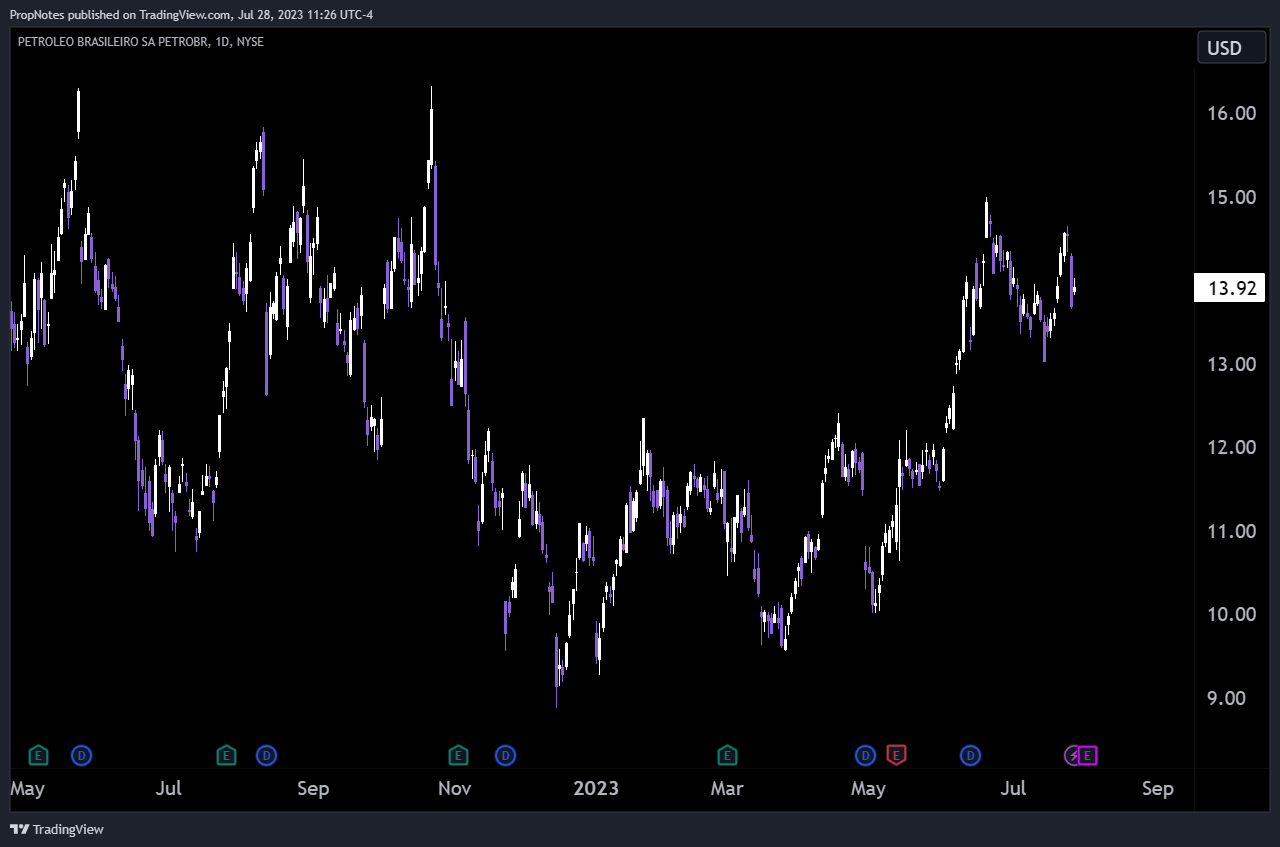

The company's stock also remains highly stable, typically range bound between $9.50 and $15:

{kind=link}

Thus, getting involved in the stock seems like a solid idea due to the potential for steady dividends and appreciation, but the price remains a bit elevated for our taste, at the higher end of the range near ~$14 per share.

This is where selling puts comes in.

When you sell a put, you're agreeing to purchase shares in a company at a pre-agreed price, if the stock price finishes beneath the pre-agreed price when the put expires.

In return for taking this risk, put sellers are paid a cash premium.

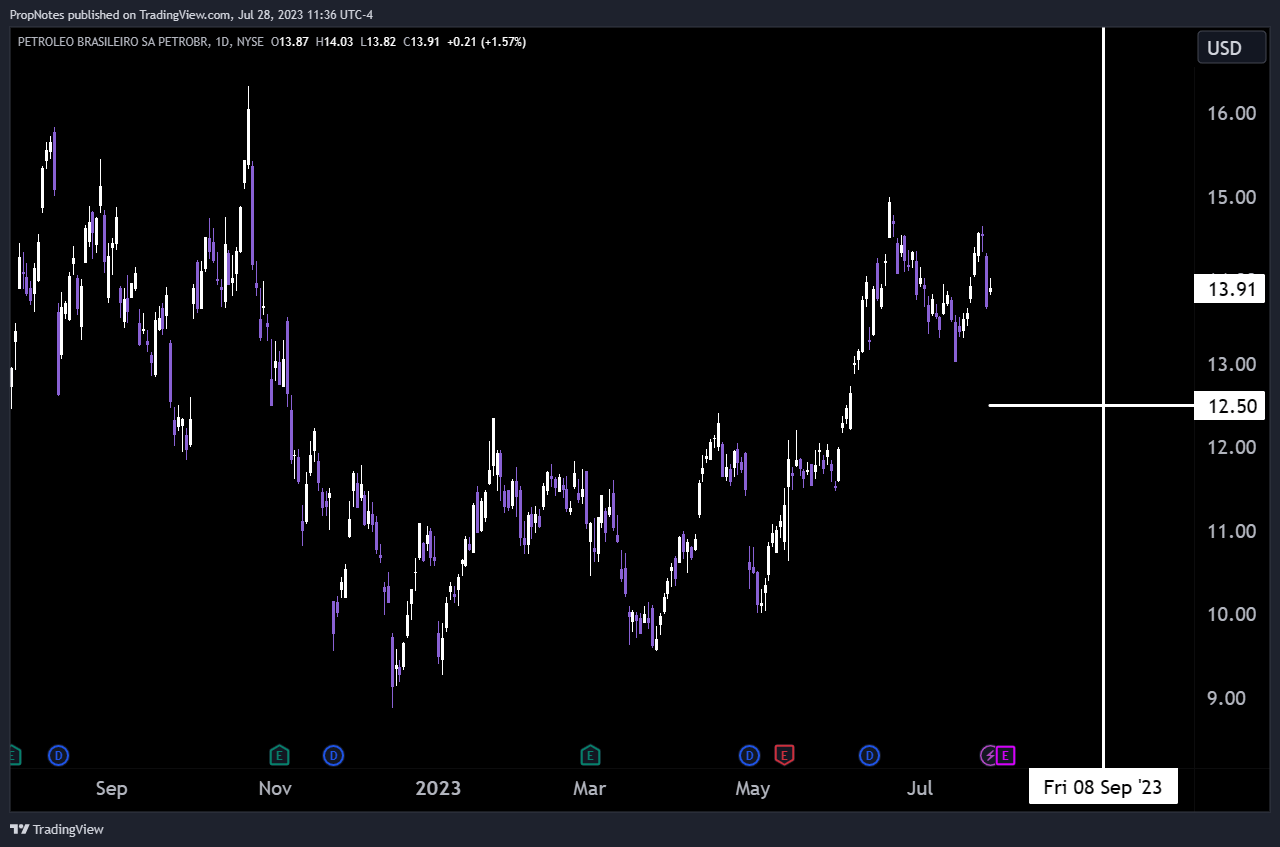

In this case, we really like the idea of selling the September 8th, $12.5 strike put options:

{kind=link}

With these options, put sellers would receive a $25 premium per contract, which translates to a 2.04% return over the next 42 days. This annualizes to 17.6%.

The breakeven point for this trade is -12% below the current market price, which is a handy margin of error given the upcoming earnings report.

Finally, if assigned on the position, then put sellers would be acquiring shares in a solid, profitable, steady global energy player that we think is strongly positioned to provide dividends and returns well into the future.

Risks

There are a few risks with this trade, the main one being increased politicization of the company. While infrastructure development may prove to be a tolerable risk (and even ultimately profitable to shareholders!), if the company is forced to refine at a loss, as some have speculated, then the stock would likely suffer heavy losses or serious impairment. Other scenarios include tightened price caps or other environmental regulations which could stifle Capex or profit.

Otherwise, the global energy market may weaken, which would likely affect revenue and free cash flow. This could halt the generous dividend payments the company has been pumping out as of late.

Additionally, the aforementioned earnings report could cause losses if the stock gets crushed and put sellers are forced to buy stock at a price higher than the market.

Finally, currency risk remains an issue, with the company suffering billions and billions in losses per year in order to pay out USD returns to shareholders. If the exchange rate for the Brazilian Real continues to deteriorate, then that could begin to weigh on net income attributable to common stockholders.

Summary

All in all, Petrobras is a cheap, profitable company with a steady stock price and solid capital return potential.

We think that selling puts on this company to earn cash-on-cash returns is a great opportunity to begin earning solid yield and potentially begin building a position.

A win-win!

For further details see:

Petrobras: Very Cheap, Highly Profitable, And Returning 17.6%