PEYUF - Peyto: Conservative Transition

2023-07-03 10:27:11 ET

Summary

- Peyto Exploration & Development Corp. is slowly adding rich gas production to its traditional dry gas production business.

- The main business strategy is to keep the dry gas costs where possible while adding the additional value of rich gas production and sales.

- The margin goal for the current year is one of the better results in several years.

- Management will continue to decrease costs to maintain cost leadership.

- The cyclical growth story is set to resume in more normal industry conditions.

(Note: This article was in the newsletter on June 18, 2023, and is updated as needed. Note: This is a Canadian company that reports using Canadian dollars unless otherwise noted.)

Peyto Exploration & Development Corp. ( OTCPK:PEYUF ) remains essentially a dry gas producer that is slowly adding some rich gas production in case the last few years of relentless gas price downtrends ever repeat in the future. Rich gas gives a company more than one way to achieve decent profitability depending upon industry conditions of course. This management has long relied upon low costs to achieve decent profitability. But the last few years have convinced management to form a "Plan B."

The tight controls on costs continue. The implicit goal is to maintain the dry gas costs when possible while adding the extra value of rich natural gas production. In the process of doing this, it should increase corporate profitability of the company throughout the business cycle.

This is a company that generally does not do things without tangible results. Therefore, investors should not expect a fast transition from what has been the company's "bread and butter" for much of its history. Instead, this company will likely attempt to transition to more ways to profit through the addition of more liquids as a percentage of production.

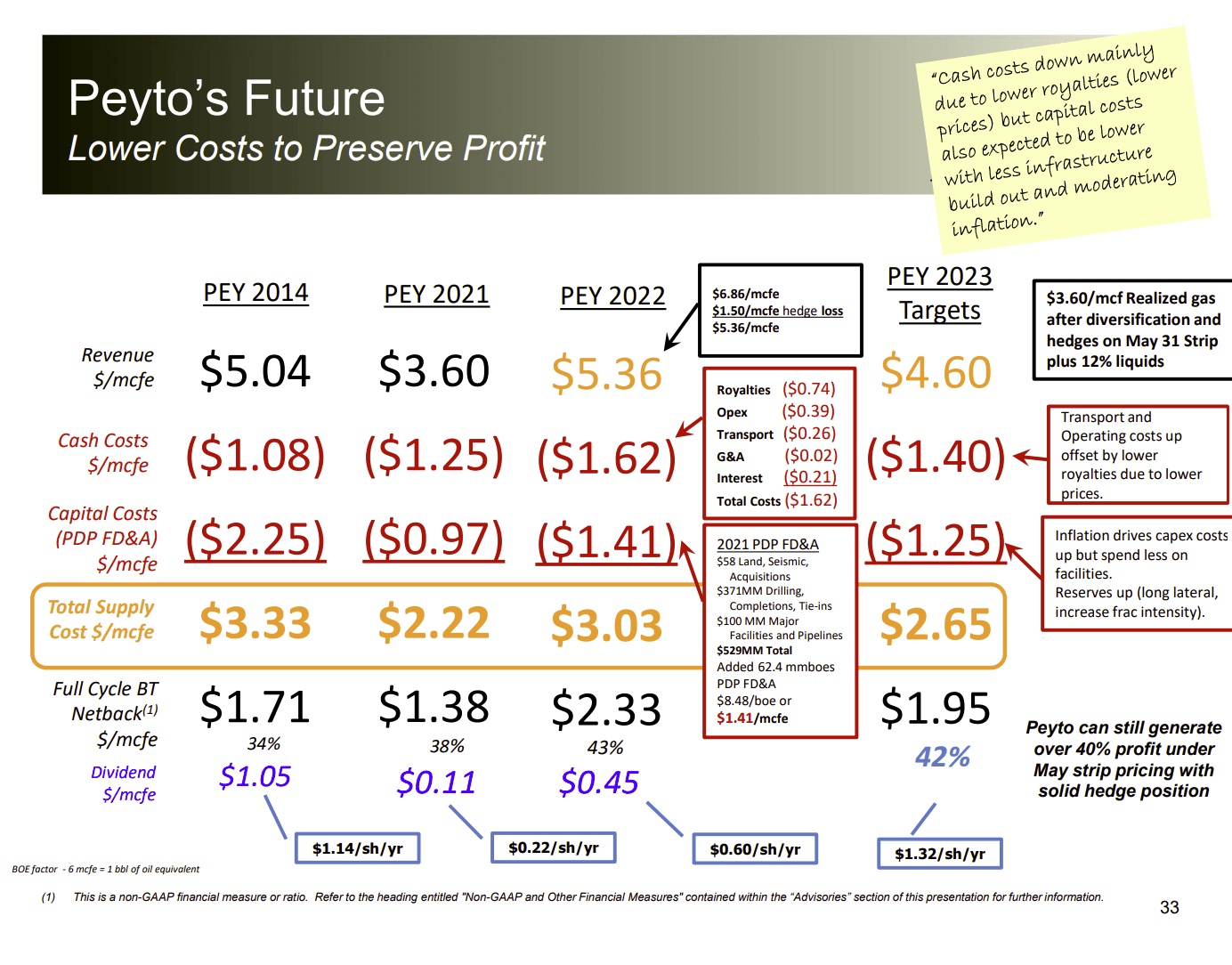

Peyto Sales And Cost Guidance For The Fiscal Year (Peyto AGM Meeting Presentation June 2023)

{kind=link}

Cost reduction emphasis has long been a hallmark of this company through the fiscal years. As can be seen above, despite an average sales price that barely exceeded the 2014 results, this management has widened the netback considerably over the years.

That widened netback happened despite the acquisition of several small deals. This management rarely purchases other companies or parts of companies. So, the acquisitions are a huge vote that selling prices are historically low.

This coming year, a lack of projected acquisitions should cause Capital costs to drop as shown above. But, management appears to be still on the prowl for accretive acquisitions.

Cash costs will drop primarily from lower prices. But management will again likely find ways to drop operating costs as they have in the past. The margin in the past fiscal year was exceptional, and this management knows that costs must continue to drop to keep that margin in the exceptional range.

Management has enough faith in the future to begin to bring the dividend back to levels not seen in some years. Canadian companies will adjust the dividend faster than American companies. Peyto is no exception to that general rule. On the other hand, the higher dividend suggests a brighter future than the market gives the company credit for.

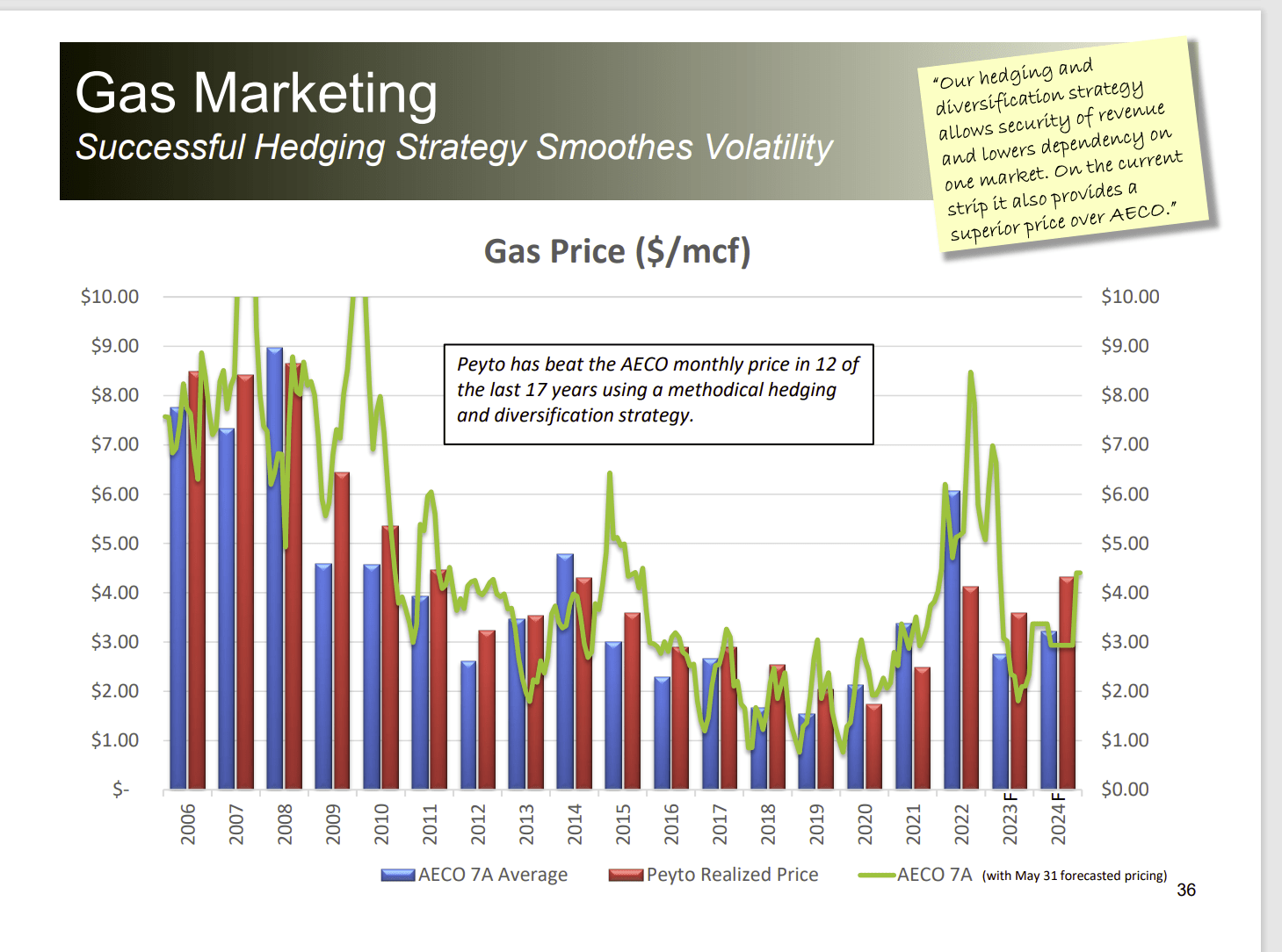

Peyto Realized Profitable Pricing Results From Hedging (Peyto AGM Presentation June 2023)

{kind=link}

Peyto generally realizes a significant profit from its hedging operations. Usually, the market does not price in hedging regardless of the results. Profitable hedging operations are generally too rare for the market to care about and properly value. But that means more dividends and share repurchases for shareholders at any commodity price level than is the case for many competitors in the industry.

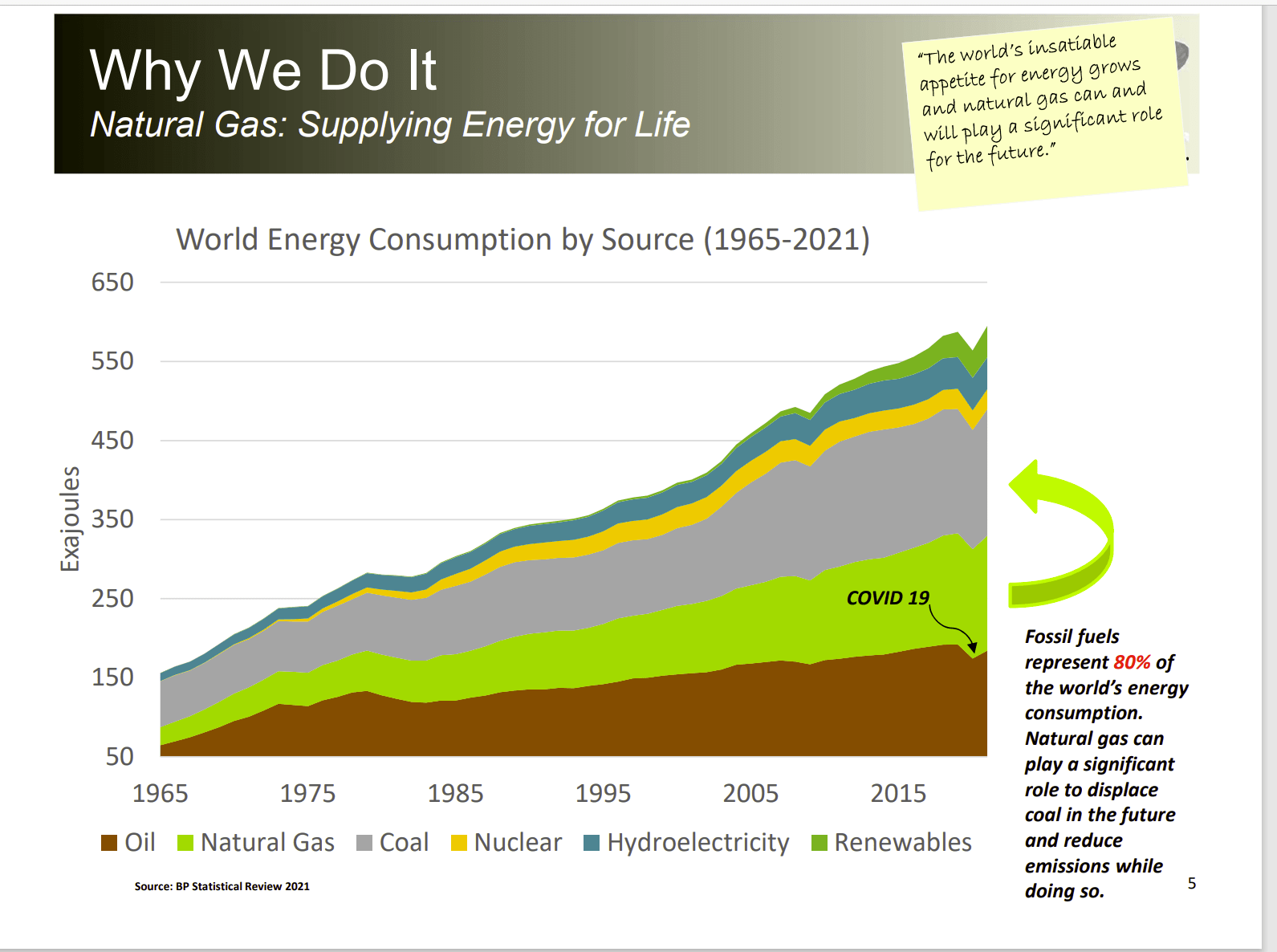

Peyto Presentation Of Fossil Fuels Use And Projected Growth (Peyto AGM Presentation June 2023)

{kind=link}

The fact is that the renewables industry has a very small part of total energy production. Despite a lot of pronouncements to the contrary, that low share of energy production is projected to continue for some time to come. There just is not the supporting infrastructure needed to support a fast conversion to renewable energy sources.

Instead, it appears that natural gas will continue to displace coal as an energy source for some time to come. This is a natural transition to lower emissions because natural gas has a considerable emissions advantage over coal. It appears to be the logical next step until other more favorable energy sources become available.

Cyclical Growth Story

Peyto has a growth story that is typical for the industry.

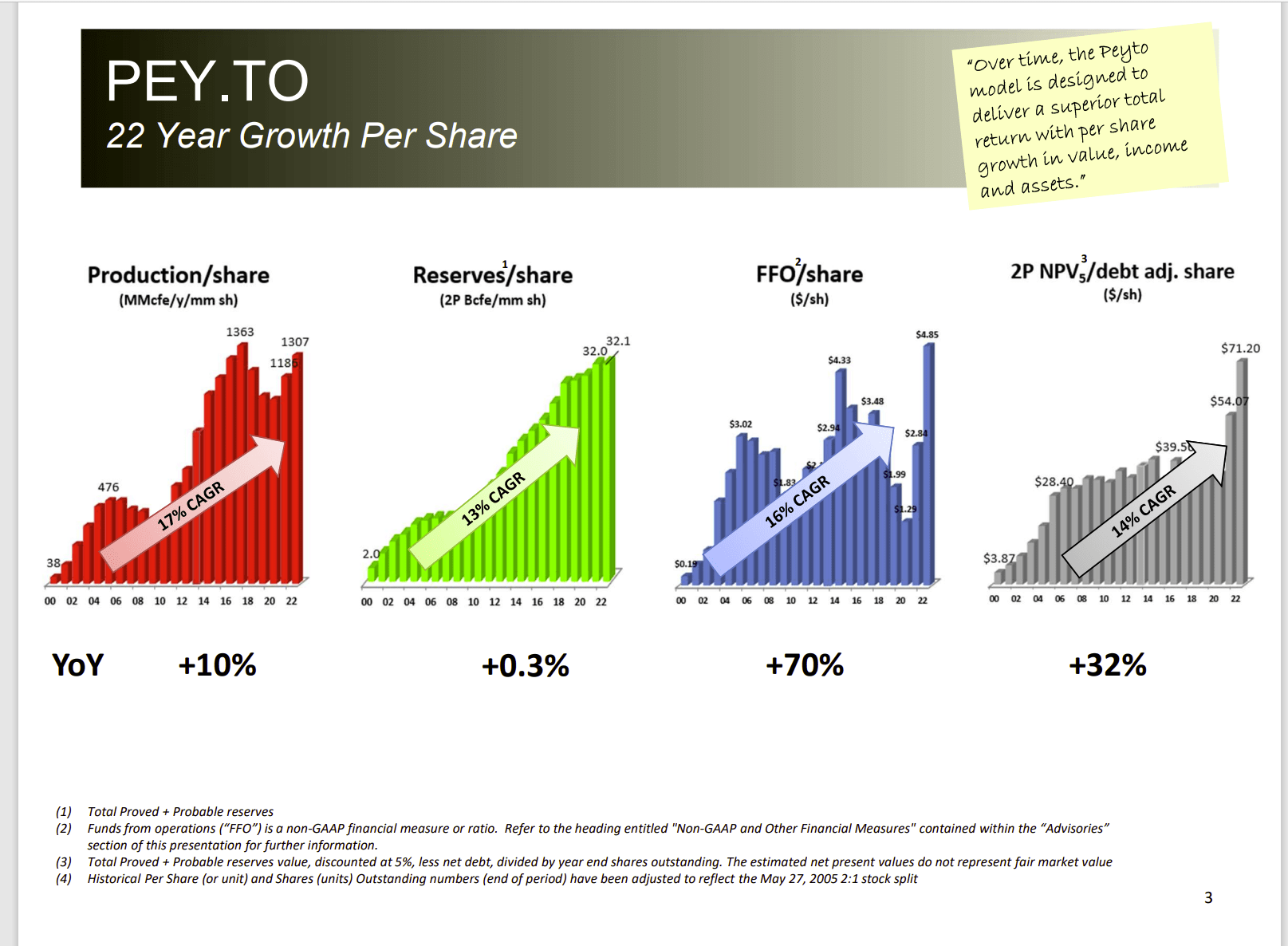

Peyto Historical Progress (Peyto AGM Presentation June 2023)

{kind=link}

Many growth stories ran into the "brick wall" of fiscal years 2015-2020 (give or take as natural gas started a downtrend that began earlier than oil). The boom times of the earlier decades came to an end as over-production became the order of the day.

Now the growth story of Peyto is set to resume under industry conditions that have not been this favorable for some time. Mr. Market, on the other hand, looks at the past and assumes it will repeat.

There will always be cyclical downturns. But the mad rush of inexperienced money into the industry appears to be over (at least for the time being). Therefore, the resumption of a normal growth cycle appears to be in the foreseeable future for the first time in a long time.

That implies that the stock has more upside potential than the downside potential the market is clearly worried about. The rising dividend indicates management's vision of the future is also at odds with the stock market.

Insiders are not always correct, and their market timing is often not the best. But they do get general directions for the long run correct more often than not. Therefore, their actions are worth paying attention to.

Key Ideas

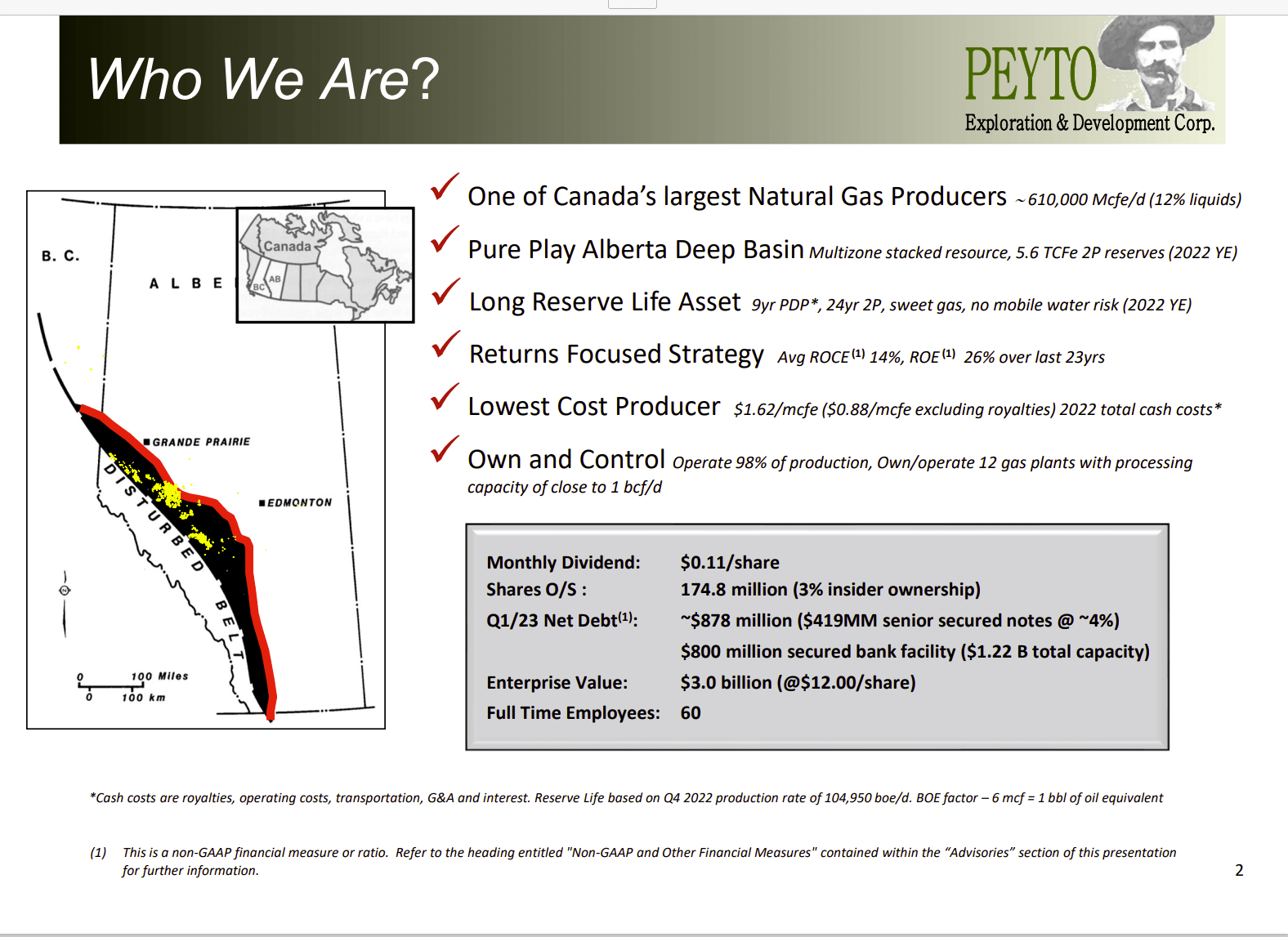

This Alberta, Canada, producer is one of the lowest-cost producers in North America.

Peyto Summary Of Company Operations (Peyto AGM Presentation June 2023)

{kind=link}

This management has integrated the company to a large extent to achieve that low-cost production. The company owns a lot of midstream assets to complement the primary upstream business.

During the downturn, there were some worries expressed about debt levels. Clearly, those worries were overdone considerably. Management has been repaying debt while growing production to allay some of those fears.

In the meantime, the rapidly growing dividend appears to be an expression of a much better future than Mr. Market appears to allow for. Mr. Market has priced a lot of unfavorable outcomes into the current price of the stock. This negative view should allow for a lot more upside potential than downside.

Management did update that so far the wildfires had a very minimal impact on production.

Natural gas still has a growth future regardless of the "green revolution." It is going to be a very long time before demand for natural gas does not grow. A company like this can be a consideration for those who can withstand a variable dividend as well as the volatility that is part of upstream common stocks. For those types of investors, Peyto Exploration & Development Corp. stock is probably a strong buy consideration as part of a well-chosen basket of stocks.

For further details see:

Peyto: Conservative Transition